Ponch...if we get there in time, we can put that hawkish central banker behind bars once and for all!

So what's next for Mex rates? Can Ponch use his street smarts to subdue inflation, capture the gang of hawkish central bankers and bring joy to the hedge fund world? Indeed, the next move for Banxico is a cut. As discussed yesterday, there is probabilistic path for rate cut, with 50bps gradually priced by the end of 2018. 100bps is in the cards in 1H2018, but it won’t take much to convince the central bank to hold off or slow-play rate cuts to see how the election pans out.

To complicate matters further, we don’t even know who will be running the central bank in 2018 (on either side of the border). The two leading candidates are Alejandro Díaz de León, who is currently on Banxico’s board of governors, and José Antonio Meade, the current finance minister. Both are eminently qualified--one could argue Meade is the more dovish of the two, but he may wind up running for president under the PRI banner.

If Diaz de León is the choice, plenty of influence will be held by Manuel Ramos Francia, Banxico’s current vice-chairman and Mexico’s answer to Stanley Fischer. Ramos Francia places a high premium on financial stability, and together with Carstens can be credited with implementing a number of measures to backstop the Mexican currency and financial system over the past ten years--up to and including the aggressive hiking cycle that took rates 400bps higher since early 2016. That could keep rates higher for longer, especially if the Fed is still hiking in 2018.

Lastly there’s NAFTA. I don’t have anything to add here. I still see little evidence Trump is going to blow up the system--if he were going to do it, he would have done so already. But this time bomb will only be defused by an agreement--one that doesn’t look on the horizon...and the Mexican election clock is ticking.

Which segues nicely into the biggest risk in the market: Victory in next July’s presidential election for Andrés Manuel López Obrador, a leftist candidate that is a weird combination of Donald Trump, Lula and Jeremy Corbyn. AMLO has a small lead in a race that will be splintered between four candidates.

The trouble is...I think he’s going to win. Sure, he could step on a political landmine as he has in past elections, but the recent global record of populist candidates versus either establishment or technocratic candidates is not good at all...Macron might be an exception, but even he was an outsider running against the establishment. Mexico has all the ingredients for a populist/nationalist victory: a charismatic candidate, an external bully, a stagnant economy, a system rife with corruption, and a long history of poverty, inequality, and large segments of the population that feel “left behind.”

In 2006, Mexico had a long string of strong growth resulting from high oil prices and strong manufacturing demand. Felipe Calderon ran a technocratic “don’t mess this up” campaign, and still only beat AMLO by a whisker (and some think that is overstated by two whiskers). Today, from a political perspective (corruption, crime, education, etc.), pretty much everything Mexico had going for it in 2006 is worse. And AMLO is still here and ready to “drain the swamp”. How will the fractured establishment compete with that?

The market is underpricing the potential for inflation to come down...yet also underpricing AMLO risk. That points to good value in steepeners.

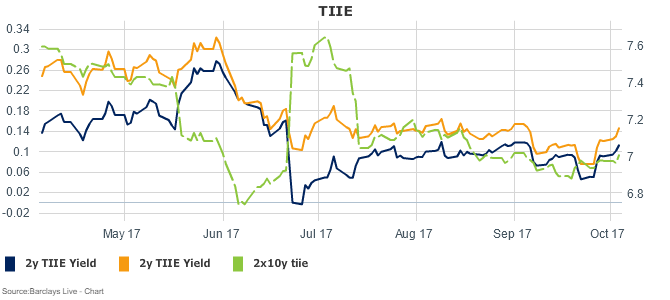

2x10 TIIE is still really flat--and while that may be true of virtually any curve in the world, there aren’t many curves where one can make a convincing case for significant rate cuts in the next 1-2 years. The flat curve is also a function of EM local flows at large--a portion of which can and will hit the exits if and when AMLO extends his lead in the polls. 2x10s is currently at 9bps--three months from now 40bps is much more likely than an inverted curve.

13 comments

Click here for commentsCheck out the volume on SVXY. Pretty much dried up. Look at it before every previous selloff. Classic! Added some puts today. Feel like a complete moron shorting new highs. Sometime you have to look stupid for a while.

ReplyHey, I resemble that remark.

ReplyIPA,

ReplyWhat strike price/timeframe are you using on the SVXY puts?

Great Unknown, I am long 80/55 and 75/50 Jan 18 put spreads.

ReplyFeels like the easy part of long Mexico is done. Rates not going lower so easily even though we all know they can. They want fx stability foremost and dxy still looks good to me from the st as a reversal back to 200 day or so. It's all about U.S. rates Imo, just follow their lead. Let them get over extended before u fade.

Replyabee, it's possible that DXY will go build the right shoulder of inverted h+s with a target of 92.70 as support. Would not mind buying it there for a s/t trade. Here, at 94 (neckline), not so much.

Reply@ abee, indeed, that's why I think there is more value in the steepener, where the long end will exhibit a higher correlation to US rates, while the front end will be anchored to inflation and monetary policy. two hikes from the FMOC in 1H2018 certainly throws cold water on the banxico easing thesis...question is, will the UST curve take a hint and steepen?

ReplyI just want to know Abee, how furious are you on that DXY trade. Are you as fast and furious as my White Crane Spreads Wings movement. Are you as explosive as my Single Whip. Or are just as relaxed as my Brush Knee Twist step.

ReplyThanks IPA!

ReplyIf you do your steepener Dv01 neutral you will be long ~5x more 2s than 10s... Given as you mentioned 2s have negative carry; the Dv01 neutral 2s/10s steepener is still negative carry (you are only reducing your negative carry by 20pct by doing the 2s/10s vs being long 2s)...

ReplyFantastic post! The possibility of an AMLO win is what has me side-lined in MXN rates currently and it's fascinating hearing your case for why he wins. Yes, the trade carries negatively, but the 10Y leg is really there to protect against the AMLO outcome, as I understand it. I'm not following the politics as closely as I should, but might the PAN/PRD alliance announced in September cut the chances of AMLO taking power? Re NAFTA, my guess is as good as anyone's. Issues highlighted in the press are content minimums in autos and Chapter 19 elimination. If NAFTA collapses, I suppose cuts get priced out, but maybe Banxico treats as a 1x external adjustment and doesn't hike further?

ReplyBeen pruning the book lately, e.g. exited -USDRUB yesterday, but adding to +EURCHF via some DKO options offering interesting payoffs. It's "Morning in Europe." I really hope the dollar bulls turn out right (I'm way longer USDs than I'd like) and we get some rally here. Warsh plus the Treasury cash build (140b in Sep and 300b cumulative through Oct, before running down again) could afford a great +EURUSD entry this month. It's funny. Macro players look for their trades in rates and FX first, but the real Trump trade is apparent looking at NOC or RTH share prices. Clearly, the biggest beneficiary of Trump playing madman and reneging on deals is the defense industry. The world outsourced defense to the US and since there were at most only one or two (deemed) needs for military deployment at a time, this was a very efficient arrangement. Now that no one can trust the US's security commitment, everyone has to spend on arms. We'll have a highly inefficient buildup of redundant military capability. This is a coup for the most advanced military tech industry in the world -- the US's. Not that I'm in that trade. Too disturbing to see how that technology is used, e.g. Yemen.

@ ben, i didn't want to get too deep in the weeds on carry/roll, but if you look at 2x10 TIIE 3mo fwd, it is (or was yesterday, anyway) 19bps, having bounced off of a low of 7bps over the summer, and topping out at 45bps in July. I figure 50bps isn't out of the question there, w/ a 10-15bps downside (driven by a bull flattening s/t or simply eating the negative carry over time). To your point on the carry/roll cost of the steepener relative to a front end receiver--sure, it's a good point and exactly why I lean towards receiving 2y--but I think the steepener leaves you net short rates (per the point I made to abee above) which works like a charm on days like today when us rates are widening and USD is strengthening.

Reply@ johno, your thoughts on the military industrial complex reminds me of the plot for the first Ironman movie.

Reply