This is one of those times I am glad I am not paid by the word. I was in the car on a long drive this evening and heard the soporific tones of NPR’s Kai Risdahl going through the day’s financial results.

“Down day for the Dow today, closing off one-tenth of a percent.”

“Down day for the Nasdaq as well, closing one-tenth of a percent lower”

“The S&P 500 fared no better, closing down four points, just under two-tenths of a percent.”

Really? I mean...really NPR? Couldn’t you have just saved us all a little time and said, “everything basically unch...again.”

There was a time earlier this year (and for the prior decade, I guess) when I would wake up, fire up my laptop to get the overnight price action. For the past three months I just hit snooze, read the Wall Street Journal, and figure prices will come to me if they are worth looking at.

Today I spent some time thinking back to 2006 as a part of a piece I am working on about the potential downside of a victory by the populist candidate in the upcoming Mexican presidential election. Turns out markets were hustling pretty good back then! There was a fare degree of vol….but that had done nothing to shake the complacency of years of monetary quaaludes and financial accumulation. There was vol….and there was the BTD mentality...but it took until at least 2007, arguably right into the weeks just prior to the Lehman bankruptcy in 2008, before it was really all over. Investors had to have their throats slashed. There was no possibility of a soft landing.

“We are at a wonderful ball where the champagne sparkles in every glass and soft laughter falls upon the summer air. We know at some moment the black horsemen will come shattering through the terrace doors wreaking vengeance and scattering the survivors. Those who leave early are saved, but the ball is so splendid no one wants to leave while there is still time. So everybody keeps asking--what time is it? But none of the clocks have hands.”

In late 2006 my boss taped that quote to the wall above his desk. In a good-natured act of part-mockery, part-admiration, we found a clock with the company logo on it, broke off the hands, and nailed it to the wall above his terminal. Both the quote and the clock sat in that same place in 2008 when colleagues were literally stopping at the bank on their way home to withdraw cash in case it wouldn’t be open the next day.

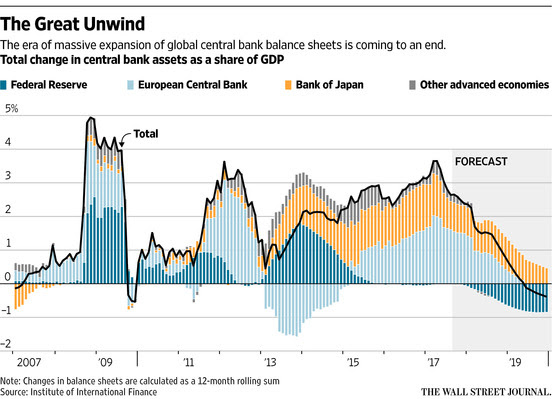

Right, so “The Great Unwind”. This chart caught my eye in the financial paper of record earlier this week:

I would have lost a nickel on this one--I was a little shocked that the ratio of the change in central bank assets to GDP was at the highest levels of the decade early this year...and is only just not starting to come down. But look at the slope of that line...steep. We all remember back in 2012 when the Fed was ready to sound the all clear….only to see the growth and inflation go down the chute again in 2013. Perhaps the steep negative slope of monetary accommodation and the wheezing of the global economy weren’t uncorrelated events..but it is also self-evident that correlation was not forecasted by the monetary authorities in charge of the printing press at the time.

So while it is boiler plate Fed-speak, it came as a mild surprise to hear the Atlanta Fed Governor Rafael Bostic say this yesterday in a speech on the subject of balance sheet “normalization”:

“On balance, the limited market reaction to the rollout of the Fed's new balance-sheet policy leads me to conclude that financial market participants do not view it as a significant tightening of conditions or a hindrance to economic growth….I don't expect financial market conditions to be significantly affected in the coming months by balance-sheet reductions.”

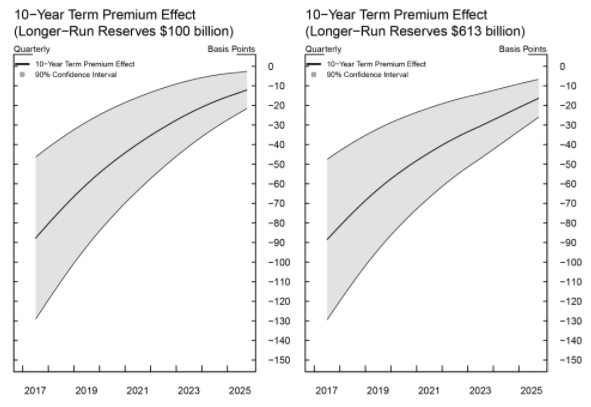

There’s so much wrong with that statement I don’t really know how to approach it. In the interest of journalistic integrity, let's stick to the facts. Or failing any facts, let’s stick to what the Fed has told us already about the impact of QE on long-term rates. Back in April, a gang of economic pirates at the Federal Reserve said, “Avast, ye scurvy dogs, ye olde term premium rests at the bottom of the sea in Davy Jones’ Locker, 100 basis points below the point where Captain Ben skewered the hull of the wee ships sailed by risk-averse landlubbers.”

Ok, maybe not just like that, they were economics PhDs...but they did highlight how balance sheet normalization will cause an unwind of their estimated 100bps in compressed term premium wrought by the Fed’s QE programs, which doesn’t even count knock-on impact from the ECB, BoJ, and BoE asset purchase programs that may or may not be wound down over the same period of time.

I think the steam in the economy and increased supply effect from balance sheet normalization will eventually steepen the curve--right now the market has voted in favor of a repeat of 2013, where tighter conditions will lead to a slowdown in growth that will force a reversal to more accommodation.

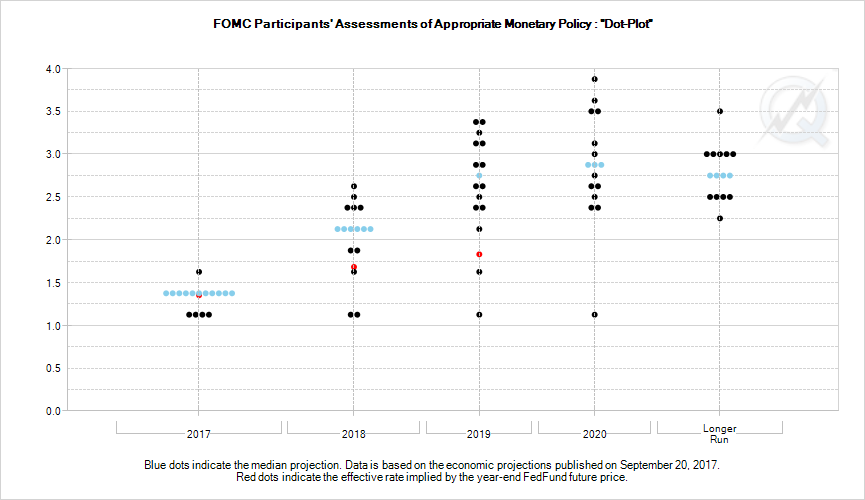

The same economic wonks (the nerds, not the governors) at the Federal Reserve are forecasting a fed funds path that looks like this...

The Fed governors decided to split the difference with those forecasts and those of the market in the September SEP.

Given the growth and wages data I noted earlier this week, and some good reasons to believe that inflation is being sandbagged by some one-off effects, I think there is good reason to price in a path close to the “dots”...say nothing of the nerds’ “dots”!

So yeah, I can hear Al Edwards laughing already….ice age, I get it…but his latest piece did mention that a more hawkish Fed led by Warsh would be his choice to try and defuse this credit driven time bomb. Yet the Fed at large, as illustrated by Bostic's speech yesterday, prefers to stay at the party a little longer. I still believe as my old boss did...you can’t defuse it...people won’t leave the party until the black horsemen crash through the window, slash the throats of the guests, and pillage the house.

But maybe, just maybe….a steeper curve would convince a few party-goers to call it a night.

Shawn

TeamMacroMan2@gmail.com

@EMInflationista

Shawn

TeamMacroMan2@gmail.com

@EMInflationista

7 comments

Click here for commentsThe trading house seed investor will keep coming back for more because his kids have got no brains. All walks of life can make dollar trading foreign exchange. Yeah, you made it to the top with that team of traders. I'll be in South East Asia putting together a trading model all alone to trade this market all the way down to bottom when that day comes. Happy to be broke , alone, and allowed to find winners my way.I'm going to get up every morning and go for lovely swim at the beach , then have a lovely breakfast without any contactable means of anyone finding me. Then I'll put it all together for the rest of the day, every day.

ReplyShawn, thank you for reminding us of those turbulent times. Seems like people's memory gets shorter with every crisis. I also ran to the bank, stopped putting on new positions, covered some shorts and withdrew some money because I did not know if the funds in my trading accounts would become inaccessible. It's funny how for some of us the instincts kick in and we start thinking clearly. In hindsight, I may have panicked and should have shorted more. I guess you could say I left the party early. But those who will tell you they sold the top and bought the bottom may also be the ones who never put any significant money on those actual trades.

ReplyLooks like a few more guests may be arriving at the ball this evening, courtesy of CPI miss.

One last thing... There is a good amount of smart people who are now asking how large the repatriation of overseas cash stash would be. What took so long? I've seen several estimates and I am sure the number will continue to fluctuate a bit. One thing is for sure - it is far less than anyone thought.

i agree on the repatriation issue--it is a probability (of tax reform passage) of another probability (the applied tax rate) of a derivative (how much $ is out there) of another derivative (how much would be brought back). Call your local swap spread trader for details.

Replyhaven't dug into the CPI figures but amazing that the curve just continues to flatten. It's as if the market is saying, "the fed will insist on a policy mistake, and inflation will be like this forever." Could be, but maybe they'll just take Evans' advice and kick the can down the road.

2009 was an amazing time to manage money. I remember in January or February of that year it seemed really, really likely the feds were going to nationalize Citi and BofA and clean house. If you wanted to take the other side of that, yeah, congrats I guess...after the market bottomed in March and Bernanke claimed he saw "green shoots", there was a decision to make on whether or not to buy into the hype--and I agree with Macro Tourist's post yesterday that mentioned it was the massive stimulus from China that got the ball rolling again. Without that, commodity prices may have stayed in the gutter leaving a number of countries precariously close to sovereign default.

Yet it was also a time when ever decision felt like a career threatening one. Pick your poison, i guess.

So that BLS CPI release was less than inspiring. Real wages DOWN on a seasonally adjusted basis. Shawn good article, quick question. On the feds implied glidepath it lists an instaneous forward rate. Where is it on the graph exactly? Apologies if I'm missing it. A socail engagement last night is causing me some issues today, haha.

ReplyAnyways, anyone have thoughts on curve inversion possibilites. (A crash would allow market prices to clear, worth it?) CB's went scorched earth policy on the rates market, we all know this. In doing so the price discovery mechanism doesn't exist as I write this. So, what is going on? I agree with the premise being made by some regarding foreign bond markets and how the so called "anchoring" to US rates travelling along the curve could be the culprit. Manipulation of term premia exists, no doubt, but I don't think the anchoring alone could do this for this long. IMO value added import/export paradaigm, GSC's, shadow liquidty, and modern currency invoicing/hedging techniques have played a larger role than many think.

These off-shore entities that have popped have only facilitated the increase in global liquidity. However their role is (IMO) key. Example being the HKMA, PBOC, SAFE, BOJ group that now exists. Swaps, NDF's, dabbling in the spot market. If economic warfare had a kind of hall of fame for currency operators the names YANG Guozhong and PAN Gongsheng will be first in line to be inducted. They are willing to do anything they could challenge Nomura bank to greatest ever.

These off-shore facilities lend to state linked dealers, brokerages, SPV, and corporations who in turn help alleviate local concerns about currency risk, costs, $ shortages, etc. (alleviates $ shortages and acts as cap controls) These entities also provide excess dollar reserve acces to banks, SEOs, SWF'S, etc.

I'm at a bit of a loss to even describe capital marekts right now. It's fun to be challenged like this, but when older CFA's (level 2 for me) say that the CFA they took is completely irreevant now. "They should have trained us on funding and wholesale market, central banks, and market structure." Not sure if anyone else knows a few CFA's, but they are proud as fuck (worth it or not) and love that alphabet soup, I was kinda shocked. Anyways, looking at positions in commodities, Equities, looking to get exposure to healthy Italian banks, NGX7, $DXY, ALL long positions. Not sure about timing, but after the 19th congress I think China faces stiff headwinds. So I think they will take a chance to devalue.

Shane Cameron, really glad to see someone else here with bullish view on nat gas.

ReplyCrude is going to try and get above $52 and go for $55. XLE will get above $70 in that scenario.

I'm in your corner IPA! I think it's set to do some work to the upside. Petronas just scrapped a 36B investment in Canada due to reg filing. Now they want to enter the US because they know the Americans will actually sell it. Seems like people are sleeping on this transition phase going on in the world. Some countries want to end fossil fuel usage completely. This is just awful leadership by poltiicans in these countries. They are not even close to a transition like this. So, in the meantime energy like nautral gas will be the go to. It's even a PR win for leaders because they can boast they are making progress. I'm all sorts of long-term bullish on comodities. Price points will be crucial because it seem the rest of the world is fucking broke man. P.S. weren't we told that coal was dead? Anyone been watching the demand for coal? Crazyyy

ReplyThere is over 300 million people in America , and there is over 50 million people in England,and you can drag a dozen million over from France. Find someone else.

Reply