Think about history’s great entrepreneurs: the people that set out to change the world, and did just that. Today’s best example is Elon Musk. Take a couple minutes out of your busy day and watch a bit of his presentation of the Tesla Powerwall.

What do you notice first, other than entry music fit for the reigning WWE Intercontinental Champion? Elon has a great hook. Fossil fuels are going to destroy humanity. Now think about your last powerpoint presentation to an investor, client, or boss. Yeah, you used some generic corporate-approved background theme and loaded it down with bullet points and charts. Me? “Guilty.” Good grief, the evidence is probably out there on the interwebs somewhere.

I bring this up after reading an article in last weekend’s edition of Barron’s, “The Coming Renaissance of Macro Investing” by macro superstar John Curran. He opens with a story about Nixon’s Treasury Secretary William Simon cutting a deal with the Saudis in mid-1974 to buy their oil in exchange for recycling those dollars into US treasuries. Curran claims this set the stage for two generations of US opulence because USD “demand” from petrodollar states underpinned the strength of the dollar as a reserve currency and allowed the US economy to grow amidst low and relatively stable interest rates.

That's a good hook--not quite Musk’s threat to global humanity, but one that appears to show a courageous Treasury secretary that stepped into the crucible and saved America from inflationary doom.

We could sit here all day and argue about the economic history of the United States and the role of the dollar’s reserve currency status in the development and maintenance of a global hegemon. Let’s look at the facts.

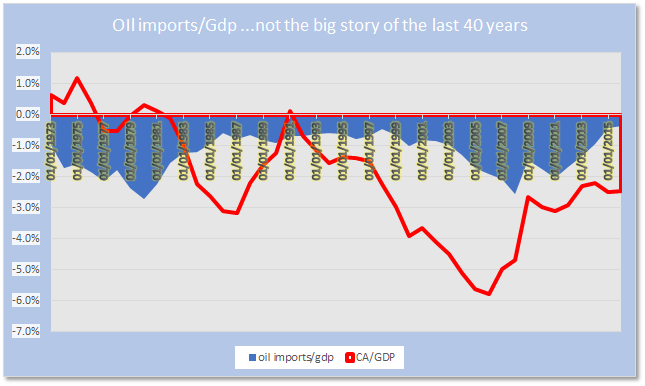

Source: St. Louis Federal Reserve and Energy Institute of America

This chart shows the gap between the current account deficit and net oil imports as a percentage of GDP. In the early 70s, this was a significant issue. America had a strong manufacturing and export base, so when the Arab oil embargo put those imported barrels at risk, and the price of oil skyrocketed, exports suffered, and US consumers were squeezed.

Curran correctly notes that the deal between the US and the Saudis was about neutralizing oil as an economic weapon. But it was far more about national security and guaranteeing energy supplies than it was about recycling petrodollars and establishing the USD as a reserve currency in a post-Bretton Woods world.

That didn’t come until several years later, when President Reagan declared “morning in America”. By the 1980s, Europe was still a fractured, socialistic mess, while relative prosperity in the United States, unsurpassed financial markets, the Cold War and strong property rights conspired to give Reagan the ammunition he needed to up the ante on the Soviets: bonds.

The key ingredient: Foreigners wanted US assets. They bought treasury bonds. They bought Michael Milken’s junk bonds. They bought Louie Raneri's mortgage-backed securities. They bought corporations. They bought golf courses. They bought movie studios. Anyone remember the press squealing about the Japanese buying up the entire United States?

Help me out here...is Japan a big oil exporter? No. The world wanted our assets because we were buying their oil AND their stuff--and we had the best assets and rule of law on offer.

The demand for US assets to finance the current account deficit was MUCH bigger and deeper than Curran claims. That’s important because he uses the petrodollar argument as the foundation for his claim that the Chinese are due to seize the dollar’s global reserve status.

There is certainly some appeal to his argument: he details the ways in which the Chinese are seeking to rotate away from the dollar as a medium of exchange in oil markets. To understand that to be a threat to the dollar’s status as a reserve currency ignores the last points in the above chart: net oil imports as a percentage of GDP are approaching zero...and adding in the trade surplus in petroleum products leaves energy as a positive or immaterial force in US financial flows.

Curran notes that the increase in domestic production has led to lower oil prices and lower revenues for Gulf states--but he pushes that argument too far when he says that leads to lower demand for Treasuries and dollars. If we are exporting oil, won’t we receive dollars in return? Won’t US exporters than invest that money either in expanding domestic production….or in US treasuries, corporates, or equities?

The last plank in this piece circles back to macro at large, which can be summarized as MACRO IS DEAD. LONG LIVE MACRO. Everyone says macro is dead. Must be a contrary indicator. What’s the evidence here?

The Fed “normalization” will lead to diminished support for the US Treasury market. ...The US will need to finance enormous and growing entitlement programs, and our historical international sources will no longer support us.

The key here is central bank credibility. Say what you want about the Fed, the flat curve and (relatively) resilient USD is telling you the market believes they will strangle inflation behind the metaphorical dive bar of global financial markets. That’s another plank in the arsenal of a global reserve currency and one that isn’t going away soon.

There is little evidence that global investors are on the verge of abandoning their faith in the US in favor of China. China exports goods (their trade surplus) which leaves them a BUYER of foreign assets. What are they going to buy? Russian corruption? Until the Chinese consumer becomes even close to the rabid, voracious, insatiable animal known as the American consumer, this trend isn’t changing.

And lastly, despite our president’s best efforts, the US is still a destination for capital the world over when people want to put their money in a safer place. That’s not about to change either--not for people in Latin America, the Gulf States, Africa or even China.

We all like to think of ourselves as contrarian investors, or smarter than the average bear. But this one just doesn’t hold water to be the “paradigm shift” that blows us out of the current malaise of low volatility and rings in a new era of macro investing.

Shawn

TeamMacroMan2@gmail.com

@EMInflationista

Shawn

TeamMacroMan2@gmail.com

@EMInflationista

26 comments

Click here for commentsMichael Pettis is very good on this subject - bottom line, as you say, is that if you want to be a reserve currency, then you need a current account deficit, and you need to have a system of government that allows you to finance that deficit. There is a nice point in Niall Ferguson’s book on money where he cites the Rothschilds as saying that they charged a lower interest rate to monarch who allowed some form of parliament, because they felt that those monarchs were less likely to be deposed in a revolution.

ReplyThe other unique thing about America is that its economy is relatively small relative to its current account, so the deficit is not a threat to growth.

Props on the note Shawn. I couldn't agree more. I don't know how many Luke Growman CFA's of the world I'm going to be forced to say this to...If America is the worlds number 1 food provider, soon to be leading energy provider, professional services provider, etc. I think we can all agree that the dollar is going nowhere. Not to mention that the dollar is used as the preferred currency in half the world. BIS debt statistics will just blow you away. Finally, America is still the safe haven for all assets. Our "Yankee" rule of law, property rights, and contract laws/rights are a huge factor as well. So there are innumerable arguments I could make to refute this "dollar is dead" nonsense.

ReplyI might side with Russell Clarke in suggesting that it pays to check out the micro at times as well. You know when the macro space is sleepy...like now. However, like most on this blog, I love the macro concept. A strong dollar doesn't automatically mean macro strategies can't succeed. I've been in the currency markets and EM world all year. During a strong dollar and a weak dollar. Apparently it's the same thing Glenpoint Capital did this year.

So...who's ready to put some psoitions on in Eastern Europe?

Indeed, if you want the 'exhorbitant privilege' of a global reserve currency you have to supply that currency to the world by running a deficit. If you don't, in a growing world a shortage of currency leads to deflationary pressures which become unbearable and debts start to be defaulted. The 'Triffin Dilemma'. https://en.wikipedia.org/wiki/Triffin_dilemma

ReplyThe Chinese, like the Germans are 'culturally disposed' to running surpluses and there is almost nothing, beyond erecting protectionist barriers, that can do anything about it - well, not without changing the international trading system to restore a semblance of balance. So, neither Europe nor China are going to take America's place anytime soon and there is no one else of a size who can. Of course, unbalanced trade and thereby rising debts and savings causes its own issues.

I am always surprised what a short-term memory people often have, especially when it comes to financial markets. Last time I checked in 2011-2012, the yen traded against the dollar for most of the time below 80 yen. Was the dollar declared dead back then? By no means, nor does anyone declare the dollar dead now, at least not sane people we respect to read and listen to. But you ignore a huge piece of the equation, something that is not balance sheet driven, nor oil driven, but simply a function of where investors perceive their funding to be safe. That was certainly not in the US in 2007-2008 nor for several subsequent years. The US equity and with it many related assets are helplessly overvalued, a bursting of this bubble can occur at virtually any time. You will see that investors halve no qualms to kick out the USD again and load up on the currency of a country that is heavily indebted simply because investors perceive it as a safe (and stable) heaven. Those are dynamics that we cannot and should not ignore.

ReplyI agree with your other points in that oil cash flows are meaningless to the US nowadays.

good comments all-- @AsiaProp, good point on the safety of funding--the GFC shows the risk and consequences of sloppy regulation--the US got bailed out on that point by no other jurisdiction of size having done much better. That said the funding crisis passed quickly and IMO the US FTQ characteristic probably came out stronger in the end.

Reply... Japan, Germany, shall I continue with a list of major industrialized nations that have fared way better during and after the GFC? If you lived in Japan during and after (I have) and went to restaurants and bars in Tokyo you would not even have known there was any sort of crisis around anywhere. Just saying the GFC was more a US financial crisis and it resulted in one of the worst asset bubbles in human history of which we have not even tasted the worst yet by far. I am a USD bull for relative value reasons but the US is in far worse shape than you make it out to be, especially fundamentally speaking. Its just the shining star in asset bubble stardom and markets and investors love kinky and sneaky snake oil salesmen

ReplyHard to believe that today people woke up, looked at the date and realized it's time to sell. It is conceivable that experienced heads at the office told the younger gen how scary it was back then, immediately followed by shrugging, hedging and reasoning as to why it won't happen again. It will... Just not today, not now, and not in the same way per se. We need more "buy stocks for the next 6-7 yrs" crowd to teach us how to live our lives before the inevitable happens. What may that be? Way above my pay grade to speculate but if a gun was put to my head I would say this: too many people letting their guard down all at once. Case in point, SVXY is a good example. Buy that baby for the next 6-7 yrs if you are that bullish. I am waiting on the other side. Just have to be patient, very patient.

ReplyBravo, Shawn. The future is way too complex for me to see far into (I'm usually exceeding myself if I have some clarity about what's going on in the present!). My attitude to Curran's piece was, "yeah, show me," and you articulate very well why his arguments are, in fact, "show me" arguments. Thank you.

ReplyThe GFC was triggered by foreign banks in the US. The didn't have enough dollar reserves. They don't have the deposits as a base like their American counterparts. So, they went through the swap markets. From 99-07 dollar denominated assets at non US banks quadrupled from 2 trillion to 8 trillion. Now this excess demand for swaps increased the dollar basis. This caused the implied forward rate of the dollar to increase. When LIBOR is being purposefully fixed at a low rate it distorts the dollar basis calculation for these transactions. It's rumored that some of the fixing committe were trying to hide problems they were facing at their respective banks. The free market believed the dollar was more valuable so the swap had to increase in cost. LIBOR being to low the spread was huge and it scared other banks from taking the opposing side of the swap. So an interbank lending problem ballooned into a disaster. It popped off because of problems inside of the Eurodollar system. This affected the wholesale funding market. Money Markets stopped by commercial paper. Banks couldn't fund daily activities. Lehman dried up overnight.

ReplyMy point above was that the dollar is everywhere. It's so prevalent that the strong dollar hurting EM's thesis is starting to fade. NOW, I'm not suggesting EM's are 100% safe from a currency spike. I'm merely suggesting things are changing and the em's should be in a better position to handle outflows. The monetary research in the field shows that everyone has dollars. So increasing what they can buy with said dollars is a good thing for Americans and the dollar owners of the world...which is everyone. It's a global currency. EM's understand better than anyone the risks they are taking. Yet, the businesses, citizens, farmers, and the government all prefer dollar invoicing.

Now, I agree with @AsiaProp that there is a giant asset bubble and risks are high. That's (IMO) a no-brainer. The risks are known. Where I disagree with him is as follows. I view the US's position differently. US is the only country that has any kind of "1 n a Million" chance to grow themselves out of debt. I understand how impossible that seems and it would be a daunting task. The problem is that the world doesn't function as well with an impaired US economy. Hence the IMF chief Lagarde's point last night saying the worlds most powerful economy needs a tax overhaul desperately. Why would she say that? In fact the IMF is quite fond of bashing on the western economies. Because the IMF knows the United States drives the global economy, period. 275 Million and growing US consumers with sophisticated shopping tastes. The bigger their wallets the better shot the rest of the world has

P.S. I'm no fan of the fiat system were stuck with just to be clear. I think it's a fucking travesty what governements all over the world have done to the citizens purchasing power.

Just to be absolutely clear, when you refer to GFC you mean global financial crisis, and in particular the one that expressed itself from the end of 2007 well into 2009, correct?

ReplyIn that case it is imho absurd to argue the crisis was triggered by foreign non US entities and even more absurd to find the culprit in libor fixing. The crisis was almost entirely US born, facilitated by an ultra lose Fed, by US politicians that promised American consumers that it is an inborn right for every last resident to own his or her own home, by US home owners who lied on mortgage application forms and overleveraged. When hookers in Nevada held 5 or 6 mortgages and plumbers or police men took out HELs to finance a second mortgage anyone should have known that this cannot end well. Another culprit was banks, US banks, mortgage lenders who did not check records and application forms and instead signed up whoever walked into the door. Rating agencies also played their part by selling ratings. This was not a crisis caused by Deutsche Bank, Spain, or Greece or the smurfs for that matter. I think we should not throw the past 10 years into one giant pot, happily stir and claim its all the same.

Re your point on USD, I can't help to get the impression that you are arguing from a position of slight hubris. It is actually very simple: Whoever has something others want has selling power. Whoever wants something others have to sell has buying power. By that simple fact Americans and the USD still plays an important role and will most likely play am important role into the future. However let us agree that the population in the US is dwarfed not just by the population of the EU as a whole but especially by China. This matters, and it expresses itself in multiple economic metrics of power that already overshadow the ones of the US. China had reached a level of standing that it negotiates major contracts with other nations in its local currency and this will increase and it will make the USD less relevant in the exact same way the British Pound has lost relevance since the peak of its industrial might. Again, I am not arguing that the US will not be relevant anymore, I am simply not following your hubris.

Just a few years ago it was the US that was at the brink of a collapse while China chucked along and while multiple major industrial nations in Europe hardly were pinched.

The USD will still be very relevant and will be a means of barter between many nations but it will be less relevant than today, the trend in contract negotiations between non US nations speaks for itself. And it makes a lot of sense. Holding a diversified fx basket makes a lot of sense as well as targeting fx holdings as function of trade conducted with other nations. As other nations gain in power it is all too natural that other currencies' weights in baskets and in contracts will be more highly weighted going forward while the USD's weight will decrease over time, to a level that still resembles a lot of relevance, just less so than before.

Yes, what you said regarding mortgages, easy credit, securitization, all occurred and contributed to the crisis. These reasons you give were symptoms. Easy credit globally, US banks, people, etc all played a role, but the root cause was domestic non-US banks running out of available dollars. They turned to swaps, but they overdid it. This extreme dollar demand pushed up the implied forward rate which in turn caused the dollar basis to increase dramatically in the XCCY space. I am not shifting blame here. US banks played a huge role as well. I am well aware of that fact. My point wasn't to give them a free ride. My point was to show the root of the GFC. To do that I got pretty granular and mechanical, but I am 100% right. Foreign banks accumulated 8 trillion dollars (up from) 2 total 10 years earlier. That's crazy dollar demand, but what's even worse is that a large portion of these accumulations were accomplished with swap agreements between two counterparties. I can get the info from the NY Fed if you still think I'm wrong.

ReplyYES, LIBOR did have a role to play. Just like American banks, European banks were levered up. Lower rates and easy credit was the rage. They take on to much debt and they risk not being able to service the debt. This makes the cost of funding paramount. So an agreed lower LIBOR rate did play a role because dollar basis is determined by first assuming a no-arbitrage condition. Then using data for the euro-dollar spot and forward rates as well as on euro Libor—a proxy for the European interest rate—You can calculate the dollar interest rate implied by euro-dollar FX swaps. So LIBOR is important. If it's too low it's a distortion in the market. This was the point of origin for the whole thing. What happened after wasn't what caused the crisis. it was just the next step in an already unfolding crisis in the shadow banking system or the Eurodollar markets

Now, with China 80% of the country is broke. They face enormous demographic headwinds as well. Sure China is important, but things only get harder from here. The US is the only developed country that has a growing birth rate. Americans are also working longer, which only facilitates the US portion of the accumulated capital stock in the world. In regards to the dollars inevitable waining influence...the facts show something different. The polar opposite in fact. The US dollar is more in demand now than it was 3 years ago. 3 years ago it was more in demand than before GFC. In fact, it seems to grow in demand globally on an annual basis. I mean 30% of trade as well as cross-border lending between Europe and Asia is settled in...US DOLLARS. Again, another fact I can prove.

I agree with several of your points. However, I suppose we can just agree to disagree on some others.

I could not possibly disagree more with your assessment on the root causes of the financial crisis. It sounds like as if Lehman Brothers was telling me it was Deutsche Bank which caused the crisis, oh hold on Dick Fuld just added "it actually was Nazis, wait, he is being more concrete, it was the Germans who caused the global financial crisis, wait, Dick finally found the real culprit: it was international banks."

ReplySorry I could not help it. Let's agree to disagree on this one, though the facts are all on the table.

Fair enough but again, you are somehow imagining I'm placing blame on those "evil foreigners." The genesis of the problem is pretty well understood (understood as best the Eurodollar system can be understood) the dollar shortage, MM liquidity, the foreign dollar appetite, etc all of it. I mean what you are claiming is that it was solely the fault of US banks, brokers, and people. Foreign banks held a shit load of this toxic MBS crap. It is and has been a global lending network. They all partook and got paid in the end. This alleged indignation from the rest of the world towards American greed and American banks is hilarious. Hhahah come on man.

Reply@Shane,I just disagree with your hypothesis and analysis because no swaps in the world nor any implied forwards pushed up mortgage rates in any meaningful way, go back and check even 25 or 30 year fixed rates at that time, they were ridiculous low given the then rates environment and demand for such rates. Swaps never push up dollar demand unless it is a specific cross currency swap that sees one sided demand for USD in exchange for non USD cash flows. That is not what most banks traded. Most such swaps you reference are pure USD swaps and they don't move the USD demand needle a single bit. I simply don't understand why you make such assertion and introduce it as a factor for the mortgage crisis. Enough said.

ReplyTo add and clarify, nor did any swaps push down mortgage rates in any meaningful way. US mortgage rates are by far the most driven by mortgage interest remand and by benchmark lending rates that the Fed directly controlled. It should have been the prudent decision for Greenspan to raise rates by a multiple hundred basis points but he decided to let the balloon inflate itself with his easy money policy. In no ways were his hands bound by libor markets.

ReplyBy the way, the concerted effort to manipulate libor fixings had a miniscule effect on the overall libor rate, we are talking a few Basis points here and there. None of those fixings distorted libor by more than that. Just saying as you seemed to allude to that as well in an earlier post unless I misunderstand. In any case easy credit and banks leveraging up is a direct function of Central Bank policy. The US Fed is guilty as charged and was entirely complicit.

ReplyChina broke? You surely are swinging your big baseball bat here. Funadematally speaking, most analysts would argue that the US consumer is broke not the Chinese one. Surely Chinese corporates have taken on too much debt and this may and probably will cause problems. But every metric there is out there is clearly indicating in which direction the Chinese economy is heading and where in contrast the US hegemony is heading. Can I suggest we take nationalism and pride and patriotism out of this discussion because I firmly believe they clout the picture. You come across as someone who has incredible difficulties admitting that China has in many ways taken over and will in my ways surpass the US by most econometric measures.

ReplyNationalism nice buzzword bro. 63% in Shanghai earn less than 8,000 RMB. That's one of the most prosperous cities in China. Relatively speaking, China has a small (growing) middle-class market. Side note those very middle class take the first chance they get to leave the country with their money and settle anywhere other than China. Demographics get bad for them, quickly. China is like an event. They are devouring the worlds capital stock (National factor endowments) They then go on to build cities to nowhere, or grand towns that copy the US, pointless construction, etc. Did you know they are currently (with what money I know not) bulldozing millions of homes and paying the residents in the hopes they will move to those ghost cities. Then, they just rebuild more homes on the same land the just bulldozed. It's worse than the pyramid builders. No, the hegemony as you call it remains with the US. When the time comes that some nation challenges the US I will gladly admit it. It's just not now

ReplyJesus...I didn't notice all your messages. BROOOO I agree the fed is at fault...how are you not getting me with that. The fed itself didn't know what was going on in the bowels of the wholesale funding market. So they are to blame, but the Eurodollar system allowed the crisis to become what it did.

ReplyYes LIBOR did matter. it was a small culprit, but it added to the problem. The point of LIBOR is to get a broad or global agreed upon rate. Banks take the fixing committee's lead and use it as a baseline. If you purposeful suppress it then it distorts markets. So a german mark for dollars swap deal is made based on respective currency rates or basis. What they found out was that many non banks and smaller banks didn't recieve the same rates on short term money than a few large ones. With enough time these small distortions build up. This is the reason for the XCCY swap problems. This alerts us to distoritons in the normal smooth funcitoning system. Further investigation found it was a severe dollar shortage problem that the XCCY swaps were exposing.

ReplyI let Shane's posts speak for themselves. Just want to add couple facts to this picture:

Reply* China has been a larger trading nation than the US since 2013, already

* EU external trade dwarfs US trade by quite a margin

* The EU also has far larger FDI than the US

* The EU, China, and Germany (external trade only as intra EU trade is already counted in the EU figure) export over 4 times as much as the US.

* China imports more from the EU than from the US

* The EU imports more from China than the US

* China is pushing very hard and has been very successful so far in establishing the yuan as largest settlement currency of choice between China and most other Asian trading partners

* Most every macro economist agrees that the yuan will over time become a major trade settlement currency outside of Asia as well.

Those figures alone demonstrate that the US is a goods and services powerhouse but by far not as powerful as it once was. Inter-block trade is an incredibly important input into currency exchange rates. The US only stands in those tables among the top nations because of its financial market. More and more trade agreements between major non-US nations and blocks are settled in non USD currencies. The trend here is clear. I find it hard to imagine any sane person would challenge and question those facts.

And thank you Shane for correcting yourself in that Libor rates settings mechanisms and libor rates themselves played a very "small role" ("small culprit" as you literally worded it) in the causes of the global financial mortgage crisis, I guess we can finally agree on something.

In summary, I agree with Shawn's (OP) major conclusion, the US dollar is by no means dead but it is hard to argue against the prevailing trend that it has already lost some in importance over the past few years and there are no catalysts on the horizon that would predict a trend change. it makes a lot of sense given the major trading nation, China, is aggressively pushing into trade settlement in its local currency.

The US is now a services and software powerhouse. China is a goods powerhouse. Now we can all agree, no?

ReplyLet's focus on a risk factor in markets that has been forgotten. Not the USD per se, but USDCNY. China just wrapped up its Communist Party Congress and Politburo meetings. Xi Jinping has started to warn explicitly against excessive risks and leverage in China's domestic (real estate, equity, debt) markets. With global growth stable, if slow, and global markets stable and sleepy, this would be an ideal time for another overnight RMB devaluation, or the initiation of a protracted series of small steps. China needs this now, as indications are that the trade-weighted USD is going to drift upwards over the medium term.

Despite the large size of the Chinese economy, Shane's point about incomes is a good one - most Chinese are not in the middle class or in the wealthy elite, and consumer growth is therefore confined to a small segment of society. There is little doubt that official GDP figures are a manufactured fiction. [Long time readers may recall LB's China GDP formula = 10 - 0.1x, where x is the number of quarters since 2008.] China is a full participant in the Race to the Bottom. The Chinese economy is probably growing much more slowly in reality, perhaps at 3% or less. Just like the US and EU, in order to maintain even this modest growth rate in the face of demographic headwinds, the PBoC will have to maintain easy money policies. Hence not only would a 5% devaluation of the yuan be unsurprising, it would be more surprising if they did not move to do this soon.

The situation in Catalonia is likely to put some pressure on EURUSD in the weeks ahead. Add this to reasonable prospects for a lower CNYUSD and one can't help feeling that the dollar will be far from dead in Q4. A whole generation of new 20-something fund managers and punters has grown up without seeing a really good emerging markets and high yield Pump n Dump event. These are always triggered by short-term dollar and liquidity shortages as Shane discussed above.

Let me give you a clue, youngsters, look at the INSANELY tight spreads for Southern Europe to Treasuries, CCC debt spreads etc… Yup, that's right, you just bought the Pump. Next comes the Dump.

I believe that the PBoC is already signaling an upcoming tightening, which is commonly achieved via CNY devaluation.

Replyhttp://www.barrons.com/articles/a-chinese-minsky-moment-global-markets-shudder-1508425147?mod=yahoobarrons&ru=yahoo&yptr=yahoo

Noobs, JBTFDers and other permabulls should probably take a look at charts for August 2015 and January 2016 to see how this might play out. Remember this may well be happening as we enter a period of retrenchment by central banks: from October 2017 into 2018, CBs may reduce their global market interventions to the tune of $1T.

Meanwhile over at the state pension fund, Chad, Brad and Thad are now running half the entire portfolio, occupy a suite of corner offices as the Division of Extended Volatility Investors and Leveraged Sellers (DEVILS) and the Risk Office has been closed permanently….

Be careful out there.

a 5% devaluation would be unsurprising? FX vol markets would argue otherwise. I don't see the catalyst for why they would do that. With the CNY strength tapering off on its own accord, the PBoC continuing to stabilize/replenish reserves, and growth chugging along nicely, there is no reason to upset the apple cart there.

ReplyWhile I agree that today's price action and (potential) tax deal shows the USD can rally from here and take some vinegar out of EMFX, even the 20-somethings were around two years ago when EM was totally radioactive, no?

As for credit spreads, there is plenty of complicity to go around on that one...

@leftback,have you been to Asia lately? Or perhaps Vancouver, Australia, New Zealand? If your assessment of the Chinese consumer was just remotely correct we should all fear Armageddon in terms of Chinese taking possession of every last asset there is once the masses have reached middle income status.

ReplyI can assure you, however, that this is not true, I have been sitting in the middle of it all for the past 1.5 decades and while the definition of middle income wealth in the US and Europe vs China might be very different, the Chinese economy and its consumers are in a far more advanced stage than most casual observers from the outside, even if they worked in financial services, would ever comprehend. The pictures most on this blog and elsewhere paint of China is of at least 8 to 10 years ago. I recommend a trip to some of the second tier, third or even smaller cities to get an update on consumption patterns and discretionary spending by nowadays average Chinese. I can assure you that you will be surprised.

Re your CNY topics, I don't understand why the Western financial industry is so consumed if not obsessed by some of those CCB revaluation. Volatility and what drives investors here in East Asia to move their cheese around is driven by entirely different factors.

For a light-weight punter like me, can anyone proffer an opinion on these notions by Steen Jakobsen of SaxoBank:

Reply1. The US dollar has peaked and started a multi-year cycle lower as both US and world growth can’t work without a weaker dollar (a stronger dollar kills growth through debt service, emerging markets, and commodities).

2. Everything is deflationary: demographics, technology, energy, and the debt mountain.

3. The credit impulse peaked in late 2016/early 2017 leaving global growth vulnerable in the fourth quarter of 2016 and into Q1’17.

4. US interest rates are headed to 0% in 10-year government yields by the end of 2018, early 2019.