Markets are now finely balanced between pricing a soft versus hard landing in the US and, by extension, the world. As yet, no decisive conclusion has emerged, though a substantial out of consensus out-turn on today’s payroll data may be the trigger for more thematic market price action.

At a 65 bp inversion to Fed funds, one would think that the US bond market is priced for the worst. To a degree, that is true; it will take a run of poor economic data to keep yields from rising. On the other hand, we have to acknowledge that some of the purchasers of bonds are not profit-maximizing agents. Central banks buy Treasuries (and Bunds, and Gilts, etc.) because they have a veritable Everest of foreign exchange reserves to invest, and they need liquid securities in which to invest. Pension funds, meanwhile, are perpetually short gamma, forced to chase the market higher when declining yields increase the NPV of their liabilities. The recent run-up in equity prices also may be forcing some rebalancing trades (sales of equities, purchases of bonds) to ensure that strategic portfolio benchmarks are maintained. And let’s not forget the mortgage convexity guys either, another source of perpetual short gamma. The upshot is that yields may well remain lower than they ‘should’ be in the future, a fact touched on by Trichet yesterday.

Whither, then, the Macro Man bond short? At current levels, it remains the right trade, as bonds remain very close to the top of their range and far away from the Fed funds ‘anchor.’ Indeed, Macro Man will step a stop entry at 108 to sell another 100 in the event of a strong payroll figure. However, a change of tactics is required. When it comes to bonds, Macro Man has decided to become Micro Man until further notice. The stop for the current 200 lot position is set at 109. Moreover, Micro Man will book profits on 200 bond futures at 107 (leaving a remaining 100 stopped into as close to 108 as possible.) If the market is going to oscillate within a range, it is incumbent upon Macro Man to make some money trading around a (smallish) core position.

Elsewhere, the Taiwan dollar remains bid, shaking off six months of lethargic performance. Not even the indictment of President’s Chen’s wife on fraud charges has stopped the TWD juggernaut. The authorities would love to get their hands on Chen himself, but he enjoys immunity whilst in office. The CBC reportedly showed their hand today, but that is likely simply an attempt to smooth the pace of the TWD recovery. In any event, Macro Man suspects that more TWD shorts remain to be squeezed. Therefore, he sells $10 million USDTWD three months forward at 32.53. The stop is set at 33.20 on a spot basis and will be trailed lower as spot declines.

At a 65 bp inversion to Fed funds, one would think that the US bond market is priced for the worst. To a degree, that is true; it will take a run of poor economic data to keep yields from rising. On the other hand, we have to acknowledge that some of the purchasers of bonds are not profit-maximizing agents. Central banks buy Treasuries (and Bunds, and Gilts, etc.) because they have a veritable Everest of foreign exchange reserves to invest, and they need liquid securities in which to invest. Pension funds, meanwhile, are perpetually short gamma, forced to chase the market higher when declining yields increase the NPV of their liabilities. The recent run-up in equity prices also may be forcing some rebalancing trades (sales of equities, purchases of bonds) to ensure that strategic portfolio benchmarks are maintained. And let’s not forget the mortgage convexity guys either, another source of perpetual short gamma. The upshot is that yields may well remain lower than they ‘should’ be in the future, a fact touched on by Trichet yesterday.

Whither, then, the Macro Man bond short? At current levels, it remains the right trade, as bonds remain very close to the top of their range and far away from the Fed funds ‘anchor.’ Indeed, Macro Man will step a stop entry at 108 to sell another 100 in the event of a strong payroll figure. However, a change of tactics is required. When it comes to bonds, Macro Man has decided to become Micro Man until further notice. The stop for the current 200 lot position is set at 109. Moreover, Micro Man will book profits on 200 bond futures at 107 (leaving a remaining 100 stopped into as close to 108 as possible.) If the market is going to oscillate within a range, it is incumbent upon Macro Man to make some money trading around a (smallish) core position.

Elsewhere, the Taiwan dollar remains bid, shaking off six months of lethargic performance. Not even the indictment of President’s Chen’s wife on fraud charges has stopped the TWD juggernaut. The authorities would love to get their hands on Chen himself, but he enjoys immunity whilst in office. The CBC reportedly showed their hand today, but that is likely simply an attempt to smooth the pace of the TWD recovery. In any event, Macro Man suspects that more TWD shorts remain to be squeezed. Therefore, he sells $10 million USDTWD three months forward at 32.53. The stop is set at 33.20 on a spot basis and will be trailed lower as spot declines.

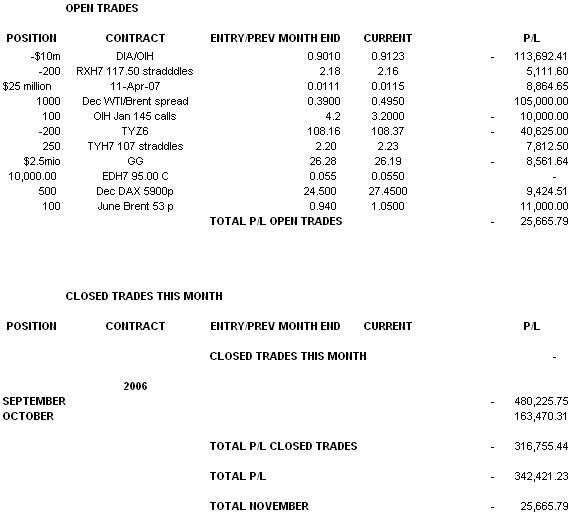

The EURJPY offer failed getting filled by 14 pips overnight but remains in place. Elsewhere, the portfolio has slipped a bit as oil prices have once again lurched lower, submarining the OIH position. Bond vol has also seems slipped back a bit, somewhat surprisingly, reducing the profits on the TY/RX straddle spread. It’s likely to be a tedious few hours until the payroll data; what happens afterwards depends on the figures.

2 comments

Click here for commentsgreat site

ReplyThank you. It's early days, but it's been fun so far.

Reply