I loved watching the Six Million Dollar Man when I was a kid. On the playground we would make that cool sound he made when he ran really fast or lifted a truck off the chest of a helpless victim.

We can rebuild him….We have the technology….the budget is limitless….crazy money...six million dollars of the best cyborg-tech money can buy.

Indeed, inflation is a thief in the night. Six million dollars certainly doesn’t go as far as it used to...and even less so in Mexico, where inflation is running well over 6%.

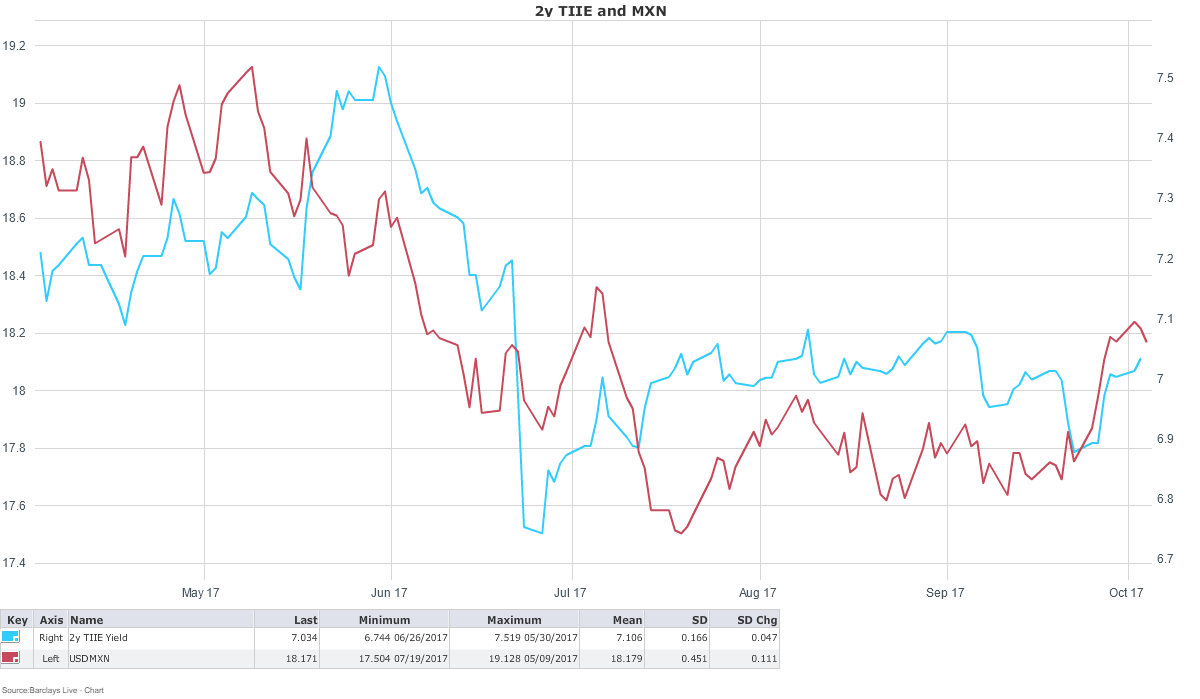

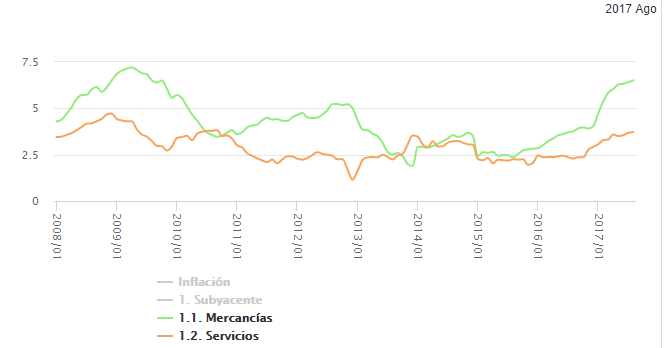

Yet there is light at the end of the tunnel. The front end tightened 30bps early this summer when Banxico went on hold (gratuitous self-promo plug here, and here), which coincided with a most joyous period of EM enthusiasm--MXN strengthened about 8% from May to late June, which gave traders the ammo to price in cuts in the overnight rate. Since then, vol died and both MXN and front end rates have been largely range bound.

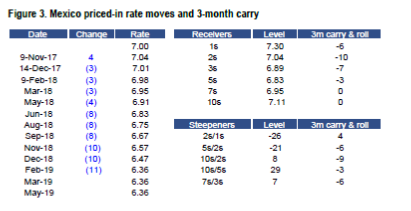

The market has agreed on a probabilistic path for the overnight rate--gradually lower rates consistent with the belief that Banxico will cut modestly sometime in 2018. Given risks around the election, this can be summarized as a roughly 50/50 chance of cutting 100bps or staying on hold.

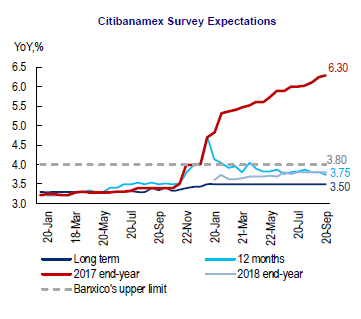

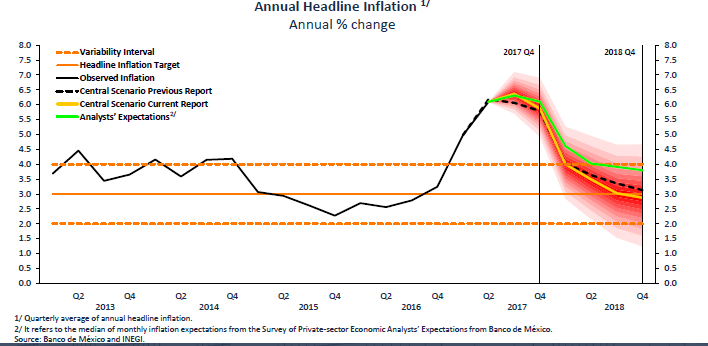

But inflation is 6.66%, higher than most people expected earlier this year (myself included). Year end expectations are still stuck at 6.3%.

Yet several factors are foreshadowing a steep decrease in inflation in the coming months:

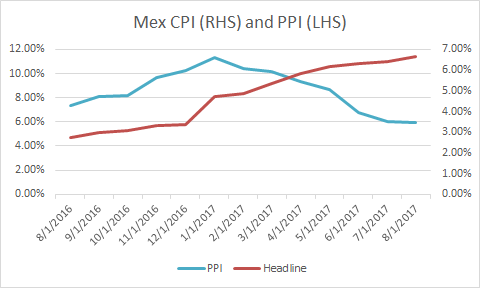

#1: PPI is a leading indicator for lower headline CPI. PPI saw a dramatic increase earlier this year that was primarily driven by increases in energy prices and the depreciation of the currency in 2016 and early 2017. Those factors are mean reverting and will likely seep into consumer prices in the coming months.

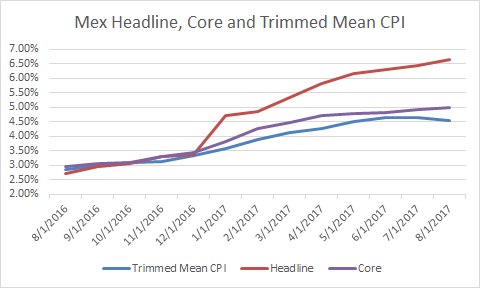

2) Trimmed mean CPI is already falling from unspectacular levels, and the gap between the core/trimmed mean indices and headline has gotten even wider after the gasoline price hike in January.. Another positive leading indicator for headline CPI.

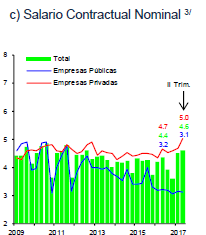

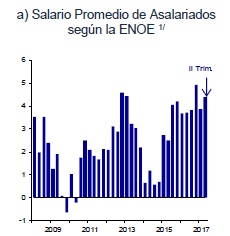

3) The recent price hikes in non-core products have not pressured wages higher. These charts show the negotiated wage hikes (left) in the private, public sectors and overall (the red, blue, and green lines, respectively), and the average salary hikes in the formal sector (right). In each case, there is little to suggest there is any second round impact on wages due to high inflation, and real wages are well into negative territory.

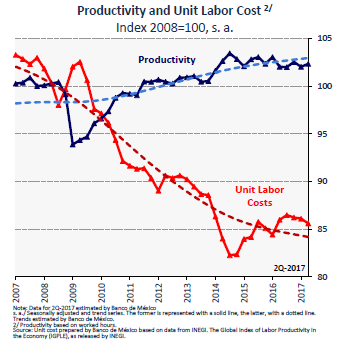

Indeed, unit labor costs have been falling as well (although not as fast as they have in the past)

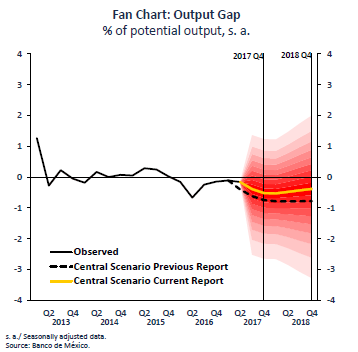

4) There is still a negative output gap--while Banxico’s forecasts are more optimistic than they were earlier this year, there is still no positive slope that would portend demand driven inflation pressure..

Negative real wages, a sluggish economy, and a negative output gap gives the central bank scope to cut rates--if inflation allows. Banxico is more optimistic than the market--and their previous forecast-- about inflation falling quickly next year.

5) Product level analysis shows no evidence of second round effects--in fact, underlying inflation may be overstated at current levels.

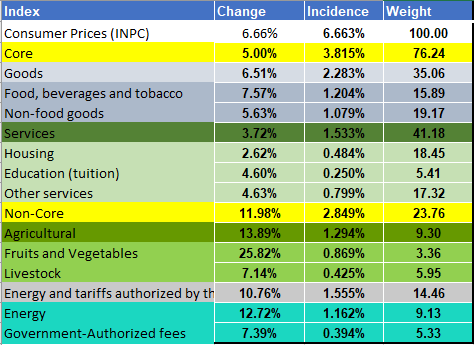

This is the YoY change in inflation and attribution of underlying sub-indices.

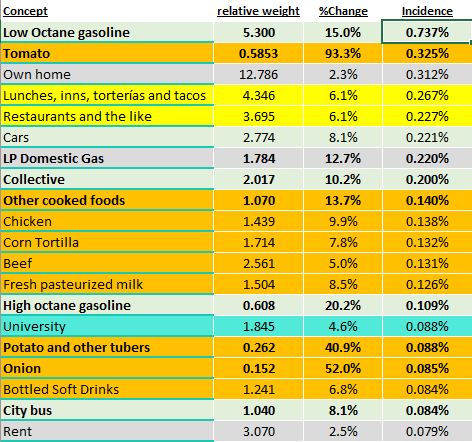

Even a cursory look will show the brutal jump in perishable fruit/vegetable and energy prices. These two factors alone, which comprise only 12% of the index, contributed 30% of the increase in headline inflation.

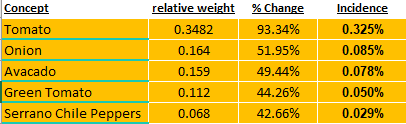

The top 20 products ranked by their incidence in the index over the last year shows just how large the impact is from one-off moves (gasoline, bus fares, “collective”, which are ubiquitous transport vans like the airport "Super Shuttle" in the US) and crop-failure style food price hikes (tomatoes, potatoes, onions). Meanwhile, components that would indicate a frothy financial system like shelter (“own home”, in the literal Spanish translation) and rent are well below the 3% midpoint of the inflation target.

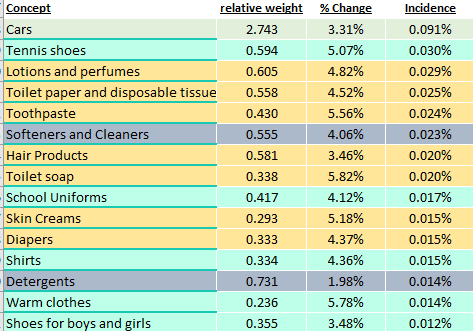

6) Merchandise inflation is high--but driven by imported goods...and MXN fuerte!!

Yet another component stands out in the data--non-food merchandise has moved up significantly as well despite the low underlying wage and growth data. Just as important, drilling into the data from Jan-Aug 2017 (thus, after the gasoline price hike) shows these prices have been sticky, moving up at an annualized rate of 5.6%. Is this evidence of second round effects?

I continue to believe the answer is no--product level analysis argues this is being driven by the lagged impact of the depreciation of the peso. This is the ten highest contributors to non-food merchandise inflation in the Jan-Aug 2017 period:

What do these products have in common? They are mostly imported goods. Given the rally back in the peso in the first half of this year, and the stability/low vol more recently, price increases in this group are set to mean revert and will likely settle in around 2-3%, which could lead to a 40-60bps negative contribution to the headline index.

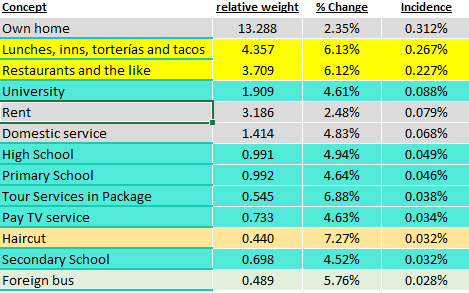

7) Services inflation is high--but driven by food inflation

Services inflation hasn’t blown out either, ending August at 3.7%. In fact it never cracked 4%--another indication that underlying inflation pressures are subdued. Services inflation has indeed increased, but it is coming off a low base.

If we take a look at the top contributors to services inflation, a couple of things stand out.

If we ignore the dreaded haircut inflation, the two big factors were are “taquerias” and restaurants, where prices have gone up over 6% and have contributed nearly 50bps to the headline number.

What to take a crack at why restaurant prices have been going up? These are the 5 products with the highest YoY price increases:

At risk of perpetuating a cultural stereotype, they use a lot of this stuff in Mexican restaurants... Mexico is in the midst of a Guacamole Crisis! If I were AMLO, I’d use that squeeze on small business owners to whack PRI like a….ah, I better not.

And restaurant owners got no help from beef and chicken prices, which were up 5% and 10% respectively. The secondary impact of headline inflation is being felt in very transitory, competitive sectors--and underlying inflation is practically non-existent. These price increases are going to roll off, and competitive retailers amidst tepid domestic demand will lower prices.

These micro factors will combine with high interest rates, fiscal tightening and a stable peso bring further confidence in the credibility of the inflation regime. Putting all those factors together, inflation can fall below 4% in Q1 2018, well before what is currently built into sell side inflation surveys.

Stay tuned for what is all means in part two tomorrow...along with a sweet CHiPs reference.

Shawn

TeamMacroMan2@gmail.com

@EMInflationista

Shawn

TeamMacroMan2@gmail.com

@EMInflationista

7 comments

Click here for commentsShame there were not more comments on what was a really good analytical piece. It's outside my personal trading sphere ,but I enjoyed the methodology employed nonetheless.

ReplyThanks...that's what I was going for--I know this type of thing is outside the scope of what most of y'all trade but I wanted to lend some insight to how I reach conclusions in a market I think I know pretty well--with any luck it inspires some similar thinking on how to generate ideas that are outside the consensus in whatever markets you are trading. Good luck!

ReplyNice. A few observations:

Reply1. It's rather quiet on the blog, (Macro Man Comment-O-Meter at extreme lows, correlates with low vol).

2. Sentiment is extremely bullish, not to mention complacent, with regard to equities.

3. Contrarian indicator: Economist Cover This one has a very reliable history!!

4. Vol selling has become more popular than prescription opioids.

5. Record short position in Treasuries.

6. Unbelievable melt-up in small and micro cap stock ETFs (IWM and IWC).

7. VIX dipped to 9.13 this morning, because jobs number is tomorrow and all numbers are Goldilocks numbers.

There have undoubtedly been worse terms to put on some contrarian trades. Long vol and Treasuries for a start.

wow. hadn't seen the economist cover. Classic. I will write up a click-bait post on that one for after NFP and we'll see where it takes us.

Replyper point #4, you're making the assumption that short vol and the increase in prescription painkillers is uncorrelated?

Circling back to the post, long vol and/or UST would be a good fit for the 2x10 mex rates steepener I'm pitching in part 2 of this post.

Shawn, you certainly did achieve what you were going for. Don't associate silence with people still off on the many tangents you have sent us on. Especially the people that are behavioural amongst us,and are old enough to question why the six million dollar man teamed up with bionic woman instead of Wonder Woman.

ReplyGrateful.

a few days ago my son said, "Dad, who are Charlie's Angels?" I said they were a team of crime fighters....there are a couple of things I remember about them, but I thought it best to leave it at "crime fighters" and move on with the day.

ReplyEager for part two. Always appreciative of your posts!

Reply