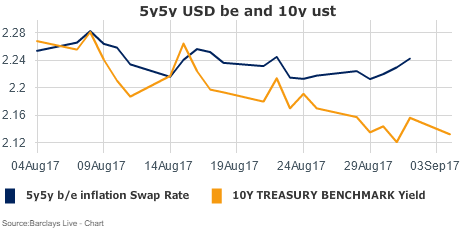

Rates rally, gasoline prices rocket higher, but the God of US Breaks has spoken….”5y inflation 5 years forward shall be between 2.21 and 2.28.”

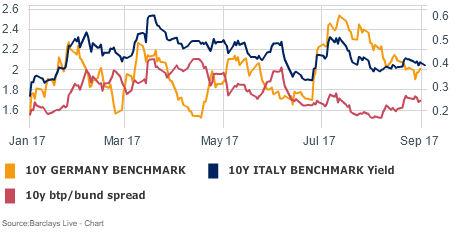

I had a couple of drinks with an ex-colleague...he’s French and was in town on vacation with his Italian girlfriend. Judging by the tail end of these graphs, they weren’t the only one on the famous European August holidays.

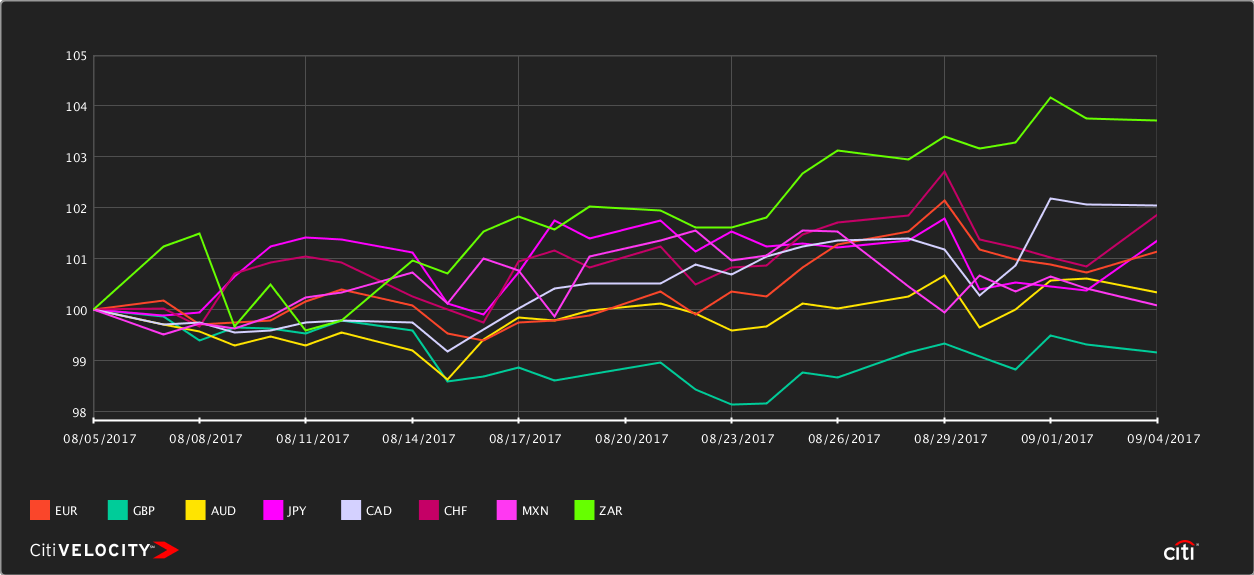

Similar story over in FX land...EUR continues to be the story of the year. ZAR made a run higher over the past couple of weeks, but nothing else notable.

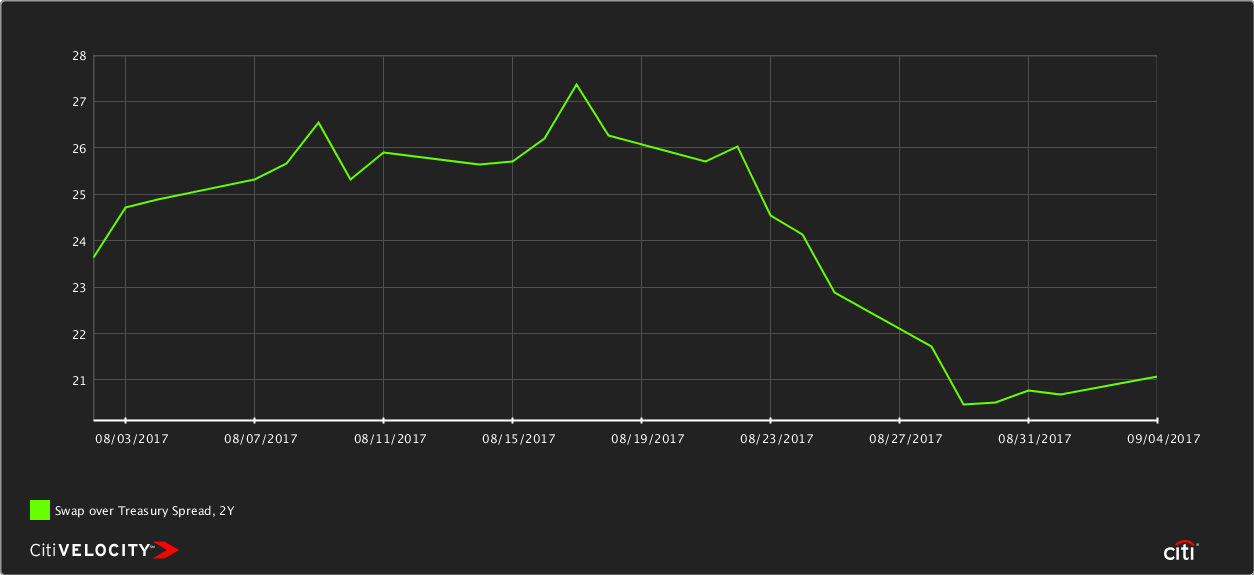

Which brings us to the always fascinating world of swap spreads. Hey, a market where something happened the past two weeks? In 2y spreads, a move down from 26 to 21 in a week gets some people very, very excited.

This means as rates were rallying, 2y swaps were outperforming 2y UST. Is this the debt ceiling rearing its ugly head? My guess here, and I'm open to other interpretations from those a little closer to the source... is that the FTQ bid from more North Korea noise combined with illiquid markets and the debt ceiling pushed more macro guys into buying eurodollars rather than front end UST futures.

I’ll take the other side here and call for a move back towards the mid-20s... I think the move in rates is a little overcooked, and even with Trump’s historic and downright bewildering ineptitude, I can’t see how a Republican president takes a Republican congress to the mat on the debt ceiling. They will find a way. And if North Korea nukes us, you could do worse than to be long swap spreads!

While it may not manifest itself in the front end of the US curve, there was another story that hit the tape late last week that I think is very important. Norges Bank, the manager of Norway’s bottomless pot of oil loot, released a letter to the government in which they call for some major changes to their management of their massive fixed income portfolio.

To quote (emphasis mine):

“For an investor with 70 percent of his investments in an internationally diversified equity portfolio, there is little reduction in risk to be obtained by also diversifying his bond investments across a large number of currencies.

The benchmark index for bonds currently consists of 23 currencies. Our recommendation is that the number of currencies in the bond index is reduced. This will have little impact on risk in the overall benchmark index.

We propose that the Ministry goes back to a specific list of currencies for the bond index rather than leaving this decision to the index supplier... The most liquid market for bonds is currently that for US Treasuries, followed by those for bonds issued by countries in the euro area and the UK...An index consisting of bonds issued in dollars, euros and pounds alone will be sufficiently liquid and investable for the fund.”

The benchmark index for bonds currently consists of 23 currencies. Our recommendation is that the number of currencies in the bond index is reduced. This will have little impact on risk in the overall benchmark index.

We propose that the Ministry goes back to a specific list of currencies for the bond index rather than leaving this decision to the index supplier... The most liquid market for bonds is currently that for US Treasuries, followed by those for bonds issued by countries in the euro area and the UK...An index consisting of bonds issued in dollars, euros and pounds alone will be sufficiently liquid and investable for the fund.”

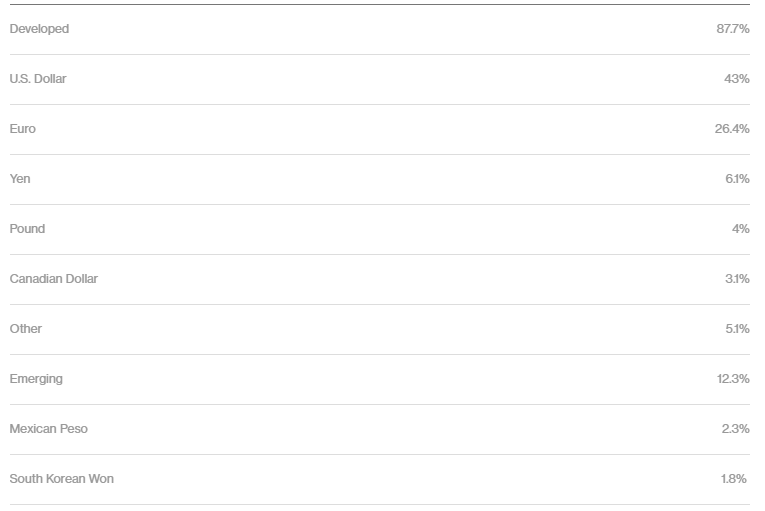

The letter says that the new benchmark would be roughly 58% US Treasurys, 38% European debt, and 8% UK Gilts. Here is the breakdown now:

The big losers here are Japan, Canada, and the entire emerging market bucket, which the letter goes out of its way to bag on.

So at some point in the next year there is likely to be some outflows from EM local debt and into US, Euro and UK paper. While that should be nominally positive for my long swap spread trade, the larger impact will be felt elsewhere.

This move away from EM debt is a radical departure from the commitment this fund made to the EM asset class back in 2012, when they abandoned the market-cap weighted index method, which put them into big, heavily indebted countries like Japan, Spain and Italy, at the expense of EM. They switched to a GDP weighted method, which was a big move.

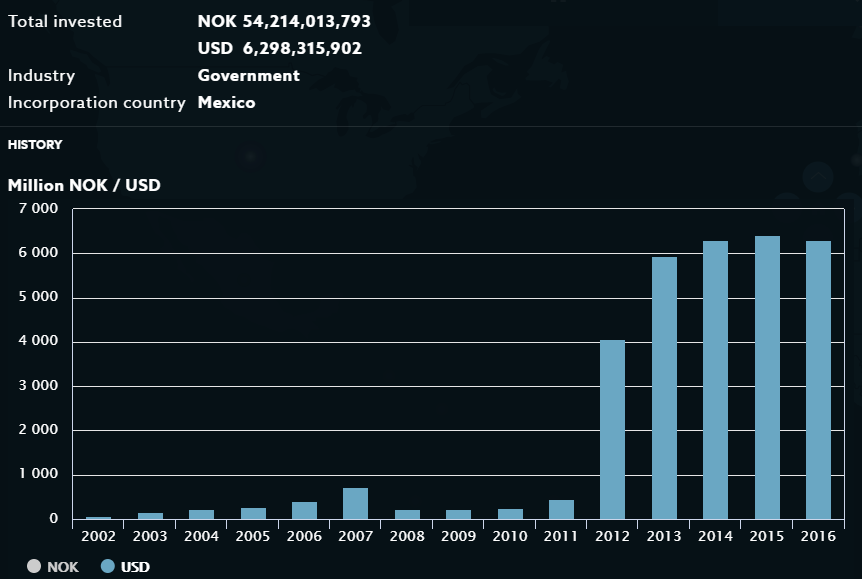

Here is what happened to the net holdings of Mexican government debt when they made the switch:

That's right, in a $70bn (now $100bn) bond market, Norges basically went from nothing to $4bn in 2012, and then to $6bn in 2013...but not right away...they started buying after the selloff driven by the taper tantrum, and didn’t stop the rest of the year. Rates ground lower relentlessly and swap spreads were the story of the year.

So the move to reverse that could be a big deal in EM, especially for debt-thirsty countries like Mexico that rely on foreign investors to plug their fiscal gap.

And given the size of the fund and its exemplary quality of management over the years, this could be a leading indicator for other SWFs and large pension fund managers. Their conclusions are relatively radical--zero diversification benefit...liquidity problems...a poor index composition...you can feel the distrust in the asset class when you read the letter.

Will this be the day the second generation of EM inflows rolled over? Stay tuned!

Shawn

TeamMacroMan2@gmail.com

@EMInflationista

Shawn

TeamMacroMan2@gmail.com

@EMInflationista

10 comments

Click here for commentsThis is awesome article.

Replyhttps://www.reetresult.co.in

https://www.resultview.in

https://rrbresult2016.co.in

https://www.exambaba.in

https://sabsehatke.com

Nice piece, Shawn. Thank you.

ReplyIn FX, the USDCNY move was notable. The macro pundits have been wrong on virtually everything this year. No wonder MIFID research prices are in free fall. No one knows anything, or worse, when they think they know something, they're wrong. Best research is right here at MM :) Shawn has had some excellent calls.

The 2Yr note always lags when we have these debt ceiling dramas. It was the same last time in 2013. The 2yr part of the curve gets hit (vastly underperforms) along with T-Bills. It all reverses after they finally raise the debt ceiling.

Replyexactly...wave in TU invoice spreads...

ReplyI'm going to write up a quick piece on China, CNY and base metals...despite your kind words I was with the consensus believing the credit impulse slowdown story--maybe it will still come, but nothing to suggest it yet.

Kinda surprised by the strength of the bull flattening today--anyone have a better explanation than the geopolitical risk FTQ story? Seems inconsistent with continued USD weakness.

I would say at least half of the move in headline 2y swap spreads from 27 to just below 21 was just due to unwind of the (now old) 2y note trading deeply special in repo. Once the repo specialness faded thru the 2y auction, 2y spreads gave up about 3 bps. The other 3 bps is debatable, but my guess is it's partly due to market participants suspecting that the Harvey aftermath reduced the chances of a government shutdown and increased the odds of a debt ceiling resolution (the headline article on BBG was from GS research I think). The quicker a debt ceiling resolution is in place, the quicker Treasury can issue bills/coupons to buff up its cash balances, which depresses 2y spreads, as it compresses LIBOR-GC basis. 3M LIBOR has remained very sticky, partly as prime fund AUM has steadily ticked up this year post MMF reform. Fundamentally I think these spreads are too wide, but nevermind fundamentals for now.

ReplyI got that wrong/with consensus too. Was looking for some slowdown in China starting this summer.

ReplyExcellent Post...I must thank you for this informative news....I appreciate all your efforts.Thanks alot for your writings......Waiting for a new 1...Please visit our wonderful and valuable website:

ReplyPackers And Movers Chennai

@snipez, you're absolutely right on the repo impact on 2yr spreads, untangling the two moves looking at TU invoice more or less ties out to your 3bps. re libor/gc, I have pretty poor visibility of this from my seat--how has that spread moved over the past month or so?

ReplyA few observations before I delve into that backlog of research reports hundreds of pages long ...

ReplyThere's a view out there that Sintra marked the beginning of a synchronized normalization to get ahead of "financial stability" problems. Maybe. Looking around the DM world, where would you have to worry about that, i.e. where are the asset/housing bubbles? Canada, Australia, Sweden, Norway. Eye-balling it, I'd say normal right now is a policy rate of 1.25-1.5%. Australia is already there, but Canada, Norway, and Sweden aren't. After today, Canada is at 1% and 1Y forward OIS is right in the middle of that 1.25-1.5% range. The statement doesn't at first glance suggest to me greater odds of an extended hiking cycle versus one-off removal of accommodation, and rate markets seem to back this up (bank acceptance futures curve flattening a bit today). By this paradigm, Norway is perhaps next, with its policy rate at 0.5%. Then there's Sweden ... they have the sequencing issue of tapering QE first, and I think RBA's Lowe would probably put them in the "inflation nutter" camp too and arguably Swedish inflation isn't as strong as headline figures suggest.

Of the above, Norway seems the best bet from here, but I've been nervous about oil. So hedge out the oil exposure? But there's real tail risks in Venezuela and Iran ...

Who's looking for another surge in EURUSD from here? Anyone? The most bullish stuff I've seen looks for a correction or pause here, but given how quickly and persistently markets price regime changes (think of the EURUSD and USDJPY moves when they introduced QE), I'm skeptical. More than that, I'm long via 2-month option structures. Maybe money down the toilet.

Nice chart in Daily Shot today: 10Y yield versus Global PMI. What gives?

Seen lots of commentary on gold. Excitement about chart "levels." What I see is a metal that's a function of real rates and USD (against INR, CNY). And it's trading right where it's supposed to be. Big yawn. View on gold? Tell me view on those variables. What causes the relationship with those variables to break? Maybe Trump's policies antagonizing so much of the world that economic blocks break away from settling trade in USD. But what would then use instead? Gold? Is it really a big enough market to take the place of USD, with its depth of USD-denominated "riskless" assets?

Are you in need of Urgent Loan Here no collateral required all problem regarding Loan is solve between a short period of time with a low interest rate of 2% and duration more than 20 years what are you waiting for apply now and solve your problem or start a business with Loan paying of various bills I think you have come to the right place just contact us We Are Here To Show You A Better Way To Financial Freedom !!!

ReplyContact Us At : abdullahibrahimlender@gmail.com

whatspp Number +918929490461

Mr Abdullah Ibrahim