The moment of truth/obfuscation/irrelevance (delete as appropriate, depending on your opinion of the Fed) is nearly upon us, with the Fed slated to release the statement accompanying its unchanged monetary policy in just a few hours. Will they acknowledge the decline in headline CPI, which was a statistical certainty? Will they take note of the Houdini-like appearance of 810,000 jobs, which goes a fair way to explaining why the unemployment rate is low and labour compensation is high? Will they focus on the continued mixed nature of sentiment data, or instead bask in the positive income shock that is $0.70 off a gallon of gasoline in the matter of two and a half months? Or will they once again offer wisdom on the housing market, fearing the worst if the apparent stabilization does not materialize? It's hard to say, and with Treasuries and the dollar perched at an inflection point, they can direct the next 10-15 bps in the 10 year depending on whether they choose to focus on downside or upside risks to nominal GDP growth. For this reason, markets have concluded that, as Huey Lewis sang in one of his darker moments 20 years ago, it is 'hip to be square'-hence the lack of follow through on the recent selloffs in Treasuries and EUR/USD, among other things.

However, with uncertainty so high, now is the perfect time to own options, as we could well get a decent move one way or another. Therefore, per last week's game plan, Macro Man re-establishes his long March 107 straddle at 1-28, the same price he took it off for. No savings was made, but no cost incurred, either.

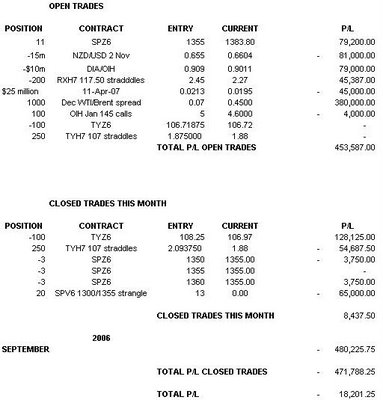

Elsewhere, the NZ CPI was not as dovish as Macro Man had hoped, but not as hawkish as it could have been, either. The market has voted with its feet thus far, taking the kiwi lower, but with the RBNZ lurking Macro Man remains wary. He trails the stop in NZD/USD down to 0.6700, with a further tightening of the screws coming after the sundry monetary policy reports later today.

Oil seems to have stabilized, though with inventory data later today that could prove temporary. Nevertheless, with the DIA/OIH spread (finally!) in profit, Macro Man can breathe a sigh of relief. A further improvement today should take the since inception portfolio P/L back into the black.

However, with uncertainty so high, now is the perfect time to own options, as we could well get a decent move one way or another. Therefore, per last week's game plan, Macro Man re-establishes his long March 107 straddle at 1-28, the same price he took it off for. No savings was made, but no cost incurred, either.

Elsewhere, the NZ CPI was not as dovish as Macro Man had hoped, but not as hawkish as it could have been, either. The market has voted with its feet thus far, taking the kiwi lower, but with the RBNZ lurking Macro Man remains wary. He trails the stop in NZD/USD down to 0.6700, with a further tightening of the screws coming after the sundry monetary policy reports later today.

Oil seems to have stabilized, though with inventory data later today that could prove temporary. Nevertheless, with the DIA/OIH spread (finally!) in profit, Macro Man can breathe a sigh of relief. A further improvement today should take the since inception portfolio P/L back into the black.

{kind=link}