Fed as expected...sorta? Is this USD rally and selloff in the front end because the FOMC didn't mark down 2018 dots and Yellen says gradual rate hikes will continue? They did have to keep that December dot implying a hike--if they took it out it would be a major mistake to try to put the toothpaste back in the tube and hike after all--but if the data rolls over it will be no surprise if they simply decide to stand pat. Maybe more indicative of market complacency and long technical positioning than anything else...I dunno....go ahead and whack bids on the levered VIX vehicle of your choice. I genuinely don't believe the December dot is a fundamental change, or hawkish signal.

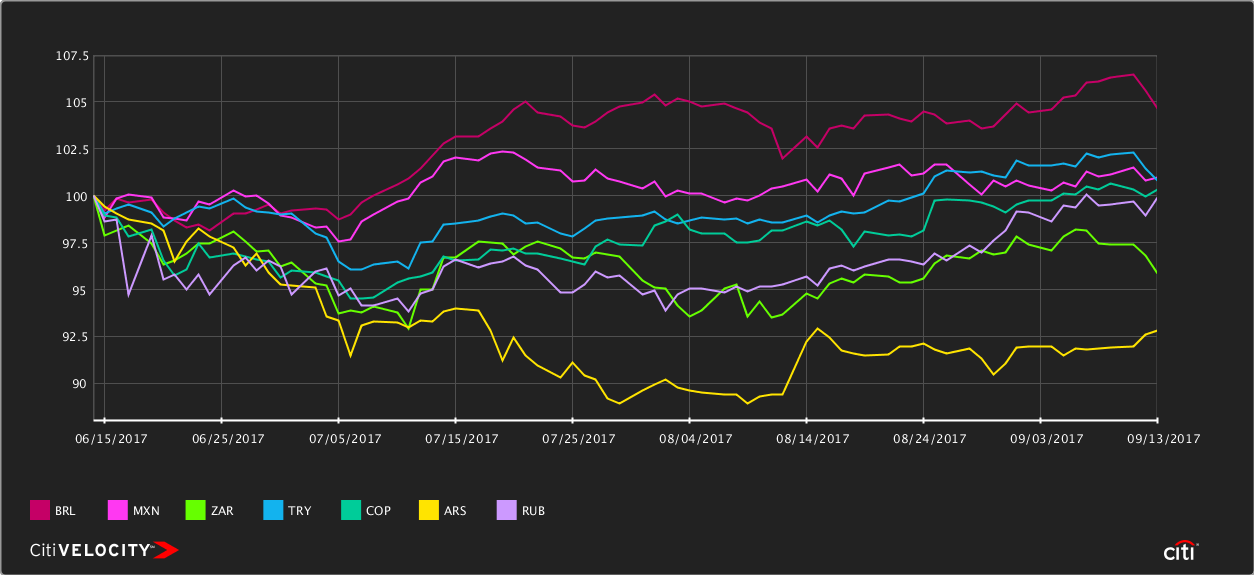

Deep dive time again folks...there was a quick mention on usd/ars in the comments last week--circling back to this market, the Argentine peso has been left out of the EMFX fiesta the past few months.

Deep dive time again folks...there was a quick mention on usd/ars in the comments last week--circling back to this market, the Argentine peso has been left out of the EMFX fiesta the past few months.

ARS has been a notable laggard over the last three months, and finishes dead last YTD, according to data from WSJ. Yet carry is over 20% per annum--a veritable tractor beam for sucking in EM and crossover investors.

While there has been continued optimism in the local political scene and inflows have continued, there is a divergence between tighter USD bond spreads and the value of the peso. Let’s break this down into its component risks.

The Credit

Frequent readers will remember my post on the government’s issuance of a 100-year bond back in June, an event many in the media, and even some old hands like Howard Marks, viewed as the end of times. The point I wanted to make is that it was driven by reverse inquiry--real money wanted a more capital efficient vehicle to express a positive view of Macri and his reforms, and the duration was better defined as a leveraged bet on medium-term credit improvement rather than a bet that the country wouldn’t default on my grandchildren.

If all goes well until year end, a couple of PMs that made that reverse inquiry are going to clear a pretty nice check...After tapping the market around 90, the century bond is going looking to take a crack at par...and that’s not even counting over 7% carry, payable in USD and settled in New York.

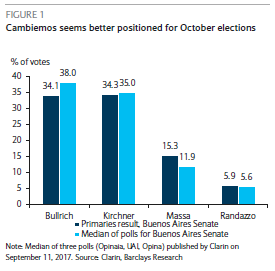

After winning an important election in June, Macri’s ratings are still relatively good by the standards of Latin America--with approval ratings ranging from the 40s to low 50s, and polling for the upcoming senate race shows Macri’s candidate with a small lead over former president Cristina Kirchner. A victory in this election would be a big signal that Macri’s platform will be sustainable politically and improve the odds for him to win a second term.

I continue to believe global trends will buy time for Macri’s agenda to work--and while an Argentine election is always a bit of a crapshoot, the trend in Latam favors center-right candidates as the pendulum has swung away from the neo-socialist candidates that won victories in the early 2000s in Argentina, Brazil, Peru, Ecuador, Venezuela and Chile.

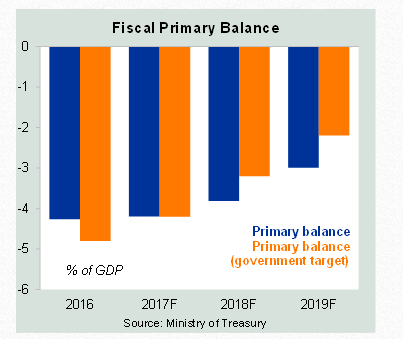

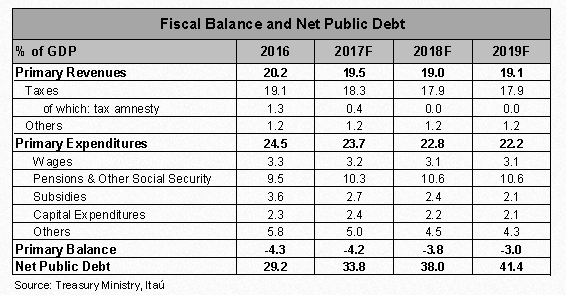

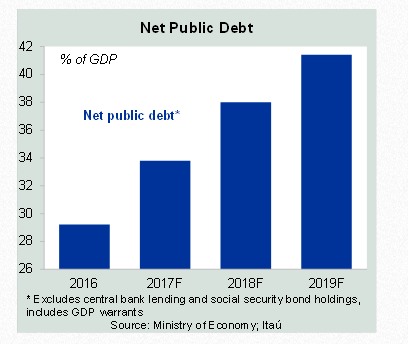

Beyond the political risk, the fiscal situation is far from healthy--and will require a bout of austerity and likely significant spending cuts. The 2017 primary balance is a nasty -4%/GDP, which means the government is going to be running up a larger debt load for the foreseeable future.

With the economy still sluggish, here’s another chart that keeps the reformists awake at night:

Put another way, just as in Brazil, nearly 40% of the budget is going to pensions and social security obligations. That is simply strangling government finances. Slashing these benefits to cut the budget deficit isn’t going to be easy on the economy, on voters, or on the government’s relationship with unions.

Will Macri have the political capital to push through a pension reform? I’m skeptical--higher taxes seem more likely, but that can’t fully close the gap. A “fiscal rule” law would be a politically palatable intermediate step. Either way, as the charts below show, an acceleration of public debt at this pace for a sub-investment grade credit is simply unsustainable.

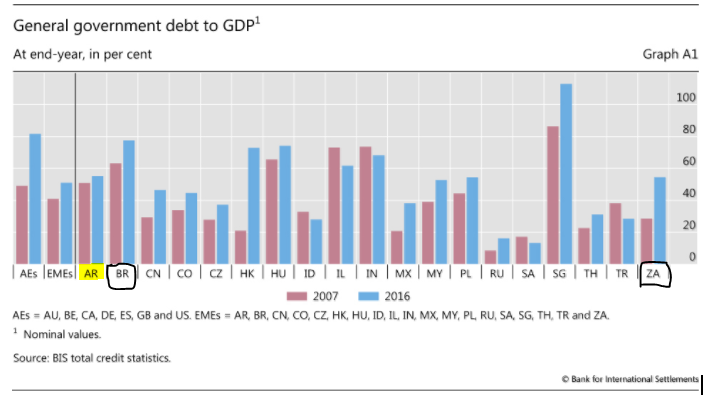

Which brings us to how Argentina fits into the broader EM sovereign credit universe. Below I have highlighted the public debt burden in Argentina, and circled a couple of similar credits--Brazil and South Africa.

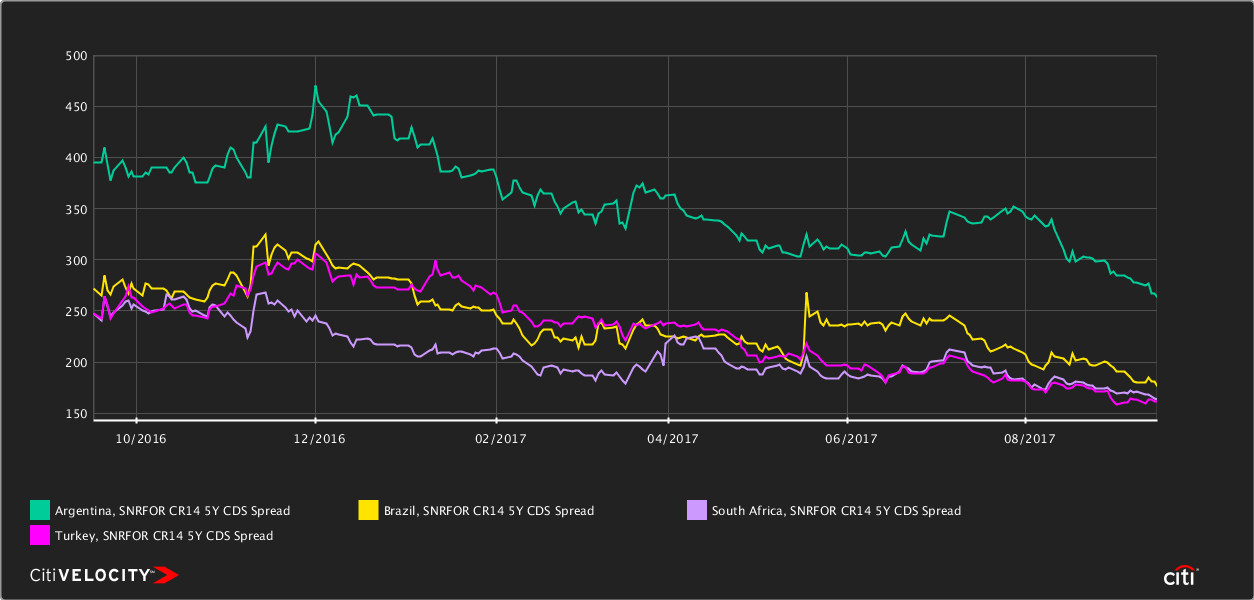

From a debt sustainability perspective, Brazil and South Africa have similar burdens--Brazil is certainly trending fast in the wrong direction--but has a much bigger stock of domestic savings and (maybe) a reform movement of its own. South Africa has a worse political situation but a stronger domestic economy and not near the primary budget gap of its Latin brethren. Pairing that with a look at 5y CDS levels (as a proxy for credit spreads at large) demonstrates just what kind of premium investors are being paid in Argentina:

Yeah, juicy….so you can see why that kind of premium compared with a center-right, technocratic, reformist government is an attractive combination for foreign investors, especially when those investors have been starved Argy exposure (and yield) for years as they were locked out of international markets.

My takeaway on the credit is that there is much more beta than alpha at these levels--I continue to believe in the positive local theme, and it will work so long as the “reach for yield” theme works globally. I expect Cambiemos will win in October, which should provide a short-term tailwind, but the medium-term is fraught and highly dependent on local and international factors that could throw the reform movement into a state of chaos.

The Currency

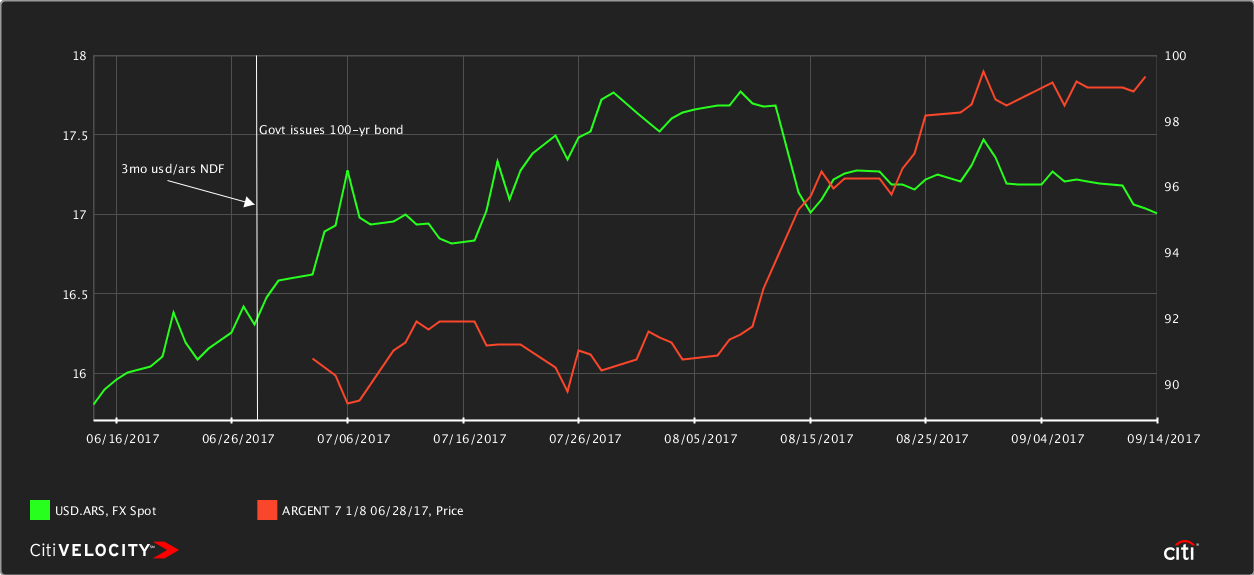

As the century bond ripped 10 points in less than three months, an investor that sold a 3mo usd/ars NDF at the same time has essentially made nothing. Spot ARS has cheapened, but with that spicy 20% carry (in ARS), you’re basically flat here.

So what gives? USD has weakened across the board….”risk-on, reach for yield, buy EM” is arguably the theme of the year...Macri’s coalition performed well in primary elections and remains relatively popular….What’s not to like about ARS?

There are some fundamental and technical headwinds that have prevented further ARS appreciation. The first is a combination of the political economy of the Macri administration and the continued triage of the damage wrought by years of the Kirschners populist policies.

The first is local real rates. ARS rates are 20-22% are for a 1-3mo non-deliverable forward (NDF). The idea here is that if you want to buy pesos via an offshore derivative, you receive an ARS asset vs. a USD liability, to be settled in New York at an agreed, published fixing rate linked to the spot rate at the maturity of the derivative contract.

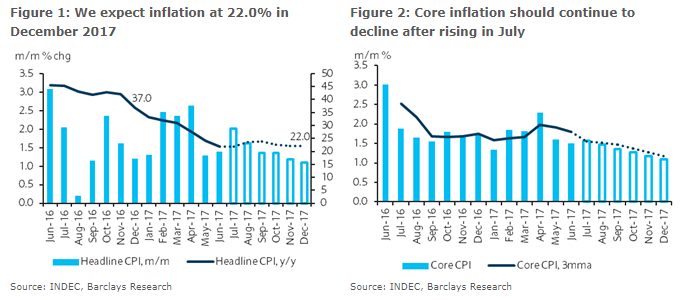

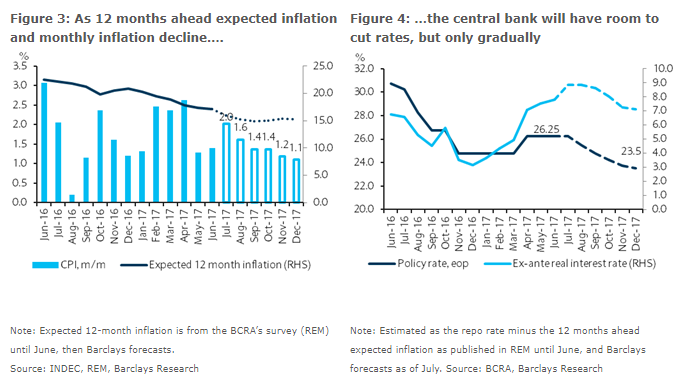

While rates are fantastically high by global standards, much of that value is eroded by inflation around 22% YoY. As I have mentioned before, at that level of real rates in Argentina you are highly levered to a positive economic and political outcome rather than a simple “cash and carry” trade. You’re gonna need help…. from inflation, from the BCRA, from Macri, and from voters. Will BCRA make progress in the battle against inflation? Will voters be patient enough with reforms to continue to support the government?

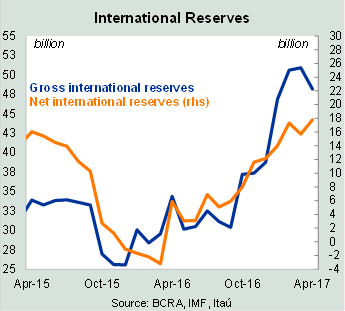

Another headwind for the peso is the central bank’s desire to accumulate foreign reserves after years of drawdowns. Earlier this year the BCRA announced they would continue to increase international reserves. The central bank is targeting a reserves-to-GDP ratio around 15% over the next two years, which according to a report from the Brazilian bank Itau, would require an increase of 48.3bn USD.

The central and provincial governments will issue more bonds in USD during that time, which the central bank will exchange for pesos. But there will be a significant gap between USD issuance and the accumulation to bring reserves to adequate levels.

That means the central bank will be on the bid in USD when there is significant appreciation not tied to improvements in the political situation and/or sovereign risk. Getting back to the opening point, that also fits with the administration’s incentive to keep ARS competitive and allow export markets to heal and grow after years of capital famine. Similar to the credit, this is an attractive carry trade if you buy into “the story”, but not without its risks. I think ARS will appreciate over time, but it won’t be quick.

A trade I like more than the credit/politics driven trades in outright usd/ars or the USD bonds is the local t-bill market, known as Lebacs, which sport a yield of roughly 27% for maturities under one year. The catch here is that you have to bring USD into the country, sell it in the spot market, and buy the Lebacs.Then you hedge that ARS exposure by buying a usd/ars ndf to the same maturity in the offshore market around 22%. You pocket 5% per annum for running the local credit risk and risk that the government again implements currency controls.

Why does this spread exist? I think it is a combination of three factors: 1) the bid for spot USD by the BCRA, 2) bullish fast money traders hitting bids in front end NDFs (Johno, I’m looking at you), and 3) higher local yields driven by supply of lebacs the BCRA issues to sterilize the ARS they are selling into the spot market when they buy dollars. Quite simply there is a shortage of dollars in the local market and there aren’t enough investors brave enough to step into the breach.

Any EM trader with stripes on their back, or one with even a cursory knowledge of Argentine financial history will tell you the catch there--one day the government may decide to implement capital controls because they don’t want to give your dollars back. You’re stuck with Argentine pesos with no way to exchange them back into dollars. Ask any US airline with connections to Caracas how that worked out for them.

But compared to 5yr CDS under 300bps, this is a very attractive spread. An investor sells USD into the local market and receives about 500bps with no FX or duration risk. The lebacs and ndf hedges mature every one to three months, so you have the opportunity to get out if the fundamentals or political situation deteriorate. That is unlikely--Macri’s structural reform agenda may or may not materialize, but he has embarked upon capital market reforms that aren’t going to be unwound before the presidential election in 2019.

Long story short, at 500bps this spread is well in excess of the risk that the government will again implement capital controls over the next 3, 6, or 12 months. It’s a clean single to right field if you have the cash and local legal set up to do it.

Not sure if the MM audience is well versed in the dynamics of on-off spreads, but feel free to step up and throw in your two cents on the credit or the local scene.

Shawn

TeamMacroMan2@gmail.com

@EMInflationista

Shawn

TeamMacroMan2@gmail.com

@EMInflationista

22 comments

Click here for comments"bullish fast money traders hitting bids in front end NDFs" -- you got me!!

ReplyFantastic post, Shawn. Thank you. My thinking on USDARS is: 1) to gain credibility, the BCRA is going to have to keep policy tight; 2) BCRA excessively loosened in Q4 and (refreshingly for a CB) owned up to the mistake and is all the less likely to repeat it; 3) after a quick 15% slide this summer and needing all the help it can get to lower inflation, I doubt they'd intervene to weaken the currency in the near-term (the horizon of fast money guys like me); the economy's rebound, ex-exports, and the expectation of a win for Macri's party in upcoming elections is a positive backdrop; on some BEER models, the currency looks cheap-ish. That said, I can't really disagree with any of your points. Fiscal sustainability is critical (without it, we can expect continuation of the old story of monetization and high inflation) and it's far from clear Macri will have the support to tackle it. You trade sounds great but suspect I'm not setup to efficiently implement it (between my banks' bid/asks and collateral requirements). Still, it's valuable to understand it and your explanation of the NDF forward points versus Lebac differential. Thank you!

Re the Fed, I thought: 1) the 1.5% 2017 core PCE projection and 1 hike dot count improved chances of a Dec hike given 1.5% doesn't assume much rebound in Q4 (I sold TUZ7 on that for a trade); 2) the 2018 median dot count for 3 hikes holding and one fewer dot below it (despite all the hand-wringing about recent inflation) was hawkish. Sure, Yellen wrapped it all in conditional statements and pointed out that the mean of participants' expectations were lower than the modes (forecasts), but she also downplayed inflation trends Brainard pointed to as a "statistical technique." Took profit too soon in some USDJPY I added right after the announcement, thinking the Fed's hawkishness had clearer implications for the front-end, but wonder about that now ... by signaling a Dec hike, the Fed has taken some pressure off EURUSD appreciation which maybe improves odds for an ECB decision to taper/reduce purchases in October, which in turn is bearish for global duration. The timing of ECB leaked dovish stories suggests some sensitivity around the 1.20-level (Nordea had a nice chart of this today).

Here's a question, how is that GOOGL -- a company that the world's best and brightest kids want to work for -- trades at the same 2018 forward multiple as the Russell?

Thanks Johno....re: your point on intervention, it is a semantic difference. The BCRA will be on the bid buying usd to replenish reserves--but they won't intervene to weaken the currency. Should flows and politics cooperate, it is a slowing of appreciation rather than any attempt to weaken the currency as per your point about inflation....BCRA wants to WIN....Whip Inflation Now!

ReplySo yeah, I continue to like the story for the same reasons as you--and I think the balance of risks favors long ARS via NDFs...but it's a slow grind.

Re: the fed, I continue to believe they are not signaling a Dec hike any more than they were before the meeting--if fed funds are pricing in 55% (or whatever it is now) chance of a hike, that's about right....b/c it should converge to 100% as data cooperates or asymptotically approaches zero if inflation, growth, payrolls, etc. fade. What does that mean for USD? I continue to believe we'll need to see the curve steepen before USD really gets trucking again, which I would define as a clean break of 1.17 in EUR.

The first set goes to DR....we'll see who takes sets two and three!!

MM, I can't resist one last comment on the geopolitical stage. Hey, Trumpy. Don't worry about rocket man. He has got your measure. There no betting on you or anyone else getting the rocket man to sit on that hedge fund desk , or any other desk on Wall Street. Any tariff's collected from the rocket man from this point will be regard as paid overdue arrears. Nor will you get the rocket man to New York or America without a rendition.

ReplyGreat Post! Now the question, how to bring USD into Argentina? Does the mrmacro mail address still function to have a discussion about it?

ReplyBest

I like Rocket Man, but I think Norma Jean is one of the most overrated songs of all time.

ReplyI believe the MM email address is going to get you the real Macro Man....no guarantees on his knowledge about the dynamics of Argentine legal custody...but you can ping me at TeamMacroMan2 {at] gmail.com.

Hey , Shawn. Have you finally figured it out that TeamMacroMan2 @ gmail.com doesn't need assistance from jockey's and trainers. Believe me, I spent my whole phd in racing learning how jockey's and trainers are the downfall of punters in the long run. My thesis was awarded a get of jail alive card :)

ReplyI did my time in trading jail, purgatory, or gulag. There are indeed a fat, slothful jockeys out there. But everyone needs a good trainer.

ReplyYou must know a good trainer , not need one. That's when the trouble begins.

ReplyYou must know him better than his horses otherwise the chocolate wheel at the casino is waiting for you my friend.

ReplyYou start talking horses, I immediately think of horseshit.

ReplySpeaking of... Is USD about to make a new low? Buy some gold.

Underrated Elton John songs: Grey Seal, Social Disease

ReplyExtremely Underrated Who song: My Wife

Dramatically Underrated Queen song: I'm in Love With my Car

Yeah, IPA. Horseshit hey! Maaaaaaaaaaaaaaaaaaate the eye just gets better :) I actually walked into the betting shop other day just to watch'em go around I couldn't even lift myself out of the chair to have a bet. I said fuck it, it was because I knew it was pointless. The Armoury is there now.

ReplyHey, IPA...famous last words....WATCH THIS

ReplyI'm not one to judge how one spends his free time, but when I was living in London I recall there were more men than punters hanging out in the local Ladbrokes. They were in what I called the "Nuthin' to Lose Club."

ReplySeeing the belly outperform today after getting (pardon the expression) horsewhipped post-fed. More punters than fundamentals--I expect we'll resume normal service on Monday.

The post and the previous on he century bond, misses to a couple of missporings. The market struggled to price the 100y paper and still struggles to price local duration. The t-bill story is ok, but nothing more than that. Now a 5y bei at 11%, implies the most spectacular failure of any modern CB running and inflation targeting regime. M

ReplyDo You Seek Funds To Pay Off Credits and Debts? PergoCF@cheerful.com ( PergoCF@qualityservice.com ) PergoCF@gmail.com Is Here To Put A Stop To Your Financial Problems. We Offer All Kinds Of Loan (Personal Loan, Commercial Loan, etc.) We Give Out Loan With An Interest Rate Of 1.00%. Interested Applicants Should Contact Us Via Email: PergoCF@cheerful.com ( PergoCF@qualityservice.com ) PergoCF@gmail.com

ReplyPlease Fill the Application Form Below:

- Complete Name:

- Loan Amount Needed:

- Loan Duration:

- Purpose Of Loan:

- City / Country:

- Telephone:

- How Did You Hear About Us:

Do You Need A Loan To Consolidate Your Debt At 1.0%? Or A Personal Loans * Business Loans etc. Interested Parties Should Contact Us For More Information Through Via E-mail: PergoCF@cheerful.com ( PergoCF@qualityservice.com ) PergoCF@gmail.com

Do You Need A Loan To Consolidate Your Debt At 1.0%? SuiteCapitals@gmail.com ( SuiteCapitals@post.com ) Or A Personal Loans * Business Loans etc. Interested Parties Should Contact Us For More Information Through Via E-mail: SuiteCapitals@gmail.com ( SuiteCapitals@post.com )

ReplyPlease Fill the Application Form Below: -

Complete Name: -

Loan amount needed: -

Loan Duration: -

Purpose of loan: -

City / Country: -

Telephone: -

How Did You Hear About Us:

Do You Need A Loan To Consolidate Your Debt At 1.0%? SuiteCapitals@gmail.com ( SuiteCapitals@post.com ) Or A Personal Loans * Business Loans etc. Interested Parties Should Contact Us For More Information Through Via E-mail: SuiteCapitals@gmail.com ( SuiteCapitals@post.com )

Do You Need A Loan To Consolidate Your Debt At 1.0%? SuiteCapitals@gmail.com ( SuiteCapitals@post.com ) Or A Personal Loans * Business Loans etc. Interested Parties Should Contact Us For More Information Through Via E-mail: SuiteCapitals@gmail.com ( SuiteCapitals@post.com )

ReplyPlease Fill the Application Form Below:

- Complete Name:

- Loan amount needed:

- Loan Duration:

- Purpose of loan:

- City / Country:

- Telephone:

- How Did You Hear About Us:

Do You Need A Loan To Consolidate Your Debt At 1.0%? SuiteCapitals@gmail.com ( SuiteCapitals@post.com ) Or A Personal Loans * Business Loans etc. Interested Parties Should Contact Us For More Information Through Via E-mail: SuiteCapitals@gmail.com ( SuiteCapitals@post.com )

Bitcoin Crypto Investment

ReplyMy investment experience with bitcoins.

There is no doubt that bitcoin is a trend today and there is a lot of success in the business world, because people prefer to save money in their wallets than in banks, last summer I lost about $54,000 due to the fall in the price of bitcoins. A colleague at work who knew my suffering in the field of bitcoin savings led me (aulakhkrupinder@gmail.com ) where I can store and invest my bitcoins with more than 100% profit margin. At first I was skeptical, so I decided to try it for just $500. I was amazed after 12 hours I made another $1,500 and was able to make an immediate withdrawal and since then I have invested and made more money. Investing bitcoins with aulakhkrupinder@gmail.com changed my life when I made more than $176,000. You can contact :aulakhkrupinder@gmail.com to Enjoy endless possibilities.

ReplyIt all happened as i stumbled into this email address blankatm002@gmail.com initially i was looking to get extra jobs to boost my salary and i found how the blank ATM card from this company gives you more than $20,000 all in 1 month. At first i though it was another internet scheme until i saw several reviews of how this blank card from this company has changed the lives of many without hesitation i ordered for the card and in less than 7 days it was delivered to me and the agent showed me how it works and it was even tested its been just 3 weeks and everything seems a lot less stressful this company has really changed my life and standard of living. I would love you on this site to visit blankatm002@gmail.com and get a card today to ease that stress and get good money its so quick.

Are you in need of Urgent Loan Here no collateral required all problem regarding Loan is solve between a short period of time with a low interest rate of 2% and duration more than 20 years what are you waiting for apply now and solve your problem or start a business with Loan paying of various bills I think you have come to the right place just contact us We Are Here To Show You A Better Way To Financial Freedom !!!

ReplyContact Us At : abdullahibrahimlender@gmail.com

whatspp Number +918929490461

Mr Abdullah Ibrahim

ReplyHi everyone. I saw comments from people who already got their loan from challot and then I decided to apply under their recommendations and just few hours ago I confirmed in my own personal bank account a total amount of $30,000 which I requested for. This is really a great news and I am advising everyone who needs real loan to apply through their email (challotloan@gmail.com) I am happy now that i have gotten the loan I requested