TMM were recently leafing through old “theme” trades and came upon the electric car one. Tesla released the Model S which seems to be getting good reviews and YTD numbers for hybrid and EV/PHEV sales seem to be very strong indeed, as can be seen below for this year. As such, we thought it was worth reviewing the lot and seeing where things stand.

First – are people buying them? The answer would appear to be a resounding YES. Sales YTD in the US are about 3.25% of all auto sales, up from 2.5% last year. Toyota can’t sell enough Priuses and even some of the less impressive EV models – Nissan Leaf, the much-politicized Volt – are selling roughly 2-3x the numbers they posted last year. Every auto maker seems to be coming out with a lot more models and particularly electric ones this year, so TMM are watching and waiting to see what full year numbers will be.

Second, does it make sense to buy them? This is not an entirely silly question – if 5% of the population is so green they will buy an EV whatever the cost, then demand today might be misleading as to where things are going. After all, the global population does not consist of bourgeoise bohemian bankers. It is on this point that TMM are feeling particularly punchy about where these sales might be going. TMM did some quick numbers on the Tesla Model S versus a 5 series BMW. Similar markets but the Tesla is about $8,000-10,000 more expensive.

In a world with sub 2% yield on the 10 year there are obviously dumber investments out there. TMM extended this table as per below to work out where the sweet spots are in terms of implied Brent prices (gasoline price * 35). As you can see, the luxury sedan segment (larger, pricier, 10-15L/100km) works for a lot of power prices and the head-to-head versus a Prius hybrid of ~5L/100km even stacks up at power prices not different from those across the continental US. Note however, that if you face high power prices and have good mileage as a German driver already driving a clean diesel might, it’s a tough sell.

Sensitizing it to the marginal cost of EV versus standard and it checks out pretty well using a $3.75/gallon petrol price. Basically, if you are paying anything less than 25c per kWh for your electricity this would materially outperform just about anything else you could do with your money, including giving it to hedge funds.

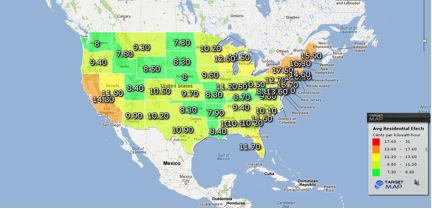

So what are power prices like in the US? Well, really, really low as it happens as you can see here.

To TMM it looks like there aren’t a lot of good reasons why the market share of these vehicles can’t increase a great deal very quickly since they are a fundamentally good investment if you’re the sort of person who drives a lot and is spending $50,000 on a car. That price point may drop soon as Tesla rolls out a 3 series competitor and a luxury SUV. These things may not be the people’s car just yet but that hardly matters – if you can take enough market share of higher end SUVs and sedans that is a big part of the over all market.

To that end, going back to an old chart, TMM think that if Vehicle Miles Travelled (orange) has peaked and average mileage of vehicles (pink) continues to do the hockeystick thing, then implied fuel demand in green has got to start heading south very soon. This is bad news for oil and really bad news for US refiners. Europe has already seen its first refiner bankruptcy last year and faces a similar malaise of falling fuel demand. TMM are not shocked that the likes of Exxon and others are in an awful hurry to sell off downstream and midstream assets.

In addition, it has quite broad implications for just about everything since it is such a major input. Declining oil demand would massively improve the Western and Asian world’s current account deficit and would put the Middle East and Russia back a long way – so far in fact TMM are reminded of a line from Syriana. Similarly, inflation in the West would slow a great deal as energy accounted for roughly 40% of the last decade’s inflation in the US. Look at the chart below. The biggest movers of the last decade were motor fuel and utilities. With the US surplus of gas and half the coal sector at death’s door due to excess supply the case for a utility fuel squeeze in the US is pretty weak in TMM’s opinion.

If Inflationistas sound pretty silly at the moment, they are going to sound really silly if this pans out as TMM expects, since money printing might be the only thing that could possibly get the US above 2.5% inflation.

So in summary, TMM are not in a mad hurry to fade the Ruble short or get particularly enthused about anything Middle East – between the secular decline in demand for a key export and the political risk there isn’t much to love. However we are pretty enthused with Tesla and US utilities. The world may be slowing at the moment but secular stories, especially those with a dividend yield 250bps above the 10 year look pretty good to us.

It should also be noted that this trend is as good for the US as China. The problem is of course that China, the home of the electric bicycle cannot get an electric car together to save themselves. Too bad.

First – are people buying them? The answer would appear to be a resounding YES. Sales YTD in the US are about 3.25% of all auto sales, up from 2.5% last year. Toyota can’t sell enough Priuses and even some of the less impressive EV models – Nissan Leaf, the much-politicized Volt – are selling roughly 2-3x the numbers they posted last year. Every auto maker seems to be coming out with a lot more models and particularly electric ones this year, so TMM are watching and waiting to see what full year numbers will be.

Second, does it make sense to buy them? This is not an entirely silly question – if 5% of the population is so green they will buy an EV whatever the cost, then demand today might be misleading as to where things are going. After all, the global population does not consist of bourgeoise bohemian bankers. It is on this point that TMM are feeling particularly punchy about where these sales might be going. TMM did some quick numbers on the Tesla Model S versus a 5 series BMW. Similar markets but the Tesla is about $8,000-10,000 more expensive.

In a world with sub 2% yield on the 10 year there are obviously dumber investments out there. TMM extended this table as per below to work out where the sweet spots are in terms of implied Brent prices (gasoline price * 35). As you can see, the luxury sedan segment (larger, pricier, 10-15L/100km) works for a lot of power prices and the head-to-head versus a Prius hybrid of ~5L/100km even stacks up at power prices not different from those across the continental US. Note however, that if you face high power prices and have good mileage as a German driver already driving a clean diesel might, it’s a tough sell.

Sensitizing it to the marginal cost of EV versus standard and it checks out pretty well using a $3.75/gallon petrol price. Basically, if you are paying anything less than 25c per kWh for your electricity this would materially outperform just about anything else you could do with your money, including giving it to hedge funds.

So what are power prices like in the US? Well, really, really low as it happens as you can see here.

To TMM it looks like there aren’t a lot of good reasons why the market share of these vehicles can’t increase a great deal very quickly since they are a fundamentally good investment if you’re the sort of person who drives a lot and is spending $50,000 on a car. That price point may drop soon as Tesla rolls out a 3 series competitor and a luxury SUV. These things may not be the people’s car just yet but that hardly matters – if you can take enough market share of higher end SUVs and sedans that is a big part of the over all market.

To that end, going back to an old chart, TMM think that if Vehicle Miles Travelled (orange) has peaked and average mileage of vehicles (pink) continues to do the hockeystick thing, then implied fuel demand in green has got to start heading south very soon. This is bad news for oil and really bad news for US refiners. Europe has already seen its first refiner bankruptcy last year and faces a similar malaise of falling fuel demand. TMM are not shocked that the likes of Exxon and others are in an awful hurry to sell off downstream and midstream assets.

In addition, it has quite broad implications for just about everything since it is such a major input. Declining oil demand would massively improve the Western and Asian world’s current account deficit and would put the Middle East and Russia back a long way – so far in fact TMM are reminded of a line from Syriana. Similarly, inflation in the West would slow a great deal as energy accounted for roughly 40% of the last decade’s inflation in the US. Look at the chart below. The biggest movers of the last decade were motor fuel and utilities. With the US surplus of gas and half the coal sector at death’s door due to excess supply the case for a utility fuel squeeze in the US is pretty weak in TMM’s opinion.

If Inflationistas sound pretty silly at the moment, they are going to sound really silly if this pans out as TMM expects, since money printing might be the only thing that could possibly get the US above 2.5% inflation.

So in summary, TMM are not in a mad hurry to fade the Ruble short or get particularly enthused about anything Middle East – between the secular decline in demand for a key export and the political risk there isn’t much to love. However we are pretty enthused with Tesla and US utilities. The world may be slowing at the moment but secular stories, especially those with a dividend yield 250bps above the 10 year look pretty good to us.

It should also be noted that this trend is as good for the US as China. The problem is of course that China, the home of the electric bicycle cannot get an electric car together to save themselves. Too bad.

4 comments

Click here for commentsWith EV in the US, you're not as much contributing to the environment than cashing in on the extremely wide Oil-Natgas spread via power generation.

ReplyTo Anon: so is this secular for a different reason (fracking kills peak oil)? I suppose so.

ReplyHowever, there are various countries that adapt ICE cars for natural gas, like the former USSR countries, Pakistan, Argentina, even Brazil. So the manufacturers know how to adapt it. Infrastructure issues notwithstanding (gas pipes and refilling stations, similar to EV), the incumbent ICE industry has a last trick that could be very lasting indeed. Can´t go long EV yet. But short downstream. As is the case for much of the last 1/4 century.

A dividend is a portion of profits that a company might decide to pay to its shareholders. Many companies decide to share a percentage of their profits with those who own stock in the company.

Replyex dividend

Re EVs. Not so much IRR on the incremental cost as a breakeven calc I would have thought. Going to take about 5years+ of fuel savings to pay for the upfront cost. So assuming a 3year first owner the value differential is going to need to hold up in the resale.

ReplyThat will depend on servicing costs and battery life/replacement cost.

On servicing I suppose you hope to save quite a lot as no more dohc's, no more turbo's for your diesel, no gearbox, no fancy exhaust system etc.