I’d love to continue the great inflation debate of 2017, with more and more charts and links to arcane central bank papers.

But wait, there’s more!

“Eurozone Inflation Points to ECB Caution on Quantitative Easing”

Good grief, can someone drive a stake through the heart of this inflation theme?!?

As if by magic, Trump’s tax plan and the Catalonia gonzo-referendum charge into the macro fold to fight with the Fed and inflation for breathing space in the minds of investors. And don’t forget the German election could portend a stronger fiscal easing with the Greens and FDP joining to push for more spending and tax cuts…Merkel might be the world’s only political leader that needs convincing to spend a budget surplus to strengthen an electoral coalition, but I think it will happen.

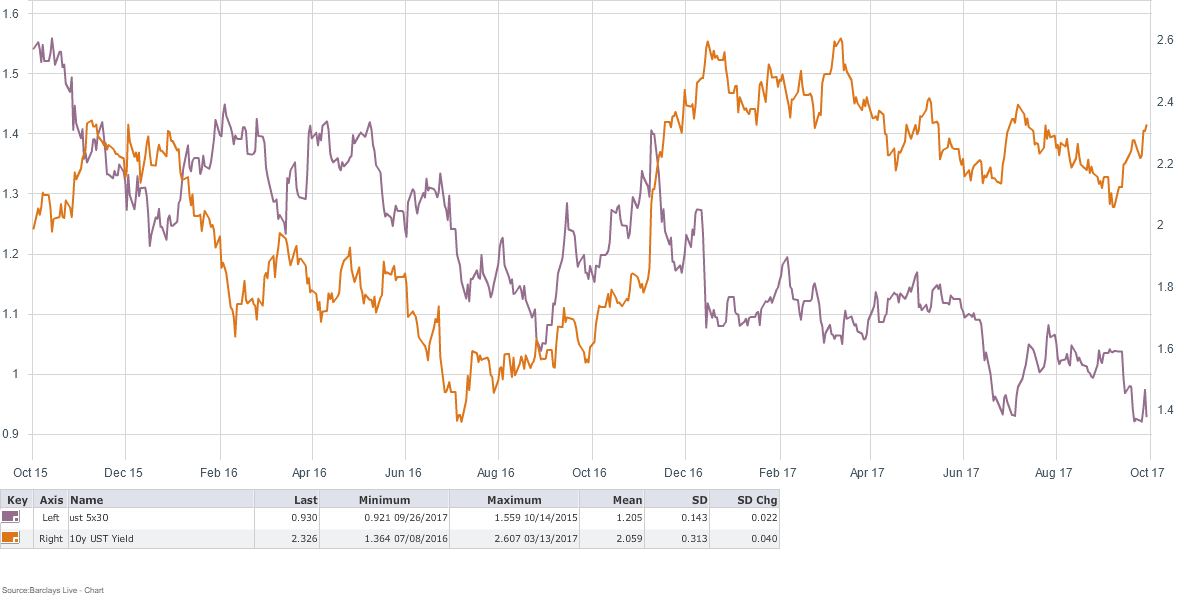

By contrast, I’m skeptical on the Trump tax plan--not only on the execution, but also on the growth implications. There simply aren’t enough grown-ups writing this bill to craft something materially growth positive for an economy like the US. The attribution of the selloff in rates over the past couple of weeks can be shared by the FOMC and tax reform, but I don’t think the market is pricing in faster growth or higher deficit spending so long as 5x30s is still stuck in the basement.

Given the way fast money ripped FVZ7 coming out of the fed meeting, I thought we’d see 5x30s grind higher….but no!

Circling back to Europe, the combo of the weak inflation data and increased political uncertainty after the Catalonia referendum will put a cap on the strong EUR theme for now.

Rajoy clearly overplayed his hand, but it is far from clear what the next step will be. Political deadlock and delay seems to fit for Rajoy--and while this was a victory in the media for the Catalan independence movement, it isn’t clear what the next step will be. Will the Catalan leadership throw gas on the fire and declare independence, as promised before the referendum, and suggested by Puigdemont today?

That would be a big sell signal for peripheral spreads and EUR. Time will tell, but I don’t believe the “strong Euro” trade will take the spotlight again until there is a political solution and/or economic data to change the narrative. That could be good news for EMFX, since an increase in political risk amidst continued positive global growth signals could shift more of those RM flows into EM.

That being said, The New York subsidiary of Team Global Macro didn’t join the "buy USD" game today. EUR gapped weaker on the Asia open and it was “sell on” to 1.175 for the London open...but then...nothing. Choppy trading throughout the day and a steadfast refusal to break the 1.17 support I noted earlier last week.

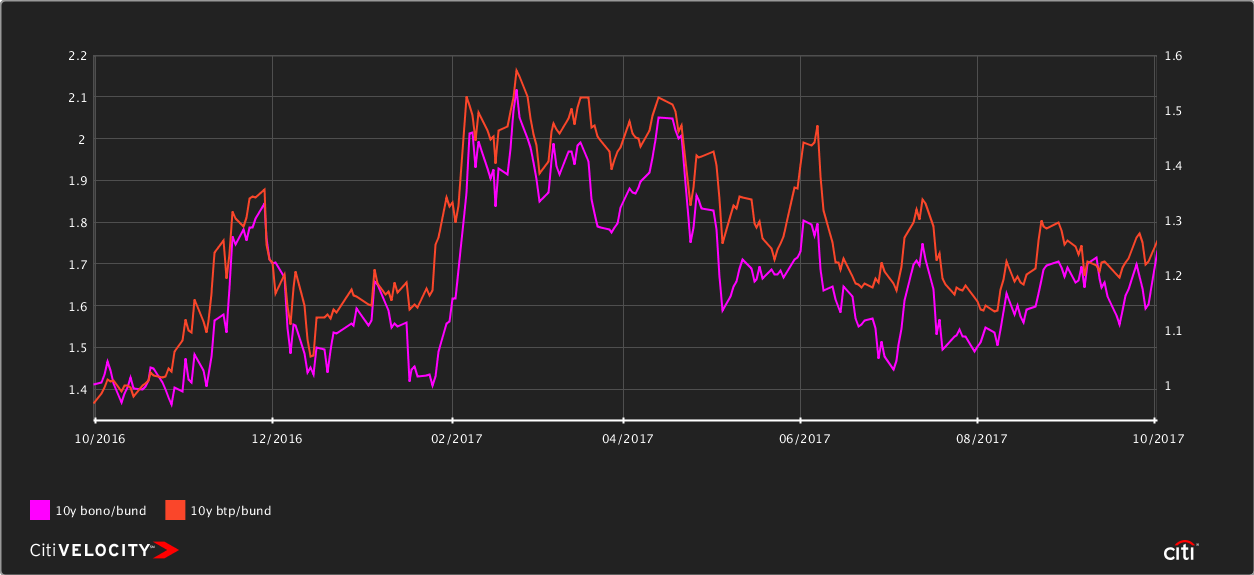

Yet there is plenty of space to see a further selloff in peripheral spreads, especially as the next risk-event in Europe is likely to be the Italian election early next year, which could usher in a squirrely Eurosceptic populist coalition that makes the Tories look like a poster child of political unity and discipline.

10y bono-bund spreads sold off 8-10bps today, but still well off the wides from earlier this year. With the withdrawal of the 2018 budget amidst opposition from the Basque nationalists, there seems to be scope for continuing widening. Given the firmly entrenched BTD mentality, I’d be loath to say we won’t see real money buying, but it may take more cheapening for them to step in.

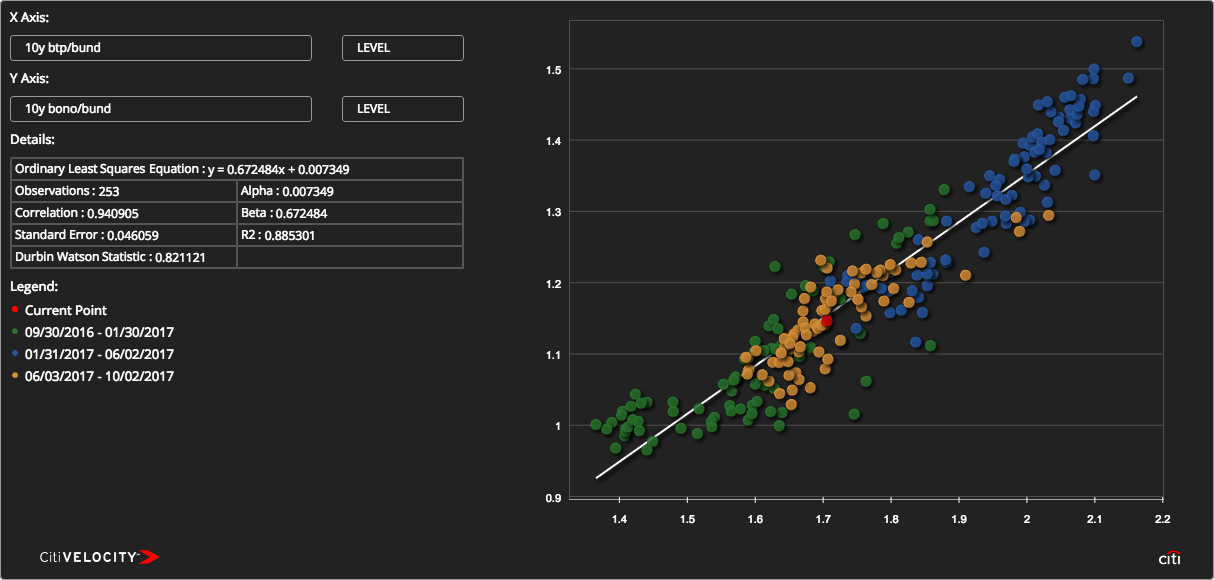

This regression is plotting the current level from Friday’s close but illustrates there isn’t much value in Spain, even after this back up. Come to think of it, if this regression shows one thing it is probably that there hasn’t been much credit analysis going on in the periphery at large since the Italian referendum.

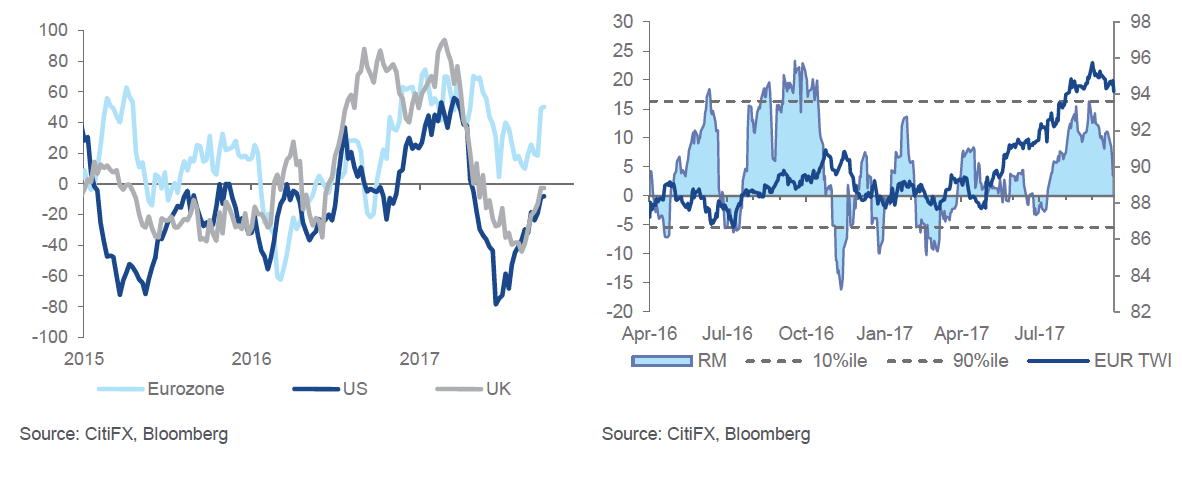

As discussed in previous posts, earlier this year the strong EUR theme had the potential to have some momentum behind it, given the unwind of the structural short in the market after years of getting kicked around. A couple of charts from citi’s macro group show that theme gained traction as the European economy picked up speed while the US disappointed--that divergence in the data appears to be mean-reverting and indeed, RM flows are slowing down. That short-term technical is USD supportive as well and points to a break of that 1.17 level.

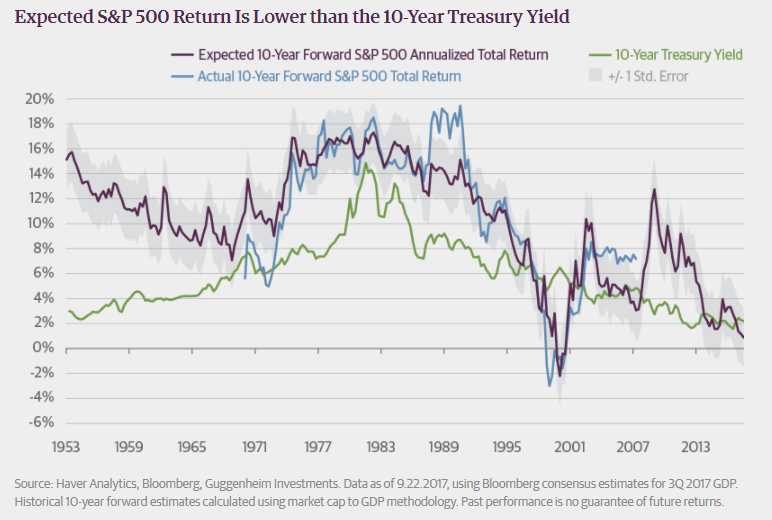

In other news….just a quick “clip and link” to a chart published today by Scott Minerd over at Guggenheim and brilliantly titled, “Stocks for the Long Run? Not Today.” The expected 10yr return for the S&P 500 has dipped below that of 10y UST, which is a big negative for risk-adjusted equity returns.

I noted this fact a while back in my discussion on the risk appetite, reach for yield, lousy returns, and lust for private equity among pension funds, high valuation by definition means lower future expected returns. Pension funds can’t wish this problem away by taking more exotic equity risk, more duration risk, or in my opinion, more exotic fixed income risk at Minerd suggests. While I agree that he is probably right about value in off-index cash flows relative to those inside the Bloomberg Barclays Global Aggregate, long-term investors need to temper their expectations for future returns and not shy away from tail hedges that will protect them in a downdraft at a reasonable cost.

Shawn

TeamMacroMan2@gmail.com

@EMInflationista

14 comments

Click here for commentsNice post Shawn. While I like minerd not sure how he comes to us equites expected return is lower than 10 year. There are many who would disagree and there is a wide range out outcomes over the short term. Longer term he is probably correct but who knows when that is.

ReplyEuro trade has legs as long as the economy is booming there. Yes it's booming in Europe, according to the numbers at least. But wait now U.S. Manufacturing is booming too. So who knows. I do believe the eu consumer is probably a decent play for the next few years but exporters I am more cautious on. But clearly there is room to go as they are cheap and given he recent strength likely going to kill earnings. But q3 and ahead yoy comparisons should get harder so let's see.

IPA, yeah I see the oil beta plays. Though they are stuck below the 200. Would like one more rally over that to feel comfortable. Then I might add to some beta plays or mlps which are lagging.

Nasdaq looks craptastic. Feeling like they might miss or at least tread water into earning ? They fangs Hardly ever miss do I wouldn't bet on it but starting to see some signs.

abee, really hope you are right on large tech. NDX is looking kind of heavy here, not confirming new highs on the rest of indices (barely though). I'm short AMZN. If h+s neckline breaks it may send the price on a deep dive. My thought is that if price closes below 8 ema on monthly that would set up the mid BB as a possible target @ $840-ish which is also a backtest of a prior high.

ReplySpain catalonia is considered by Eurocrats as the kids squabbling.

ReplyIPA, i like your call on AMZN, its for sure the weakest recently but going into earnings is a coin toss with them. MM had a nice blurb on AAPL which i think is more important, given the supply chain. I think its done. FB is also weak but it never misses so hard to get too excited.

ReplyADBE is pretty key as it is still growing fast but seems like estimates have caught up. Also keeping an eye on EM tech. DRAM is key and also BABA / Tencent, the latter two are just large cap rocket ships, which seem invincible and for good fundamental reason. Any Chinese user comments are appreciated but from what I hear both Ali/WeChat ecosystems just get stronger and stronger.

If you're point is a guy can get fired before a 10yr expected return materializes, then yes, duly noted. For asset allocators that have that time of investment horizon, they *should* be thinking about this kind of thing. I can't remember where I saw a more detailed decomposition of the valuation/expected returns concept but it is one of James Montier's favorite subjects over at GMO.

ReplyAnd re: spain/catalonia, take it from me...squabbling kids can drive the parents nuts!! Queue lashing out, threatening to turn the car around and go home, etc. etc.

"And re: spain/catalonia, take it from me...squabbling kids can drive the parents nuts!! Queue lashing out, threatening to turn the car around and go home, etc. etc. "

ReplyThe spain kids need to look at the scrabble board. There is only two K's , one O , and one Y left on the board. I couldn't be bothered with this market anymore. The game was over long ago. We're panels up and around the corner from their squabbling bullshit, look at me!. These letter's will do the job.

Interesting take by Guggenheim on equities. Reminds me of the post at: http://www.philosophicaleconomics.com/2013/12/the-single-greatest-predictor-of-future-stock-market-returns/

ReplySomehow can't find my spreadsheet replicating that work, but without having to re-do it, I can say that it agrees with Guggenheim's predictions. Will note, however, that there's a follow-up post on Philosophical Economics that critiques these methodologies.

I think anyone buying US equities today has to, at best, expect much lower returns than history. Doesn't mean equities are necessarily bad right now (though they may well be), just that returns will disappoint most peoples' expectations. I'd never want to be a retirement adviser ... it's an industry that naturally will select for bullish confidence men. If you tell prospective clients that their return assumptions will have to be lowered and they have to cut consumption accordingly, they'll just go to some adviser who's drinking the Kool Aid. Realists getting weeded out. Eventually, when returns fail to deliver, people will say their advisers were dishonest or blame "Wall Street," but 9/10 advisers are probably are honestly dumb. After all, people who buy their own BS are the best salespeople.

abee -- you asked my view on EMFX and I'm not sure I have a strong one, either way. I'm lightly positioned. There's some near-term risk with the Fed appointment. Warsh seems the favorite, which surprises me (I'd think Powell fits the profile better, a "low rates", Republican, "good soldier" who's never dissented), and so we could get some further selloff in rates on that before people realize Warsh probably doesn't start changing the Fed consensus for at least 6 months from appointment. It's just so bizarre! The stock market is the only thing Trump has going for him (as evidenced by his Tweets), and he's going to appoint the guy who wants to flip it the bird? The bigger issue for EMFX is China, to my mind. And there, we got some forward-starting monetary easing the other day, which has been interpreted variously. Suggests to me, while fiscal stimulus may slow and regulatory oversight heighten post-Congress, we won't see some Q1 hard stop in China. I'm still holding a long aluminum, short USDRUB, and a cut position in USDARS where I have been wrong.

On rates, I think supply-demand balance points to higher levels next year. Cyclical factors and reversion of one-offs point higher too. The tax plan will be an absolute dud for growth and inflation, however. I'm not keen to get short at current levels to the extent it's been driven by that last narrative. Not sure what to make of sentiment data ... JPM client survey at most bearish since 2006 but strips data and asset manager longs (not to mention the prevailing narratives one hears) suggest an entrenched low r-star/"economy can't take high rates" view. Re Warsh, if he's appointed, I think the knee-jerk is front-end steepening, but what about the long-end? I could imagine 2s10s flattening on his appointment (and steepening on Powell's).

Zerohedge is getting/has gotten so bad I want to pay someone to read it for me, and pick out the 1-in-20 worthwhile articles.

I'm skeptical of this dollar bounce narrative. Maybe it's some sample bias, but I've seen so many pundits long dollar all the way down and now saying, "no, wait, now it's going to go up now." It feels like there are too many stubborn people still calling for this. The pull-back in EURUSD has just been setting us up for an October ECB announcement, IMO. Europe is back EURUSD is only 2% above the range it traded in the old European narrative.

Wanted to add that Gratham's last letter was great. In a nutshell, market valuations are driven by inflation volatility, profit margins, and economic (GDP) volatility. On these factors, markets are not trading out-of-line. So, where are those going? My base case doesn't see much change to any of those in the next year. If I try looking into the future for risks to those factors I see 1) China having a credit bubble-related slowdown/accident driving world inflation and GDP volatility, 2) Trump/Republican's tax cuts failing to help middle class voters who then roll the dice with a Left populist who creates inflation volatility and undermines margins (through taxes, regulation, antitrust), 3) some demographic tipping point? And then there's the cause of the past two gut-checks top valuations: too-dovish central banks letting asset bubbles inflation (which invariably burst).

ReplyFor the record, my beta equity exposure is very modest. I am very long merger arb though. I also admit that financial advisers have gotten a lot of things right where I've gone wrong in the past, so who am I to call any of them dumb?

Gundlach thinks Kashkari will be appointed. What an absolute cluster-f that would be for the dollar bulls.

ReplyMy 2 cents is that Yellen stays somehow.

ReplyChina growth probably peaks sometime soon and we start to slow. The global economy is running hot now. If we don't slow pricing pressures likely to enter and will take growth down thereafter anyways. Tough market to invest in, imo but buying equites works until ppl realize there could be a recession, and right now none is visible. I'll pay attention to 10 year. Already front end of curve feels weak. I don't want to be long anymore.

Re advisors. They are salesmen, not portfolio managers. If you live in the U.S., you just buy stocks, when they go down buy more. If you lose clients, at least it's not your money and when the market goes back up, you find new ones or they come back. But in all seriousness, it's hard to both gather and manage money. Different skill sets and lots of work to get new clients. Anyways it's all going to the robots nowadays, so which do some pretty cool stuff like tax loss harvesting.

Gary Cohn would lose his mind if Trump nominated Kashkari. There's a Goldman pecking order there. If it is warsh, i guess one could argue there will be some macro impact but i'd look to fade it as he becomes "institutionalized". Powell, and probably Cohn seem like business as usual to me.

ReplyRe: zerohedge, I had to delete it from my feed. Come on, guys. It was much better when it was the home for the things sell side guys weren't allowed to say instead of the minute by minute avalanche of doom and conspiracy theories.

Not much to make out of the price action the past couple of days, no momentum/break in EUR, despite the continued noise out of Spain, and Germany if you want to lump that in. Another weak retail sales print in the eurozone though is going to again keep the narrative on EUR-anxiety into NFP rather than pushing the flows back into selling USD.

You want the truth about the American market. Here you go. Trump has three years to go , we've seen the greatest bull run in history, and the market has three years to keep climbing before it eventually finds out that Trump is a glorified 'used car salesman'. There you have it. America is worth jack to work in or live in period. Cheers from Amps from the trading desk in South East Asia.

ReplyIs everyone here in this blog going to tell me they cannot see what I'm seeing. Are you lot fuckin kidding! Or are you lot buttering your own fuckin bread. See ya.

ReplyInteresting opinion piece in the WSJ today on Warsh. The bit that stuck out: "Warsh ... believe[s] that tax reform and deregulation can increase the economy’s capacity to grow above 3%. [He] therefore might raise interest rates more slowly than the Yellen-Powell faction would." Seriously? I guess if the guy wants the job badly enough, he might reason that way to being Trump's "low rate guy." Separately Liesman saying Kashkari not being considered. Anyhow, guess I'm seeing the logic to a Warsh appointment.

Reply