A couple of charts and some thoughts to follow up on Detroit Red’s post about the potential for a

bounce in USD.

There has been a clear break in what is historically a strong correlation between the 1y3y US/EU interest rate spread--DR highlighted this in looking at breakevens and copper--I think this chart refines that point and shows there is very little change in medium-term inflation expectations in either market, as proxied by the spread of short-term rate expectations 3 years from now. Yet EUR (and pretty much every other currency) has been ripping vs. USD since this correlation broke down over the past couple of months. So something else is going on here.

DR circled the right factor by looking at copper. This breakdown coincided with the time when cooper went from having a nice run to giving (old) traders flashbacks to 2005.

Yet this is the second derivative--copper is cruising because of resurgent global demand--which is code for “China.” the PBOC has had more success stifling capital flight this year, which has contributed to the USD move--but as I highlighted here in a post last week, that misses the broader point that the growth trends in China are looking very, very good.

Stronger Chinese demand is the jet fuel for the German export machine--so while that strength may not manifest itself in interest rate differentials it certainly does in capital flows and long-term expectations for return on capital, both of which were at historical extremes for EUR in 2016 after the ECB finally pulled the trigger on QE. Yet since then the euro area current account surplus has only continued to rise.

Similarly, as I noted back in June when this move was getting going, technical positioning in the EUR was also coming off of perma-short levels. This doesn't necessarily show up in CTFC spec charts--much of the outflows were domestic corporates and real money fleeing negative rates and leaving foreign purchases of bonds and equity unhedged. As the economy rebounds, that money is repatriated or hedged back into EUR.

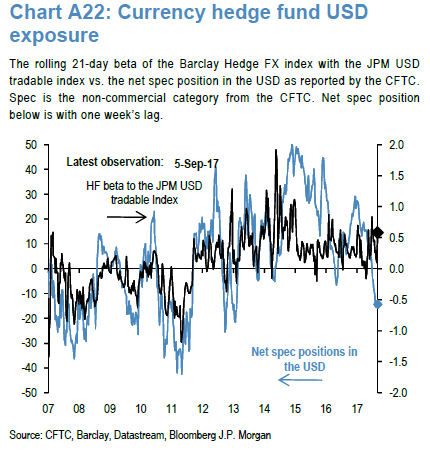

To the extent there is any tradable info at all in CFTC spec positioning charts, I dug up this on current USD positioning--a dramatic shift towards short USD over the past month--but note how long, in size and duration--the spec community was in USD pretty much non-stop since 2014, with only one real reversal last year ahead of the US election. Bottom line: the market is short USD...but not in any meaningful way, especially compared to the tailwind of economic growth and trade flows in Europe.

(the blue line is the spec position...the black line is a dubious measure at best)

And forward rates at large popped last week but still not getting away from themselves, which argues the market hasn’t quite bought into the economic momentum story yet.

To the extent there is any tradable info at all in CFTC spec positioning charts, I dug up this on current USD positioning--a dramatic shift towards short USD over the past month--but note how long, in size and duration--the spec community was in USD pretty much non-stop since 2014, with only one real reversal last year ahead of the US election. Bottom line: the market is short USD...but not in any meaningful way, especially compared to the tailwind of economic growth and trade flows in Europe.

(the blue line is the spec position...the black line is a dubious measure at best)

And forward rates at large popped last week but still not getting away from themselves, which argues the market hasn’t quite bought into the economic momentum story yet.

Looking at economic expectations and interest rate differentials there is good reason to believe there could be a reversal in USD, but the big driver is China and the related moves out of the US and into, well, pretty much anywhere. Is the short USD trade overcooked? Maybe, but...

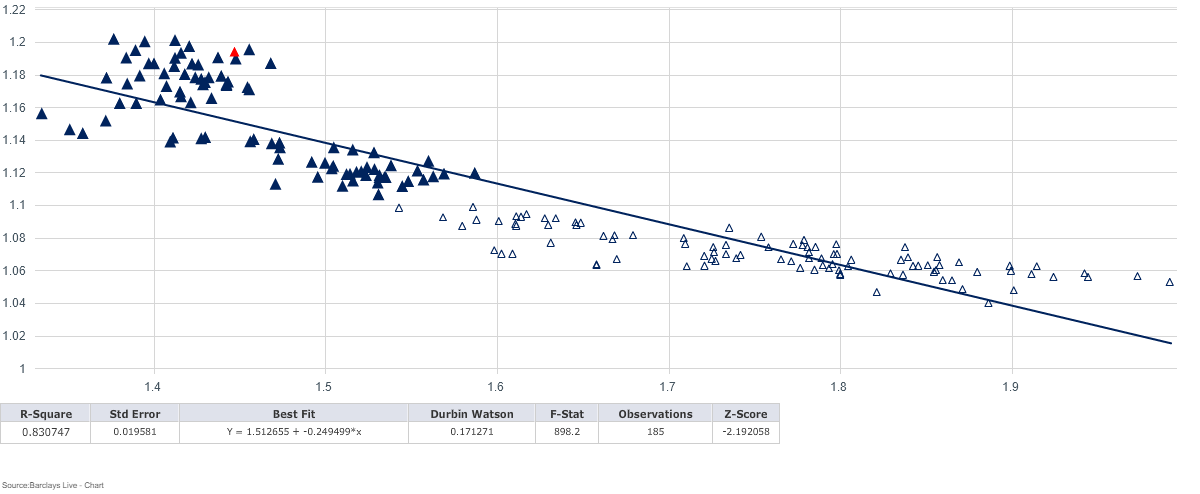

As much as both DR and I want to avoid the forecasting and prediction game….there will need to be a catalyst for a significant reversal, unless we are just catching knives for a move back to 1.17, which would be what the mean-reversion/regression scatter would seek to target. That leaves a structural long USD position on the wrong end of a few pain trades--an air pocket in Chinese growth, lower commodity prices/demand, a train wreck in corporate debt and/or EM, or….higher US inflation, a selloff in US rates, a steepening of 2/10s, or a more hawkish FOMC.

Frequent readers of the blog will know I’m not betting heavily on any of those--I agree that there is some evidence that the market is too complacent to an acceleration in wages or demand-pull inflation, but until I see evidence to suggest otherwise, I’ll stick with what this guy is says:

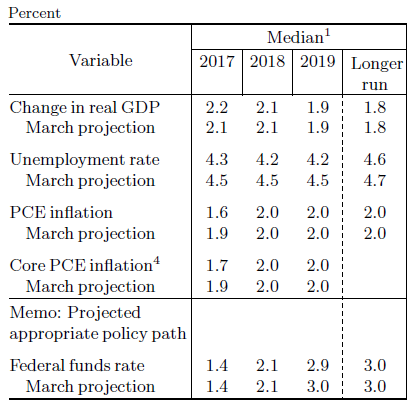

Turning to the Fed…the higher than expected CPI print last week did indeed wake up a few traders to the notion that there is indeed a Fed meeting next week, and the quarterly one where we get an update of the Summary of Economic Projections. Let's take a look at what might change.

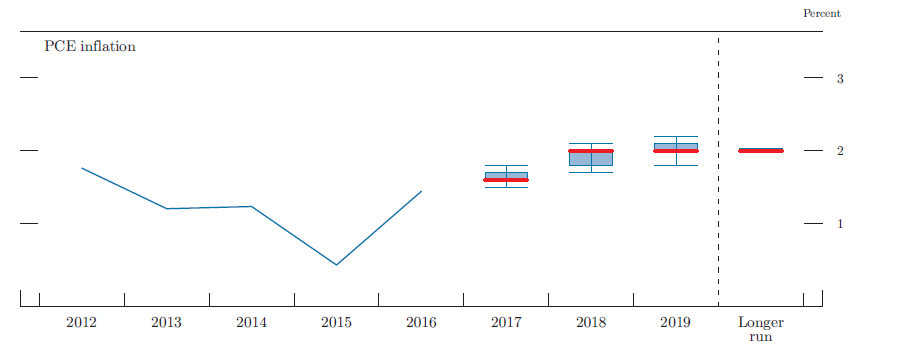

Here is a summary of the median responses from the governors were in the June SEP.

I don’t think there is a great argument that we will see much change in any of those variables--while GDP for 2017 could be marked lower, it will be reversed out with higher estimates for 2018 due to one-offs from Hurricanes Harvey and Irma.

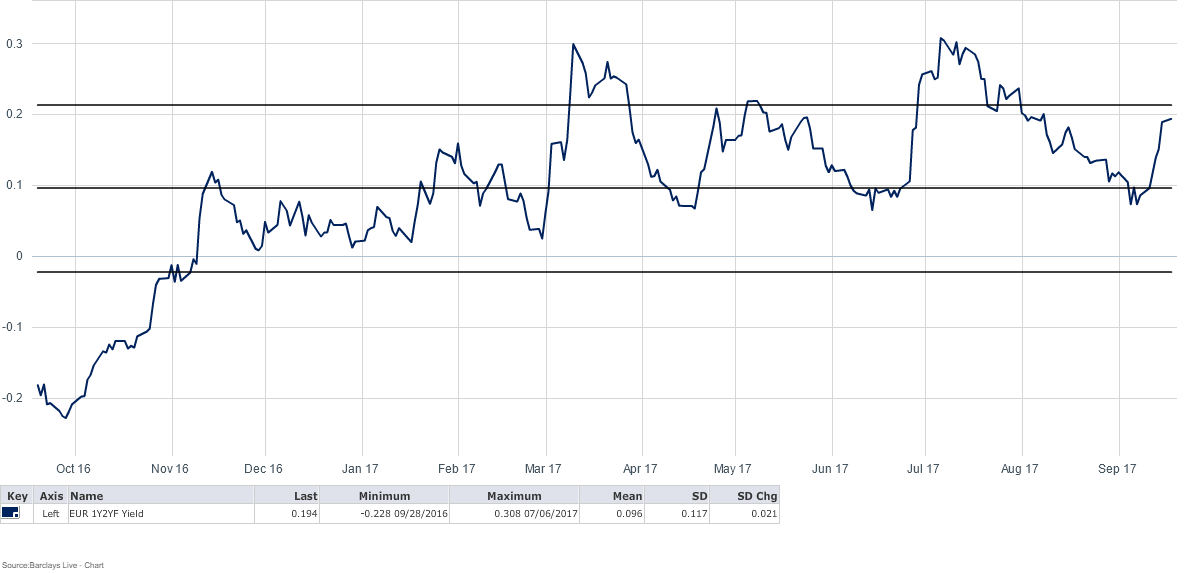

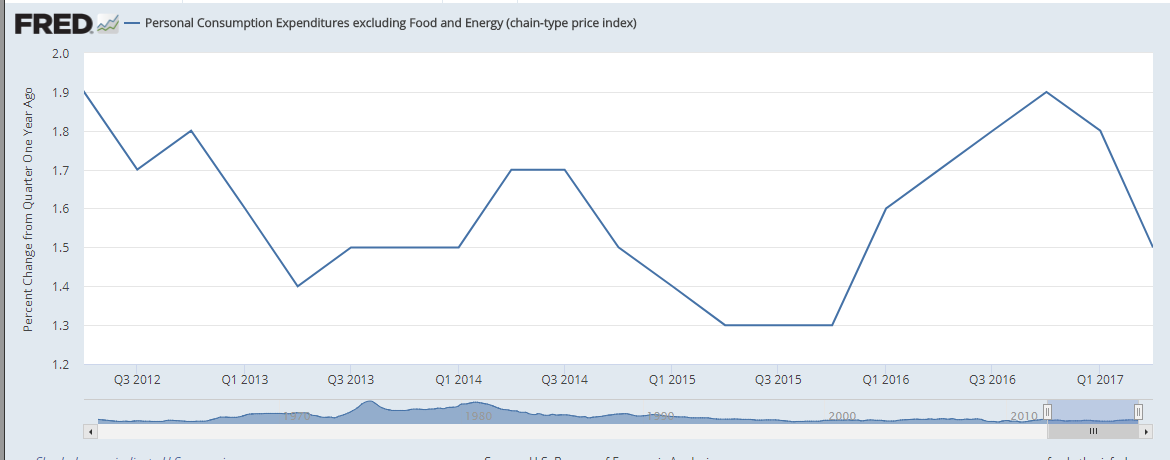

PCE inflation has been the story of the year, as the Fed has wrestled with “the conundrum” of lower inflation and higher employment.

While you see that the governors already marked down inflation expectations last quarter, only last week was there any reason to believe there wouldn’t be more to come. Yellen has made some rumblings about one-off impacts on inflation from medical prescription and cell service prices, but those can’t be big enough factors to change the trend.

The trend of lower inflation since the June SEP could force the governors to again mark down expectations for PCE inflation...

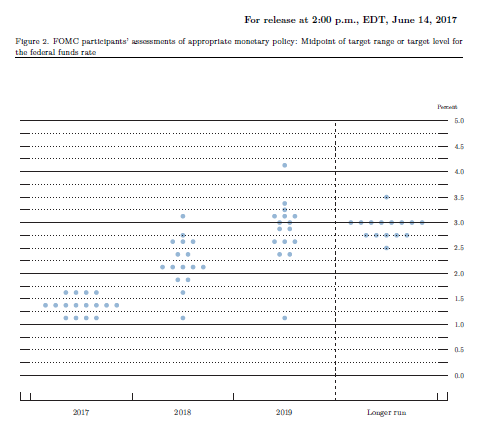

in the famous dot plot...

The risk would be to lower forward rate hike expectations and a flatter curve rather than backing off of the pledge to continue monetary normalization in the short-term.

Having lost the great Stan Fischer, Janet and Dudley are now the dynamic duo, and both have continued their hawkish rhetoric...so they can raise rates, if only! If only wages start to rise and takes inflation with them.

The statement, press conference, and SEP will seek to preserve their optionality while again trying to maintain some credibility in recognition of flatter curves and low inflation.

Going full circle back to USD and rates, that result isn’t going to give much of a push to the dollar--in fact it is more likely to keep the curve flat and allow the equity market to keep on keepin’ on. There just isn’t much evidence to suggest the FOMC will upset the apple cart quite yet.

Shawn

TeamMacroMan2@gmail.com

@EMInflationista

Shawn

TeamMacroMan2@gmail.com

@EMInflationista

14 comments

Click here for commentsSo what is your point?.....Do you think I am going to get tired of running in the opposite direction of your "phase 2 chlamydia trials" in that biotech stock your tipping!

Replyps.....I would rather be left with no profit at all than the risk of making you quid.

Once again I apologize, I thought using bold type was an innovative way of getting to the point quickly for those with short attention spans.

Replyon a related note, how many quid in a dollar?

A fistful.

Reply@amps, you still here? That would be enough to buy you some booze in Burma but not here, in NYC. I bid you adieu.

ReplyKeeping with the theme. The chart congestion in 1.38-1.40 on pound is a sweet place to park a short entry. The way Carney sounded today I'd think we see it along with a new low in the buck. I mean if 800 pips straight up is not enough to scare the shit out of shorts it'll just go tag that area to see what's there. I'll tell you what's there - Brexit vacuum.

Central Bank Balance Sheets

Replyhttp://www.yardeni.com/pub/peacockfedecbassets.pdf

ps...my friend,

ReplyWhen you are drinking,drink

When you are fighting,fight

When you are eating, eat

When you are alone, stand strong

When you become a man, be a man

"Where did it all go wrong Gorgie?"

Thanks for the posts, DR and Shawn.

ReplyRe the Fed, took profits on TUZ7 short. Agree that Yellen and Dudley will move on any opportunity to credibly hike rates, but I doubt last week's CPI gives them reason to firmly guide to a December hike. The details of CPI # weren't great (due to huge jump in shelter) and I don't take a very bullish-through from it to PCE which comes later this month. My guess is they keep a Dec hike in the dots, but keep the question open.

Re the USD, I'm only long against JPY and reduced today ahead of Fed. I see arguments made for why QE tapering will lower or raise 10Y rates (and USDJPY trades as a +ve carry bet on higher US 10Y). My guess is rates go higher ... global supply-demand points that way next year, the 10Y isn't very attractive on a hedged basis to foreign investors here, and you even had the former head of the "plunge protection team" saying he sees 20bps effect this year and 15bps next from QE unwind (for whatever that's worth). I have been wrestling with the question of what happens if Japanese inflation surprises to the upside as some (e.g. UBS) have predicted -- would USDJPY trade higher with the real yield differential or would it start anticipating BoJ tapering and fall? Probably the former as BoJ has communicated an overshoot strategy. There is also the question (as posed by one astute trader to me) of Kuroda being replaced with someone who might do away with YCC -- that would surely appreciate the yen. Versus other currencies, I just can't get excited about USD yet. China has put a break on CNY appreciation here and its economy likely slows, so it's hard for me to be bullish EMFX. On the other hand, ex-China EM has stopped de-leveraging. I'm picky about EM longs, my favorite being ARS since the primary result.

In FX, two EUR-crosses are looking interesting to me: +EURCHF and -EURHUF. In both cases, there's a long list of pros and cons on either side of the argument, so I look to price. EURCHF seems to be breaking higher now -- advantage to the "Swiss portfolio flows will pickup (after years of being below trend) now that the global expansion has broadened and eurozone looks more durable" narrative. EURHUF rallied into today's NBH meeting but the verdict of the market, judging my today's action, is "the NBH is policy-constrained and won't be able to avoid currency strength."

Still a European equity bull.

You'll notice I didn't even bother to address the balance sheet taper question--maybe I'll be proven wrong tomorrow but I think they've telegraphed this thing very well, and the end result will have little impact on the market. Worth remembering they aren't going to be whacking bids in the market--they are simply going to stop re-investing maturities (and even that won't happen very fast). The end result just don't look like a game changer.

ReplyRe: china, I'll believe it when I see it--these trends always run a little longer than we think. And while I remain positive on the Argy story, I think ARS is a bold choice for your one EM long...I am going to drop a piece on that subject tomorrow so keep tuned to this channel! (hint: can you settle bonds locally?)

Fantastic! Looking forward to your piece!

ReplySwitch to weekly charts on oil and gas equities. Let them suckers rip!

Replydun dun DUN....hawkish Fed? Oh boy.

Replyi guess....what am I missing here? were they supposed to scrap the December dot and gamble they don't have to go back on their word? Yellen just said the dots are their "best guess"....if an economist uses the word "guess", you can pretty much mark it at zero.

ReplyI did think the dots would come out flatter in 2019, and maybe 2018--is that what's going on here?

sounds like she is talking this back already. "best guess"..."There is a lot of uncertainty"...these are modal estimates....the most likely outcome, but of course their are downside risks....still not buying into this.

ReplyThank you for sharing good information.

Replyดูซีรี่ย์ฝรั่ง netflix

รีวิวซีรีย์ใหม่