Macro Man was unsurprised to see a substantial discounting of Friday’s employment data on the basis of a) the loss of employment in the manufacturing and construction sectors, b) the fact that the bulk of the revisions were in education, c) the bulk of the job gains were of either the governmental or the burger-flipping variety, and d) the numbers are so volatile that they don’t mean anything anymore. Of these, Macro Man has substantial sympathy for the fourth objection but very little for the first three.

After all, isn’t it a good sign that firms are adjusting to weaker demand by shedding labour? That US companies have the flexibility to do so is an underlying strength of the American economy versus Europe or Japan, and one of the reasons why trend growth in the US is higher than in most other developed economies (even with the recent downward revision to trend growth estimates.) And why should teachers not count? They comprise a substantial portion of the workforce, and it is unsurprising that August/September data looked anemic if school districts did not supply payroll data in a timely fashion. And if all jobs were of the burger flipping variety, why is the unemployment rate amongst college graduates 1.9%, while the rate for non-high school graduates 5.8% (admittedly down from 7.1% in July.) That firms are now forced to hire workers with relatively low qualifications is suggestive of the tightness of the labour market, not its imminent implosion.

As noted on Friday, the bond market was priced for yields to rise on any non-horrible news, and Macro Man was pleased to see the losses extended after the non-manufacturing ISM figure. However, the market remains in tactical mode, and Macro/Micro Man remains bid at 107 to take back 200 of his 300 short Treasury contracts. If the March 95 eurodollar calls go offered at a tick any time soon, meanwhile, Macro Man will likely add to the position in a lottery ticket bet.

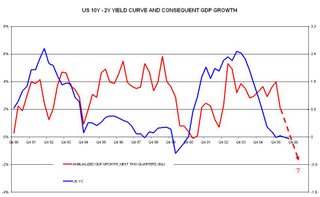

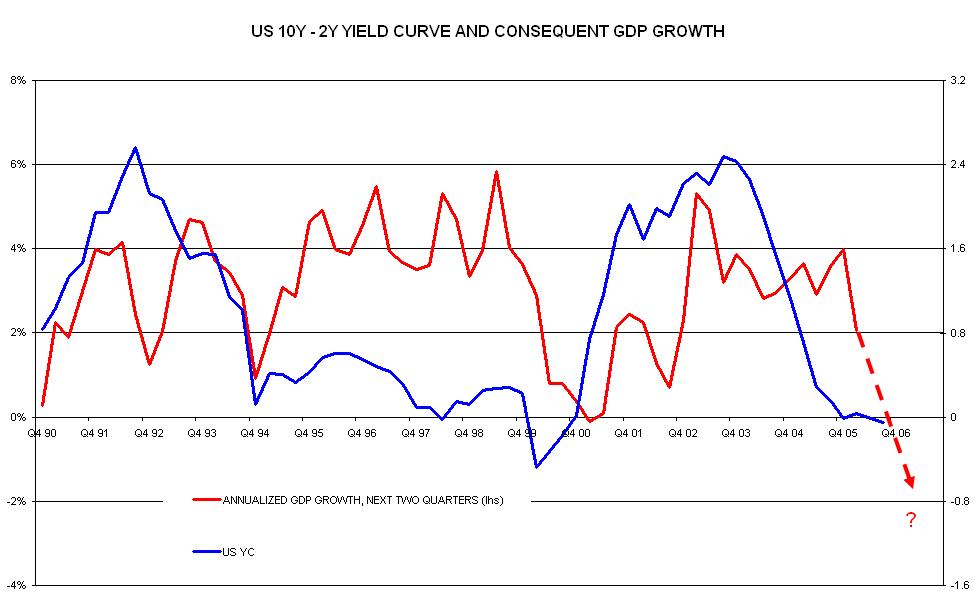

One notable aspect of the bond market selloff on Friday is that it was essentially a parallel shift higher in the yield curve. 2’s -10’s remains inverted by 10 bps, and cash- 10’s by substantially more. According to a number of commentators, including the Fed, this is suggestive of an imminent recession. Indeed, many of the more bearish economic commentators are hanging part of their argument on the signals provided by the yield curve.

After all, isn’t it a good sign that firms are adjusting to weaker demand by shedding labour? That US companies have the flexibility to do so is an underlying strength of the American economy versus Europe or Japan, and one of the reasons why trend growth in the US is higher than in most other developed economies (even with the recent downward revision to trend growth estimates.) And why should teachers not count? They comprise a substantial portion of the workforce, and it is unsurprising that August/September data looked anemic if school districts did not supply payroll data in a timely fashion. And if all jobs were of the burger flipping variety, why is the unemployment rate amongst college graduates 1.9%, while the rate for non-high school graduates 5.8% (admittedly down from 7.1% in July.) That firms are now forced to hire workers with relatively low qualifications is suggestive of the tightness of the labour market, not its imminent implosion.

As noted on Friday, the bond market was priced for yields to rise on any non-horrible news, and Macro Man was pleased to see the losses extended after the non-manufacturing ISM figure. However, the market remains in tactical mode, and Macro/Micro Man remains bid at 107 to take back 200 of his 300 short Treasury contracts. If the March 95 eurodollar calls go offered at a tick any time soon, meanwhile, Macro Man will likely add to the position in a lottery ticket bet.

One notable aspect of the bond market selloff on Friday is that it was essentially a parallel shift higher in the yield curve. 2’s -10’s remains inverted by 10 bps, and cash- 10’s by substantially more. According to a number of commentators, including the Fed, this is suggestive of an imminent recession. Indeed, many of the more bearish economic commentators are hanging part of their argument on the signals provided by the yield curve.

However, should we believe what the yield curve is saying? After all, it’s not as if many of the people buying bonds are doing so in an attempt to predict the trajectory of the US economy. Central banks have appeared happy to buy Treasuries at a level shunned by the private sector- hence the persistent real money short position revealed in survey such as the Merrill Lynch or Russell/Mellon. Moreover, central banks have consistently demonstrated the willingness to pay way over the odds for assets over the past few years. Anyone who has bought EUR/USD and GBP/USD at currently levels on a consistent basis, as central banks have, is clearly not motivated by such trifles as ‘valuation.’

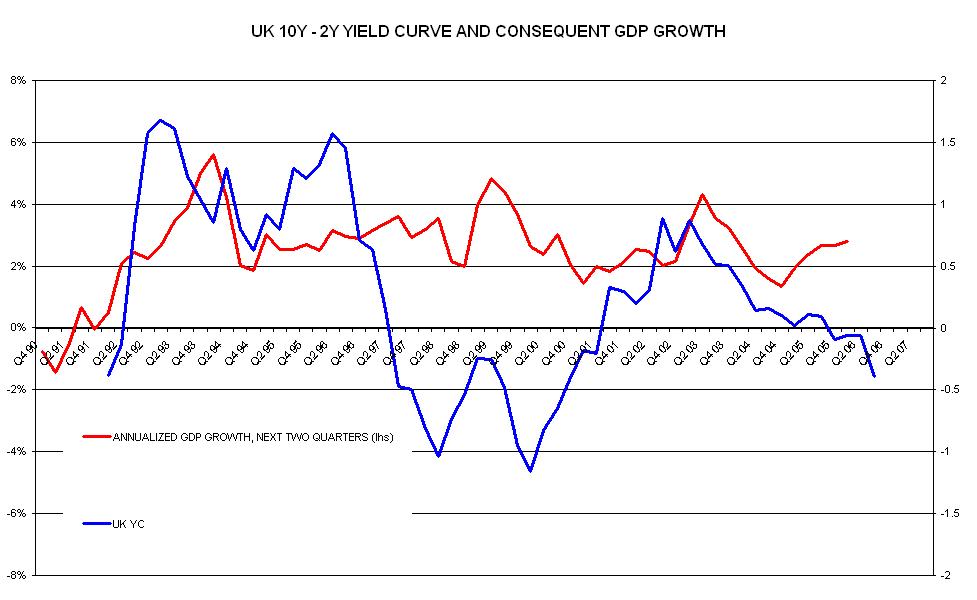

An even stronger case against relying on the US yield curve as a signal of recession is the abject failure of yield curves in the UK

Australia,

and New Zealand

to predict recessions over the past few years. Of the three countries, only the UK has even seen rate cuts, which will be fully reversed on Thursday. Macro Man wants to hear an adequate explanation for the lack of predictive power in these countries’ yield curves before he relies on a slight inversion of the US curve as an augury of doom.

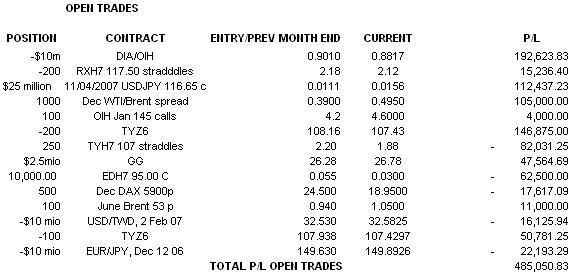

Elsewhere, the EUR/JPY offer was filled and bid on, at least partially on EURUSD buying from our old friends the Asian central banks. Macro Man looks forward to the day when these fine fellows find out what exactly it is that they’ve been buying. Overall, however, Macro Man has little room for complaint, with November starting off on a fine footing. A few more ticks lower on TYZ6 and he can start banking some of the profits.

Elsewhere, the EUR/JPY offer was filled and bid on, at least partially on EURUSD buying from our old friends the Asian central banks. Macro Man looks forward to the day when these fine fellows find out what exactly it is that they’ve been buying. Overall, however, Macro Man has little room for complaint, with November starting off on a fine footing. A few more ticks lower on TYZ6 and he can start banking some of the profits.

3 comments

Click here for commentsI believe that the buying of the shorter end by Central Banks (esp. China ) forces the curve to an inverted level that it wouldn't normally be ... I watch the 5-10 year curve and until that inverts , IMO , the economy will skate through at a lower level , but not recessionary

ReplyOne of the problems, of course, is that you've got central banks at the short end, and pension funds at the long end (hence the consistent popularity of 10-30 flatteners in the US and Europe.) An interesting dynamic over the next few years is to see if CBs do what they've said they are going to do, i.e. move out the credit curve. If so, then spreads will likely remain tighter in the future than they have been in the past.

ReplyAn interesting trade at some point will be to figure out where their 'cut-off' is in the ratings spectrum (assuming there is some broad consensus amongst reserve managers) and to play a widening of the spread between those credits just inside their universe and those just outside.

thanks for the heads up

Reply