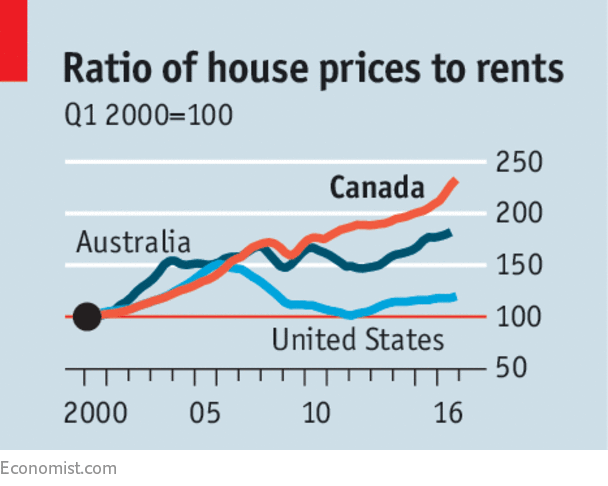

This week’s Economist riff takes us to Canada. Are Canadian housing prices in a bubble? There’s little doubt the answer is yes. The article discusses some of the macro-prudential measures the government and Bank of Canada have taken, and their relative (lack of) effectiveness.

Tough to argue with that chart, when the price/rent ratio is materially outperforming peak prices from 2006 in the US, as well as Australia frothy prices. But is Canada on the precipice?

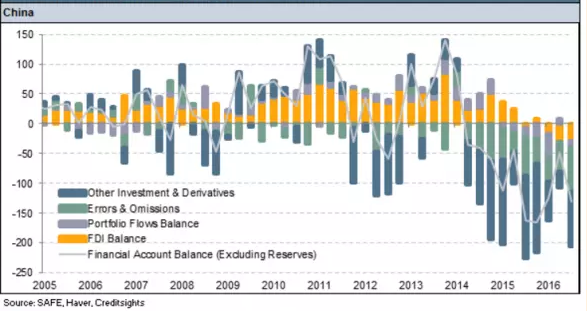

The article correctly points out the source of the bubble is capital flight from Asia, mainly China. This chart shows there has been an avalanche of capital leaving China looking for a safe destination with stable rule of law. Canada certainly fits the mold.

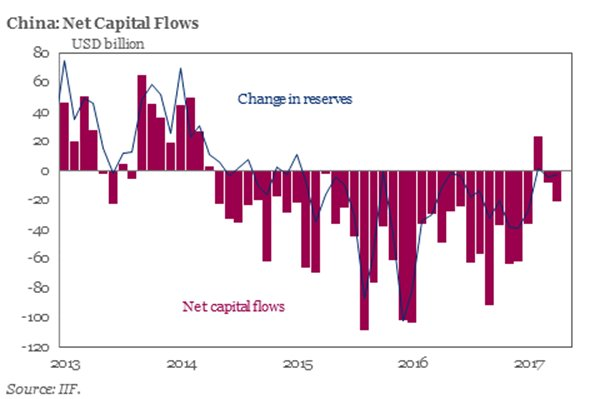

How has the Chinese government and the PBoC reacted to this capital flight? They have tightened capital controls in a variety of ways. This chart would argue they’ve actually been quite effective at it. Reserves have stabilized, and so has CNY. Similarly, front end rates in China have cranked higher as the authorities squeeze shorts. The combination of higher front end rates in China and tightening capital controls may not be completely uncorrelated to the recent slowdown in Vancouver and Toronto housing prices.

The international economics textbook would say this is unsustainable--Chinese authorities will be playing whack-a-mole trying to stop capital from leaving the country, and Canada will continue to be an attractive destination. So with money still seeking to leave China, are we near the end for the Canadian housing market?

I believe the answer is again a resounding “no”, for a few reasons:

- I would agree with the article here that Canadian banks are well regulated and capitalized. The shadow banking/zero down/ARM binge we saw in the US hasn’t gotten there (yet). There may be some bodies buried in the yard, but not system-wide.

- It’s clear that it will be a reversal of the capital flows from China that finally pops the housing bubble, which will likely be because of a hard landing/financial crisis in China, coinciding with a cratering in commodity prices. As I discussed last week, there are clear signs of a Chinese credit boom. But I don’t see the signs that there is a bubble popping there. I recognize front end rates are inverted but I don’t see the spark that is going to ignite the tinder--maybe a dead whale beaches itself onshore tomorrow, but given the firepower and incentives of the Chinese government, I suspect that day is well in front of us.

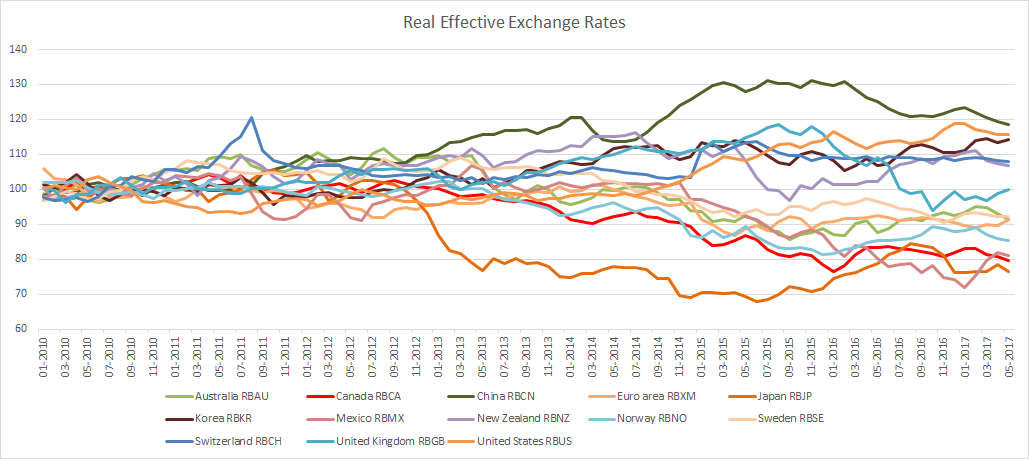

- The catalyst for an end, or a reversal, of the flows has to get back to value. The Chinese will repatriate their capital when and if there are cheap assets to buy domestically. But today there is huge value in exporting capital for your average Chinese citizen. And for these people, Canada still looks cheap. Not only do you gain a significant improvement in the rule of law, but CAD is near historically cheap levels on a REER basis, while CNY is still looks overvalued. Bubble economies tend to have overvalued currencies as the “story” behind capital flows overwhelm reality. The REER in Canada shows that is not the case, in fact, arguably the opposite. And it is worth noting that #2 in this measure is USD, which has been another huge beneficiary of foreign flows over the last several years.

Source: BIS

I’m not going out to buy a condo in Vancouver tomorrow morning. And I can see how foreign demand could make domestic assets expensive enough to price out local consumption and investment and submarine the economy. But I don’t see the evidence that we are there yet.

Shawn

TeamMacroMan2@gmail.com

@EMinflationista

Shawn

TeamMacroMan2@gmail.com

@EMinflationista

24 comments

Click here for comments

ReplyChinese and Indians migrating en masse to the West:

Paying to receive a job offer letter:

"The owner of Vstar, Nicole Sun, told Wu the company charged Chinese nationals $200,000 for the skilled worker application.

"This is the fee charge for the entire immigration application process," Sun explained to Wu. "It's the money you pay for your family to get residency status."

Undercover investigation unmasks cash-for-jobs Chinese immigration scheme

‘Every alarm bell goes off with this one,’ says immigration expert

http://www.cbc.ca/news/canada/saskatchewan/undercover-investigation-unmasks-cash-for-jobs-chinese-immigration-scheme-1.4159137

"Trump son-in-law parlays Chinese cash into luxury apartment tower"

ReplyThe Kushner Companies, headed by Trump’s son-in-law, Jared Kushner, is building Trump Bay Street, a 50-story luxury apartment building in Jersey City. It adjoins the high-rise Trump Plaza Residence.

About a quarter of the tower’s funding — $50 million — comes via the federal EB-5 investor-visa program, which grants U.S. visas to mainly Chinese investors.

http://watchdog.org/258894/trump-chinese-cash/

Imho, Carney is also to be blamed for keeping rates low forever. Kept on saying there is NO inflation. No inflation? How come real estate,gas,food,and other necessities have 'gone through the roof'.

ReplyPossibly, but I'm not sure it would have helped. Maybe the housing market wouldn't be the destination but the country's assets still would be. Higher rates and a stronger CAD would have hurt exporters and the oil business, but I agree, that might have been a small cost to pay to not have asset price inflation isolated in a handful of sectors.

ReplyThanks for the post Shawn

ReplyMust be hard for pensioners and people locked out of real estate. Feel sorry for those who sold after U.S. r/e crash thinking it would happen here too.

Similar issue in New Zealand with the Auckland housing market

ReplyI have removed it a question.

Replygclub

gclub casino online

i live on a small acreage 35 minutes from Vancouver; in the last 3 years, we

Replyhave seen our property value increase from 780k(2015) to under 1.1m(2016)

and now 1.6m (2017)....It's not all chinese money coming in: in the last

4 months, i have had people from Saudi Arabia, England, Pakistan, and

New York, and Toronto looking us over....2 houses north of me sold for 2 million each 6 months ago.....the local assessments boards are as much to blame as

anyone; with an eroding tax base, they can increase assessed values as they want...thank god i'm old enough to defer my taxes.

Interesting levels in oil, it's even giving CAD a little nudge back after its recent move higher. [I'm long 1.4 Sept calls here. Bearish on CAD housing & Oil]

ReplyIf oil breaks lower out of its previous range then it has to impact inflation, yields and potentially HY too. We don't seem to have had much comment on Oil/HY recently, i need to research more, but wonder if that will start to become a factor again.

Some input from Ben Hunt from Epsilon Theory. Given his style the nom de guerre might as well be Leftback...

ReplyWhat has happened (and apologies for the ten dollar words) is that the Fed’s reaction function has flipped 180 degrees since the Trump election. Today the Fed is looking for excuses to tighten monetary policy, not excuses to weaken. So long as the unemployment rate is on the cusp of “instability”, that’s the only thing that really matters to the Fed (for reasons discussed below). Every other data point, including a market sell-off or a flat yield curve or a bad CPI number – data points that used to be front and center in Fed thinking – is now in the backseat.

The Fed is tightening, and they’re not going to stop tightening just because the stock market goes down 5% or 10% or (maybe) even 20%. Bigger game than propping up market prices is afoot, namely consolidating a reputation as a prudent central banker before the inevitable Trump purge occurs, and consolidating that reputation means keeping the evilest of all evil genies – wage inflation – firmly stoppered inside its bottle.

Let’s be clear, not all inflation is created equal. Financial asset price inflation? Woo-hoo! Well done, Mr. or Mrs. Central Banker. That’s what we’re talkin’ about! Price inflation in goods and services? Hmm … a mixed bag, really, particularly when input price inflation can’t be passed through and crimps corporate earnings. But we can change the way we measure all this stuff and create a narrative around the remaining inflation being a sign of robust growth and all that. So no real harm done, Mr. or Mrs. Central Banker.

Wage inflation, though … ahem ... surely you must be joking, Mr. or Mrs. Central Banker. How does that possibly advance economic efficiency and social utility? I mean, even a first year grad student can *prove* with mathematical certainty that wage inflation only sparks a wage-price spiral where *everyone* is worse off. What’s wrong with you, don’t you believe in math? Don’t you believe in science? Hmm, maybe you’re just not as smart as we thought you were. But I’m sure you’ll be very happy as an emeritus professor at a large Midwestern state university. No, Ken Griffin is not interested in taking a meeting.

Whatever you think full employment might be in the modern age, 4.3% is at the finish line. And 4.1% or 3.9% or wherever the unemployment rate is going over the next few months is well past the finish line. You’re already seeing clear signs of labor shortages, particularly skilled labor shortages, in lots of geographies. Wage inflation is baked in, and modern populist politics make it impossible for corporations to play the usual well-we’re-off-to-Mexico-then card. Not that wages in Mexico or China are really that much better anymore, depending on what you’re doing, and there are inflationary wage pressures there, too.

Bottom line: I think that the Fed is going to do whatever it takes to prevent wage inflation from getting away from them, and shrinking the balance sheet is going to be a vital part of that tightening, maybe the most important part.

Doing the same in England:

Reply"Pound Drops as BOE's Carney Says Not Yet Time to Raise Rates"

https://www.bloomberg.com/news/articles/2017-06-20/pound-drops-as-boe-s-carney-says-now-isn-t-time-to-raise-rates

Hmm.. a new low in crude, and a new low in US30y. Regular readers will recall that we predicted this would happen….

ReplyWe have talked repeatedly here about how the oil price impacts US inflation, which then drags the long end of the curve around with it. The answer to the question above is yes, I think we are going to start to hear about high yield credit a bit more now that WTI has broken below $44. Unless and until EVERYONE has gone over to the short side in oil, we can see prices drift lower, to $40 and perhaps lower. That's going to be panic stations for the shale guys and their lenders.

Small caps have been astonishingly resilient but for obvious reasons they usually sell off when HY spreads widen. The transmission mechanism should be fairly obvious. ETFs like HYG are liquid, but the underlying assets are not, and trade in a lumpy manner, introducing some gap-like price action once things go pear-shaped. Another major breakdown in oil prices might therefore be the trigger for an unexpected period of disorderly price action and volatility.

Many commentators now think the Fed is severely boxed in by market dynamics here and is now actively trying to pop this massive bubble in everything. According to this view they will be staying on course until the market breaks down, and may stay on course even if it does break down, confounding many JBTFDers. So the short end rates will drift up, according to this view, and if you look at the 2y auction, that's what seems to be happening.

Sitting in the belly and at the long end, we are fairly happy with this scenario. Tightening here will slow growth during an already slow growth phase, and we are very likely to see additional yield curve flattening and even a very modest inversion before this is done. It's what the textbook says happens when the central bank tightens….

Having stated the above, we are probably going to take a bit off today, it would be easy to be blindsided by IEA/DOE data releases, which could light the fuse for a nasty little squeeze in crude, rates and the dollar.

Be careful out there...

"According to this view they will be staying on course until the market breaks down, and may stay on course even if it does break down, confounding many JBTFDers. So the short end rates will drift up, according to this view, and if you look at the 2y auction, that's what seems to be happening."

ReplyWow LB ... it looks you're hinting at an inversion here? Surely that's the only end point if they keep going. If not the macro/CPI data have to turn soon!

I think it's unlikely that they let curve invert but if they keep up on fighting the data they definitely will. I expect data to continue soft in the US and plan on keeping my long TY & EDZ8 positions but feel risk/reward is much better in Europe now. Ultimately european eco cycle will follow that of the US and I expect it to very soon ( if you look at the citi eco surprise indexes usual lag is 8 weeks). I am playing this through 10y2y flattener in Italy, as it correlates very well with data and it's probably the country where I feel current inflation is the most overstated. Underemployment is huge there (france and spain only ones where issue is larger imo) which makes the output gap much larger than it seems.

ReplyAs for other stuff, still short XRT but paying close attention to redbook same store sales picking up. Everyone is taking retail weakness for granted and a pickup in sales will probably lead to major squeeze. On the negative side, almost stopping out my FCX long. Gave me a brief moment of joy but gave it all back in a glimpse.

On the eqty mkts, short ES here + short a collar. You can sell a 12% otm put and buy 3% otm call zero cost giving you a nice risk/reward on the short. Also bought some upside exposure through selling OTM calls on IWM vs buying OTM calls on SPY. If you look at Sep/Oct you can get > 6:1 leverage. Not something I think is very likely but the payoff is nice and pairs well with the other structure.

Great calls, LB. Also some great posts, Shawn. Thank you for the quality work.

ReplyWas in London last week. Thankfully stopped out of what delta-one exposure I had to oil on the EIA data and took off EURNOK position as it re-priced against its drivers. Still thinking oil can trade higher from here, but price action has me re-examining. I would expect additional OPEC action in July if prices continue falling/stocks continue rising. If not, I'd wonder about their resolve.

Very small/few bets on this moment ...

Interesting perspective on Europe as punters are absolutely loving EU equities at the moment. Thanks for the insight.

ReplySold a pile of US fixed income today, the whole trade feels a little bit over-extended for now. The RSI for TLT is around 70 on modest volume, and usually that level has preceded yields backing up a bit. The flattener may be running out of steam in the short-term here, and the prospect of being slapped upside the head by a change of direction in FX or the crude oil market is ever-present. So we plan to step aside and watch the energy reports and the US economic data for the rest of the week.

Long term thesis still intact here, but tactically we would rather have some cash on hand at the moment.

The house price to rent ratio looks most out of line in Vancouver and Toronto. Less so in other parts of the country. The problem is that in the RE sector we don't have the necessary degree of transparency to really know how much leverage is in the system. And, what % of sales goes to foreign buyers.

ReplyStill one hears anecdotal evidence that banks are lending to much vs incomes and that a small interest rate move would have a disproportionately large impact on leveraged borrowers. One other point mentioning is that the geographic regions/areas with the lowest standards with respect to the enforcement of anti-money laundering are all the ones that stand out with high house prices. And this may well be part of the problem too.

James, you may find Garth Turner's blog interesting, www.greaterfool.ca

ReplyHe likes to go on about the CDN RE market and occasionally some personal finance (he is a financial advisor). His view is similar to what you've stated, the market seems to be stretching every metric that can be used to measure it.

Thanks for the post ,Must be hard for pensioners and people locked out of real estate. Feel sorry for those who sold after U.S. r/e crash thinking it would happen here too.

Replygoldenslot

Thanks to everyone for the discussion here--per some of the comments on local inflation relative to the BoC's "official" inflation, I did some digging around in the data to see where this might be coming from. To make a long story short I don't know what the BoC is smoking. I'll post a follow up later in the week.

ReplySorry to bore you G7 traders out there with a deep dive on Mexico again, but i think it is worth a glace for potentially similar analysis elsewhere.

The media is suddenly awash in stories like this one below. Sentiment swing seems to be complete. These conditions are ripe for a decent squeeze in crude (and presumably energy stocks, which have lagged the market in a major way). We're not playing it yet, but we would not be surprised to see such a move get rolling here.

Replyhttp://www.cnbc.com/2017/06/20/oil-just-entered-a-bear-market-and-bofa-says-its-heading-to-30.html

It's very likely that we will do very little here into the end of Q2, but we might put on a few highly predictable Q3 fund flow trades next week, unless unexpected events interfere with normal market rhythms. It would be rude not to…….

Ditto

Replyyou may find Garth Turner's blog interesting

Replyสล็อต ออนไลน์ ได้ เงิน จริง

goldenslot mobile

ฝาก 100 รับ 100อาณาจักรการพนันออนไลน์ UFAAUTO789 ในโลกการพนันมักมีปัญหากับการโกงลูกค้าหลายรูปแบบ ใครที่เคยเล่นการพนันออนไลน์จะรู้ดี ไซต์บางแห่งปิดตัวลงและหลบหนี จึงไม่สนว่าลูกค้าจะเดือดร้อนหรือไม่ และยังทำให้ระบบการพนันของเว็บไซต์อื่นเสียไปด้วยทำให้ลูกค้าไม่มั่นใจในการพนันออนไลน์ เราขอร่วมเป็นส่วนหนึ่งของผู้ให้บริการเดิมพันครบวงจร เพื่อให้ลูกค้าทุกท่านสามารถวางเดิมพันได้อย่างมั่นใจไร้กังวล หัวใจที่เครดิตจะหายไป เรากำลังรอให้บริการลูกค้าทุกคนเป็นพิเศษ ไม่ว่าลูกค้าจะฝากน้อยหรือฝากมาก เราก็ให้การบริการที่เท่าเทียมกัน คุณมีสิทธิเลือกเดิมพันได้อย่างอิสระ ไม่ว่าจะเป็น แทงบอลลีกชั้นนำทั่วโลก คาสิโน บาคาร่า สล็อต เกมยิงปลา รูเล็ต ไฮโล และอีกมากมายรอให้บริการคุณตลอด 24 ชม. เรามีแบรนด์มากมายเช่น ufabet เว็บตรงทางเข้า ที่จะนำเสนอ คุณรู้สึกตื่นเต้น Click Here

Reply