Today is the morning prices had to find me...from my wi-fi resistant hovel in the rural midwest I hear the treasury curve is bear steepening...can it be?!? The rhetoric behind the Senate bill looks like “we can all have a unicorn” type stuff...tax cuts for all!! I’d hazard a guess that nobody has made a buck this year going long on Trump’s ability to execute--so I’m still skeptical.

Notable moves in Canada as well...driven in part by lousy data but also moves by the local regulator to tighten mortgage standards. This gets back to an issue about local versus national housing price increases I addressed over the summer--stay tuned for an update next week.

And a little housekeeping here-- I couldn’t post this chart in the comment section of the previous post, but I thought it was worth highlighting. CNY is 2% of international payments, and (arguably) falling. Beijing and the PBoC are dragging their feet on the internationalization of the currency--they simply don’t want it...yet. They prefer (capital) control and stability. While there have been some signs that Chinese local debt will gain greater acceptance in real money circles or (gasp) EM local market indices, we’re not there yet either.

I’d like to quickly circle back to “Fed speak”, which will become more important as we finally get a answer from Trump on the next chair of the FOMC, and more data over the next couple of weeks. In a speech in early October, San Francisco Fed chief John Williams gave another hypothesis on the “one-offs” that might be sandbagging inflation:

“An even bigger contribution to low inflation has been coming from the healthcare sector. Mandated cuts to Medicare payment growth, which also tend to be incorporated into payments for nongovernment health services, have kept inflation in overall health-care services unusually low for several years. These legislated changes have been a key factor holding inflation below the Fed’s 2 percent target, despite a strengthening economy.”

He reiterated this stance in a breezy Q&A with the New York Times earlier this week. Does Williams’ health care hypothesis have any more efficacy than Yellen’s targeting of telecom prices? Let’s look at the numbers.

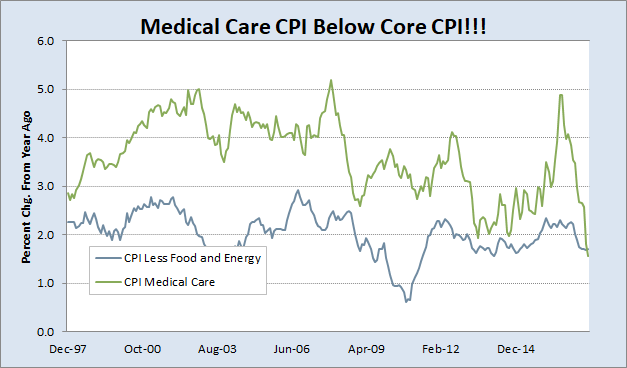

Indeed, Medical care CPI has cratered and currently stands below core CPI for the first time since “Who Let the Dogs Out” topped the charts.

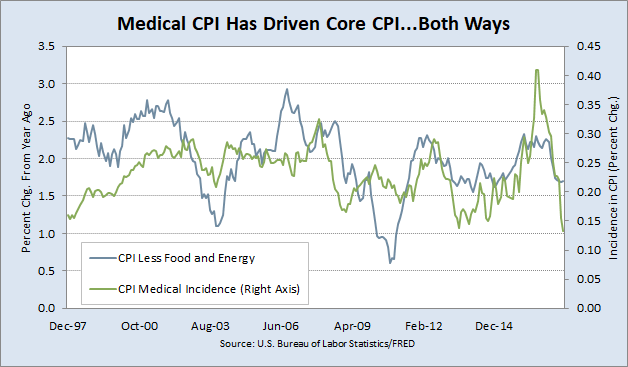

But there’s a strong correlation there--the NY Times article implies medical care CPI is unrelated to headline--but this chart would argue otherwise. The contribution of medical care CPI is at the lows--but off of very high levels that single handedly drove core CPI above the 2% threshold around the beginning of the hiking cycle. Now that has normalized.

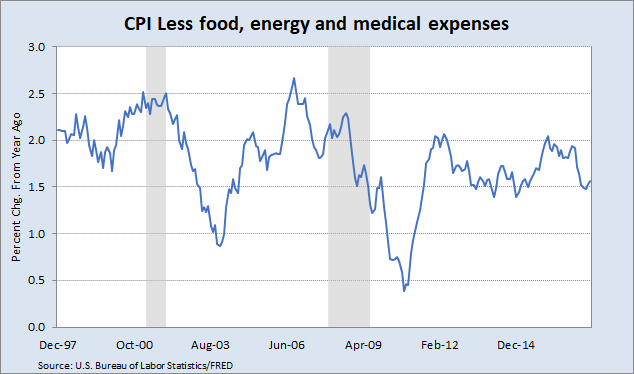

And as much as I hate stripping every inconvenient item out of CPI, if you look at this chart you don’t see anything too different than the plain vanilla core CPI, or the fed's trimmed mean and median CPI measures. Add back 10-15bps for trend medical expenses CPI if you prefer. It just doesn’t matter.

While I would agree with Williams this is a bit of an outlier, it is also one that is highly correlated with underlying CPI trends. Skilled labor is a significant portion of medical expenses and thus will increase somewhat in line with nominal GDP. Look for a mean reversion bounce back here which will drag core CPI higher, but not enough to really be a game changer for monetary policy. But thanks Dr. Williams...keep those theories coming!!

Lastly I quickly want to touch on oil prices. WTI is still top of the range, and while Brent (below) has finally broken the 56 level, it simply refuses to take a run at 60.

Supply has been a two way street here, with continuing OPEC chatter, issues in Iraq, and continued free flowing wells in the US.

I have inside source on the supply demand picture in the oil industry. Ok, it’s the New York Fed. Check out how demand has been growing as a contributor to the oil price since the recent lows in early July:

Demand isn’t dead!! Keep a close eye on tightening supplies because any OPEC resolution or supply disruptions could have a much bigger beta on oil prices than they have in the past, especially with US production much closer to full capacity than it was a year ago.

19 comments

Click here for commentsShawn, a little light reading for the weekend...

Replyhttps://www.buildaustralia.com.au/all-projects/

Massive recruitment drives ongoing/coming for Australia. 10-15 years of this ahead.

Could we get the loop? With all the planned diversification from mining in Oz, I think it will actually kick start the mining sector.

Australia - the new mini China boom to keep everything ticking over. Funded by China... Cough. (consider the last 5 years as a consolidation. Next 12-18 months to see it clearly).

Nice post, Shawn.

ReplyMy weekend parting shots list:

1) Re US hegemony, let's not forget that the US (and its brand image) has long attracted much of the world's best and brightest. Consider a country of 0.3b taking, a totally pulled-from-ass, 25% of the rest of the world's best and brightest. That's (7.3b x 25%) / 0.3b = 6x leverage, i.e. the US is 6x levered to the work product of the world's top minds. Look at the % of Silicon Valley companies started by 1st generation Americans as exhibit A. Now consider what Trump is doing for that brand image. My guess is America is beginning an intellectual deleveraging cycle.

2) A glance at CHIQ says AsiaProp is right about the Chinese consumer. Price always wins the argument.

3) The UK is toast, going by Martin Wolf's FT assessment today.

4) Trump rips up the Iran deal. Expect him to do the same with NAFTA, especially with votes to win in 2018. I feel truly awful for Mexico.

5) If China marks down its official growth target to the rate skeptics call "real," I bet Chinese stocks double. Financial markets are ironic that way.

6) What's going on in Japan? TOPIX/yen relationship signals regime change.

7) Earlier this year, I could hardly find a currency I didn't want to own against USD. Now I like USD more than a slim majority. In FX, the standout for me is EURCHF. Very long in option formats.

Johno,

Replygood call on the TOPIX/Yen correlation being broken. It's wild really. IMO it's due to the face the BOJ has purchased 85% of total Japanese ETF stock. So even when the Yen strengthens the TOPIX is not affected. In fact it seems to get a boost from the strong Yen. Those ETF's trapped at the BOJ won't allow the TOPIX to drop and recouple with the Yen.

https://www.ft.com/content/0f534aa4-4549-11e7-8519-9f94ee97d996

ReplyAfrica after that...

Nice and quietly China is buying continents.

North Korea my ass.

“Intellectual deleveraging cycle”. That’s brilliant. You gotta trademark that.

ReplyShawn, thanks for that visual on oil demand. Today is the highest weekly close since the 4/10 week (on both NYMEX pit and GLOBEX). I would like to point out that XLE daily is looking like it's flagging here. Pole distance is $7. While the momentum studies are getting oversold the price is totally nonchalant. I think it challenges $70 next week and probably goes well north of that by the end of the year, like $75-ish maybe. Crude should follow.

Reply“Intellectual deleveraging cycle”. That’s brilliant. You gotta trademark that.

ReplyTrademark nothing, not in this lifetime. @Buystocks was spot on. If you haven't made coin the last 7 years than forget this market. Forget trying to jump in now. Fuck that, who'd want to have to come on the trading desk now starting a career on Wall Street and bringing a family up in that environment. Fuck that. Not at my age.

@Buystock, thank you very much for your comment. It was always there, but that kick it out. I'm going back to being a mug punter, thank you very much. Now you know why some them just go drifting.

ReplyLacy Hunt on Inflation and more...

Replyhttps://www.cmgwealth.com/wp-content/uploads/2017/10/HIM2017Q3.pdf

LB finds himself sharing Shawn's skepticism about Trump's ability to deliver significant pieces of legislation. It is fairly likely that the tax reform bill will be held up, amended in the House or will simply die because of the lack of ability of this White House to work with the legislative branch. In any case, this seems like a great Sell The News set up, as most of the potential profit enhancements of tax reform have probably been priced in at this point.

ReplyA quick word about fixed income. The 2.40% level in the 10y held up well the last few weeks - this in the face of all manner of "reflationary" rhetoric. If you read the mainstream media you would think that the yield curve was steepening to benefit the banks etc… when in reality the curve has continued to flatten for months. Bond shorts are desperate for the long end to blow out, but it simply hasn't happened. There is a fantasy that Trump + John Taylor = 4% GDP and 5% 10y, to which I say LMFAO.

Read the Lacy Hunt article above (thanks Eddie) for a discussion of the yield curve, with which we completely agree. [Btw, regular readers will know that we called most of the important turns in the long bond over the last ten years. E.g. Spring 2010, December 2016…] We are long TLT, for the record, and have been adding to the position over the last 2-3 weeks.

“Intellectual deleveraging cycle”. That’s brilliant. You gotta trademark that.

Agreed. Brilliant. Expect to see it reproduced in the mainstream media without appropriate citation…. ;-)

It's interesting how hostile people are when Chinese data and truth are juxtaposed in the same sentence. Nobody questions the scale of the Chinese economy or indeed of social progress in PRC. but that's not the same as saying it is a good place to invest. Chinese money continues to exit for other locales (Vancouver, Sydney etc.. ) precisely BECAUSE they know that the Chinese financial system is a house of cards that will fold like a cheap tent when the wind blows hard enough.

The levels of debt are remarkable for a country that has already entered a demographic downturn. It's intellectually dishonest at this point to pretend that most of the official US economic data are real, so why should we expect this from China? , where a limited understanding of statistics and probability reveals that the official growth numbers are extensively massaged, if not simply completely invented by Beijing, i.e. "model-generated".

Keep half an eye on Catalonia, people. Things could get ugly there in a hurry, and that will have potential for contagion. We are for the time being also long vol, short IWM and have a piece of that "SVXY collapse" trade idea discussed here by others.

Here is a ZeroHedge (I still sift through it from time to time) article out today describing exactly what I was describing in my argument about the genesis of the GFC. It was the last post before this thread. In case anyone thought I was making shit up...cuz ol boy thought I was nuts. We were just missing eachother, something...

ReplyOn Wednesday, we noted the renewed tightness developing in dollar funding markets. Ignoring embryonic signs of stress in the financial “plumbing” can be dangerous. The divergence of LIBOR from Fed Funds on 9 August 2007, which occurred two months prior to the peak in the Dow, always comes to mind. ZH

http://www.zerohedge.com/news/2017-10-18/dolar-funding-shortage-it-never-went-away-and-its-starting-get-worse-again

I agree with you LB regarding the China touchiness. It's bizarre. The Yuan has fallen in usage via SWIFT data tracker. The fact of the matter is they are very poor in china, but obviously they have a growing middle class, and now some super wealthy. Very highly concentrated wealth that leaves a billion people hungry. They face awful demographic challenges as well.

In the US however, the birth rate is rising rapidly again. Researchers discovered it was the fact that high-school girls weren't get pregnant and women were waiting about 3 years later to have kids. People claim that Chinese leadership will create a safety net or S.S. fund for all the Chinese citizens. This is literally impossible due to something as simple as basic math.

I'm not hating on China by any means. I'm just looking at the facts. I'm well aware of America's misgivings as well. The influence peddling, vote buying, and the legislation gridlock in D.C fucking pisses me off to no end. The Fed is the enemy no doubt.

TAX REFORM is a game changer for the US. I'm talking specifically about the 50% of Americans who get refunds and pay no tax, but should. Tax Policy showed that 40% of the 50% could pay a few thousand minimum (with the other income tax breaks it wouldn't hurt them) I mean half of US taxpayers paying nothing then paying a few k is like an annual 1.2-1.4 Trillion boost to the revenue at the Treasury. The US is also the only nation without a VAT. Just those two streams of revenue would be huge. We could begin paying debts down, funding healthcare/medicare, interest on debt, S.S. etc. So in my view the US is not the proverbial boxer wobbling up against the ropes like everyone else thinks.

long vol and I own a piece of the "SVXY crash" trade also. Just took a position in the Canadian mess that's brewing. I'm long USD/CAD

P.S. anyone the Paul Tudor Jones movie making the twitter rounds again? I'm a bit younger so I had never seen, but I'd heard of it. I thought it was pretty dope

Shane, when you said "Very highly concentrated wealth that leaves a billion people hungry." Is this metaphorically speaking or literally?

ReplyLB, agree with your thesis on long term bond yield, but as always, I think you are a little bit early, again.

Wow, my fault I must have been in a hurry. I was simply saying that much of China'a wealth is very concentrated relative to the the other 1.2 billion in that country. That (IMO) won't end well. And again China is claiming they're going very automated in their factories (I dig the idea so we can sell them the robots) Now, this is CRAZY IMO because all of those hungry people will eventually say enough is enough. The democratic revolution haunts the party leaders sleep. So they think they want to create a S.S. trust fund as a safety net for the hundred's of millions....yeah...that will loose their jobs. That is where the math steps in and stops that fairy tale. Impossible to pay for...so I' just don't think its the future leader of the galaxy like everyone else does. It doesn't mean I don't have respect for Chinese people or China itself. It is very important in the world. Just not ready to say, "yeah I could see it in 30-50 years." So yeah that's what i meant

Reply@Buystocks, thank you again. I remember being eight years old when some Eastern European nutter down the street chased me and my friend around the block offering shares in a greyhound racing syndicate. I passed his offer to my father, and he was down there at his front door within a minute, no questions asked. The guy was a nutter. Have a go this lot.

Reply@Buystocks, for being the commentate of the year you get to keep Team Macro Man's furniture , and do as you please. You may donate it to charity , or you may hang on to it and use it as leverage one day in case of the need of an emergency. Just don't call me, and don't bother me.

Reply@TMM, I say , that about sums up the shit men down south. Good luck.

Reply@Shane, watch it quickly before PTJ tells them to take it off their site.

Replyhttp://documentaryvine.com/video/trader-the-documentary/

@IPA thanks for the line on the video bro!!!! No idea what he was tripping about it being released...it's perfect. It's an honest cut IMO. Good traders are cut-throat (generally)they will definitely be humbled, and its inside look at how traders placed trades in the open outcry exchanges. Fucking hat tip @IPA

ReplyEddie, I'm no economist, but I suspect there's something wrong with Hoisington's logic on pages 2-3 where they assume M2 is a fixed ratio of M0 (and then use some fixed or declining ratio of GDP to M2, V, to estimate growth effects). Isn't this the kind of Ec 101 thinking that's been debunked, say, here: http://www.bankofengland.co.uk/publications/Documents/quarterlybulletin/2014/qb14q1prereleasemoneycreation.pdf

ReplyI do think there's something to their argument about income growth and borrowing constraining the US consumer, however.

Ah, the PTJ documentary. Seeing that, I was like, "man, if he's a 'Great' then I really have a shot at this game!" Still, HUGE respect for the passion and intensity, and no arguing that his methods worked for him then.