This week’s Economist Riff takes us to Argentina. Last week Argentina made headlines by issuing a $2.75 billion in bonds that mature in 100 years, a feat previously only accomplished by creditworthy-ish countries like the UK, Ireland, and Mexico.

This caused the financial media to rend their garments and pull their beards:

Argentina’s 100-year bond: Sure sign of market gone crazy -WSJ/Marketwatch

Alright...I’ll grant these guys it is easy to whack this piñata. Before we proclaim this is this cycle’s version of the AOL/Time Warner deal, Let's look at the facts, and what’s going on beneath the surface.

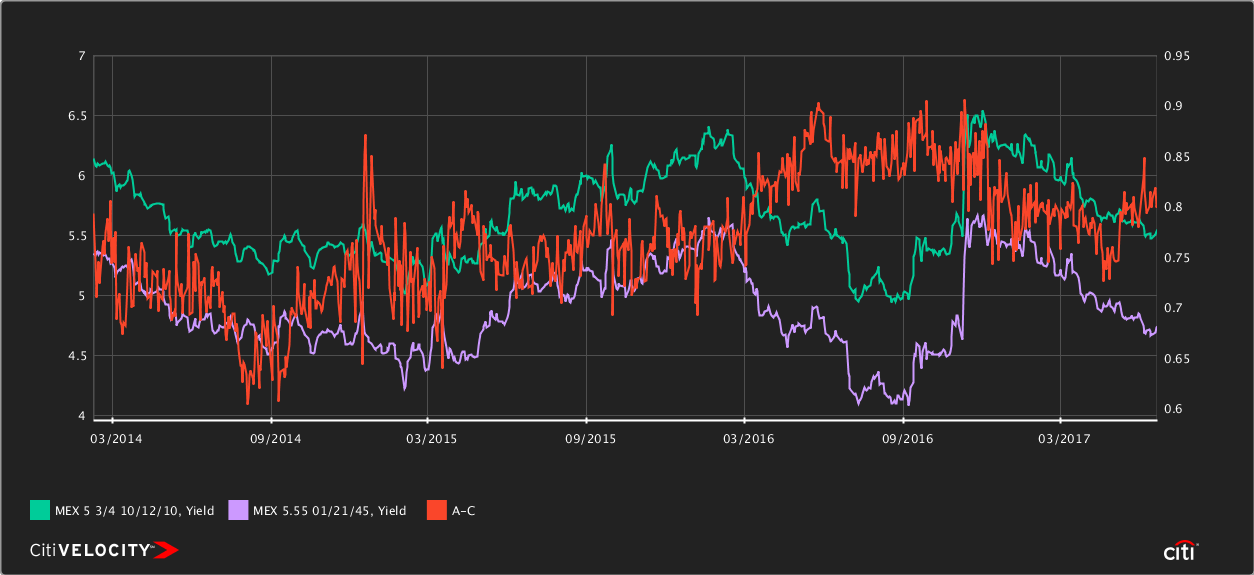

Mexico is a great comparison here because they have a 100-year bond, and if everything goes right in Argentina for the next 10 years, they might reach Mexico’s level of credit spreads.

You get paid an additional 80bps every year for extending to the 2110 bond, a spread that has been relative stable for the past three years, despite material swings in Mexico credit over that time. What is the marginal additional credit risk from 2045 and 2110 relative to today until 2045? I’d argue not very much. The stability of the spread shows the key difference in the relative value of the two bonds is not credit, but duration. All those additional coupon payments add up to about an additional two years of effective duration on the bond, a pickup that rises along with the price of the bond, meaning an investor can make more in both carry and capital appreciation when yields fall while tying up less capital. That is an attractive proposition for a real money account that doesn’t want to sell credit default swaps to gain more leverage, especially insurance companies and pension funds.

The same logic follows in Argentina, where you pick up 60bps and about 1.5 years of duration for extending from 2046 to 2117. That is the point lost on the cacophony of voices decrying the recklessness of lending billions for a century to a country that has defaulted three times in the past 23 years: in the 30 year, you’re picking up something like 500bps over treasuries. At those levels of spreads, there’s already a huge probability of default priced in--the additional 70 years doesn’t make much of a difference. A dollar lent to Argentina for 100 years is worth about a nickel today--so you’re not hoping Argentina pays par to your unborn grandchildren, but rather that they will continue to service that debt over time.

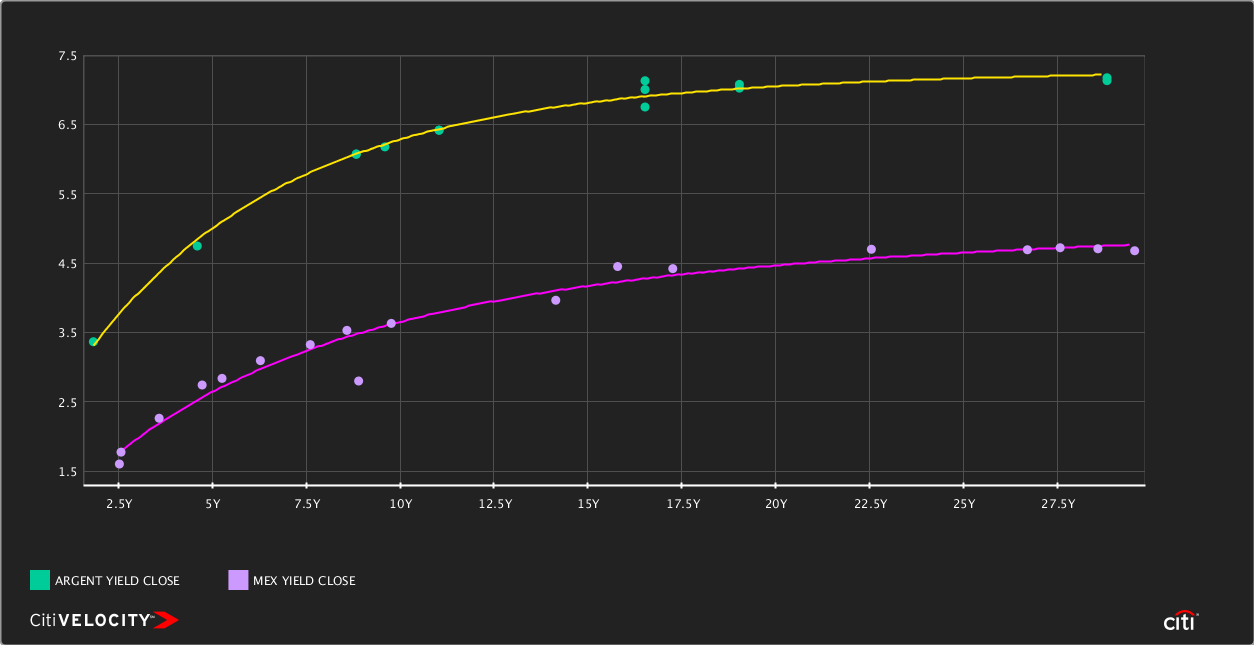

To further illustrate this point, look at the USD yield curves for Mexico and Argentina. Remember, Argentine bondholders hope and dream their bonds will trade flat to Mexico some day.

Argentina has a much steeper curve under ten years, but then flattens out. This is where the credit risk lies--you don’t get paid much for the marginal risk of default beyond this point. This is time period over which you are betting on the success of Macri’s reforms, and betting on him being able to bury the country’s famous habit of returning to populism. If you’re bullish on Macri, the steepness of the curve and sizable spread shows there is still a ton of money to be made here, and the century bond is a great way to express that view.

Macri certainly has a tough road ahead--the market has cooperated by giving him some breathing room with the debt load and inflows to stabilize the currency, which will help stem inflation. But the fiscal reforms necessary after years of profligacy are going to hurt, and it is unclear if he’ll be able to deliver the growth and productivity the country needs. Politically, the Peronists are rudderless after years of being dominated by the Kirschners, so Macri may be able to capitalize on their weakness. The potential upside is huge, so while I’m not as bullish as those that put down $2.75 billion on the country last week, I do believe the future is bright and Argy will continue to be a decent carry trade so long as the broader reach-for-yield trade continues.

4 comments

Click here for comments"Economist Riff of the Week"

ReplyLook at me "kiddy Busson" f##k over another one

Look at me "kiddy Busson" fiddle around in the treasury market mumma son

Look at me "kiddy Busson" fiddle around and crush the hope and dreams of the young

Look at me "kiddy Busson" f##k over another one

Thanks so much for your posts, Shawn.

ReplyThe source of a financial armageddon is taking place right now:

Replyhttp://www.pionline.com/article/20170529/PRINT/170529882/alternative-credit-turning-heads-of-ldi-proponents

Economist Riff of the Week

Replygoldenslot mobile

GCLUB มือถือ