In one of last week’s post, I made some off-handed remarks about what makes a good macro trade, or in that case, what doesn't. Yes, you need a big picture view. You need complacency, stupidity, regulatory dislocation, misaligned incentives, or some combination, to generate the market mis-pricing necessary to score big when there is a catalyst to set the tinder ablaze.

Reading the newspaper over the weekend, I got thinking about the Czech Republic after the anti-establishment ANO party won big, putting their pseudo-Perot type figure Andrej Babis in line to be the next prime minister.

I thought the big story would be the large share of the vote won by anti-establishment candidates in this election and last week’s election in Austria. If you look at the type of candidates that are winning elections in Central Europe, it is consistent with the global trend towards liquidating the establishment, more so than necessarily far-left or far-right movements. Look at recent history: the United States, France, South Korea (sort of, by South Korean standards anyway), and Czech Republic have elected decidedly anti-establishment figures, while non-traditional and/or radical parties or candidates have done well in the UK, the Netherlands (Wilders and the Greens still gained seats at the expense of the establishment, even if not as many as predicted), Czech (again) and Germany.

Indeed this is the story of 2017, and will continue to be later this year and into 2018 when we will get potentially market moving elections in Mexico, Brazil, and Italy--with an election in Hungary already in the bag for their nationalist prime minister, Viktor Orban--who arguably kicked off this trend in EMEA back in 2010.

Yet after kicking the tires on Czech assets over the weekend, there doesn’t seem to be much stress about politics. The far bigger story this year has been the decision by the CNB to float the koruna, allowing it to appreciate versus the euro. And as so often happens, the really juicy macro trade may be a layer beyond the current potential for policy tightening in the Czech Republic.

First, getting an award like this is always a little awkward. It is like winning coach of the year in the SEC West. Sure, great job...but come on...look at the neighborhood.

Yet the CNB is a strong, highly credible organization. Their chief economist hit the tape with this hatchet job on the rates market late last week:

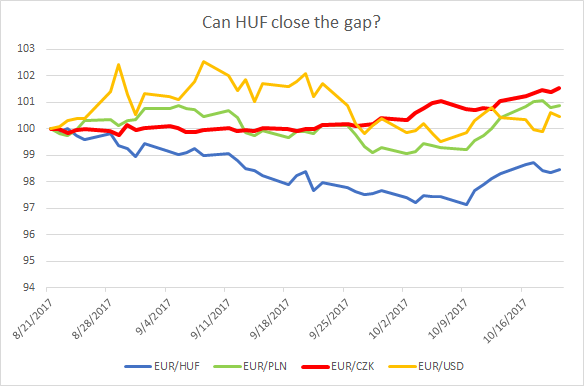

Doesn’t get much more explicit than that. Listen to the game masters. This type of verbal intervention, or forward guidance if you prefer, has pressed rates and CZK higher. If rate hikes are coming, is there still more upside in CZK? The currency has continued to well over the last couple of months...note the break higher from high levels

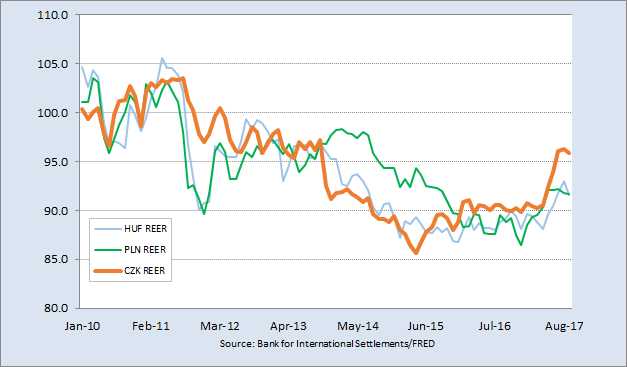

And interestingly, duration has gotten pummeled. A big element here is that foreign investors piled into the country recently, and now are getting barbequed by rate hike expectations. CZK REER has only broken away from its CE peers since the break higher in rates over the past couple of months.

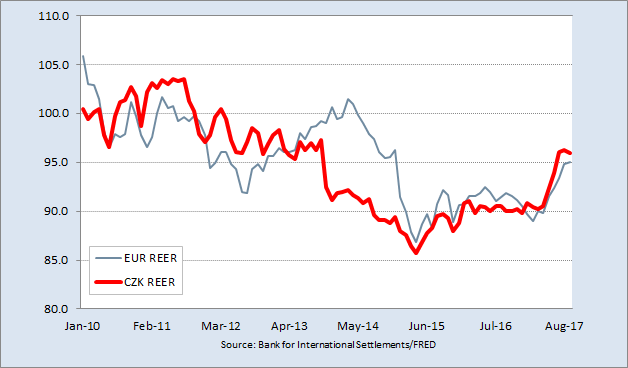

Yet the move in the currency is totally uninteresting when compared to the Teutonic juggernaut to the west:

That leads me to believe that unless there is some weird softness in the inflation data, the CNB will have to deliver on the rate hikes priced into the curve, which should continue to support CZK over the next few months.

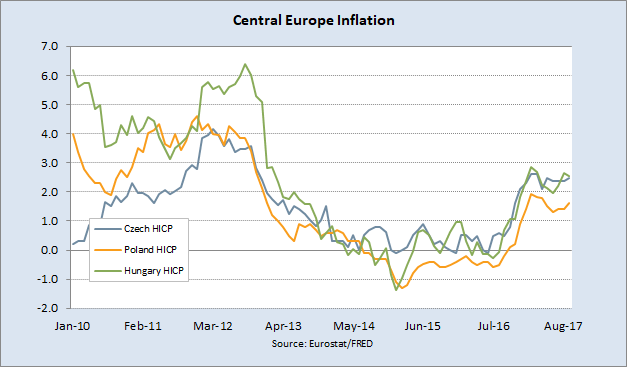

Perhaps lost in the din is why CNB is tightening policy in the first place. Inflation!! I found it Margaret! But what is the first thing you notice in this chart? Hungary and Czech HICP have been pinned to each other for most of the past four years.

So we might expect the HNB to be following a similar course to the CNB? No, quite the opposite.

I have to admit, this is one of my favorite charts of the year. The 2y rates crossed only days before the CNB allowed the CZK to float and the two trends barely took a breath, despite inflation following in lockstep! I’ll have to go a few more rounds in the EMEA ring to build out this idea, but that inflation chart and the cross in 2y HUF and CZK rates is what a breakdown in central bank credibility looks like.

We have some dry tinder here:

- higher inflation,

- a very tight labor market,

- a government that has to borrow tons of money every year to finance itself, and

- inflows from the EU

For now I think the answer is still “no”, the prior REER charts don’t illustrate a big dislocation in competitiveness, and the chart below argues the currency side might be more of a “single” than a homer. But rates...yes….carry/risk vs. reward ratio could be very appealing.

Rates in Hungary should be higher. But nobody makes money on should. Will it actually happen? Place your bets, folks. Macro at its finest.

Shawn

TeamMacroMan2@gmail.com

@EMInflationista

Shawn

TeamMacroMan2@gmail.com

@EMInflationista

19 comments

Click here for commentsShawn I have been doing some fresh work on this subject. So apparently all this refinancing is normal, but this year it just so happens to coincide the dates they want to hike rates. There ability to fund themselves essentially has been curtailed due to very uneven growth the last year (overall decent growth, but some areas were bad) This divergence of even flows of money to pay the bills to a "pay us the second you get the money" type arrangement.

ReplyNow making matters worse is these bonds are bunched together and the redemptions will all come within a month's time. This being their obligations to pay out (CEE)and a decent chunk of it dollar denominated. So they are very worried about a funding squeeze. Just to pile on the dollar is raging back again and they seem pretty worried. However the local currencies weren't experiencing problems with the dollar strength, at least as much as they could tell at UniCredit. They ran a few variable tests and found all the currencies except Turkey (political reasons) were hardly impaired by the USD bull run. Controls for variables like debt, inflation, event one-offs were all pretty negative (good). I think that's all I have thus far, but I'm gonna dive into this more later.

Alright, I'm dipping out

(I have seen this USD puzzle in other studies in the last 2 years. I wonder if EM's aren't as sensitive to the dollar anymore? Sounds crazy but most EM's pretty much use the dollar for everything anyways. Future discussion maybe?)

@johno yeah that PTJ short film is AMAZING...I know he had his faults later on in his career, but it was just great watching him on the phone putting bids in...

You know what I like best about this market. The way the chlamydia CEO pimps out it subsidiaries on its website. Like , hey....."I'm going to be too busy doing my chlamydia Eastern Suburbs tour"...."but, nonetheless, you can catch up with the labor of my business...and, ah.....and I'll get around to you and the next quarterly meeting at a hotel to be named"

ReplyIf it had a brain, it would be lethal.

ReplyIt would be the "Atomic Bomb"

ReplyThis is what happened to my friends when they spotted her on a balcony in Maroubra, Eastern Suburbs.

Replyhttps://www.youtube.com/watch?v=pXCCBeuMWLo

reminds me of trading eurodollar spreads.

ReplyShawn, it obvious whats going on. Their got a couple cases under their belt, there dirty I won't have anything to do with them (make them money). So, lets use the cases to show the world I don't have the ability to get square even against a couple cases little than a team of faggots and pedo's. Wrong, I will always be me. And the world now knows YOU.

ReplyLB's motto has been to not touch Eastern Europe with a bargepole until the headlines scream Death of Eastern Europe.

ReplyWe added a little to our bearish small cap and SVXY position at the open today.

Keep an eye open for more distribution days early this week. Little spikes at the open, to suck in the tiny punters, then a slow bleed down later in the day. These days happen often towards the end of bull markets as the large sell to the small and unwary. Dumb money indicators have been flashing of late. 65% of people (many of whom are not, or have never been, invested in the equity markets) are convinced that the market will be higher next year. Perhaps "because of tax reform" but more likely "because it has been going up". Tiny punters are the most likely to suffer from recency bias.

For those who haven't read Chris Cole's pieces on the way short volatility exposure is now embedded in this market, they are worth a read. Most people are unaware of the size of implicit as well as explicit short vol positions.

Give some thought to the historic size of the short US5y and VIX positions in the speculative community. Then think about how markets often operate under extreme conditions, and prepare accordingly.

Thank you for your post, Shawn, and everyone who contributes to this blog.

ReplyLooking at REER for Czechia versus Poland and Hungary, it is on the high side.

REER

What is your take on going long PLNCZK? Not only is Poland cheap versus Czechia by historical standards, but you also get a little bit of positive carry.

Political risks have weighed on PLN (possible EU sanctions), but maybe one could argue that after this election higher political risk premia should be justified in CZK.

Thank you for your post, Shawn, and everyone who contributes to this blog.

ReplyLooking at REER for Czechia versus Poland and Hungary, it is on the high side.

REER

What is your take on going long PLNCZK? Not only is Poland cheap versus Czechia by historical standards, but you also get a little bit of positive carry.

Political risks have weighed on PLN (possible EU sanctions), but maybe one could argue that after this election higher political risk premia should be justified in CZK.

Thank you for your post, Shawn, and everyone who contributes to this blog.

ReplyLooking at REER for Czechia versus Poland and Hungary, it is on the high side.

https://fred.stlouisfed.org/graph/fredgraph.png?g=fv5F

What is your take on going long PLNCZK? Not only is Poland cheap versus Czechia by historical standards, but you also get a little bit of positive carry.

Political risks have weighed on PLN (possible EU sanctions), but maybe one could argue that after this election higher political risk premia should be justified in CZK.

@ Marco...yeah not much to pick from there--other than the czk real appreciation this year after going off the peg/floor. I think the political issues in Poland are and will continue to be more acute than in Czech. I don't see a clear trade there but could be convinced by someone closer to the scene. I think the value would be in Hungary where there are signs that the currency is going to take the brunt of policy remaining too easy for too long.

ReplyYour chart illustrates how quiet/correlated/complacent CE FX has been for a really long time--czk vs. huf REER has traded in a 10% range for the entire post-GFC period. That would argue a material break in the relative monetary regimes could have a big impact on the currencies well in excess of historical ranges.

Hi Shawn, appreciate you looking at CEE. Not my wheelhouse (what is?), but I do trade it now and then.

ReplyA few things on HUF in particular order. Current account surplus plus a shrinking central bank balance sheet driven by the "self financing plan" tightening liquidity has had me thinking the currency could appreciate despite NBH's wishes (both THB and TWD are cases of high surplus countries seeing unwanted appreciation this year). Also. NBH may be running into constraints, not wanting to do FX swaps too far out the curve for fear of reducing flexibility. On the other hand, you have 3% target higher than rest of region, another expected easing in December, and a central bank willing to risk over-heating to keep a competitive exchange rate. The inflation figures have had a lot of one-offs in them (utility rate cuts, minimum wage hikes, etc.) in past years. My understanding is analysts are looking for inflation to let up a bit.

Re CZK, this is the one that got away. What's always scared me about this one is how crowded it is. I mean, speculators accumulated what I thought was a crazy-sized (as % of GDP) position ahead of floor abandonment. That said, the labor market is much tighter in CZK than any of its peers (Poland, for instance, has seen lots of Ukrainian labor migrating to it) and wage inflation is alive. This country has about the clearest case for hiking cycle of any out there.

Equities are lower today but 12y-o HFMs who want to JBTFD and add Risk to their Portfolio can now do so using FB messenger on their smart phones. That's not too indicative of a market that is toppy, now, is it? Facilitating tiny punters...

ReplySmall caps lagging large caps, market bleeding lower into the close. We used to have a phrase for that: Risk Off. But that was before the New Market. It's different this time.

thanks Johno, that's the type of detail I was hoping this post would unearth. The current account surplus is the difference maker there--would be interesting to dig deeper into the underlying inflation drivers.

ReplyTo your point on CZK, it has been the the trade of the year for the past three or four years that finally worked...rates was the sleeping giant.

I could be mistaken, but didn't the Czech Koruna break it's peg to the Euro. Economic boom times in the last 5 years caused the currency to appreciate so CNB intervened...now we have inflation. They were recipients of 62% of real estate investments and capital flows. In an already record investment year for the CEE as a group.

Reply49y-o former FM re-opening SPX shorts and re-buying VIX (Dec) here. Channelling my inner Nico in the hope that it's not different this time...

Reply@Celeriac - You seem to have forgot that the correct way to trade Nico's calls was to fade them. Good luck with those shorts, enjoy your margin call!

ReplyLearn a new way to gamble.

Replycasinoeing.org