Is the Canadian housing market in a bubble? Is it about to precipitate an nationwide financial crisis? If so, what can, or should, the BoC do about it?

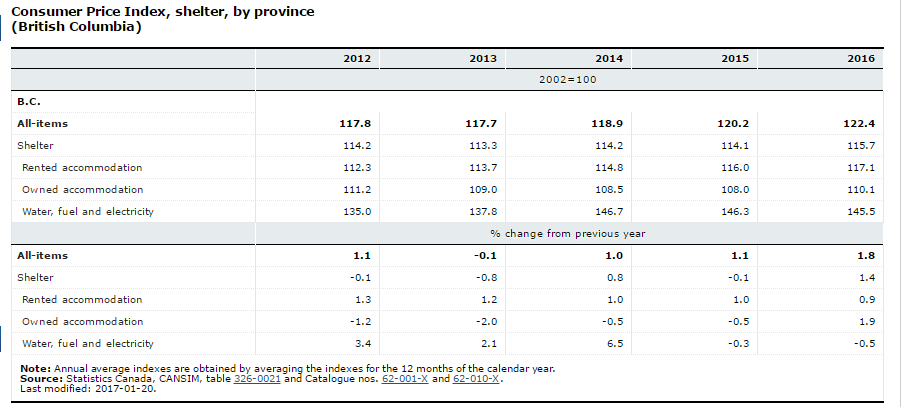

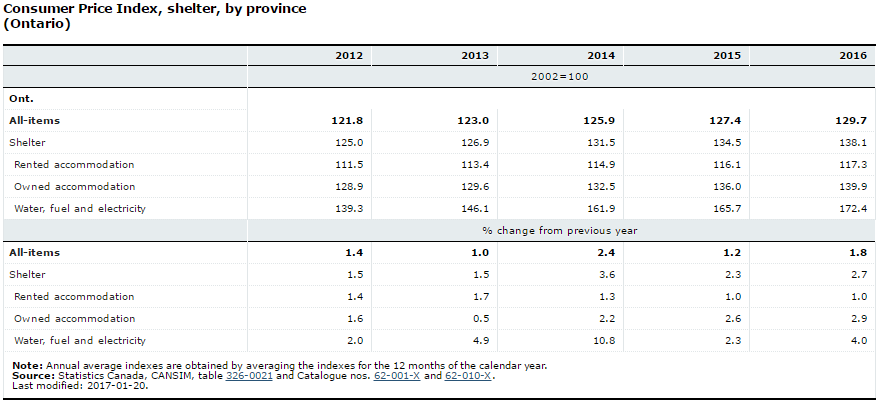

The mathematicians at Statistics Canada that produce the BoC’s CPI measures would like you to know shelter costs in BC and Ontario were up 1.4% and 2.7% respectively in 2016, and “owned accommodation” inflation in both provinces hasn’t cracked 3% since Strange Brew came out.

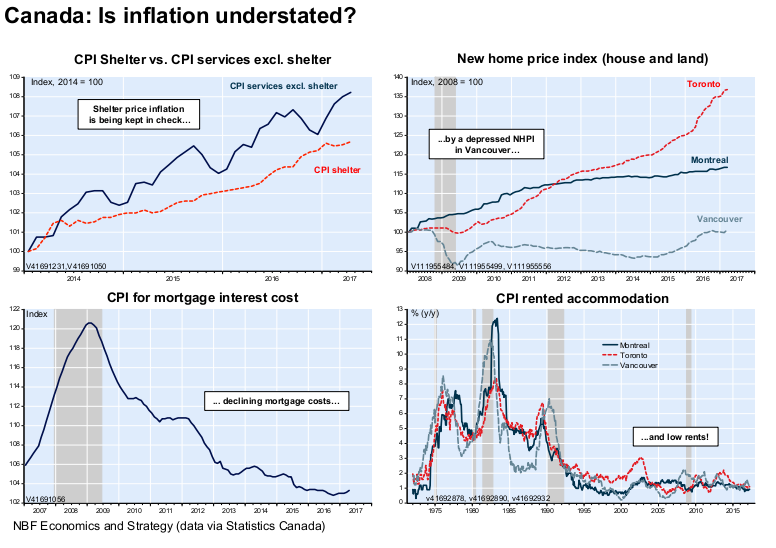

Why such a dramatic divergence in the official statistics and data from actual sales? National Bank had some great charts on this last month:

A report from the consultancy CD Howe identified this threat back in 2012:

“To calculate the owner-occupied housing component in the CPI, Statistics Canada uses a so-called user-cost approach...Assumed prices for dwellings rather than actual prices for houses, and the inclusion of a mortgage interest component, makes the CPI less sensitive than otherwise to housing price changes.”

The piece recommends that Statistics Canada construct and maintain, in addition to the current CPI, an inflation indicator based on a net-purchases approach. While the BoC has been asleep at the wheel on the subject, the folks at National Bank did it for them, constructing an index that mimics the US Case-Schiller index.

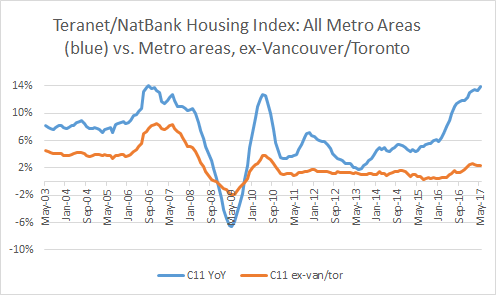

What is interesting here is that the price spike is indeed isolated to Greater Toronto and the area around Vancouver. When taking out those metropolitan areas, the remaining cities, which combined with smaller cities and rural areas have 2/3s of the population, have seen zero real price appreciation this decade.

With shelter costs 28% of the CPI index, you can see how incorporating this data would throw some sand in the gears at the BoC. Changing to that method would add 3.7% to the current CPI, bringing it to a tasty 5-handle. “Governor Poloz….Agustin Carstens from Banxico on line 2….ok, I’ll tell him you’re not here.”

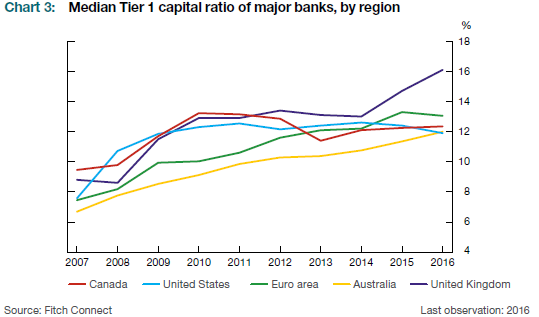

Is this bubble a threat to the whole economy? The financial system continues to look resilient. Canadian banks are 1) big, relative to the scale of the bubble, 2) wicked profitable, and 3) better capitalized than in 2008:

Other financial metrics suggest there is much more resiliancy in the financial system than those in economies that have recently hit the pavement. And as much as I hate to cite Warren Buffett as a barometer, he did just throw a pile of money at Home Capital.

Another factor is that more immigrants are arriving--about 70% of which show up in Vancouver or Toronto. This, combined with the foreign buyers discussed on Monday, are creating a localized scarcity of housing.

I’ll spare you a ton of charts that show low uninsured loan/value ratios but a leveraged Canadian consumer...no smoking guns there--in my opinion they suggest an inevitable, but impossible to time, downturn and/or recession rather than a financial crisis. While Vancouver and Toronto are clearly insane, I just don’t see how that means the whole economy is on the edge of the abyss.

So what is Poloz supposed to do? Here is the menu of options:

- Hike rates--you’re going to need to be aggressive, Banxico-style. Remember, “real” inflation is on a 5-handle, and nobody ever defused a financial time bomb with a couple of measly 25bp hikes! CAD will strengthen materially. Sorry Prairie provinces. Sorry exporters. Sorry oil sands workers and investors. You’re to be crucified in the name of financial stability.

- Macro-prudential measures--BoC has done some here, but nothing aggressive. Perhaps rightly, Poloz is hoping governments continue to do the heavy lifting.

- Sit on your hands and hope someone else fixes it. The current strategy, and prefered solution of bureaucrats worldwide since time immemorial.

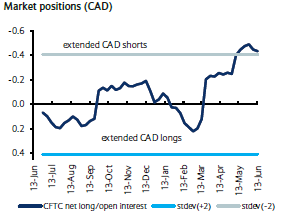

Where does that leave us trading CAD rates and FX?

The market is pricing in a very slow and small tightening cycle from the BoC: roughly 48bps in hikes in the next year starting in Q4, and 66bps in the next two years. By contrast, for the next year the market is pricing in the following moves from other relevant central banks:

Fed: +17bps

RBA: +6bps

RBNZ: +21bps

ECB: The magic 8-ball says, “Ask again later.”

But even rates modestly above the overnight came only after Poloz made some hawkish comments last week--a verbal intervention he thought was so important he did it in an interview with a radio station in Winnipeg. The Wilkins speech was on the tape too, but I’m still skeptical.

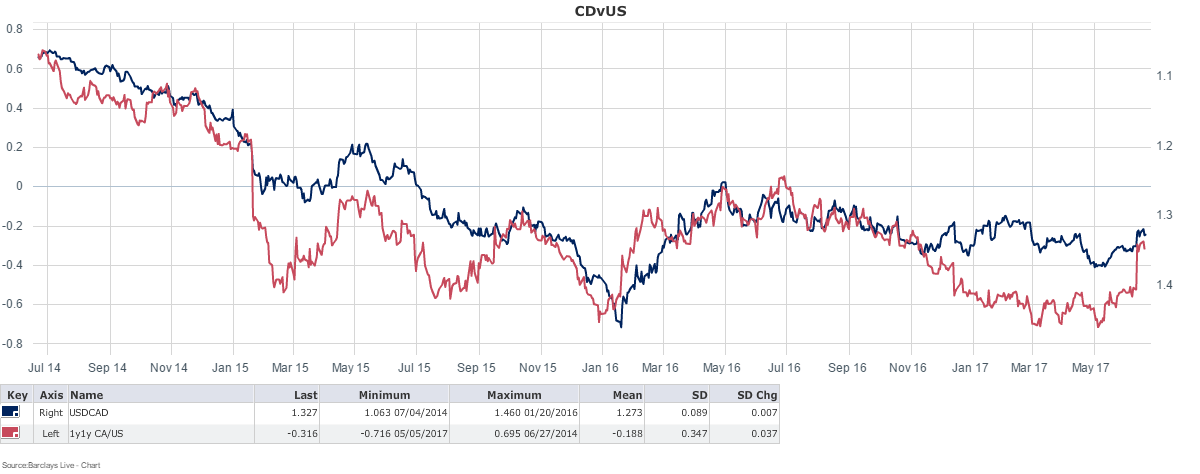

Regardless, the move higher in rates left the 1y1y spread between US and CAD rates near the middle of a two year range, while the loonie still refuses to strengthen.

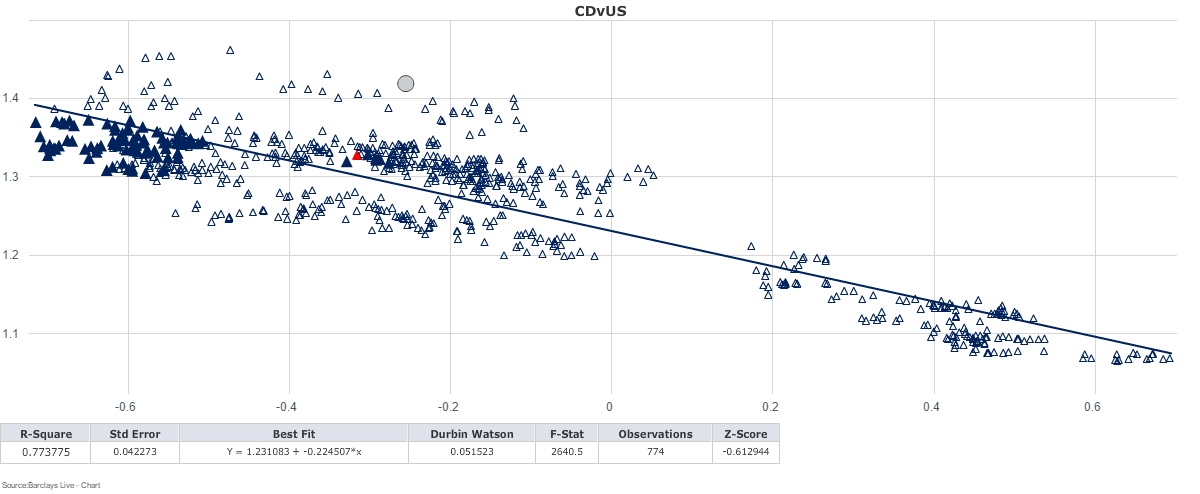

A regression of the 1y1y us/cad rate spread vs. USD/CAD shows...not much. Nothing to see here, move along folks.

Lower oil prices, low interest rates and the smoldering housing price bubble are the likely culprits holding back CAD. I would tend to agree with those seeing a technical bounce/squeeze in oil over the next few weeks, which should nominally support CAD.

- I don’t see a clear trade in rates--I’d more likely be a receiver than a payer. I don’t believe Poloz will deliver on the hawkish rumblings, and foreigners will continue to buy Canadian debt. Steepeners probably make more sense here than elsewhere.

- I’d reluctantly trade from the long side in CAD, more due to valuation, positioning, relative performance given global USD weakness, and the previously mentioned bias towards a s/t bounce in oil.

If those views look inconsistent, it’s because they are. I don’t think we’re at the end of the road here-- I know there are a lot of ridiculous stories of price increases and leverage, but Canada looks like it is a choppy traders’ market rather than a macro opportunity.

Shawn

Teammacroman2@gmail.com

@EMInflationista

Shawn

Teammacroman2@gmail.com

@EMInflationista

65 comments

Click here for commentsThanks Shawn, you're killing it right now!

ReplyBerkshire Hathaway got a big discount on the Home Capital placement and the C$2B loan was in part to replace an existing credit facility. The only thing that doesn't completely match up with Buffet's moves in 2008 is that he didn't buy some hybrid equity.

Keep on keepin' on Shawn... quality posts. Seeing the bubble for what it is, and getting the timing right on the bust are two different things. We should recall that the Fed continued to incrementally raise rates for quite a while until the US bubble popped.

ReplyLB is close to terminating what has been a long term trade in US fixed income, specifically long duration govies. TLT is showing signs of exhaustion, the chart shows TLT near to closing the gap from the Trump election as it crawls higher on lower and lower volume. Positioning shows that shorts in TY and US have mainly capitulated, so we are running out of buyers for the time being.

At the same time we see all kinds of negativity surrounding crude oil and the energy stock ETF, XLE, is lagging the market. A squeeze could be imminent in crude as the conditions for one have been building for a few weeks now. We're not catching the falling knife yet but we do have the Kevlar vestments close at hand, waiting for signs of capitulation among the few remaining bulls.

Great post.

ReplyI wonder though about the Canadian situation:

a) what % of bank earnings is from housing i.e mortgage/home-equity-loans etc

b) what % of bank earnings is from consumer household debt

I read some reports that 25-30% of the GDP growth in the past 10 years in Canada has been attributed to Housing.

Higher rates will put a damper on housing, as well as increase the cost to fund record levels of household debt.

CAD$ may appreciate in the near-term with BoC activity/communications but the macro setup in the not too distant future is bearish for Canadian economic activity IMO.

Its all about delta in poloz comments on rates...2 weeks ago they still were neutral. After wilkins they mentioned rates. 2 year moved big time. Im bullish on cad, especially crosses.

ReplyNice thoughts regarding housing costs and cpi. Low interest rates are the culprit mostly making payments affordable. Also rental yeilds do suck in canada.

Canadian banks are machines. Be careful shorting them, along with auzzie banks. Its not like us or eu banks. They are very well run. But for sure housing related credit growth juices earnings.

Good comments all...I agree on the importance of housing to bank earnings, I thought of that but didn't dig into it. I did see a point on rental yields in the BoC financial stability report--I believe it said 5yr financing costs are 2.8%, and rental yields are 2.9%! Yet house purchases for investment purposes is going up, not down... I would surmise the factors holding back rents are the same holding back the housing market outside Vancouver and Toronto--the broader economy is just not all that healthy.

Reply@leftback, I agree with you as well--given the flatness of the curve and eurodollars, I don't see how yields go much lower without bad data, or gasp...an increase in risk aversion, and on that front the US surprise index is at the lows. Something has to give.

I live in Vancouver, It's crazy here but hopefully it just might start slowing down a little.

ReplyPeople talk a lot about Canadian economic activity and that its mostly confined to Vancouver and Toronto and the rest of the country is flat.

ReplyWhat industries are actually thriving in Vancouver? Timber and fisheries? So the Vancouver RE market is soaring because people are making a killing in the timber and fishers industries? BS. Its all foreign money driving the real estate ecosystem that is driving the entire Vancouver economic area. The trickle down is huge.

Toronto is more diversified but its not like Toronto has turned into Silicon Valley in 10 years that starting salaries for engineers is 100-150K. My mate is a VP @ IBM in Toronto and they pay engineers 45-65K a year, which is the same salary engineers were paid in Toronto area in 1998.

So again, what is the booming industry in Toronto that is driving housing? None. Its all foreign money pouring into RE.

People are under estimating how much this country has depended on this foreign money driven housing boom.

The Canadian banks may not have to foot the bill on the housing debacle because a lot of their mortgages are CMHC insured but their earnings are tied to the housing story and the debt that has been accumulated by Canadians who have felt the need to lever up to participate.

Any way you slice it, things are not looking good for the Canucks.

I don't care if you agree or not..Sir. I'm giving the USA and UK trading session away...Why? well this new show come online its called " Deeply Breaking Bad Little Fella and Kiddy Busson"

Replyhttps://www.youtube.com/watch?v=XZ0Gr6HWbbg

Before I leave , I won't leave the traders here empty handed..

ReplyIf you need someone to help build your trades call on

"Kiddy Busson"

If you need someone to get out of bed each day and help you find alpha call on

"Kiddy Busson"

And if you need someone to protect your alpha call on

"Kiddy Busson"

Chow guys!

It's crazy here but hopefully it just might start slowing down a little.

Replyสล็อต ออนไลน์ ได้ เงิน จริง

goldenslot mobile

Before I leave , I won't leave the traders here empty handed..

ReplyIf you need someone to help build your trades call on

test

I hope Canada gets better soon.

Replyดูซีรี่ย์

รีวิวอนิเมะ

ReplyThanks for sharing

ซีรี่ย์เกาหลี

รีวิวหนังใหม่

ReplyThanks for the information

ซีรี่ย์2021

ดูการ์ตูนDC

ReplyGood and useful information

ซีรี่ย์2021

ดูการ์ตูนซุปเปอร์ฮีโร่

Thank you for sharing Information.

Replyดูหนังฟรีออนไลน์

รีวิวซีรี่ย์เกาหลี

Nice info.

Replyเว็บดูหนังฟรีออนไลน์

New Moview review

ReplyThank you for creating good content for us to read.

ดูซีรี่ย์ฝรั่งออนไลน์ฟรี

รีวิวการ์ตูนดัง2021

ReplyThank you for creating good content for us to read.

ดูซีรี่ย์ฝรั่งออนไลน์ฟรี

รีวิวหนังใหม่ชนโรง

Thank you for sharing good stories.

Replyดูซีรี่ย์ฝรั่งออนไลน์ฟรี

รีวิวการ์ตูนอะนิเมะ

Replythanks for sharing

ดูซีรี่ย์ฝรั่งออนไลน์ฟรี

รีวิวการ์ตูนอนิเมะ

ReplyThank you for sharing good information.

ดูซีรี่ย์เกาหลี

ดูหนังฟรีออนไลน์

ดูหนังใหม่ 2021

Replyดูซีรี่ย์เกาหลี

Thank you for sharing good content

Replyดูซีรี่ย์เกาหลี

ดูหนังการ์ตูนฟรี

culprit mostly making payments affordable. Also rental yeilds do suck in canada.

Replyดูหนังฟรีออนไลน์

รีวิวซีรี่ย์ใหม่ 2021

I won't leave the traders here empty

Replyดูหนังออนไลน์

seriesfin.com

Thank you so much

Replyดูหนังใหม่ 2021

seriesfin.com

Thank you so much

Replyดูหนังใหม่

seriesfin.com

Thank you for creating good

Replyดูหนังออนไลน์

seriesfin.com

ReplyThank you

ดูหนังฟรี

movienewhit.com

And if you need someone to protect your alpha call on

Replyดูหนังฟรี

movienewhit.com

Thank you for sharing good information.

Replyดูหนังใหม่ 2021

seriesfin.com

Replythanks for sharing

ดูซีรี่ย์ออนไลน์

ดูการ์ตูนNetflix

ReplyThanks for sharing good information.

ดูหนังใหม่ชนโรง

ดูการ์ตูนอนิเมะ

Thanks

Replyหนังใหม่ชนโรง 2021

movienewhit.com

ซีรี่ย์เกาหลี

Replyseriesfin.com

ดูหนังใหม่2021

Replyseriesfin.com

Thanks for sharing good information.

Replyหนังใหม่ชนโรง 2021

seriesfin.com

Timber and fisheries?

Replyหนังใหม่ชนโรง 2021

seriesfin.com

I feel really good reading your article. Thanks for sharing the great stories.

Replyดูหนังใหม่ 2021

seriesfin.com

ดูหนังใหม่ 2021

Replytrailer222.com

Thank you for sharing good information.

Replyดูซีรี่ย์ออนไลน์

ดูหนังNETFLIX

ReplyVery Good bro.

ดูหนังออนไลน์

ข่าวหนังใหม่ หนังฮิตติดกระแส

ขอบคุณสำหรับการโพสต์ค่ะ

Replyเว็บดูหนังออนไลน์ฟรี

ดูหนังออนไลน์

ขอบคุณมากค่ะ

Replyหนังใหม่ชนโรง

ดูหนังฟรีออนไลน์

Thank you very much

Replyเว็บดูหนังออนไลน์ฟรี

ดูหนังออนไลน์

Thank you for creating good content for us to read.

Replyดูหนังใหม่ชนโรง 2021

รีวิวหนังใหม่

Very Good bro.

Replyซีรี่ย์เกาหลี

รีวิวซีรีย์ใหม่

ดูหนังใหม่ 2021

Replyรีวิวซีรี่ย์ใหม่

Thank you so much.

Replyดูหนังออนไลน์ 2022

moviehd222.com

Thank You

Replyดูหนังชนโรง2022

dramaslist2u.com

And if you need someone to protect your alpha call on

Replyดูหนังชนโรง2022

dramaslist2u.com

It's crazy here but hopefully it just might start slowing down a little.

Replyดูหนังชนโรง2022

dramaslist2u.com

ReplyThank you for sharing such great information.

ดูหนังฟรี2022

dramaslist2u.com

Nice thoughts regarding housing costs

Replyดูหนังฟรี2022

dramaslist2u.com

ReplyIf you need someone to help build your trades call on

ดูหนังฟรี2022

dramaslist2u.com

I just love this blog. Thank you for such informative knowledge. I also have similar views that I apply in my life and business at Gati Packers and Movers In Delhi. I will start following you for more such great content.

ReplyGati Packers and Movers In Bangalore

Gati Packers and Movers In Gurgaon

Gati Packers and Movers In Mangalore

Gati Packers and Movers In Pune

Thank you for sharing good content

Replyดูหนังฟรีออนไลน์

movie123-days.com

inflation in both provinces hasn’t

Replyดูหนังฟรีออนไลน์

movie123-days.com

ok, I’ll tell him you’re not here

Replyดูหนังฟรีออนไลน์

movie123-days.com

Replythanks for sharing

ดูซีรี่ย์ออนไลน์

รีวิวหนังใหม่

AKBET25 เว็บพนันบอลออนไลน์ ที่ดีที่สุดในไทย สมัครกับเว็บตรงไม่ผ่านเอเย่นต์ สมัครง่าย ได้เงินจริง slot pg ฝาก-ถอน ออโต้ 30 วิ บริการตลอด 24 ชั่วโมง

ReplyWhy visitors still use to read news papersดูหนังออนไลน์ฟรี when in this technological world the whole thing is presented on web?

ReplyThank you for this article. I really like it. รับทำบัญชี

Reply