Today I spent some time skimming the annual report of the Illinois Teachers Retirement System pension fund. Because I'm weird like that. While a number of critics have whacked this piñata, I believe they have (rightly) done so on philosophical grounds surrounding fees, taxpayer and employee contributions, and actuarial assumptions. As with many things in life, these issues obscure the real bottom line: performance. Let's take a look at some numbers.

As of this time last year, the fund had $124bn in liabilities against $45bn in assets. In the words of the report…”The unfunded actuarial accrued liability was $71.4 billion at June 30, 2016. The funded ratio was 39.8 percent at June 30, 2016.” Those are some brutal numbers.

$71bn!! Let’s get the crack investment staff on the case...we need to make some money!

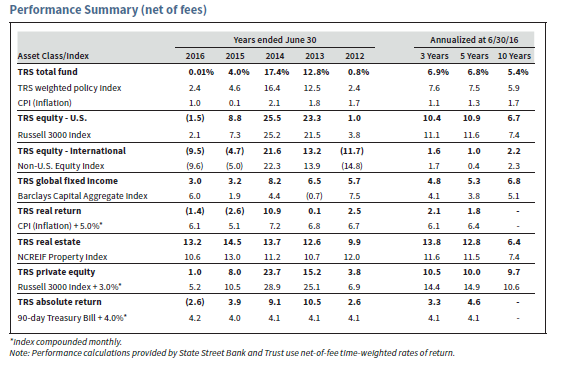

Alas...In 2016 the net return on that $45bn in assets was zero. A scant 240bps south of the benchmark. Yet liabilities went up by about $14bn, owing to demographic changes, a lower assumed future rate of return and lower discount rates of future obligations. Five and ten-year returns are also showing a consistent underperformance--but the liability side of the balance sheet continues its unyielding rise.

Results for the fiscal year that just ended aren’t available yet. Judging by results through the 3rd quarter, it looks like they had a decent year of returns...that might keep the plates spinning a little longer...but you can see by the 2016 numbers that the gap is just too big to close with any rational investment strategy.

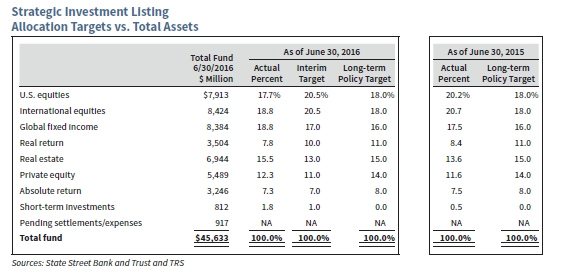

To ostensibly deal with this problem of systematic underperformance and low returns, the best consultants money can buy gave this fund a new asset allocation plan. Less investment in public equities, and more in private equity. Less in cash and fixed income, more in "real return", which is code for investments that have a return above that of inflation. Here’s the plan:

What does it mean? Less liquidity. More fees.

Alright-- I’ll be the last one to discourage alternative investments at large. The bottom line is performance--will this lead to higher risk-adjusted returns? The proof is in the pudding. How has the fund done historically in these asset classes? Illinois TRS has underperformed their private equity benchmark (Russell 3k + 300bps) each of the past five years--which summed up to 4.9% over the five year period. In the “real return” bucket, the fund’s assets have underperformed dramatically in four of the past five years, and a total of 4.6% compounded over the five year period relative to the benchmark, which is CPI +5%.

By my back-of-the-envelope math that adds up to about $1.4bn left on the table in private equity relative to benchmark returns, or over 3% of AUM...and $720mm, or 1.7% of AUM in real return. Over $2bn in underperformance and 5% of AUM, just in two relatively small asset classes! And you can probably slap another 1% of NAV to that in management fees above and beyond long-only traditional equity and fixed income managers. A billion here...a billion there…pretty soon you’re talking about real money.

As the fund continues in its quest for investing alchemy, the author of the report describes private equity as such: “Investing in private equity carries additional risk, but with skillful selection of managers, returns can be significantly higher than public equity investments.”

Indeed...but the author has no explanation for why they are so fantastically unskillful at it. Over the last five years the Illinois TRS private equity bucket has underperformed not only its benchmark but also the publicly traded domestic equity bucket. The author also fails to address the reason private equity returns can be higher than public equities: because you can take advantage of small-to-medium sized investments in companies that don’t have access to public markets or have a compelling reason to stay private (venture capital, mezzanine/convertible debt, distressed debt, etc.), or large investments that are often turnaround stories or capital structure arbitrage (LBOs).

Infinite amounts of money don’t have higher rates of return than public equities simply because you wish it to be so. Illinois TRS already has $5.3bn invested in this space. What opportunities are they, or the PE market at large, not already exploiting with that kind of size? Who are they going to hand a billion dollars to that will do better than their current PE investments?

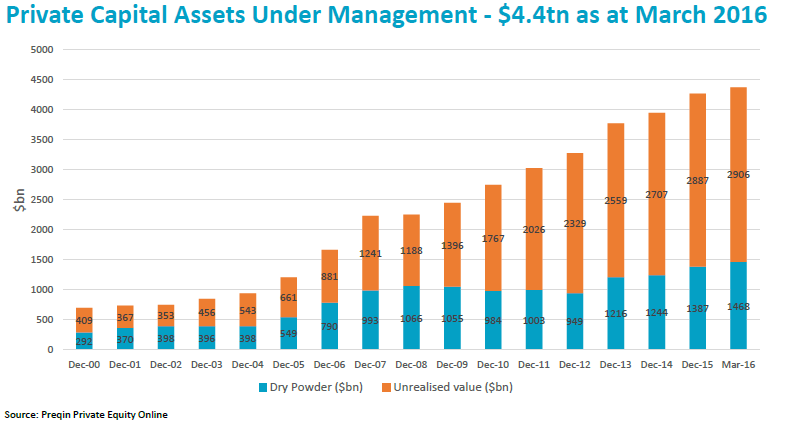

This is the strategy their consultants suggest they double down on--but there is also no explanation in the report as to why they are increasing their allocation at the expense of more liquid strategies, or why we should expect greater risk-adjusted returns in a space that has seen a $1.2trn increase in AUM since 2010, with another $500bn waiting on the sidelines looking for the next unicorn.

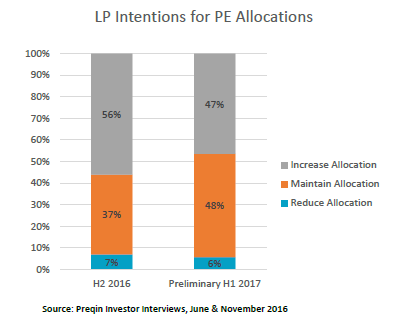

Illinois TRS isn’t alone...this huge increase hasn’t stopped investors from putting more money into the asset class...and 8x more investors seeking to increase their allocation than decrease it.

Despite two-thirds of the very same investors saying they are concerned about valuation.

What else should teachers expect, when the fund hires investment consultants with no evidence of success or value added in picking winners.

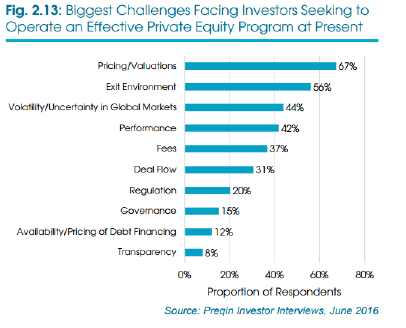

I am a big believer that past performance is not indicative of future returns. Knowledgeable people could argue the “real return” asset class, which is a hedge for spikes in inflation, is unloved after years of below trend inflation. This bucket also encompasses risk-parity, which has done relatively well, so it is unclear that this space is totally downtrodden. Regardless, as these charts show, few could argue that private equity is an under-owned, unloved asset class ripe for a contrarian, strategic allocation.

Even if there is opportunity in the PE space, the key to outperformance in alternatives is manager evaluation and selection. If you can’t get that right, and can’t minimize tracking error to something south of 4% per annum over a five year period, you need to step back and reconsider the basic foundation of your due diligence and manager selection strategy.

We may be talking about Illinois, but I’m from Missouri on this one. Show me, guys. Show me where I’m wrong on expected returns for private equity and real return strategies at billion dollar sizes. Show me why we shouldn’t expect continued subpar performance.

And I said I would focus on performance, not fees…. but….ugh!! I just can’t help myself!! I have to throw this quote from the annual report: “TRS remained dedicated in FY16 to the prudent use of the System’s assets to administer required duties and activities on behalf of its members….Total expenses to manage the investment portfolio increased by 7.6 percent to $750 million, or 1.4 percent of all TRS assets.”

Wow...I have no words. Well, maybe a few. Governor Rauner...call me!!

Governor...together, we can do this. Call me. Let’s do lunch. To illustrate the new low cost culture, it will be Portillo’s, not sushi.

Let’s summarize. Illinois TRS wants to increase long-term returns with:

1) more risk, 2) less liquidity, and 3) higher fees…in a fund with a 1) 10 year history of underperformance, 2) fiscal black hole and 3) a morbidly obese pot of fees.

This reminds me of some good advice. “Don’t just do something, stand there!!”

Illinois TRS, I beg of you...for the good of your hard working teachers and pensioners: Don’t increase risk, sacrifice liquidity, and pay more in fees unless there is a demonstrable, high probability risk-adjusted pickup in long-term expected returns. The fund’s performance in the traditional equity and fixed income space has been ok-ish--roughly in line with benchmarks, and with materially less tracking error. The teachers and pensioners in Illinois--it is their money remember--would be far better off “standing there” in a global allocation to stock and bond indices that still exploits long-term risk premia, with vastly superior liquidity, and exponentially lower fees.

Yes, the Illinois pension fund system is a well publicized fiasco. And they are most definitely playing the PR game with no lack of subterfuge...These guys even have the audacity to quote GROSS returns on their website and claim they have outperformed, as if the $750 million they pay out in fees every year doesn’t count. That’s like a golfer that hits the ball on the green and calls every putt a gimme, then tells his friends he shot a 68.

This pension system has been dealt a bad hand by the state government shortchanging contributions over the years. Yet many other states that have the same problem have been generating returns in line or better than market benchmarks, and are adequately funded. At least they are good stewards of their clients’ money. In Illinois, the fund’s managers have even bigger problems and aren’t even doing their investing job right. What’s the definition of psychosis again?

- Literary: The act of doing the same thing over and over again and expecting a different result.

- Psychology: a severe mental disorder in which thought and emotions are so impaired that contact is lost with external reality.

Both sound about right in Illinois.

3 comments

Click here for commentsScathing!! Great post ... what horrific mess. You would think they could internalise some of that asset management malarky to pay less in fees ;). It's just one of those things. Maybe picking a "good manager" is not always a guarantee that you outperform, but picking a bad one certainly seems to guarantee that you do!

ReplyIt is entirely possible that there are some even worse pension funds out there doing really ridiculous things that might even blow one of them up. Perhaps the next TBTF bail out will be the pension funds, b/c the Boomers have to f*cking win, they always do, and even when they lose (2008) they change the rules….

ReplySome time try reading Mark Blyth on the Boomers. Entertaining.

http://www.gq.com/story/mark-blyth-economics-interview

Thanks LB ... I agree with you on pension funds. We haven't even discussed Chad and his mates selling vol! Poor buggers ...

Reply