Well, that was disappointing. The FOMC statement (and more importantly, the market reaction to it) was not what Macro Man was looking for. The Bernanke Fed has evidently devolved into the business of wishcasting rather than forecasting. Lower energy prices should lead to a moderation in inflation (funny how the emphasis shifts from core to headline CPI when it’s convenient, eh, Ben?), but strangely do not provide any sort of growth-positive income shock, or at least not one worth noting. So inflation is going to fall because of the modest growth trajectory and “the cumulative impact of monetary policy actions”, among other things.

Let’s examine this for a moment. What exactly has been the “cumulative impact of monetary policy actions”? Let’s look at corporate borrowing rates. The Moody’s index of Baa rated borrowing costs is currently at 6.48%. The day that the Fed tightened policy for the first time (June 30, 2004), the index was at 6.71%. Hmmm......so the impact of monetary policy actions is that it is cheaper for companies to borrow now than it was the day the Fed started tightening. OK, it is the case that mortgage rates have risen along with Fed funds, particularly the much-ballyhooed ARM rates. Yet the flip side to higher ARM rates is the substantially higher deposit rates that savers earn on cash (and yes, Virginia, despite their profligate reputations, US households do actually save money.) In June 2004, US household interest income was running at an annualized $890 billion rate. Fast forward to August, and interest income is now running at a tasty $1.03 trillion dollar rate- an increase of more than 1% of GDP. Given the extent to which asset allocators and sovereigns have scooped up Treasuries, Macro Man suspects that the Fed has overestimated the lag (and indeed, the degree) with which monetary policy impacts the economy.

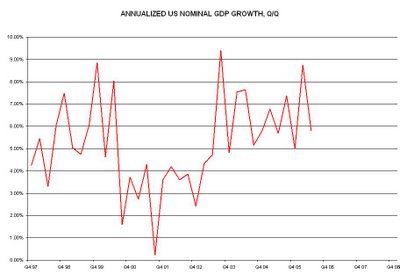

What we are left with, though, is a Fed operating a ‘golden mean’ wishcasting policy: everything in moderation. Growth is expected to clip along at a moderate pace, and inflation pressures are expected to moderate. What this means in practice is that they are likely expecting the run rate of nominal GDP to decelerate to 5% or so. As the chart below indicates, that slow of a pace has been difficult to maintain for more than a quarter at a time during this expansion. The Q3 GDP figure released tomorrow, however, might be one of those occasional hiccups. Nevertheless, Macro Man is struck by the sort of inverse ‘Lake Woebegone’ expectations of the market. Every institution that Macro Man has professional dealings with is calling for real GDP growth to be on a 1 handle, yet the Bloomberg consensus is for 2%. Truly, a market where everyone is evidently more downbeat than consensus! Give that we evidently remain in a range and that the initial GDP reading is highly dependent on the (volatile) trade and inventory assumptions, Macro Man will look to fade any gap higher in bonds after the report. He doubles the short Treasury position at 108.

.

Elsewhere, foreign exchange remains a sucker’s game. The noise to signal ratio is very high, with ranges persisting and flow dominated by short term traders and, the rumour goes, sovereigns. Macro Man was simultaneously irritated and amused to see confirmation that China is, after all, a Communist country. The State Administration for Foreign Exchange, who regulates the domestic currency market and manages the country’s $1 trillion FX reserve portfolio (partially by day trading EUR/USD and/or selling volatility), issued a new regulation today prohibiting domestic banks from quoting CNY NDFs offshore. There was no reason given, but it presumably has something to do with eliminating the possibility of arbitrage profits between the onshore and offshore markets. As a result, the offshore market will become wider, less liquid, and less reflective of onshore fundamentals. For SAFE, evidently, currency speculation must be centrally planned and administered by the public sector agency set up to do it, e.g. themselves. That the regulator is essentially destroying private sector competition for profits with the stroke of a pen goes a long way to explaining why this market remains one with many more visible losers than winners.

Elsewhere, foreign exchange remains a sucker’s game. The noise to signal ratio is very high, with ranges persisting and flow dominated by short term traders and, the rumour goes, sovereigns. Macro Man was simultaneously irritated and amused to see confirmation that China is, after all, a Communist country. The State Administration for Foreign Exchange, who regulates the domestic currency market and manages the country’s $1 trillion FX reserve portfolio (partially by day trading EUR/USD and/or selling volatility), issued a new regulation today prohibiting domestic banks from quoting CNY NDFs offshore. There was no reason given, but it presumably has something to do with eliminating the possibility of arbitrage profits between the onshore and offshore markets. As a result, the offshore market will become wider, less liquid, and less reflective of onshore fundamentals. For SAFE, evidently, currency speculation must be centrally planned and administered by the public sector agency set up to do it, e.g. themselves. That the regulator is essentially destroying private sector competition for profits with the stroke of a pen goes a long way to explaining why this market remains one with many more visible losers than winners.

Sadly, Macro Man’s two forays into currencies are among the losers. The RBNZ did its part in easing his pain, though, as the statement overnight opened the door (very slightly indeed, mind) to acknowledge the contemplation of rate cuts at some point in the future. Macro Man does not expect rate cuts over the next six months at least, but given that 25 bps of tightening was priced as a done deal by year end, the squeeze in NZD and kiwi rates could have further to go. Per yesterday’s post, Macro Man battens down the hatches on the short NZD/USD position by trailing the stop loss down to 0.6600, just above the day’s high. The surge in the energy complex has brought the portfolio back into positive territory since inception in early September, so now is no time to leave money on the table with shoddy risk management.

Let’s examine this for a moment. What exactly has been the “cumulative impact of monetary policy actions”? Let’s look at corporate borrowing rates. The Moody’s index of Baa rated borrowing costs is currently at 6.48%. The day that the Fed tightened policy for the first time (June 30, 2004), the index was at 6.71%. Hmmm......so the impact of monetary policy actions is that it is cheaper for companies to borrow now than it was the day the Fed started tightening. OK, it is the case that mortgage rates have risen along with Fed funds, particularly the much-ballyhooed ARM rates. Yet the flip side to higher ARM rates is the substantially higher deposit rates that savers earn on cash (and yes, Virginia, despite their profligate reputations, US households do actually save money.) In June 2004, US household interest income was running at an annualized $890 billion rate. Fast forward to August, and interest income is now running at a tasty $1.03 trillion dollar rate- an increase of more than 1% of GDP. Given the extent to which asset allocators and sovereigns have scooped up Treasuries, Macro Man suspects that the Fed has overestimated the lag (and indeed, the degree) with which monetary policy impacts the economy.

What we are left with, though, is a Fed operating a ‘golden mean’ wishcasting policy: everything in moderation. Growth is expected to clip along at a moderate pace, and inflation pressures are expected to moderate. What this means in practice is that they are likely expecting the run rate of nominal GDP to decelerate to 5% or so. As the chart below indicates, that slow of a pace has been difficult to maintain for more than a quarter at a time during this expansion. The Q3 GDP figure released tomorrow, however, might be one of those occasional hiccups. Nevertheless, Macro Man is struck by the sort of inverse ‘Lake Woebegone’ expectations of the market. Every institution that Macro Man has professional dealings with is calling for real GDP growth to be on a 1 handle, yet the Bloomberg consensus is for 2%. Truly, a market where everyone is evidently more downbeat than consensus! Give that we evidently remain in a range and that the initial GDP reading is highly dependent on the (volatile) trade and inventory assumptions, Macro Man will look to fade any gap higher in bonds after the report. He doubles the short Treasury position at 108.

.

{kind=link} Elsewhere, foreign exchange remains a sucker’s game. The noise to signal ratio is very high, with ranges persisting and flow dominated by short term traders and, the rumour goes, sovereigns. Macro Man was simultaneously irritated and amused to see confirmation that China is, after all, a Communist country. The State Administration for Foreign Exchange, who regulates the domestic currency market and manages the country’s $1 trillion FX reserve portfolio (partially by day trading EUR/USD and/or selling volatility), issued a new regulation today prohibiting domestic banks from quoting CNY NDFs offshore. There was no reason given, but it presumably has something to do with eliminating the possibility of arbitrage profits between the onshore and offshore markets. As a result, the offshore market will become wider, less liquid, and less reflective of onshore fundamentals. For SAFE, evidently, currency speculation must be centrally planned and administered by the public sector agency set up to do it, e.g. themselves. That the regulator is essentially destroying private sector competition for profits with the stroke of a pen goes a long way to explaining why this market remains one with many more visible losers than winners.

Elsewhere, foreign exchange remains a sucker’s game. The noise to signal ratio is very high, with ranges persisting and flow dominated by short term traders and, the rumour goes, sovereigns. Macro Man was simultaneously irritated and amused to see confirmation that China is, after all, a Communist country. The State Administration for Foreign Exchange, who regulates the domestic currency market and manages the country’s $1 trillion FX reserve portfolio (partially by day trading EUR/USD and/or selling volatility), issued a new regulation today prohibiting domestic banks from quoting CNY NDFs offshore. There was no reason given, but it presumably has something to do with eliminating the possibility of arbitrage profits between the onshore and offshore markets. As a result, the offshore market will become wider, less liquid, and less reflective of onshore fundamentals. For SAFE, evidently, currency speculation must be centrally planned and administered by the public sector agency set up to do it, e.g. themselves. That the regulator is essentially destroying private sector competition for profits with the stroke of a pen goes a long way to explaining why this market remains one with many more visible losers than winners.Sadly, Macro Man’s two forays into currencies are among the losers. The RBNZ did its part in easing his pain, though, as the statement overnight opened the door (very slightly indeed, mind) to acknowledge the contemplation of rate cuts at some point in the future. Macro Man does not expect rate cuts over the next six months at least, but given that 25 bps of tightening was priced as a done deal by year end, the squeeze in NZD and kiwi rates could have further to go. Per yesterday’s post, Macro Man battens down the hatches on the short NZD/USD position by trailing the stop loss down to 0.6600, just above the day’s high. The surge in the energy complex has brought the portfolio back into positive territory since inception in early September, so now is no time to leave money on the table with shoddy risk management.