I used to have a colleague that would giddily exclaim, “Down Goes Frazier!” anytime he was short a bond that flashed, “HIT” on the broker screens. Since he was pretty good at his job, it became so ubiquitous on the desk that it was easy to forget where it originated.

Those of us that grew up in the 90s remember George Foreman as a lovable middle aged man that made a living beating up mediocre boxers and selling indoor grilling equipment. But in the 70s, he was a total badass. Foreman pummelled the champ into virtual submission, knocking him down six times before the ref stopped the fight midway through the second round.

So that was the phrase that went through my head when I saw that negative NFP print. The unthinkable has come true….A seven year streak of positive prints is over.

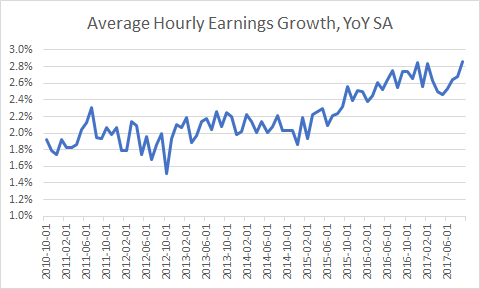

An awful number, even looking through the noise from the hurricane? Not by a long shot. UE continued lower, indicating there was no easing of labor market conditions. More importantly, average hourly earnings grew faster than expected, and continued a trend higher that has been intact since early this year.

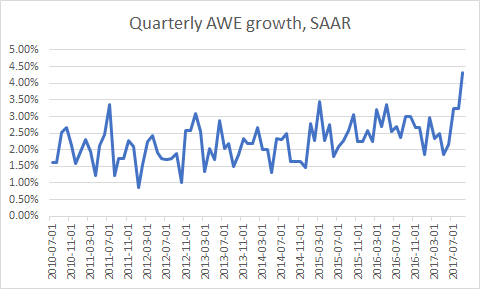

I’m always a little suspect of YoY numbers since they are by definition dependent on what happened a year ago--a look at annualized AHE over the last three months, seasonally adjusted paints a rather surprising picture:

.

Pretty clear picture there. Three periods of recent history--2010 to 2015, when wages bumbled around 2%....2015 to early 2017, when they bounced around 2.5%. Now one could reasonably infer wages are set to find a new range at or above 3%.

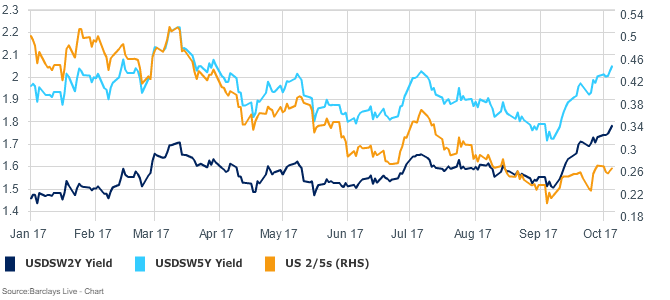

And yes, the Fed has hiked interest rates, and has the torpedoes armed and ready to deploy in December. Yet the curve remains amazingly flat--no doubt in part because of this year’s low headline inflation prints implying we may be near the end of the economic cycle. But with the recent prints in payrolls/wages and some good arguments for why headline CPI is understating financial conditions, seems like 2/5s should be a little closer to the steeps than the flats, when there is little evidence the Fed is going to waterboard the economic recovery with an aggressive hiking cycle.

And we all know what USD has done this year--until the past few weeks anyway.

Why does the curve refuse to steepen? This chart is from Kashkari’s diatribe last week. The FOMC’s most dovish voice says,

“I believe the most likely causes of persistently low inflation are additional domestic labor market slack and falling inflation expectations…..I will argue that the FOMC’s policy to remove monetary accommodation over the past few years is likely an important factor driving inflation expectations lower.”

I think the above evidence takes an ax to the first leg of Kashkari’s labor market argument. And the second? The clear implication is that the combination of tapering asset purchases, hiking rates, and eliminating SOMA re-investments (that is, reducing the balance sheet) has over-tightened monetary conditions.

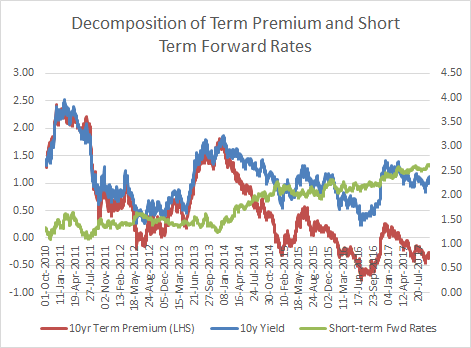

I think Kashkari has misidentified the source of lower inflation expectations. Market-implied inflation expectations fall by definition when there are buyers of nominal rate bonds relative to inflation linkers. Without kicking the hornet’s nest of term premium arguments, the NY Fed’s ACM term premium model shows a steady if unspectacular increase in short-term forward rates with the term premium still solidly in negative territory.

Source: New York Fed

The bottom line is that there is a ton of demand for assets relative to the marginal propensity to consume. Global investors want to buy more long-duration assets relative to the quantity being issued by either the government, or corporate borrowers, forcing down future returns. That doesn't foreshadow lower inflation. It illustrates easy financial conditions.

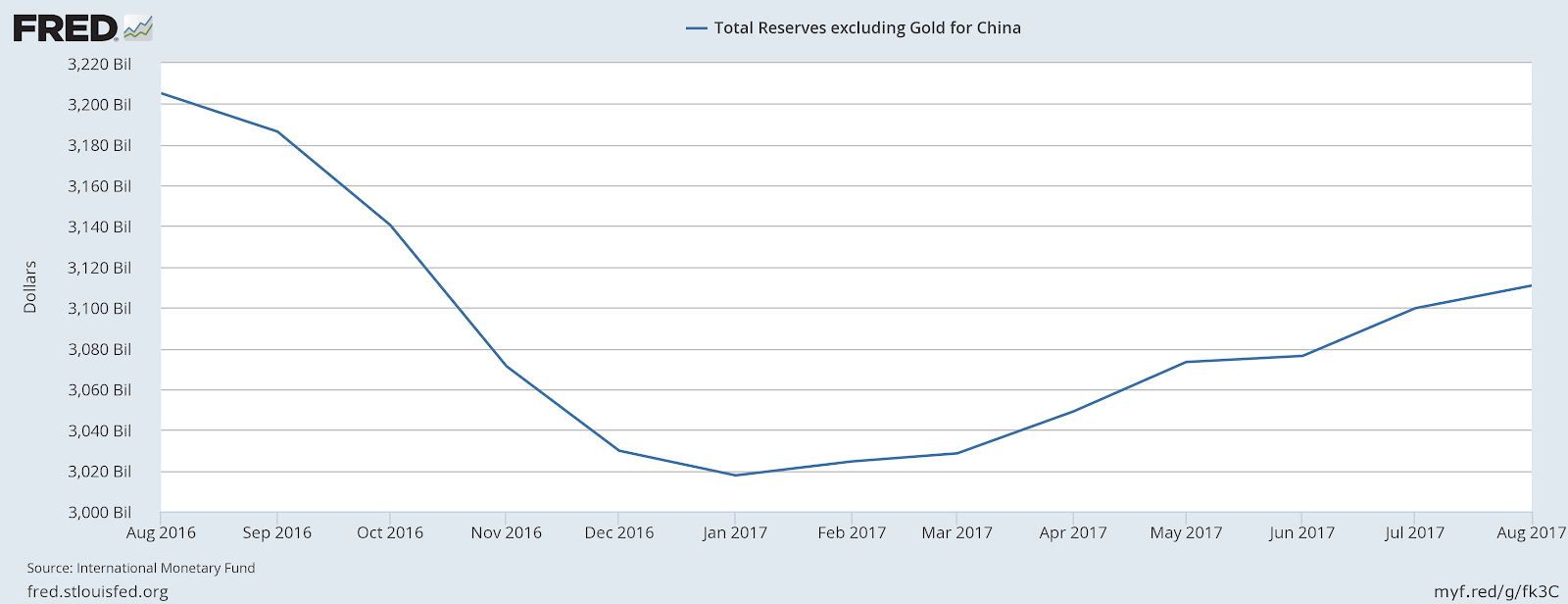

That demand for assets extends not only to foreign corporations and individuals, but also to central banks. Remember a year ago when smart people we saying there was a floor below which the PBOC’s foreign reserves could not sustainably fall? If it ever existed, it is nearly $100 billion in the rear-view mirror now.

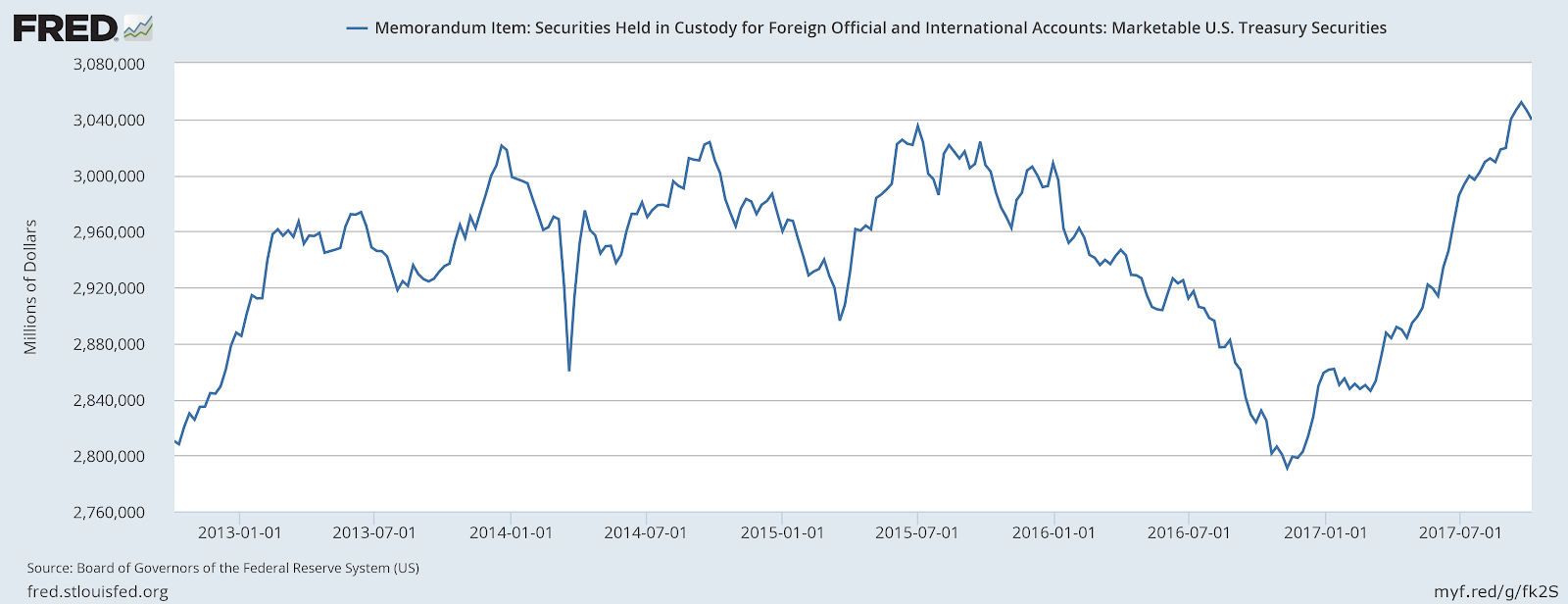

And the Chinese aren’t the only ones--the US current account deficit combined with resurgent manufacturing demand has put foreign central banks into overdrive to limit the appreciation of their domestic currencies. Foreign central banks have purchased roughly $200 billion of treasuries this year.

One might think that reflected a global interest in buying US Treasuries--but foreign private investors have added a modest $24 billion this year. Any chance that money is going into spread product???

Which brings us nicely back to this:

The Economist gives us about one of these per year. It just shouts out “contrary indicator”. Twitter practically had kittens.

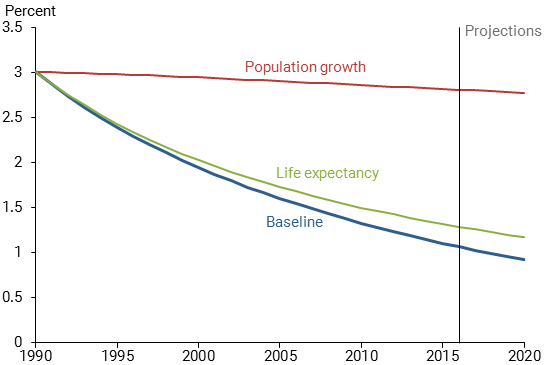

Take the time to read through the article, it’s actually pretty good. They go through a number of arguments for how we got here and what might happen next. Only one did I find rather dubious--the suggestion that we are near the endgame because there are more people in developed markets starting to retire, and as they burn off assets real interest rates will be forced to rise.

That ignores billions of people in emerging markets. Not only are they in a better demographic situation--they are living longer as their standard of living increases.

A recent paper by the San Francisco Fed shows that it is actually life expectancy rather than demographics that has driven real rates lower over the past thirty years.That means as people in EM countries increase their living standards, they are not only making more money, they are hoarding more of it in anticipation of living a long and fruitful life, which pushes global real interest rates lower. More on this subject later this week.

We can parse this market in practically any way we like--bemoaning the lust for cov-lite, sub-investment grade bonds, Argentine bonds with comically long times to maturity, levered short vol positions, or private equity, but at the end of the day there is a ton of money chasing assets, and not enough scary stuff happening in the world to convince them to change course.

History tells us these trends don’t end well. But we don’t know when the music stops. The Fed doesn’t want to be the villain that breaks the market--but there’s a ton of evidence I’ve noted here that argue financial conditions are too loose, and even by its own measures, core inflation isn’t telling the whole story. I just can’t get away from the memory of 2004-2006, when the fed hiked 25bps every meeting for three years and still armed the greatest financial weapon of mass destruction history has ever seen.

To the Fed Governors...I know you guys love your jobs but look at your own numbers...to borrow from Reagan…”Doctor Yellen, Steepen this Curve!”

Shawn

TeamMacroMan2@gmail.com

@EMInflationista

Shawn

TeamMacroMan2@gmail.com

@EMInflationista

19 comments

Click here for commentsTim Duy has a more appealing chart on the 3mo SAAR and a few eloquent thoughts on the same subject.

Replyhttp://economistsview.typepad.com/timduy/2017/10/on-track-for-a-december-rate-hike.html

Not to come over all "Ice Age" here at MM, but the inevitable conclusion of QE episodes is a flat curve and a lower long end, if only because such an immense amount of liquidity has been trapped during the years at or near the Zero Bound.

ReplyIt is going to get a lot flatter yet, Shawn, if we recapitulate the Japanese experience, in which "economic slowdowns/recessions" were associated - not with YC inversions - but by episodes of flattening that led to.... where we are today... Abenomics. There are reasons to believe that one of the primary drivers of US CPI, crude oil, has peaked and will drive inflation expectations lower.

Tom Duy's post is interesting, in a number of ways. The recent soft employment report sets up a "rebound" report in early November, that would give the Fed perfect cover for the ensuing Dec hike. Dame Janet likes December hikes, that's when they did their first one, remember? The Fed doesn't give a rat's ass about inflation, jobs or the rest of it, they are just going to hike.

As we now know the Dec hike is a sure thing, we can assume that it has been effectively priced into the long end of the Treasury market by fixed income participants, who are looking past the hike to a winter slowdown. The 2.40% level on US10y was bought aggressively last week, putting a floor under USTs and flashing a buy signal.

Lance Roberts, meanwhile, reviews the overbought environment for equities, and highlights some interesting second order effects in the economy. Lance is especially good at long-term charts and points out the declining ROC of a number of indices.

https://realinvestmentadvice.com/most-hated-bull-market-ever-10-06-17/

Long bonds and volatility here; short Spoos and small caps, which are under-performing today. Let's imagine a few things that "can't happen" - let's say Q3 earnings meet, or disappoint, Street expectations?; tax cut plans of the Bullshitter-in-Chief soon come to nothing, and political problems in Spain drive a flight to quality in global fixed income markets. Volatility spikes. Chad, Brad and Thad are forced to cover their extensive short positions in volatility vehicles. Tiny punters close down vol selling bets.

See you at a 1% US10y.

Al Edwards, is that you??? If so I've been wanting to buy you a beer for about a decade. Call my people, we'll set it up. (if anyone can send me his latest ice age screed, please pop it over to TeamMacroMan2@gmail.com)

ReplyI get it about Japanification--I'm going to have to sit down with a bottle of pinot and think about where DM economies are in that metaphor. I think Larry Summers had it right about secular stagnation years ago--but today I look at data like this and the state of the labor market and have to ask why the front end won't steepen.

And yeah we've seen this movie before, where Lucy pulls the football away at the last second...but at the same time i read this type of "this time it's different" analysis for why labor markets aren't producing inflation, or why curves will never steepen again, why oil prices will never rise again, or why robots will destroy monetary policy as we know it. I don't have a crystal ball, maybe some of those things are true--but is the market underpricing the possibility that the Fed comes through with the hikes in the dot plot for 2018? I tend to think the data argues the answer is yes.

the spread between 1y1y and spot 1y is 35bps, while that has bounced off of 18, it is just back to levels from July and still well off of 50ish earlier this year and 65-85bp range throughout most of 2015. Granted, libor was lower then--but I hardly think 3mo LIBOR at 1.33 is the work of volker-like reactionaries. and 2y1y vs. 1y1y? Hasn't moved an inch!! Right at 16bps where it was a month ago.

Just all seems a little too comfortable to me.

Agree the short-end looks too flat though reluctant to place my bet before a Fed Chair is appointed. I read a couple of Warsh's speeches. Statements of what by now should be obvious to non-academic observers. The problems are mostly known. But what are this guy's solutions? "Reform." Being "strategic." Whatever that means. So, I get that he doesn't buy secular stagnation and he thinks real rates should be higher, but when? Now? Or when Trump gets US trend growth to 3% (i.e. never)? Where would he set interest rates today? Still don't have much sense for that.

ReplyI'm guessing it'll be Powell, but I have no form in predicting these things.

Minutes/Praet speech last week suggest ECB extends at 20b/month for 9 months. Seems modestly constructive for EURUSD and duration shorts.

https://www.thestreet.com/story/14292536/2/august-jobs-miss-plays-into-bear-s-worries-about-u-s-deflation.html

Reply"There is mounting evidence that underlying U.S. CPI inflation has already slid into outright deflation in exactly the same way that Japan did seven years after its credit bubble burst. Hence, we repeat our call for U.S. 10-year bond yields to ultimately converge with Japan and Germany at around minus 1%," Albert Edwards wrote in recent research.

This stagnation is due to deleveraging by households at a time when the population is aging rapidly, in Edwards' view. "Both factors would also combine to push the West into a similar deflationary bust, despite the best efforts of policymakers (who incidentally would in no way follow the advice they had previously given Japan to liquidate capacity)," he said.

Like many other market observers, Edwards focuses on wage data. He noted that ordinarily, at this point in the U.S. economic cycle, a tight labor market would normally have caused a "notable upturn" in wages and inflation. This would prompt the Fed into a tightening cycle that would usually end in a recession.

Edwards had expected this to happen at the start of the year, and the ensuing recession to tip the U.S. into deflation, but now he said he had been "too optimistic" about that scenario. He noted that over the past six months there were "consistent downside surprises" in the pace of acceleration for wages, which came hand-in-hand with "an unprecedented slump in underlying U.S. CPI inflation into outright deflation."

Core CPI (excluding food, energy and shelter) never fell over a six-month period since the 1960s, according to Edwards, who added: "Deflation did not need another US recession to emerge. It is already here."

Not gonna lie to you punters. But that George Foreman's photo just reinforced the dreams I've been having the last 15 years of doing to horse trainers what they've been doing to punters since whenever. Really, do these punters think they can just crawl from under rock and ask for a tip sheet and a direct hotline to Goldman Sucks trading desk after taking bets that Goldman may not even survive the sub-prime real estate debacle. Please, leave a poor mug alone. Happy to be broke , alone , and allowed to find winners my way.

ReplyTake a look at the last chart here:

Replyhttps://ftalphaville.ft.com/2017/10/02/2194266/the-fed-is-going-to-make-interest-rate-risk-great-again-sort-of/

Not gonna lie to you punters. But that cover of the economist just reinforced the reason for Macroman consulting Inc. not handing the tip sheet, or giving the direct hotline number to those critters that just came crawling out from under a rock. Life's good being broke and happy in the knowledge that 1% of the 1% er's are being denied alpha returns due to your printing press being shutdown and telecommunication's terminated. Life has never been better knowing the tipping sheet will never see daylight in their world.

ReplyNot gonna lie to you punters. But fuck he was the big fella.

ReplyNot gonna lie to you punters. But when Rupert goes, his going to take those 'ratings' with him up into the big sky. You can't eat iphones , but his proved to God you can eat 'ratings'.

ReplyNot gonna lie to you punters. But , yeah...I don't care about it anymore. There is no one left to run with in their world, whatever that is.

ReplyFed Flow of Funds Data:

ReplySince Q3 2007, non-financial companies have swamped all other buyers/sellers of stocks by ≈$4 Trillion

https://imgur.com/a/J2Fxg

@amps...check out the youtube of that fight. Foreman just pushes frazier back and cracks him in the head time after time. And every punch he throws is a total howitzer. Ali was watching...and thinking.

ReplyNot gonna lie to you, Shawn. But I'm not really into boxing. You don't have to have a boxer ability to duck and weave when an onslaught of critters come out from under a rock offering a share prospectus for investors for a company they don't belong in, nor should be allowed to run. It is a good thing though that the CEO of said company moved offshore. Happy to be broke, alone, and allowed to find winners my way.

ReplyWhat's up with Bridgewater? LTCM on steroids?

Replyhttps://twitter.com/wolfejosh/status/917576959764377600

So Bridgewater lends money to it's auditor?

Replyhttps://twitter.com/pierpont_morgan/status/918101910435049472

Shawn, I thought that was a great post.

ReplyI think the simple fact is we don't just have the ageing demographic issue wrt inflation, but of course we have globalisation of capital and trade which has inadvertently led to an excess of global labour supply and an in-built excess capacity problem. Proper deflationary conditions in fact, but being fought with extraordinary monetary policy that simply serves to help build up imbalances in trade, haves and have nots and of course risky debts. A solution is to change trade rules and insitgate wealth taxes to bring things back into balance.

Ali, Frazier, Foreman...great times. But don't forget Ken Norton.

ReplyThanks for the comments AI...clearly this week's muted (i.e. boring) price action didn't put any momentum into my thesis.

ReplyYour points (and those by Johno earlier) are good ones, and perhaps I broadened the scope a bit too much by bringing demographics into it when i think the most salient point is that inflation can tick higher, the market can re-price to come closer to the 2018 "dots", and 2/5s can lift itself off the canvas (to stay with the boxing metaphor). 5/30s would be another matter where your points hold a lot more weight.

I have some other long-term thoughts on QE, demographics, etc. that should hit the tape tonight or tomorrow morning.