As I noted last week, Mexico was ground zero in 2016 due to Trump’s double-barreled promise to build “a beautiful wall” and rip up NAFTA. The panic set off by Trump’s rise to power last year only threw gas on the fire in Mexico, which was already burning due to the pain in EM and falling commodity prices.

In local rates, 10y TIIE blew out above 8% in January when Trump twitter-bombed the market--claiming he would rip up NAFTA, implement a border tax on auto imports, and pressure foreign car companies to build factories in the US rather than Mexico. Since mid-February, Trump has become a paper tiger for Mexican risk, and 10y TIIE has retraced nearly 100bps from the wides.

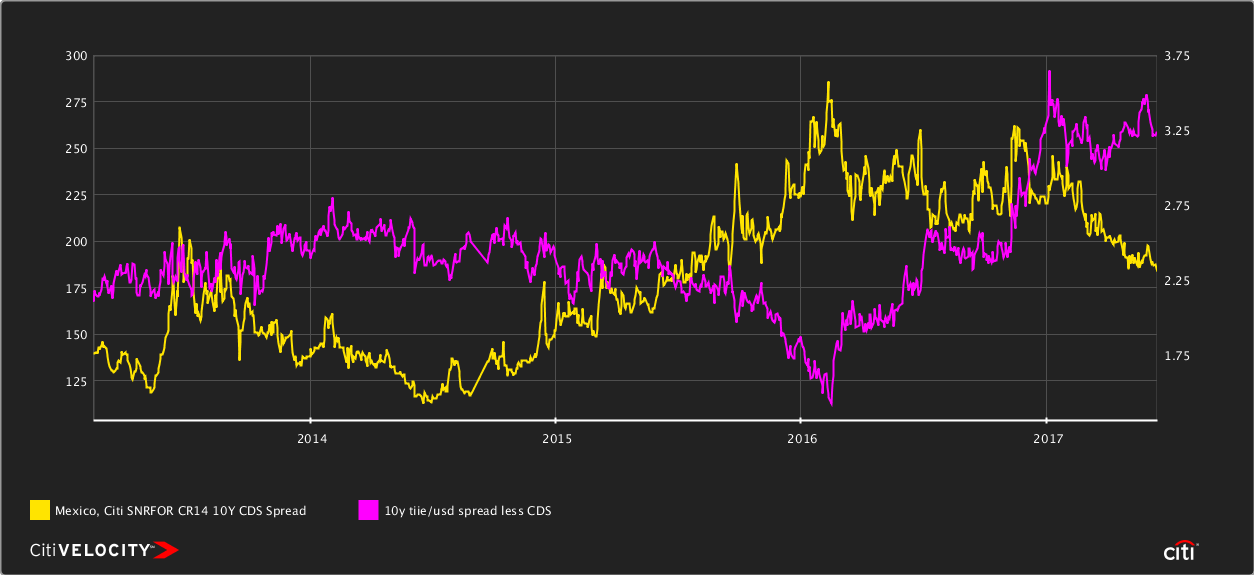

The charts below show that rates are indeed lower, but mostly due to lower US rates and lower credit risk. A reasonable proxy for local rate/FX risk is 10y TIIE, less 10y US and 10y CDS. This spread is still roughly 75bps above mid-2017 levels, despite a reform agenda that has successfully plugged the fiscal gap left behind by the drop in oil prices and production.

I believe local rates are lagging due to a combo of high inflation this year, residual reluctance of locals to move back into the nominal curve, and 2018 election risks--but given the full retracement of other Mexican assets, high real rates, and the potential for an end to hikes or even rate cuts from Banxico, there is still good value in local nominal rates.

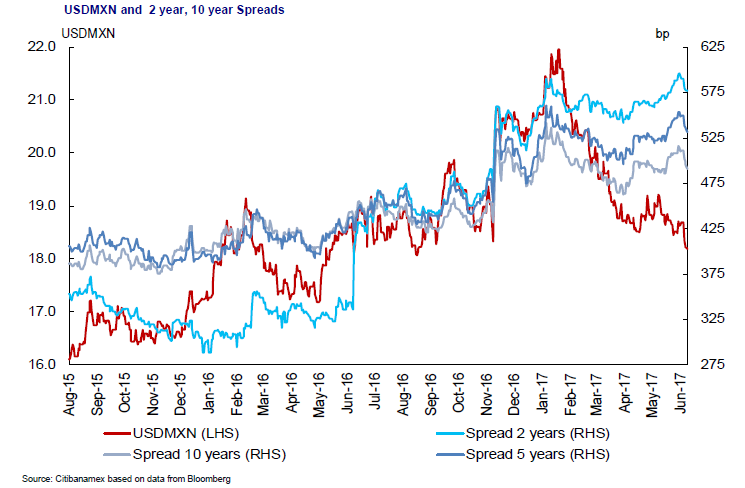

10y TIIE (RHS) and 10y mex/us (LHS) still much higher than pre-election...

...Despite full retracement in CDS (LHS) --reforms are working, but local rates are lagging.

… and despite a full retracement in MXN….which still screens cheap to EMFX on a REER basis

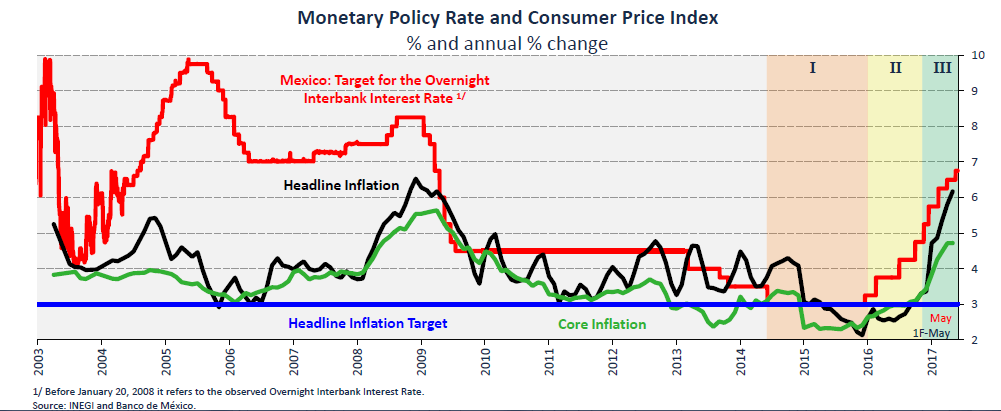

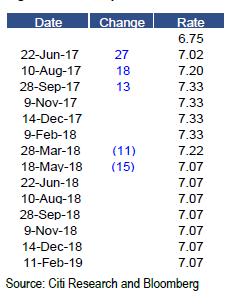

Why has the Mex/US spread been so sticky? The big depreciation in MXN coincided with some local factors to cause a big spike in inflation. The central bank reacted by increasing the overnight rate to 6.75%, a rate reminiscent of the pre-GCF days.

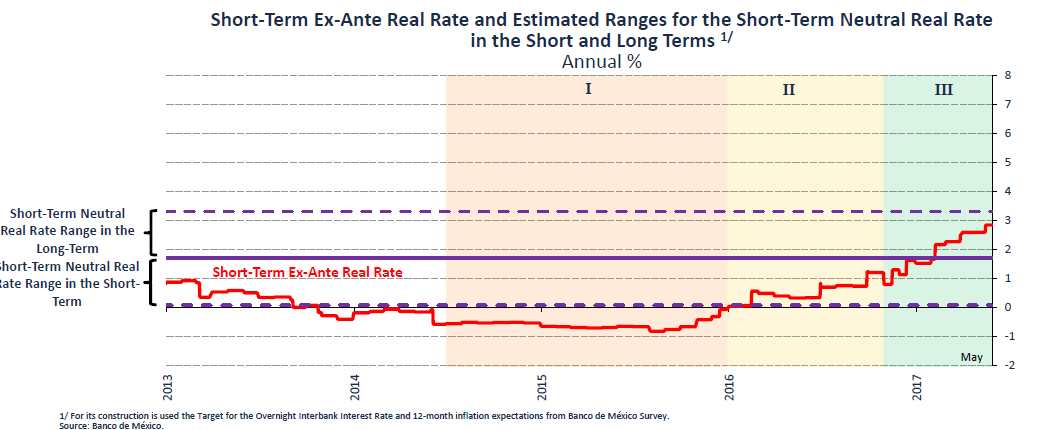

This aggressive hiking cycle has led to very high ex-ante real rates as the central bank seeks to anchor long-term inflation expectations around their 3% +/-1% target--yet breakevens imply no future reversal from current levels of real rates.

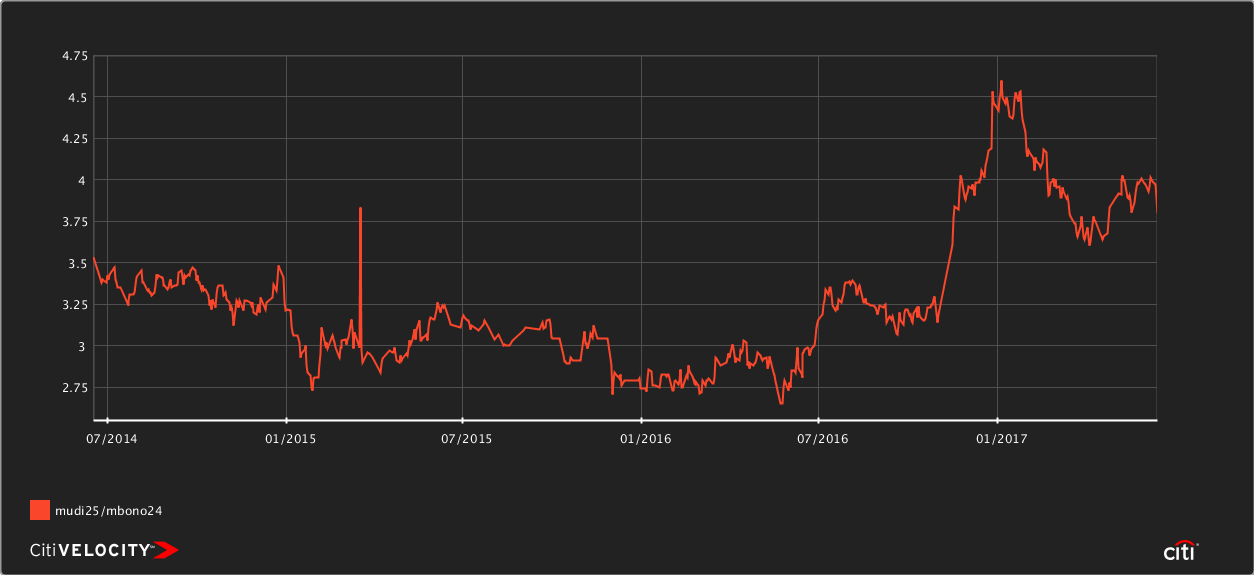

Mudi25/mbono24 benchmark breakevens still at 3.8%

Some would claim Banxico still has some wood to chop there with medium term inflation breakevens still at 3.8%. I see a medium-term breakeven of 3.5% to be a more reasonable inflation risk premium given the high real rate, institutional strength of Banxico and what is still priced into the front end--that leaves 20-30bps in upside in the nominal curve even if you don’t get any love out of lower real rates, which isn’t out of the question given trends in the US and oil.

The long rates trade could also work if the central bank moves to reverse the tightening cycle in the near future. The big reversal in MXN has extinguished the risk that pass-through inflation will contaminate long-term inflation expectations, but nominal rates and breakevens are still pricing in some of that risk. Also, some of the exogenous factors that pushed inflation higher this year are one-offs that will reverse out next year (gas prices and mass transit hikes being the biggest culprits).

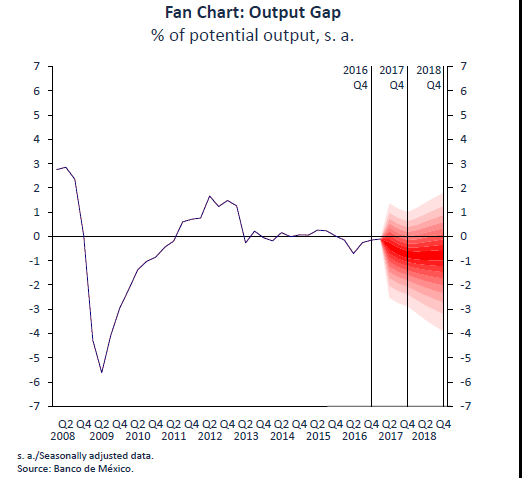

There is also a persistent output gap-- with still listless growth, a flat curve in the US, and a weakening USD, there aren’t many external factors to change that. The important point on this graph below is not only the negative output gap, but also the negative slope in the central bank’s forecast--That is a signal Banxico will cut rates aggressively if and when headline inflation or inflation projections revert to their target range.

And that isn’t priced into the market now--the 1y1y fwd rate is flat to the overnight, despite easing cycles priced in elsewhere in EM.

What’s next? Another 25bp hike at next week’s Banxico meeting looks baked in. The fundamentals argue that could be the end of the hiking cycle--usually that’s a good time to receive rates. Inflation will need to cooperate, but continued slack in the local labor market combined with trends in the US, China, MXN, and commodity prices are supportive of lower CPI figures ahead. More on this in future episodes.

Depending on your global view, the three best expressions of the long Mex rates trade are:

- Receive 2-5yr TIIE or buy 3--7yr Mbonos; curve is flat, but not yet pricing an easing cycle--buy CDS leg tactically as an AMLO hedge

- Receive 10y mex/us spread in swaps

- Receive 10y mex/us spread and buy 10y CDS

What are the risks? You know the drill:

- EM has had a great run, higher inflation in the US could put the fed in (real) hiking mode, which would push USD higher and whack local rates again

- Not to beat a dead horse but vol is in the gutter, which is a powderkeg. I wouldn’t hedge with MXN puts but continue to like the hedges noted last week, or selling COP, CLP or ZAR to lay off EM risk.

- Trump crawling out of his political grave before midterms or Muller drive a stake through his heart, and/or Trump setting fire to NAFTA in desperation.

- The biggest risk is Mexico’s presidential election--the left-wing populist Manuel Andres Lopez Obrador is leading polls, likely part of the reasons locals are hesitant to increase risk. AMLO can, and will, cause more volatility in Mexican assets in the run up to the election in July 2018. The risk to the theme here is that the election will make Banxico slow to cut rates in 2018, even if financial conditions call for it. I’m comfortable with this risk because 1) AMLO’s relatively lackluster showing the the state elections last week, and 2) the political implosion of Trump negates AMLO’s biggest rallying cry. That said, vol will return in 2018. Buying Mex CDS is the best hedge here.

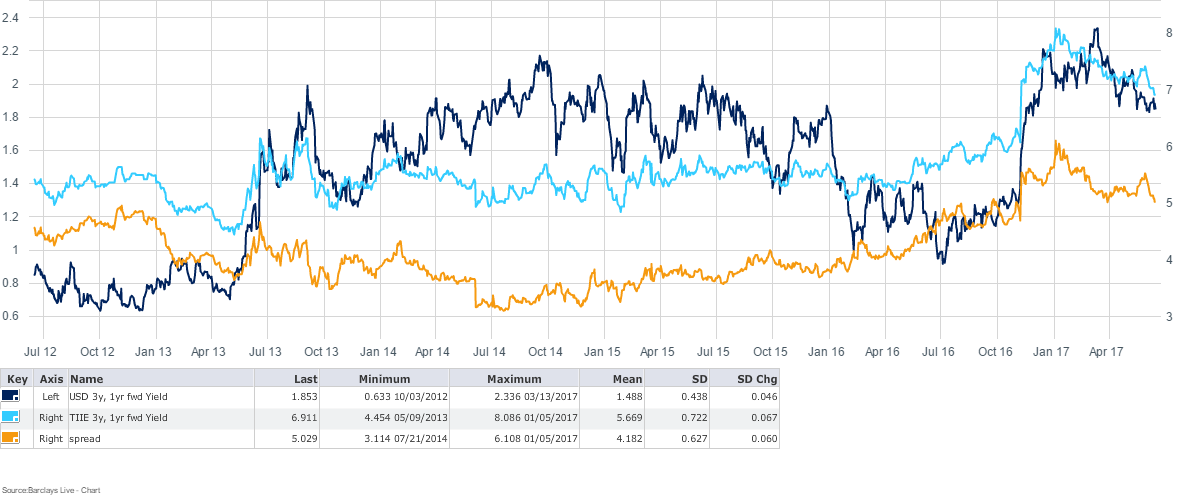

Update (June 16): Shortened up my call on duration after looking at this chart of 3yr, 1yr fwd in TIIE and US. Still some value here relative to November, and this segment will fly if Banxico signals cuts in 2018.

5 comments

Click here for commentsExcellent post.

ReplyNice javascript shawn. Thanks for the post. excellent again. What would you do for 1 trade on a non institutional account?

ReplyLB, re Canada. I think the change in tone of Poloz is a bigger deal than oil or china, which in my view will be contained. crosses look interesting

IPA. Even though I am skeptical that the WFM deal closes so easily, this should put a nail in TGT. Not sure who was buying on the close here. Will look to short on any move up. Meanwhile Costco which trades at 26x forward PE gotta be worried. Sure I know Costco model is great, hard to copy, but nothing is forever. Hoping DLTR gets down into the mid 60's as I think they are the only ones who are not directly impacted.

ReplyI'd usually try to stay on topic, but I'll step in with my Peter Lynch view here--Costco is going to be ok. Most weekends I sit at the cafe having a churro with my kids and watch the constant avalanche of consumer goods walking out of that place. It's amazing. Don't ask me what that means for forward p/e's, though.

ReplyRe: equity or non-inst expressions of lower rates in Mex--not sure on that one, I haven't looked at the banks in a while, Santander Mexico, Banorte and Inbursa are big publicly traded names there. And Walmex is a bellweather.

Thanks for the nice and useful information.

Replyดูหนังออนไลน์เต็มเรื่อง

รีวิวหนังใหม่ชนโรง