With all of the fuss around yesterday’s Comey testimony, I thought it would be a good time to have a look at the “Trump trades” from the beginning of the year. The charts will show that, as in the pic above, despite continued bluster and gesticulating, the “Trump Trade” has given way to the “Xi Trade”.

After the election, the big one was “Trumpflation.” The idea was that Trump is going to spend a ton of money on infrastructure and defense, leading to more bond supply, higher deficits, higher term premiums and higher inflation. This led to an acceleration in global growth expectations, pushing inflation expectations higher around the world.

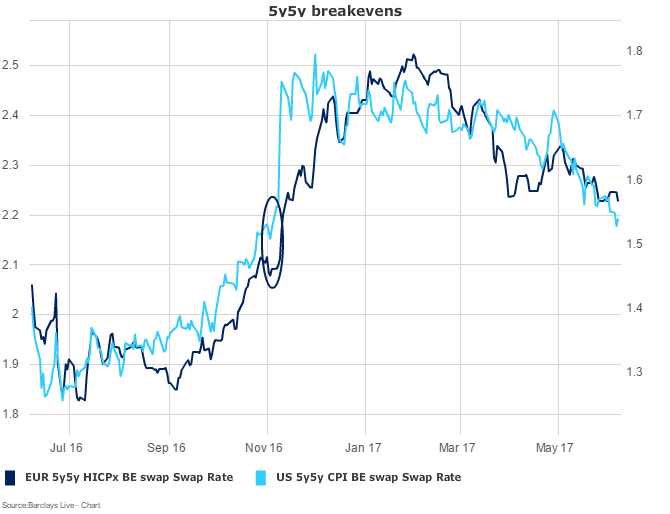

Since November, 5y5y US breakevens have been trending lower consistently. EUR 5y5y breaks took longer to reach recent highs and have been more reluctant to retrace given a better run of economic data. US breaks have retraced the whole move higher since the election, while EUR breaks are still about 10bps off those levels.

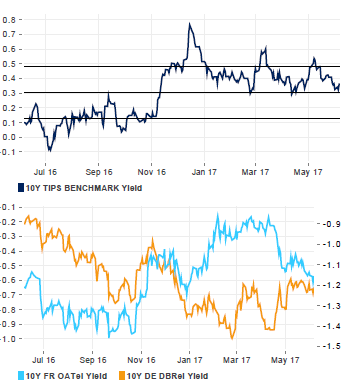

Real yields have a case of the “suppo-sta’s”. They were suppos-sta go higher.

Nominal yields have bull flattened, indicating a quick end to the Fed’s tightening cycle--not exactly a vote of confidence in Trump’s ability to increase growth rates in the US.

Not much to pick from between 10y UST (blue) and the 10y UST/Bund spread (orange).

We were also told USD would stay strong since Trump had finally solved the growth riddle, simply by promising to spend a ton of money to spur domestic demand and business investment. EUR and JPY depreciated hand-in-hand, but JPY has gone sideways while EUR has been ripping. Jens Nordvig, head of Exante Data and former Nomura FX guru, believes there has been a fundamental turn in capital flows back towards Europe. This ties out to my intuition--in 2016 capital fled Europe due to QE and low growth expectations. Now growth has picked up (a little bit, anyway), and the Trump demand resurgence has been exposed as a lot of hot air. The German export powerhouse flexes its muscle again.

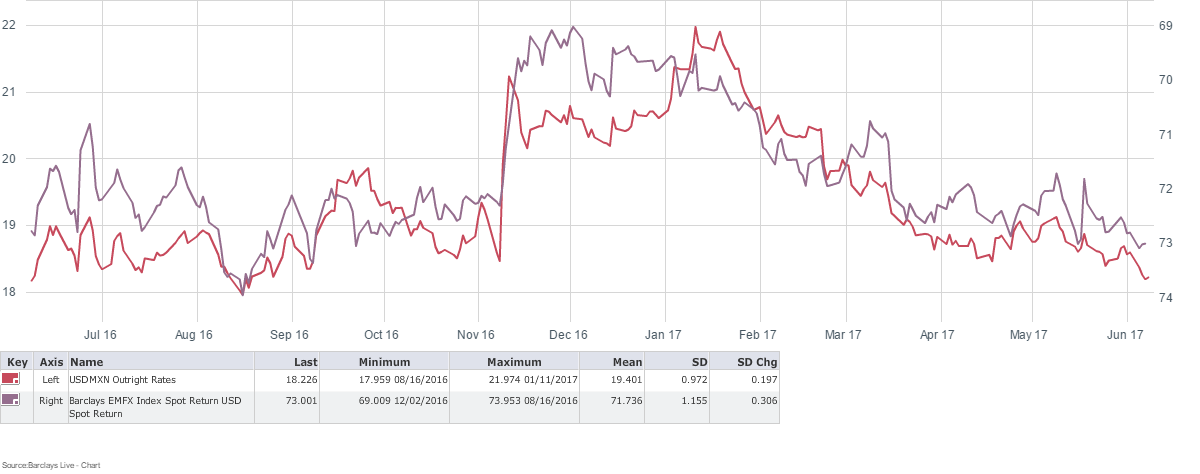

The most famous blast zone of Trump risk was usd/mxn and Mex rates. The peso fell 6% on the day after the election, and after coming back modestly into year end, melted down completely shortly after New Year’s when Trump unleashed a Twitter bomb suggesting he would implement a “border tax” on Mexican auto imports and withdraw from NAFTA. MXN moved opposite of EMFX at large, which was recovering nicely.

MXN (red) vs. EMFX (purple, inverted so it moves the same direction as MXN)

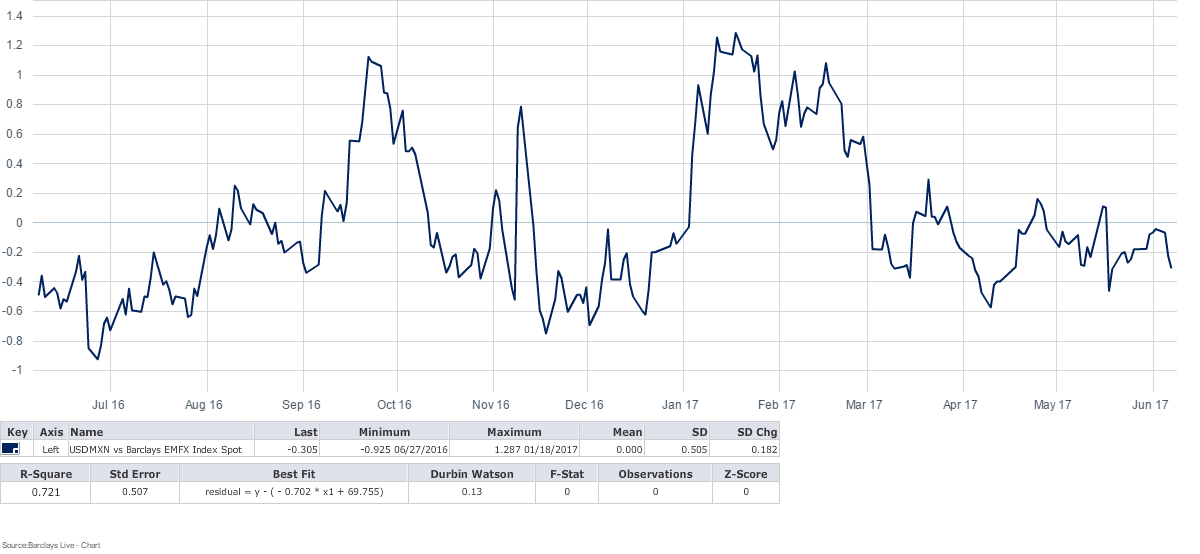

This is a chart of the residuals of usd/mxn vs. the EMFX Index--higher figures indicate MXN is cheap relative to the regression. This shows how MXN has not only closed the gap from November outright but also unwound all of the underperformance relative to the rest of EM complex.

Similarly, TIIE got demolished by Banxico aggressively hiking rates to defend the peso or financial stability, the locals' paranoia about Trump, and corporates with USD liabilities crushing offers in the cross-currency market, leaving banks as huge payers into a market with no bid.

In late February, Banxico implemented measures to backstop the peso and stabilize rates. Those measures combined with very attractive real and nominal forward rates convinced foreigners to buy duration, and local pension funds chased yields lower after moving aggressively into short duration and linkers in a futile attempt to shield themselves from the selloff in rates. These accounts extended duration as Banxico continued to hike and global curves flattened. 2x10 TIIE officially at zero….Bottom line: the herd turned.

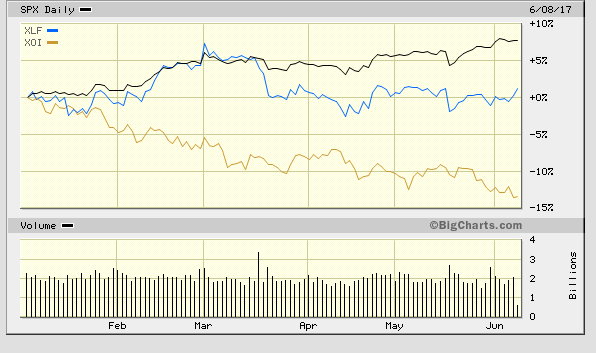

Next was stocks. “Risk on!” Came the cry from equity desks around the world. More spending! Lower corporate taxes! Offshore corporate profits repatriation! Business confidence! Deregulation! Financials and oil/gas stocks led the way, thankful that one of their own was finally back in the White House.

Since the beginning of the year financials (XLF) have chopped around while oil/gas stocks (XOI) have gotten hammered by the combo of a slothful, inept Trump administration and lower oil prices.

Similarly, small cap stocks stood strong after the election--Trump was going to cut taxes, regulation, cancel Obamacare, etc. etc. Sorry, Charlie.

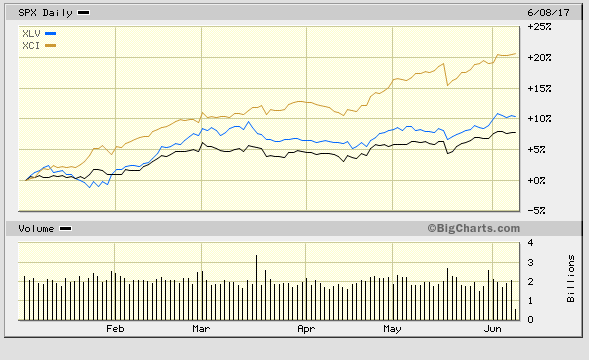

Alright, but the S&P had a great run after the election--why hasn’t it given back any of its gains? The sectors that underperformed in November and December have reversed course--Health Care (XLV), and here’s the big one--technology (XCI). The 20% gain in tech has plugged the hole in the index left by the sectors that led the big move higher late last year. Thank you, Mr. Beta.

And lastly from the equity world, there was Trump’s mantra borrowed from populist windbags the world around, “Putting America First.” A funny thing happened on the way to autarky--an avalanche of money flowed into emerging market equities.

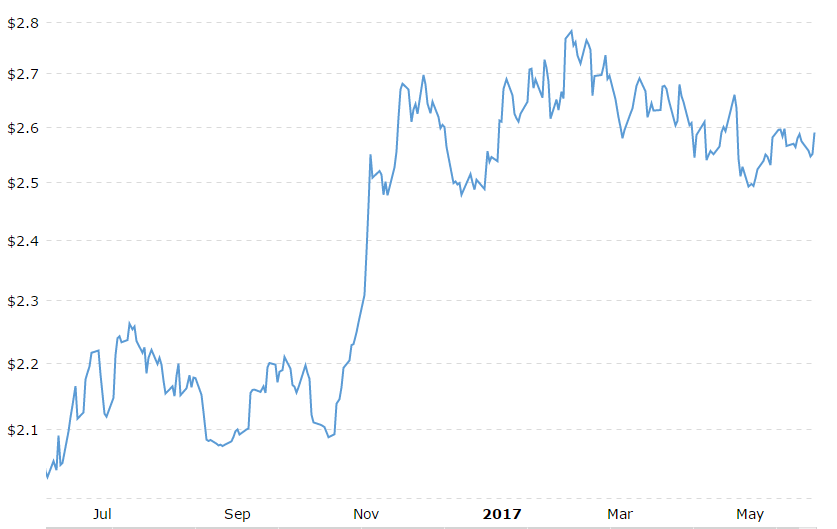

Why the reversal? Copper prices rocketed higher after the election because Trump was going to build more stuff. Here’s one that has held up, but credit goes not to Trump but to the resurgence in EM growth and Chinese demand--the Xi Trade.

Copper (HG1)

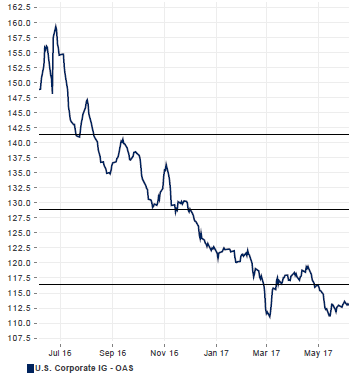

Lastly, there is credit. IG spreads were already recovering after the brutal start to 2016 and the shock from Brexit. They never really took much of a breather, just continued to grind tighter and tighter.

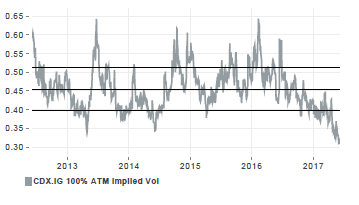

Vol played a significant role in this as well--was the utter destruction of vol one of his campaign promises? IG implied vol has clattered through the lows. Like tech stocks leading the S&P higher, this is credit traders juicing coupons and eating their seed corn.

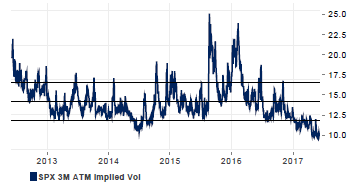

By contrast S&P vol is certainly historically low but hasn’t seen the steep decline of bond and credit vol.

Where does that leave us? I try to avoid crystal ball stuff but here’s how I see it:

- Trump and the US political scene at large: I think he’s done politically--and taken together, the market agrees. Trump is going to be fighting with Congress, Comey and Muller until the GOP majorities get liquidated in the mid-terms. After that his agenda is over, and Democrats will be circling like sharks around a wounded tuna.

- Nominal rates and breaks have priced fiscal stimulus at zero, which close to the right price given the way Trump has frittered away his modest political capital. But the flattening of the curve and unwinding of hikes by the FOMC beyond this year shows markets are somewhat complacent about inflation picking up on its own accord. That being said, don’t hold your breath.

- EUR can continue to benefit from a sea change in capital flows after several years of outflows.

- Mexico: We come here today to bury the “NAFTA withdrawal” trade. Again, if Trump could have put together a coalition of domestic manufactuers, unions, and xenophobes to rip up the treaty, he missed his chance. The TIIE curve will invert as growth stagnates and the inflation spike fades, but Banxico will be loathe to cut rates too quickly ahead of the 2018 election. Election risk will become salient around the end of the year when polls should start to become more reliable as it becomes clear who PRI and PAN will run against AMLO, but Trump’s ham-handed political circus will take some of the air out of AMLO’s campaign.

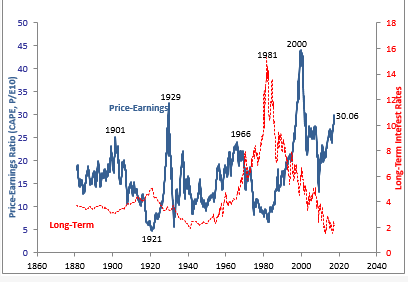

- Stocks--Can’t stop the Feeling! Just dance, dance, dance…. Seriously, corporate profits will have to “show me the money” to keep this train rolling, but that hasn’t stopped the market before. This probably would have gotten me fired as an equity manager but I believe value is indicative of future returns--and I can’t see how this chart and current demographic and geopolitical trends end in a reasonable return on risk capital, unless 1929, 1966, and 2000 were really good times to buy stocks.

- IG, HG, vol--see above. Taken together, real money is getting squeezed and is increasing risk by buying tech, high yield, selling vol etc. to keep the ball rolling. The longer it goes on, the smaller the exit door gets.

- EUR, DXY, EM--the prior two bullets notwithstanding, I think the flows can keep going--I prefer EM rates over EMFX--but I’ll want the hedges I discussed in Wednesday’s post in my back pocket. The resilient copper chart illustrates global demand is still stronger than it was last year. This is the new paradigm for 2017….the Xi Trade.

TeamMacroMan@gmail.com

@EMInflationista

15 comments

Click here for commentswow nice post shawn. Gonna take me sometime to go through it all.

ReplyThanks for the MYR comments Johno. I'm still worried that asian trade is peaking soon, so looking for trouble first with the usual suspects. Figuring it will show up in MYR first. so far so good I guess.

Nasdaq getting the hammer today. Of course I covered some rather nasty losing short positions yesterday in your favorite "machine learning" stock which is now down big. Ah... But Nasser sell off seems quite contained to Tech leaders. Russell up on the day. Lets get a few more days of this nasdaq sell off before we can make any conclusions.

Nicely done, Shawn.

ReplyYes, Trump seems done. Totally inept. However, I've seen it argued that Virginia and New Jersey governors' races later this year will be a wake up call for the Republicans, who will then pass some tax cuts to avert the mid-term massacre to which you allude. Whether they do that, and whether it works, will be seen.

Re Europe, the EUR is already priced richly to regression models on short-term drivers, i.e. the flows are reflected in the price (I've just this week realized all my PnL in the 1.10-1.12-1.14 EURUSD flies I wrote about when EURUSD was <1.07). I do see a new narrative emerging, with "morning" in Continental Europe thanks to Macron, on the one hand, and the Anglo-Saxon countries with their broken social contracts and desperate electorates on the other. However, that "morning" is perhaps more to do with Xi than European politicians in that China's growth cycle is benefiting European exporters now. That impulse is going to start fading away (looking at lead-lag relationship between China's credit impulse and global PMI). We may have one more small gasp of credit loosening in China to see that things remain stable through November, but I think, overall, Chinese growth now slows. So, just when the European political narrative gets more constructive, the external growth narrative (to which Germany is sensitive) goes in reverse.

abee, regarding Asia, one thing to keep in mind besides China is the smart phone cycle, which should boost activity in H2.

I went long CLN7 today and sized up a petro-currency bet yesterday/today. We'll see ...

abee, sorry to hear about NVDA, you've been stalking that one for a while. I got burned on my NQ shorts way too many times on this last leg up to even try. Was watching it dive today with jealousy and doubt, but as soon as they came my way and started loading up on XLE my day was made :) So it looks like a rotation for now. We've been talking about big money hiding in large cap tech. It came out of nowhere and just snowballed. Agree, need to see a trend develop first, otherwise it's nothing but a small correction. We may be aided by JBTFDippers to short the retracement. Heck, they stepped in and bought it into the close 100 pts straight up. Let's hope it tries to cheer the Fed next week and does its usual dance for the quadruple witching. We are going to get our chance, imo.

ReplyJohno glad you brought up smart phone cycle. This is a lay up. Every major iPhone release they do the same thing. Buy into the summer sell into the fall. Dram is all Samsung holding back supply and micron/ Hynix with their peckker in their hands trying to figure 3d out. Anyways my point is that it's all a cycle. Smart phone growth isn't in a secular uptrend, in fact it's pretty flat. Paying peak multiples when margins are at peaks, I dunno. . Data center spending is real and does make the business longer term more diversified but I don't think it's immune to slow down either. I'm trying to track that as well. Same for autos.

ReplySo Huwai is selling more expensive phones now, benefitting all the suppliers. But tech hardware is still a deflationary business, Imp...

I wish I could be like citron. Too bad I was saying the same things a while ago on nvda. Great company. Gpu computing is for real. I love it. But do you really think everyone needs to pay $1000 for the latest card which gives all of the margins. Most companies don't even have the data cleaned to be used in deep learning projects.

Kinda feels like 2007 Goldman quant blowup. I am thinking this rotation is gonna screw with many quant funds. Might buy some Russell puts soon.

Outstanding post, Shawn. Stick a fork in him, he's done.

Replyabee, in order for me to believe in a true rotational reason behind Fri tech rout, I would have to see much higher volume on the beneficiaries: XLF and XLE.

ReplyQQQ volume was gigantic, highest since Aug of 2015, AMZN flash crashed @ 14:50 Eastern and they were pretty much throwing all tech out of the window in droves indiscriminantly. It was a day all the latest going trades got reversed, including the stinker XRT getting some undeserved love. It all looked like machine driven, I totally agree with your thesis.

GBP looks interesting as a long here. One of the bullish narratives about the election was that May would have a >50 MP majority that would allow here to side-step the hard-Brexiters in her party (given the MPs who ran, I wasn't so sure of that). The outcome of the election is that soft-Brexiters (specifically the DUP) can't be side-stepped. What am I missing, on the political analysis?

ReplyWhile the politics may in fact be a positive development, I concede that 1) shorts have room to re-build, 2) the property and finance industries are headwinds, 3) consumer spending should head lower as real incomes are pinched, 4) negotiations have to begin. Assuming all that was in the price before Thursday (a questionably assumption), and my political analysis above is correct, then GBP should be higher, not lower.

Favor GBPUSD for now and maybe switch to -EURGBP ahead of the Fed. Don't want to get runover on EUR leg if there's an especially favorable reaction to the Macron parliamentary win.

johno .. I'd just tweeted

ReplyRight then. Less Mayism, no socialist gov., Softer Brexit, no Scot indy2, media full of 'it's a disaster'... all GBP buy signals

So I have.

Another busy weekend with 12 Open House signs at every residential intersection in Richmond Hill and Markham. The same houses are still for sale. People may stubbornly not reduce prices (yet) but they will once the reality that recent prices are of the past not to be seen again for a very long time.

Reply12 of about 40 people who come to qigong meet up every friday and tai chi on Sunday are long 3-4 houses each as investments. Then each of them have a network where they too are long 3-4 properties and so on.

Next recession is going to humble a lot of Canadians.

My take on the election and GBP is that in the longer term of this government we now expect not just softer exit negotiations ,but more uncertainty over whether the Tory party can actually hold together without another election. Without a doubt the harder exit is of the table because of the DUP.

ReplyAnother and potentially more important consideration is the Tory party fiscal platform is going to change considerably. If this election showed us anything it is that there is no appetite for more austerity. The fiscal program will be to spend more on key issues that sunk this election. Frankly , given the options for raising more revenue are limited I'd say this probably also means borrow more to spend more. Overall I would say that eventually becomes a weaker currency. Maybe not right now until the dust settles and policy becomes clearer ,but eventually so.

johno: I would second you and Polemic on sterling here, sold some EURGBP this morning actually.

ReplyStill, while on balance I think sterling has been punished a bit too hard in recent days, it's hardly a clear-cut situation. Worth keeping in mind that:

(1) While the election outcome is tilting the range of possible brexit outcomes more towards the softer end of the spectrum, I still cannot see an *actual* soft brexit (as in, EEA membership for instance) as the final end point. This would require accepting freedom of movement, which would be seen as too politically toxic. So I think the softening will rather take the form of consensus building around a (possibly very) long transition period. (Still a good thing obviously.)

(2) Also, while chances of a "softer" outcome (as defined above) have now increased, arguably the risk of the negotiations completely failing has as well. This is partly because the ongoing kerfuffle risks leading to major delays, leaving even less of the nominal 2 year article 50 timeline available for actual negotiations, and partly because selling the inevitable unpopular compromises with the EU to parliament will now be harder.

Reason I nevertheless like GBP here is because I think the increasingly explicit calls for a long transition period / overall softening of the hard-brexit approach are a genuine new development, whereas the negatives above were largely in the price already. The timeline was always going to be too short to agree anything but a framework agreement (hence the need for a transition period), and the Tory majority was pretty thin as it was... With that said, so far the market seems to disagree with me... We shall see.

Speaking about the market disagreeing: what's your take on EURNOK these days? I've stayed in the trade but hedged with a longer-dated CL short. EURNOK seems mostly correlated with spot crude prices, so I think of this as a backwardation play with the NOK cheapness vs oil as an extra kicker. Is not working great so far but still believe that with patience this should do fine in the end. And it's certainly doing better than the outright play I had initially... :-)

The Tory core favouring a hard exit are going to lose their argument going forward. The DUP and indeed the Tory Scottish block alone would now guarantee that. Labour are going to almost have a coalition seat at the table on some issues as the price of their support. It really is not that much of a stretch to see how this government could become untenable. In another election Labour might actually be in. Frankly, I would rather be long BRL than £ in terms of political uncertainty risk.

ReplyMy Expression

Replythanks for the blog very interesting

Yes, Trump seems done. Totally inept. However, I've seen it argued that Virginia and New Jersey governors' races later this year will be a wake up call for the Republicans, who will then pass some tax cuts to avert the mid-term massacre to which you allude. Whether they do that, and whether it works, will be seen.

thanks you!

gclub

@11:58

ReplyMore than doubled from the crash

http://www.marketwatch.com/investing/stock/HCG?countrycode=CA

Nice post..!Thank you for posting this blog.

Replygclub

gclub casino online