No doubt you’ve read something about the flattening of the yield curve. You may have even heard it inverted. I can always tell when an arcane financial concepts hit the mainstream by when my relatives ask me about it. I’ve gotten that one a few times lately.

But let's take that question at face value. Let’s put aside curve inversion for a moment. What does a *flattening* yield curve mean for monetary policy and the economy?

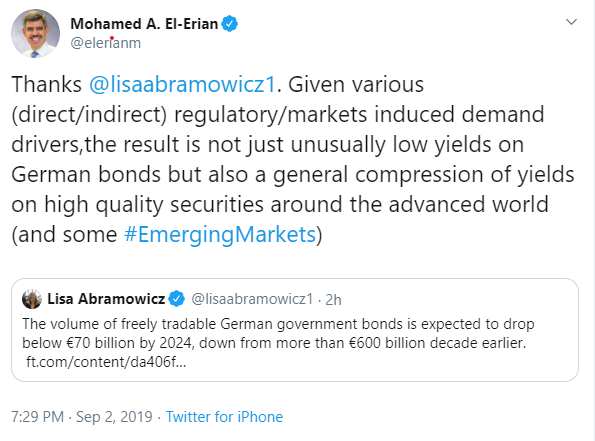

Mohamed got me thinking about that question this afternoon:

The biggest story in financial markets over the past year is not the inversion of the US yield curve, but the bull flattening of the bund curve: here is a chart of Germany 5y/30y slope vs. assets on the ECB balance sheet:

The end of the ECB’s asset purchase program coincided quite closely with a slowdown in global growth that resulted in the bull flattening of the 5y/30y bund curve. What does that mean? Slowing growth--but also little optimism for a pickup in growth or inflation in the future. Combine that with the factors Mohamed mentioned and you have the recipe for a very big bull flattening.

Fast forward to the next ECB meeting. How should monetary policy react? Traditionally, as growth slows monetary policy eases, either through rate cuts, or more recently, asset purchases. You can see that clearly in the chart above in 2015 and heck, right through to 2017.

The flattening in 2014 and again in 2016 both reversed out quite nicely--the first time the result of increased QE from the ECB, and the second time after global growth recovered from the nadir of China growth fears and low oil prices in early 2016.

Where does that leave the ECB today? In a heap of trouble. They need to steepen the curve.

Among the myriad problems in Europe are their banks. The flat curves, low growth, and regulatory constraints have strangled big European banks. Look at this chart of return on equity in European banks vs. US banks:

Sources: Bloomberg, Federal Reserve Bank of St. Louis (FRED)

A flat curve means that banks can’t borrow low (from depositors) and lend high (to borrowers). They have to rely on credit spreads or simply do nothing at all and make money off fees. When banks can’t make money on lending, credit growth suffers. A similar chart of US vs. European credit growth would show a similar dissonance between the US and Europe.

The ECB must find a way to steepen yield curves. How can they do it? Easing monetary policy *must* be a signal for higher growth and inflation, otherwise it is ineffective and most likely counterproductive. If the ECB believes further easing won’t steepen yield curves, they should say so explicitly and tell the government this is their problem now.

That would lead to an easing of fiscal policy--via issuing more long end bonds. That would give Mohamed the supply he so desperately wants for his friends at Allianz.

Now, let's contrast the situation in Europe with what we see in the US:

By way of example, look what happened back in 2007: when the Fed started cutting rates, the 5/30y UST spread started to steepen--as one would expect if monetary stimulus coinciding with the end of the business cycle leads to higher growth in the future (the vertical line coincides with the first cut from the Fed).

Throughout 2008, the curve stayed steep...going over 200bps in mid 2009. The first round of QE

Steepened the curve even more: 5y/30y spread topped out at over 250bps in 2010.

That was very supportive for credit growth--which is one of monetary policy’s core transmission mechanisms.

Now, looking at the situation today: here is the same chart, 5y/30y ust spread and the fed funds rate.

This time, the curve FLATTENED when the Fed started cutting rates.

The market is telling the fed and the ECB that they don’t believe the traditional monetary policy transmission mechanisms work anymore.

Do you believe the market has that right? The market opportunity is clear---bet on further flattening and stagnation if monetary policy is broken--bet on steepening if you think a combination of normal business cycle re-ignition and Fed and ECB easing can sort this out and return growth to trend.

My take: I think the market has gotten way out ahead of itself and is trading on 1) fear and 2) momentum. Real money guys benchmarked to indexes--who happen to be getting eaten alive by passive indexation--caught on to the rally in the front end, but have reacted by buying long end duration and convexity. They are going to stay long until proven otherwise. Nobody wants to be left behind in the great bond rally of 2019.

Now, put on your behavioral finance hat. If you have skin in the game, ask yourself or your colleagues these types of questions:

- What is the probability the US and/or European governments pass fiscal stimulus packages of at least 2%/GDP per annum?

- What is the probability that US and European monetary policy will prove ineffective over the next year--as demonstrated by a 5/30y curves in US and Germany flatter 1 year from now vs. where they are today?

- How much of this is Soros-esque reflexivity, reflecting the “fear of fear itself” and a self-fulfilling prophecy of lower long-term interest rates? If you buy into that--what evidence can you bring to the table?

- Curves have re-steepened in the past--prove to me why this time is different.

These are the type of questions that can get us past rank speculation and productive discussions about what is baked into the markets and how we can exploit that to generate alpha.

skewrisk@gmail.com

@EMinflationista

skewrisk@gmail.com

@EMinflationista

222 comments

Click here for comments «Oldest ‹Older 1 – 200 of 222 Newer› Newest»Hey Shawn,this is where I was last week when asking what's the question. It might give you a boost...

ReplyThe way I see it we have three old fashioned variables that are going to come to a head over the next year:

1) People

2) Central Banks

3) Political

Slice or dice it any way you want, it will come down to the reaction of each variable to the other. Every thing else is peripheral.

Same auld, same auld, but maybe just maybe this time is different.

Been a while since I checked the blog and what timing. Great post mate.

ReplyI myself am in 2 minds, one thinks yeah ripe for a steepener but then maybe we're "in a new paradigm" where once the usual mechanisms could be relied upon but now in an ongoing ZIRP world does this still hold true? Are we, in the words of the Vapors, turning Japanese?

Replyjustabeancounter...

hey , you want start in my Queensland Funds of Funds "Guesser" fund?

My "Guesser" fund will strip fees from your capital that is employed within a another "Guesser" fund.

From which point ...my funds will handed down the lineage to more guessers.

If i learned anything from him...it okay to stay away from guessers...hand it over.

How significant to steepening would be a resolution of the China vs US trade/tariffs situation, i.e., would that represent a stimulus on par with potential fiscal or monetary stimulus?

ReplyBig blow Numbers on Friday? Good news on the trade/tariffs? The Fed backs Trump?, Trump backs the economy? The people back Trump?. Other nations follow suit? That is how you do it.

ReplyEasy!

@gus

Replyyour question triggers some thoughts ...

steepening would represent a stimulus, as normally achieved through sufficient lowering of short rates, which is basically what monetary stimulus is (in the pre-NIRP traditional framework). So sufficiently low short rates and steepening and monetary stimulus used to be synonymous, and now we have already low short rates without steepening, and the question is how much monetary stimulus is achieved just from lowering rates versus steepening curve at whatever rates. Achieving steepening without lowering short rates if necessary could still come from fiscal stimulus (sell enough long bonds) or the maybe fed could engineer steepening by selling long bonds.

But even if it may be possible to achieve steepening as a policy tool (and didn't Ben Bernanke say it is always easy to create inflation if desired), it may be important to consider your question in the context of reverse effects: a steepening may not cause as much as also result from and reflect stronger economic growth and both real and nominal growth expectations. The bond market and yield curve is not just a channel to affect the economy, but is a big signal reflecting the state of the economy.

Reply@gus...

piss off gus....piss off all you nine power brokers! I'm retired hahaha...

Replysomeone bring Kerry back. someone tell him that the murdoch's are getting jack shit...and lachan is bigger a fuck up than ever...

Replyamps has had few tonight. but bear with me lads. i think it's only right that since i've been given enough rope here to hang myself...that i might as well push the envelope. give'em a chance.

hey , sir...lord...whaddya think of Kerry's magic touch?

ya think Kerry would love to be here today and run with amps?

ya reckon?

ya reckon Kerry was spot on to leave a little ol' bookworm a gift.

or do reckon ...being from your club...that Kerry gave away too much to just about anyone?

i know whaddya would've done with those broodmares.

anyway , it's all academic now. you lot never knew...and will never never know...i will make sure it.

Replywhere can amps buy his "rat pack" hollywood hat?

who's in the rat pack in hollywood?

that's right ...the world's most frustrated gangsters.

Replyits sunday morning here...amps has finally found the perfect setup.

lets send amps to america.

why not put amps with miley cyrus?

come one...why not...

amps is a pro at being made a spectacle of to make others money...

while miley is pro at making a spectacle of herself to make money...

it's the perfect american capitalist dream!

called it the american dream team.

yeah la la la land really suits amps...yeah

Replyit's all rigged. from trump tower...to notting hill...from canberra...to hollywood...from wall street...to aspers...from the palace...to south sydney...it all rigged.

the only way you can be truly independent...is to do a gates/jobs/zuckerberg...build your own shit in the garage...and tell people good luck...

To whom it may concern: Europe is well and truly cooked. Draghi just closed the Brexit case. Doubling down on my EURUSD parity.

ReplyAnd....here's a bolder prediction: Germany will leave the Euro within 3 years. If they don't do it under a reasonable centre-right/centre-left govt, a far harder right-wing government will do it in a much messier fashion. Why?

France is the lynchpin and is considerably more ill than most of the world realizes. It's always the quiet ones that kill you. When the bill comes due for France, there isn't enough money in the world to fix it....

France’s recent structural reforms under Macron have lit a fire there to the upside. The EZ has a wonderful combination of lowest unemployment in years, super stimulative monetary policy, a cleaned up banking system (with only a few small exceptions in Italy), and fiscal firepower in aggregate. The weakness in German manufacturing is triggering fiscal and monetary stimulus in the face of a very strong domestic backdrop across Europe. EZ reflation trades are screaming buys here

Reply

Replyits monday morning here...and amps has finished reading the weekend papers.

his find it quite amusing that the players down south are disputing the rights to future pay tv sports channel 12.

his would like to inform y'all that packer & gongstors & ((co)) real estate holdings and cash are nothing but american options on the rights to the channel. that's all they are...american options.

they have been worthless since the day Kerry left us...there just pieces of paper with an option to exercise the use of the channel at any given time shall the channel be free & available for use...that is all.

the holders of these american options have waited opportunistically for their chance to cash in on an option of great utility that was originated way before they knew anything about it.

Kerry left behind a bunch of opportunists...that think they own the option rights that he left behind...

stop your bitching down in sydney and get a life...

Hat Tip:

don't take any advice from victoria...

Replyall your american & european options in cash & real estate are way out of the money and are worthless. their not coming back into the money. the theta has expired years ago.

unless you can bring Kerry back...

give it up guys.

"The market is telling the fed and the ECB that they don’t believe the traditional monetary policy transmission mechanisms work anymore.

ReplyDo you believe the market has that right?"

Something is broken. The two questions I am asking are:

1. Will retail investors buy negative yielding certificates of deposit? Because if they don't bank NIM will fall apart (as you mention)

2.) Barring the weekends events, was the great bond rally of 2019 a sign of general panic, or panic purchasing, or a locking in of rates in anticipation of continued low interest rates (and possibly negative rate environments?

Pretty basic I know but I can't just move on from these questions.

Hi everyone. I will love to share a testimony with you. a few months ago, my man left me for another lady. I love him so much and all I could think of was suicide. I tried several ways, but none worked. I decided to read online and read about spells and spells. I tried it, lost a lot of money, but it was the same result. I almost gave up until I met a spell Caster that convinced me of success and I read people's comments on his website. I was skeptical when I contacted him because I lost a lot of money. With two weeks of casting a spell, my man returned home to me... Now my man is very docile and loves me more. I am now 2 months pregnant and happy to have him back in my life. I would advise you to contact this powerful spell caster, who gave me a second chance to happiness and love, I tried a few spells and none worked. If anyone can help you bring back your love and guide you in your search for life solutions, it is him. Contact him directly at -Email- blackmagicsolutions95@gmail.com ......You can also Whatsapp him on +2349083639501. Be blessed.

ReplyIt's quite unfortunate that retail/BTFDers have managed to alienate the pros in this blog (skr, cbus, nico, LB,IPA, Abee, etc.. )during such exciting times in markets right now.

ReplyThanks guys. Let me guess, just buy the dip because QE infinity?

Yep. Unfortunately the troll was successful in killing the blog

ReplyInvest with 200$ and get a returns of 5,000$ within seven business working days.

ReplyWhy wasting your precious time online looking for a loan? When there is an opportunity for you to invest with 200$ and get a returns of 5,000$ within seven business working days. Contact us now for more information if interested on how you can earn big with just little amount. This is all about investing into Crude Oil and Gas Business.

Email: investmoneyoilgas@gmail.com

CBD oil Japan

ReplyRick Simpson oil Japan

Ricks hemp oil Japan

Medical cannabis Japan

Hemp oil Japan

Where to buy CBD oil

CBD Hemp oil Japan

Rick Cannabinoild oil Japan

Cannabidiol Japan

Rick Cannabinoild Japan

you could create a message board, Ganga bhakti moderate it daily for an hour, and allow the ads to make you money.Ganga music

ReplyBusiness and Personal Loans, Loans ranging from $5,000-$100,000,000.

ReplyWe Offer suitable financial services Globally,Business and Personal Loans, Loans ranging from $5,000-$100,000,000.Our passion is helping ones in need.Feel free to engage our leased facilities as We have provided over $2 Billion in business loans to over 25,000 business owners just like you. We use our own designated risk technology to provide you with the right business loan so you can grow your business. Our services are fast and reliable, loans are approved within 24 hours of successful application. * Personal loans, * Truck Loans * Car Loans * Real Estate Loans * Refinancing Loans * Debt consolidation loans * Education Loans * Farm Loans * Corporate Loans * Business Start-up Loans We offer loans from a minimum range of $5,000 to a maximum of $500 million, Better loan services Will give you loan with an affordable interest rate of 3% and loan duration of 1 to 30 years to pay back the loan (secure and unsecured). Our aim is to provide Excellent Professional Financial Services. Intermediaries/Consultants/Brokers are welcome to bring their clients and are 100% protected. In complete confidence, we will work together for the benefits of all parties involved. Do not keep your financial problems to yourself in order for you not to be debt master or financial stress up, which is why you must contact us quickly for a solution to your financial problems. It will be a great joy to us when you are financially stable Email us via: betterloancompany@gmail.com.Better loan firm We are certified and offer fast and reliable services.(betterloancompany@gmail.com)

I'm very glad to find this website on block.

Replyข่าวบอลไทย

อ่านข่าวกีฬา

This 123.hp.com/laserjet brand of printers come up with fast and two-sided printing options along with business-class features. This LaserJet Pro m404n model printer is compatible with Apple products and the AirPrint option

ReplyNow that we’ve come to the end of the HP Laserjet Pro m404n Printer setup process, if you have any further queries, navigate to our web page.

Hello everyone..Welcome to my free masterclass strategy where i teach experience and inexperience traders the secret behind a successful trade.And how to be profitable in trading I will also teach you how to make a profit of $12,000 USD weekly and how to get back all your lost funds feel free to email me on( brucedavid004@gmail.com ) or whataspp number is +22999290178

ReplyHello everyone..Welcome to my free masterclass strategy where i teach experience and inexperience traders the secret behind a successful trade.And how to be profitable in trading I will also teach you how to make a profit of $12,000 USD weekly and how to get back all your lost funds feel free to email me on( brucedavid004@gmail.com ) or whataspp number is +22999290178

nice post Thx UFABET คาสิโนยอดนิยม

ReplyI was carried away when I read

Replyhttp://www.giocodazzardo.org/

http://www.sitiodejuego.com/

http://www.daftarmerekdunia.web.id/

http://www.daftarpresidendunia.web.id/

http://www.sejarahdunia.web.id/

That cover is Amazing

Replyhttp://www.daftarpeninggalandunia.web.id/

http://www.optimuseuludum.com/

http://www.sakkagyanburusaito.com/

http://www.shinraidekiru.com/

http://www.oszukujehazard.com/

Thank you for hosting

Replyhttp://www.onrainpoka.com/

http://www.onrainsakka.com/

https://www.futtoborushiti.com/

https://www.debestegoksite.com/

http://www.bestevoetbalgokken.com/

NICE for giving a chance to share ideas

Replyhttp://www.stronaoszusta.com/

http://www.stronazgrami.com/

http://www.umegliuagente.com/

https://www.watashitachiha.net/

https://www.dracobetfraudator.com/

Such an amazing and helpful post this is

Replyhttp://www.ecogaudit.com/

http://www.aleaballsreliable.com/

http://www.optimemitterentpiscis.com/

http://www.optimusonline.net/

http://www.kumpulan-marveldunia.web.id/

ReplyWe have other cat breeds ready for adoption, Welcome to British Shorthair kittens cattery, home of Registered British shorthair kittens for sale. As Registered and well recognized British shorthair kittens breeder, we have been raising British Shorthair kittens since 2015.As British shorthair kittens breeder,we have extensive experience in breeding and grooming British Shorthair Kittens . We provide an opportunity to become an owner of our highly valued British shorthair kittes for sale which have been well trained and have all qualities of a good British Shorthair such as calmed personalities of British shorthair kittens and good tempers ,hypoallergenic kittens for sale.We equally provide shipping services to ensure your British Shorthair kitten arrives your location with no hassles. So feel at home adopt a British shorthair kitten online or adopt a British shorthair kitten near me with ease.

Welcome to our farm where we breed Registered pomeranian puppies for sale.As a registered pomeranian puppies breeder, we have made it possible for pomeranian puppy lovers to

buy pomeranian puppies online,buy zwergpitz pomeranian from our family run farm. Pomeranian dogs are small dogs with a weight of 1.36 to 3.17 kg and a withers height of 15 to 18 cm. They are compact but robust dogs with a lush, textured coat and a tall and flat tail. The top coat forms a fur ruff on the neck, for which poms are known, and on the hindquarters they have a margin of feathered hair.You can click HERE to view our available pomeranian puppies

Hello, and welcome to our website for the best hand raised

hand raised macaw parrots for sale. We pride ourselves in the best taming practices of macaws among aviaries. All of ourmacaws for sale are bred in a disease-free Biosecure breeding sanctuary. They are well socialized, having been raised in our home as members of our own family in order for them to become ready to be a member of yours, we have green wing macaw,severe macaw for sale,scarlet macaw for sale,blue and yellow macaw for sale among others. They are quite comfortable around all ages, including the elderly and young children. When you purchase a bird from Us, we are committed to offering lifetime support and guidance to you and your family.You can read more and view our available birds.You can

READ MORE and view our avilable bird

ReplyWELCOME TO pug puppies BREEDERS HOME BUY A PUG ONLINE|PUG PUPPIES FOR SALE|ADOPT A PUG ONLINE|PUG|BLACK PUG PUPPIES FOR SALE

We are so glad you stopped by to check out our amazing TEACUP Pug puppies. All of our animals come fully up to date on vaccinations, heart-worm tested negative, and de-wormed, as well as neutered, and treated for any ailments found upon veterinary examination Adopt a teacup Pug puppy

Ownership of a Pug includes a commitment that is wider in scope than providing doggy necessities and allowing this jovial little pet to occupy a portion of your home. Pug ownership is a give-and-take relationship that will continue throughout the little dog’s life. That enjoyable companionship thrives when each member of the pair respects the other and camaraderie rules the union. Your Pug will entertain you, love you, and be obedient and faithful to you if you spend time with your doggy friend.

Adopt a pug puppies online puppy onlie or pug puppies for sale online does not all depends on the money involve. You have to love

Black pug puppies for sale at heart before you go in search of pug puppies for sale or adopt a pug puppy.This means that you have to keep the pug puppy price or cost of a pug puppy or a teacup puppy in mind before you harnest the interest of buying a pug online.

WELCOME TO buy Persian kittens online/CAT FOR ADOPTION CATTERY.

First question to ask here should be,What is the price for a PERSIAN KITTEN BREEDERS,Persian kitten price/cost,Can i adopt a Persian kitten online?Persian kitten Breeders.Are persian kittens playful? As the name implies, this website is devoted to our love for animals. We are the home of CFA/TICA Registered Persian Kittens and The Cat Groomer.Persians kitten Cattery has been registered with the Cat Fancier’s Association since 1994, breeding and showing purebred, pedigreed Persian Cats and Kittens, We offer companion kittens in the colors of brilliant WHITE PERSIAN KITTENS FOR SALE (White click here to adopt a Persian kittens for sale for Sale with Blue Eyes, White Persian Kittens for Sale with Odd Eyes and White Persian Kittens for Sale with Copper Eyes). Persian kittens also breeds adorable SILVER PERSIAN KITTENS FOR SALE and GOLDEN PERSIAN KITTENS FOR SALE with vivid green eye color and eye liner. Persian kittens are socialized at a young age, hand fed and kept in a clean and cozy environment. You are assured of a healthy companion when they leave; veterinarian examined, vaccinated, wormed and come with a 2 year genetic guarantee. The time devoted into each Persian kitten makes a world of difference in your little one’s personality and it’s health. A small variety of Persians known as TEACUPS are available as companions. Teacup sized Persians are a separate breeding program from my show cats and come in a variety of colors. Adopt a Persian kitten online are not conducive to children, they are difficult to breed and raise and therefore expensive. All companion kittens are sold to be neutered and spayed. I request that the application on this website be submitted if you are interested in being a prospective parent. We offer a secure form of payment and financing through various means,So adopt a kitten online today

the art of cannabis is tetrahydrocannabinol, one of the 483 known compounds in the plant, including at least 65 other cannabinoids

Replybuy real weed online

how to buy weed online

buy legal weed online

buy recreational weed online

buy weed edibles online

can i buy weed online

buy medical weed online

buy weed online canada

buying weed online reviews

buy weed online legit

buy weed online without medical card

buy weed seeds online canada

order marijuana online

order marijuana seeds online

how to order marijuana online

order marijuana online without a medical card

can you order medical marijuana online

order marijuana online

Marijuana—also called weed, herb, pot, grass, bud, ganja, Mary Jane, and a vast number of other slang terms—is a greenish-gray mixture of the dried flowers of Cannabis sativa.

ReplyThe main active chemical in marijuana is THC (delta-9-tetrahydrocannabinol), the psychoactive ingredient. The highest concentrations of THC are found in the dried flowers, or buds. When marijuana smoke is inhaled, THC rapidly passes from the lungs into the bloodstream and is carried to the brain and other organs throughout the body. THC from the marijuana acts on specific receptors in the brain, called cannabinoid receptors, starting off a chain of cellular reactions that finally lead to the euphoria, or "high" that users experience. Feeling of a relaxed state, euphoria, and an enhanced sensory perception may occur. With higher THC levels in those who are not used to the effects, some people may feel anxious, paranoid, or have a panic attack.

Cannabis plant used for medical or recreational purposes. The main psychoactive part of cannabis is tetrahydrocannabinol, one of the 483 known compounds in the plant, including at least 65 other cannabinoids.

buy real weed online

how to buy weed online

buy legal weed online

buy recreational weed online

buy weed edibles online

can i buy weed online

buy medical weed online

buy weed online canada

buying weed online reviews

buy weed online legit

buy weed online without medical card

buy weed seeds online canada

order marijuana online

order marijuana seeds online

how to order marijuana online

order marijuana online without a medical card

can you order medical marijuana online

order marijuana online

Marijuana—also called weed, herb, pot, grass, bud, ganja, Mary Jane, and a vast number of other slang terms—is a greenish-gray mixture of the dried flowers of Cannabis sativa.

ReplyThe main active chemical in marijuana is THC (delta-9-tetrahydrocannabinol), the psychoactive ingredient. The highest concentrations of THC are found in the dried flowers, or buds. When marijuana smoke is inhaled, THC rapidly passes from the lungs into the bloodstream and is carried to the brain and other organs throughout the body. THC from the marijuana acts on specific receptors in the brain, called cannabinoid receptors, starting off a chain of cellular reactions that finally lead to the euphoria, or "high" that users experience. Feeling of a relaxed state, euphoria, and an enhanced sensory perception may occur. With higher THC levels in those who are not used to the effects, some people may feel anxious, paranoid, or have a panic attack.

Cannabis plant used for medical or recreational purposes. The main psychoactive part of cannabis is tetrahydrocannabinol, one of the 483 known compounds in the plant, including at least 65 other cannabinoids.

buy real weed online

how to buy weed online

buy legal weed online

buy recreational weed online

buy weed edibles online

can i buy weed online

buy medical weed online

buy weed online canada

buying weed online reviews

buy weed online legit

buy weed online without medical card

buy weed seeds online canada

order marijuana online

order marijuana seeds online

how to order marijuana online

order marijuana online without a medical card

can you order medical marijuana online

order marijuana online

dank vapes are the best brand of vape cartridges in the market. These dank vapes cartridges have however suffered a backlash in the recent weeks with multiple reports on how these dank vapes carts cause cancer and other related lung disease.

Replydank vapes cart however remain one of the best cartridges. dank vapes are sold in multiple states over the USA. dank vapes cart compost one of the black markets finest vape products. But this backlash has caused a fall in the consumption of the vape by adults.The Kingpen brand is also on the rise in market demands as well as skywalker OG products.

Recently juul pods also faced a similar backlash. juul starter kits have also fallen in market demand. mango juul pods are refillable juul pods and can be gotten as juul pods bulk. juul skins and juul accessories all

come with the juul kits.

buy juul online at cheap prices buy cocaine online

buy Keytruda online and other cancer medications such as buy avastin online , buy Herceptin online

jungle boys , buy weed online , marijuana, buy weed online , buy lsd online , dankwoods , parexa pods

buy adderall online

Replybuy oxycodone online

buy percocet online

buy methadone online

buy hydrocodone online

buy oxycontin online

buy phentermine online

buy adipex online

Quality content!

ReplyWelcome to MEGA CANNABIS ONLINE DISPENSARY Buy Magic Mushrooms online,Buy cannabis oil online, Buy vape cartridges, buy edibles, buy magic mushrooms online and have them DISCRETELY SHIPPED

to you (US/UK/EUROPE). We are the best online store selling legal cannabis (CBD) oil for pain, exotic kush strains and RSO for cancer,vape oil,(CBD) infused coconut oil and much more. We’ve also got CBD Pet treats, which can be administered to your pets like cannabis (CBD) oil for dogs and cats. With a vast gallery of cannabis oil and its related products, we offer you the best for your needs.This is Where to Buy Cannabis (CBD) Oil , exotic kush strains, Kush seeds, concentrates and magic mushrooms Online. MORE INFO.

Buy MEDICAL and RECREATIONAL Cannabis online

Magic Mushrooms for sale

Buy Medicated Dog and Cat Treats online

Buy Magic mushroom grow kit online

Brass knuckle carts for sale

Buy Vap Pen online

Mail Order CBD infused edibles

Buy THC live Diamonds online

Tincture oil for sale

Buy RSO online

Buy Dragon Tears online

ReplyGreat article!!!

Are you looking for WHERE TO BUY MARIJUANA ONLINE DISCREETLY in the US, UK or in EUROPE? We offer high quality Cannabis strains and seeds at afforable prices. The marijuana strains we sell are carefully selected by leading breeders. We carefully pack and send all marijuana weeds and seeds orders discrete and stealthy.MORE INFO

Mail Order Marijuana US

Buy RSO oil online

Buy shatter wax online

Buy Heavy Hitters carts online

Buy Authentic vape carts online

Buy Cereal milk Kush Online

Buy weding cake kush online

Buy Kush seeds online

Buy Marijuana Edibles online

Buy exotic weed strains online

Buy Live resin online

buy exortic carts online

Replybuy exortic carts online

Buy gorilla glue #4 online

Buy granddaddy purple feminized seeds

Buy blue dream Weedstrain

Buy white widow weedstrain

buy exortic carts online

Buy blueberry kush online

Buy lemon haze online

Buy pineapple express online

Buy purple haze feminized seeds

Buy alaskan thunderfuck

buy exortic carts online

Buy lemon kush

buy exortic carts online

buy exortic carts online

Buy jack herb online

Buy Exortic carts Online

Buy sour disel online

Buy white widow online

buy exortic carts online

buy exortic carts online

Buy white widow

Buy Obama kush online

Buy spacial kush online

Buy bubble kush online

buy exortic carts online

Buy blue dream online

buy exortic carts online

Buy blueberry kush online

Great article! explicit information. I'll be checking from time to time for updates.

ReplyWhere to buy MAGIC MUSHROOMS online for depression. 100% Recommended.

buy weed online

Replybuy kush online

buy real weed online

buy synthetic weed online

how to buy weed online

order marijuana online

buy cbd oil online

order cbd oil online

real marijuana online

different types of weed

weed for sale online

buy edibles online

buying weed online reviews

order marijuana online

real marijuana online

buy marijuana online

cannabis oil for sale

order wax and shatter

marijuana for sale

buy edibles online ship anywhere

cbd oil for sale

marijuana edibles for sale

buy legal buds online

buy medical marijuana online

buy medical weed online

where to buy marijuana online

buy wax and shatter

order cannabis cbd

wax and shatter for sale

buy real weed online

mail order marijuana

buy medical marijuana

buy weed edibles online

buy cannabis online

can you buy weed online

buying weed online

order edibles online

order marijuana online without a medical card

how to order marijuana online

can you buy marijuana online

Our List of vaporizers such as the dry herb vaporizers,Pax 3, firefly 2 and Davinci iq are being flaunted in the market alongside vape pens.Thc vape pens and cbd vape pens are one of the best vape pens you can think of if you want to buy a vape pen online or searching for vape pens for sale.With the new trend of vape pens in the market, people who buy vaporizers online from vape stores or smoke shops are now confused if the vape store or smoke shops are the ideal places for both portable vaporizers or deskstop vaporizers for sale.The concept of vaping and asking questions like what is a vape can now be answered here on our online vape store alongside other vape questions regarding the type and best vaporizers to buy online.Vaporizers like the pen vaporizers,the crafty and many more.Top selling vaporizers and vapes are the Pax,Herb-E Vaporizer,Firely 2 vs pax 3,Storz & Bickel,Smok vape pen 22,Pen Vape | Juul Vape Pen | Cartridge Vape Pen | Dry Herb Vape Pen |Juul pods near me. thc carts and thc cartridges

ReplyWe are India's largest Logistics marketplace. We serve the entire gamut of Logistics from Storage space to distribution along with 3PL, Built to Suit, WMS, Consultancy, Equipment rental services. We handhold you for a hassle-free experience & optimized solution.

Reply3PL Service

3PL Logistics

warehouse in delhi

warehouse in mumbai

This is such valuable information! Thanks for sharing!

ReplyGTPL Hathway Limited

Adani Power Ltd

HSBC Holdings PLC

HDFC Life Ltd

Jungle boys is an award winning Marijuana brand from Los Angeles. The Jungle boys farm is an authorized and licenced kush grower and distributor.

ReplyJungle boys also comprise of a jungle boys clothing brand with fabrics such as hoodies, caps, t shirts and sucks.

The Jungle boys kush strains are wwide spread across both sativa, hybrid and indica species. Jungle boys indica fire brands are usually recommended to patients with medical conditions such as insomnia.

Jungle boys strains such as the Sin mints, Zack pie ,Jungle mints, Jungle boys,

Jungle apples , Jungle boys frosted cake , Jungle boys hippy crasher and Motor breath are best sellers of the brand.

buy Jungle boys online at wholesale prices from the Jungle boys farm

We sell the best Vaping products such Dankvapes , stiiizy pods , Muha meds cartridges , e-cigarettes , Blu , supreme carts , smart carts , packwoods , cereal Carts , exotic carts , kingpen , dankwood , Brass knuckles , Rove carts ,all this at

Replydank vapes

buy dank carts

exotic carts official

dank vapes carts

sativa strains

organic smart cart

dank vapes official account

smart carts weed

heavy hitters vape

kinpen

smart cart vape

dank vape

heavy hitters cartridges

king pen

smart carts

buy stiiizy pods cartridges

smart carts

supreme carts

buy dankwoods

buy stiiizy cartridges battery

rove carts

brass knuckles vape

710 king pen

kingpen cartridges

cereal carts

We sell the best Vaping products such Dankvapes , stiiizy pods , Muha meds cartridges , e-cigarettes , Blu , supreme carts , smart carts , packwoods , cereal Carts , exotic carts , kingpen , dankwood , Brass knuckles , Rove carts ,all this at

Replydank vapes

buy dank carts

exotic carts official

dank vapes carts

sativa strains

organic smart cart

dank vapes official account

smart carts weed

heavy hitters vape

kinpen

smart cart vape

dank vape

heavy hitters cartridges

king pen

smart carts

buy stiiizy pods cartridges

smart carts

supreme carts

buy dankwoods

buy stiiizy cartridges battery

rove carts

brass knuckles vape

710 king pen

kingpen cartridges

cereal carts

thanks for sharing this article was helpful want to thank you. Good job! You guys do a great blog, and have some great contents. Keep up the good work.

Replybuy puppy online

shih tzu puppies for sale

shih tzu puppies for adoption

shih tzu puppies for sale near me

cheap shih tzu puppies for sale

Thank you very much for sharing about curve flattening and monetary policy 29, it’s difficult for me to get such kind of information most of the time always… I really hope I can work on your tips and it works for me too, I am happy to come across your article. See great dane mix puppies for sale

ReplyEcstatic Psychedelic is an international psychedelic shop which operates world wide. Our main branch is based in USA where we carry out most of our operations.

ReplyDelivery is done within the USA, CANADA and EUROPE with no hassles. Visit our shop now and get best deals.

buy dmt online

buy mdma online

dmt trip

what is dmt

mushrooms

Ayahuasca

how to buy lsd online

buy Penis envy

where to buy Penis envy shrooms

penis envy mushrooms

golden teacher mushrooms

magic mushrooms

buy liberty cap mushrooms

liquid lsd

buy liquid lsd

dmt drug

what is lsd

buy albino penis envy

what is penis envy

ecstacy

penis envy mushrooms

molly

kratom powder

mescaline

ayahuasca tea

shrooms

where to buy kratom

vial of lsd

penis envy

buy lsd online

buy lsd blotter paper

buy dmt

liquid lsd 25 buy

sheet of acid for sale

lsd vial

where can I buy dmt

buy acid online blotter

how much is a bottle of lsd

where can i buy lsd

buy psychedelics

where can you buy dmt

acid sheets price

can you buy 5-meo-dmt online

Being Go Limpo’s founder, I would like you to know the story why I thought to came into this line of business n how does I personally feel why most of us do not focus on our one of the basic needs Water tank cleaning services and why is it essential to get it done for every one, every single person of our community and what factors helped me deciding the lower pricing.

ReplyBeing Go Limpo’s founder, I would like you to know the story why I thought to came into this line of business n how does I personally feel why most of us do not focus on our one of the basic needs Water tank cleaning services and why is it essential to get it done for every one, every single person of our community and what factors helped me deciding the lower pricing

Replyhttps://golimpo.com/water-tank-cleaning-in-delhi-n-ncr/

Your current article normally have got much of really up to date info. Where do you come up with this? Just stating you are very imaginative. Thanks again

Replyshisha near me

vape shop uk

vape store near me

best e liquid uk

Thanks for the great analysis and graphs. I like your thesis: "bet on further flattening and stagnation if monetary policy is broken--bet on steepening if you think a combination of normal business cycle re-ignition and Fed and ECB easing can sort this out and return growth to trend."

ReplyGreat Dane Puppies For Sale

Replyhttps://greatdanepuppieshome.com/

Blue Great Dane Puppies For Sale

Great Dane Puppies For Sale Near me

ReplyDo you even vape bro? Pre-filled marijuana vape cartridges are easy to use, easy to dose, portable and convenient way to consume marijuana which is preferred by many marijuana patients today. For our patients seeking a discreet way to medicate, THC Vapes Carts And Pods is fortunate to present THC oil filled and pre-filled cartridges. Ranging in strain type and THC levels, you’ll find several brand options for patients below. We work with local companies to ensure that we can present the best price and best quality CBD oil vapes cartridges online for our patients. https://thcvapescartsandpods.com/

buy thc vape carts online

buy vape cartridges online

vape shop online

buy vaporizer online

thc vape cartridges for sale

order thc vape carts online

buy buy stiiizy carts online

buy best thc vape carts online

buy smok vapes cartridges online

buy cannabis oil online

cannabis oil for sale

best vaporizer for sale

thc vape cartridges

heavy hitter for sale

buy vape accessories online

order brass knuckles online

buy brass knuckles vapes carts

order marijuana vaporizer online

Arizer Solo 2

thc-kush-syrup

buy kingpens online online

buy 710 kingpens online

sour-diesel-cannabis-oil

buy ABX vape carts online

buy juul pods online

buy juul pods near me

juul pods classic tobacco online

juul pods for sale

buy juul pods flavors online

juul pods mint flavor

order juul pods online

buy juul pods mango flavor

kfcconsole

Replyativan-2gm

Replyamber-oil

xanax-2mg

mdma-100mg-pills

phentermine-2

phentermine

percocet

dimethyltryptamine-dmt

magic-mushrooms

valium-10mg

adderall-amphetamine

lsd-lysergic-acid-diethylamide

alpha-pvp-crystal

codeine-linctus-syrupcare-plus

phenergan-elixir-5mg-5ml-promethazine-sugar-free-oral-solution-100ml

buy cough syrup

buy codeine linctus

buy care plus

phenergan-elixir

phenergan-elixir

phenergan

buy phenergan-elixir

buy lean

lean for sale

buy lean online

lean

buy moonrock carts online

Replybuy juul accessories online

buy juul compatibles online

buy pre - filled vape cartridges online

prefiiled vape cartridges for sale

juul skin

buy juul skin online

buy disposable online

buy juul disposable online

buy pre rolls online

pre rolls for sale

order pre rolls online

buy CBD oil online

cbd oil for sale

order cbd oil online

Buy THC Oil Pre-filled Cartridges

CBD Vape Oil Cartridges for sale

THC Vape Shop Near me

buy dr zodiak moonrock clear carts flavors online

dr zodiak moonrock clear carts

ReplyWelcome to wockhardtstore.com where you can buy codeine which helps for pain relief and treats, coughing, diarrhea. you can also get wocklean purple,Tek lean, Act syrup, woklean, PMG syrup which are Natural syrup and mainly use for relaxation and it is legal in all the 50 states of U.S.A. Get pain medication from our store, painkiller and pain relievers online.

what is codeine

codeine cough syrup

promethazine hydrochloride

condeine for sale

buy codeine

buy codeine online

buy promethazine with codeine

codeine phosphate

wocklean purple

wocklean for sale

buy wocklean

order wocklean online

buy wocklean syrup

buy wocklean purple syrup

buy natural purple syrup

drup free syrup

order wocklean red syrup

buy wocklean green

buy wocklean for relaxation

relaxation syrup

buy painkiller

pain killer medication

painkillers online

buy painkiller online

painkiller for sale

painkiller side effects

buy drugs without prescription

pain medication

order painkiller online

buy pain pills

pain relievers

pain relief pills

methadone

viagra

wockhardt-levothyroxine

guaiatussin-ac-codeine-phosphate

ativan-2gm

buy moonrock carts online

Replybuy juul accessories online

buy juul compatibles online

buy pre - filled vape cartridges online

prefiiled vape cartridges for sale

juul skin

buy juul skin online

buy disposable online

buy juul disposable online

buy pre rolls online

pre rolls for sale

order pre rolls online

buy CBD oil online

cbd oil for sale

order cbd oil online

Buy THC Oil Pre-filled Cartridges

CBD Vape Oil Cartridges for sale

THC Vape Shop Near me

buy dr zodiak moonrock clear carts flavors online

dr zodiak moonrock clear carts

A technical solutions architect is somebody who helps companies design and delivers a range of solutions to their problems. technical solution architect

Replyhttp://ufa345gold.com/

Reply7m

My spouse and I absolutely love your blog and find most of your post's to

Replybe precisely what I'm looking for. Does one offer guest writers to write content for you?

I wouldn't mind creating a post or elaborating on a few of the subjects you write related

to here. Again, awesome site!

how to buy weed online

where to buy weed online

how to buy weed online

where to buy weed online

how to buy weed online

where to buy weed online

how to buy weed online

where to buy weed online

how to buy weed online

where to buy weed online

how can I buy weed online

where to buy vape carts online

how to buy weed online

where to buy weed online

how can I buy weed online

where to buy vape carts online

how to buy weed online

where to buy weed online

how can I buy weed online

where to buy vape carts online

how to buy weed online

where to buy weed online

how can I buy weed online

where to buy vape carts online

how to buy weed online

where to buy weed online

how can I buy weed online

where to buy vape carts online

how to buy weed online

where to buy weed online

how can I buy weed online

where to buy vape carts online

Great Dane Puppies For Sale

ReplyGreat Dane Puppies For Sale

blue great dane puppies for sale near me

harlequin great dane puppies for sale

black great dane puppies

Mantle Great Dane puppies for sale

Fantastic blog i have never ever read this type of amazing information. NCR Ranger Coat

Reply

ReplyTHC Vape Cart Store is a Fast, Friendly, Discrete, Reliable online carts dispensary which ships top grade cartridges around the world. Buy juul pods online has been distinguished by the superior quality of our products and by our overall focus on wellness.

covid-19 prevention

thc vape carts store

dank vapes shop near me

bulk vape carts overnight discrete delivery

exotic carts shop

mario carts online shop

buy dankwoods online uk

where and how to buy real vape carts online

dankvapes for sale

officail dank vape website

real brass knuckles online for sale

juul pods for sale

full gram cartridges for sale

Cheap king pens for sale online

where to buy legit juul pods online

what are juul pods

This is the best post I have ever seen. Very clear and simple. Mid-portion Is quite interesting though. Keep doing this. I will visit your site again.

ReplyHarley Davidson Marlboro Man Jacket

สล็อต

Replyสล็อต

สล็อต

สล็อตออนไลน์

สล็อตออนไลน์

สล็อตออนไลน์

I promise Dr Iboe that I will share this testimony all over the world once my Wife return back to me Thing don't just work out until you make the right choice in your life, In my life i made the right choice when i contacted Dr.IBOE the great spell caster who is specialized in restoring broken relationship or marriages. My name is Taxman from India, and i am here on this page to thank DR.IBOE for a job well done, Because i never believe that i would have gotten my Wife back if not for the sake of Dr.IBOE that is why i won't be leaving this page without dropping the contact details of Dr.IBOE which are via email: driboespell@gmail.com you can also call him or Whatsapp directly on +2347037344123 contact Dr.IBOE in order to restore your broken marriage or relationship.

ReplyVape carts 4 all specialize in the very finest, pharmaceutical-grade, Organic & Vegan Cannabis and cartridges. We deliver it straight to your home across the globe. Source your medicinal cannabis products with peace of mind, from our all vegan, strictly organic and pesticide-free menu.

Replywest coast extract vape carts

krt carts solvent free web site

krt carts sovent free

buy krt vape cartridges online

krt vapes

krt vape cartridges

krt dab carts

curepen

buy curepen online

cali gold extract

buy cali gold extract

Cali gold carts

Cali gold extract cartridge 24k

brass knuckles jack herer

tahoe og brass knuckles

Psychedelics are a hallucinogenic class of drug whose primary action is to trigger psychedelic experiences via serotonin receptor agonism, causing specific psychological, visual and auditory changes, and altered state of consciousness.

Major psychedelic drugs include mescaline, LSD, psilocybin, and DMT.

buy ayahuasca

mdma crystal

what is mdma

buy mdma online

buy psychedelics online

ayahuasca tea for sale

buy acid tabs

penis envy mushrooms

buy golden teacher mushroom

buy psilocybin mushrooms online

where to buy dmt

Hello, you have shared magnificent information, Basically I have gained some new useful knowledge on your site.i also found this important piece of information while doing some research online

Replybaby capuchin monkeys for adoption near me

capuchin monkeys for sale near me

capuchin monkeys for sale

capuchin monkeys for adoption

adorable baby capuchin monkey for sale

buy capuchin monkeys online

capuchin monkeys for sale cheap

cheap capuchin monkeys for sale

capuchin monkey for sale near me cheap

monkeys for adoption near me

adopt a capuchin monkey for free

adopt a capuchin monkey for sale in Ohio

How to Resolve my HP Officejet Pro 6968 Printing Black Pages?

ReplyAre you stuck in the middle while printing on your HP Officejet 6968? Is your printer printing back pages abnormally? This guide explains how-to instantly fix all of those issues in a jiffy. You can adjust the print preferences under “Printer settings” by enabling the “Print on Both Sides Manually” option. Still no luck in fixing the printer? Do not worry. Our tech-savvies are here to resolve all of your concerns. Contact our Customer Support Team right away to speak with a technical professional to troubleshoot HP Officejet Pro 6968 and fix all your printer problems in the blink of an eye.

wow people should look(DoFollow Backlink)

ReplyNice Article. Thanks for sharing this beautiful information.

ReplyGreat Dane Puppies For Sale

Great Dane Puppies For Sale

blue great dane puppies for sale near me

harlequin great dane puppies for sale

black great dane puppies

Mantle Great Dane puppies for sale

great dane puppies for sale near me

How to get my HP Officejet pro 6968 back online?

Reply At first, you have to navigate to the Settings icon and click Devices and Printers.

After that, choose the HP Officejet pro 6968 printer.

Now, right click the printer and check whether the printer is active or not.

Next, you need to choose the Set as the Default printer option.

And make sure to save the changes.

Finally, try to print and documents from HP Officejet pro 6968 printer and verify whether the printer is online.

Contact our professional expert squad to know more details regarding HP Officejet 6968 printer and solutions to troubleshoot hp officejet pro 6968.

british shorthair kittens for sale,

Replybritish shorthair kittens for sale near me,

british shorthair kittens for sale price, british shorthair kittens for sale in florida,

british shorthair cinnamon kittens for sale,

british shorthair kittens for sale texas,

british shorthair kittens for sale california,

british shorthair kittens for sale ohio, white british shorthair kittens for sale,

british shorthair kittens for sale in pa,

blue british shorthair kittens for sale, british shorthair kittens for sale illinois,

cinnamon british shorthair kittens for sale,

british shorthair kittens for sale ny, british shorthair kittens for sale in michigan,

british blue shorthair kittens for sale,

british shorthair kittens for sale los angeles,

british shorthair chinchilla kittens for sale,

british shorthair kittens for sale in usa, british shorthair kittens for sale oregon,

british shorthair kittens for sale nyc,

silver tabby british shorthair kittens for sale,

lilac british shorthair kittens for sale,

british shorthair kittens for sale georgia,

chocolate british shorthair kittens for sale,

british shorthair silver tabby kittens for sale,

golden british shorthair kittens for sale, british shorthair kittens for sale in pakistan,

british shorthair kittens for sale massachusetts, british shorthair scottish fold kittens for sale,http://www.kittenbreeders.company.com

Hello, you have shared magnificent information, Basically I have gained some new useful knowledge on your site.i also

Replyfound this important piece of information while doing some research online

Great Dane Puppies For Sale

Great Dane Puppies For Sale

blue great dane puppies for sale near me

harlequin great dane puppies for sale

black great dane puppies

Mantle Great Dane puppies for sale

great dane puppies for sale near me

Usually I never comment on blogs but your article is so convincing that I never stop myself to say something about it. You’re doing a great job Man,Keep it up.

ReplySuch short little lives our pets have to spend with us, and they spend most of it waiting for us to come home each day. It is amazing how much love and laughter they bring into our lives and even how much closer we become with each other because of them.

(buy puppy online )

buy puppy online

cavapoo puppies for sale

cavapoo puppies for adoption

cavapoo puppies for sale near me

cheap cavapoo puppies for sale

cheap cavapoo puppies for sale near me

shih tzu puppies for adoption

cavapoo puppies for sale near me

Stream Comet TV on Roku

ReplyIts time to activate Comet TV on Roku and start watching the top and entertaining programs. It’s the category, Sci & Tech where you can find the channel. After adding the channel, find the activation code and you can provide the code visiting the channel activation page. Start watching the entertaining Comet TV channel programs such as The Outer Limits, Men into Space, Wild World and lot more

To get help and support to complete Comet TV activation, to know how to watch Comet TV on Roku, check out the latest article and Blog post on our portal.

I like Your Blog

Replybuy documents online

buy fake licence online

buy fake Canadian currencies

buy Canadian dollars online

BUY CANADIAN FAKE DOLLARS

buy fake Canadian dollars

counterfeit Canadian bills

buy fake Euros online

buy fake Euros note

get fake Euros notes sale

buy fake Euros online

Counterfeit Euros for sale

fake Australian dollar for sale online

Benefit of using Undetectable Australian Dollar

Undetectable Australian Dollar for sale online

buy fake Australian Dollars online

fake bank currency

Counterfeit Kuwaiti Dinar Banknote for Sale Online

ReplyI enjoy your story

buy fake licence online

buy fake Canadian currencies

buy Canadian dollars online

BUY CANADIAN FAKE DOLLARS

buy fake Canadian dollars

counterfeit Canadian bills

buy fake Euros online

buy fake Euros note

get fake Euros notes sale

buy fake Euros online

Counterfeit Euros for sale

fake Australian dollar for sale online

Benefit of using Undetectable Australian Dollar

Undetectable Australian Dollar for sale online

buy fake Australian Dollars online

fake bank currency

Counterfeit Kuwaiti Dinar Banknote for Sale Online

banknote for sale online

buy banknotes online

buy fake banknotes online

banknotes for sale

UNITED ARAB EMIRATES DIRHAM ONLINE

counterfeit money online

Buy UAE Dirham online

Buy Counterfeit Pound Sterling

buy fake GBP Bills

undetectable fake money

order fake banknotes online

buy fake banknotes online

fake banknotes for sale

Magic Mushrooms Dispensary is a premiere shopping destination that offers you the chance to buy all types of shrooms from the cost confines of your home.

Replymagic mushrooms dispensary

shrooms for sale

buy legal psychedelics

psychedelic is mushroom

chitwan mushrooms for sale

buying magic mushrooms

buy salvia xetract 40x divinorum

ibogaine for sale online

mushrooms online dispensary near me

mushrooms

types of magic mushrooms

where to buy magic mushrooms

Buy Ayahuasca powder ayahuasca also knows

Replyas the tea, the vine, la purga is a brew made from the leaves

of the Psychotria Viridis.

Purchase Ayahuasca Tea

It is known that ayahuasca is a spiritual and religious drink

by ancient Amazonian and it was not easy to buy ayahuasca tea

or vine online overnight. We are 100% loyal and legit to our

customers moreover we got affordable prices and guarantee fast

delivery to all destinations worldwide

Buy Ayahuasca Online.https://trippysche.com

where to buy ayahuasca

how to get ayahuasca

what is in ayahuasca

where can i buy ayahuasca

what does ayahuasca do

how long does ayahuasca last

where to get ayahuasca

Purchase Ayahuasca Tea

how to make ayahuasca

what is dmt

how to make dmt

how to smoke dmt

how to get dmt

where to get dmt

dmt is the brain

where to buy magic mushrooms

where do magic mushrooms grow

how to find magic mushrooms

where to get

magic mushrooms

how to make magic mushrooms

how to grow magic mushrooms at home

what do magic mushrooms look like

what are magic mushrooms

how to identify magic mushrooms

how tobrew ayahuasca

where to get lsd

where to buy lsd

where to buy lsd

how to store lsd

how is lsd made

how to identify liberty caps

where to find

libertycaps

where do liberty caps grow

liberty caps mushrooms

liberty caps identification

how is lsd

made

We are cannabis bud dispensary which offer top quality grade marijuana for sale, cannabis for sale, weed for sale with track & trace shipments,Weed Shop USA,Weed shop UK, Weed shop EUROPE

Replybuy marijuana online,

buy cannabis online,

marijuana mail order,

420 mail order,

buy hash online, hash for sale,

buy weed online USA,

can i order weed, can i order marijuana,

Gelato strain for sale,

Moon rock strain for sale,

CBD oil for sale

Bud for sale

Website ::http://medicalmarijuanabudshop.com/

Email : info@medicalmarijuanabudshop.com

Text:+1(518) 212-7793

BITCOIN, BINARY OPTION: l am one of the Victims. At first, the software seemed to be really professional and authentic. I found many favourable reviews about its performance and delivered results. So, I decided to invest in it and try to achieve success in the online trading sphere. Soon, I realized that the software was swallowing all my investments. Brokers are nothing more than a dangerous and fraudulent platform. I invested over $ 140,000 and couldn't withdraw my money, months passed and still nothing. So, I reached out to Wizard Charles to help me recover my funds, I have been able to recover $ 100,000 and the remaining $ 40,000 is in progress. I really can't tell how happy I am. Contact him via mail.totalinvestmentplatform@gmail.com

ReplyWhatsApp: +1 (646) 4810376

Visit Website: https://www.facebook.com/101745678391674 ;

Welcome everyone to the world of online gambling. 928bet Easy to bet Give the best price With free credits Here only one deposit - withdraw, convenient, fast, safe

ReplyBuy Nembutal Online Nembutal Buy Nembutal For Sale Where Can I Buy Nembutal Buy Liquid Nembutal Buy Nembutal Pentobarbital Buy Nembutal Sodium Online Buy Nembutal Pills Online Nembutal For Sale Online Nembutal For Sale In USA Buy Pentobarbital Sodium Online Pentobarbital For Sale Sodium Pentobarbital Buy Online Pentobarbital For Sale UK Sodium Pentobarbital For Sale

ReplyNice article.keep up with the good work.I will like to introduce you to my blog.

ReplyThis beautiful Congo African Grey is currently available!

This sweetie pie loves to snuggle and is super friendly. fruits and vegetables must

be thoroughly washed to remove any harmful chemicals before being fed to the bird.

We also feed our african crey witha variety of Uccello seeds, pellets and nuts.

Feeding pet birds the right foods is important for their health fruits and vegetables

must be thoroughly washed to remove any harmful chemicals before being fed to the bird.

Feeding pet birds the right foods is important for their health.

Our website is

https://parrotdize.com

email: info@parrotdize.com

Phone: +123-456-1010

ReplySuperior post, keep up with this exceptional work.

It's nice to know that this topic is being also covered on this web site so cheers for taking the time to discuss this! Thanks again and again!

Yorkie Puppies for sale

Teacup yorkie for sale

Its so refreshing to see a post that talks straight to the point. thanks so much for writing about this it has really helped.

ReplyWeed for sale

buy weed online

Superior post, keep up with this exceptional work. It's nice to know that this topic is being also covered on this web site so cheers for taking the time to discuss this! Thanks again and again! Yorkie Puppies for sale near me

Replysphynx kitten for sale $500

We are an online and retail dealer and distribution center based in USA. We specialize in providing quality firearms and accessories to registered buyers

Replyberetta px4 storm for sale

sig sauer p938 for sale

glock 30 for sale

beretta for sale

Welcomes at Mumbai Escorts Babes to romance with Female Russian and Indian Escorts in Mumbai. I will give you Full services both incalls and outcall only five-star and four-star hotels in Delhi. If you are interested please contact me for more information visit our website.

ReplyIndependent Aerocity Escorts - Aerocity Call Girl and Female Model Escort Services in Aerocity for your spicy erotic desires. Aerocity Escorts is the best Escorts Girls service in Aerocity free and paid sex incall and outcall independent agency.

ReplyIndependent Mahipalpur Escorts girl, I will give you Full services both incalls and outcall only five-star and four-star hotels in Mahipalpur. If you are interested please contact me for more information visit our website.

ReplyEscorts In Mahipalpur

http://macro-man.blogspot.com/2019/09/curve-flattening-and-monetary-policy_29.html

Replyhttps://bhrepublicadominicana.blogspot.com/2016/10/worldunlock-codes-calculator-latest.html

https://www.keywordresearchinc.com/find/dmt-space-cart

https://kcorinspirations.blogspot.com/2018/04/clone-samsung-galaxy-e5-more-ergonomic.html

https://fromaflagshipphone.blogspot.com/2014/12/symphony-d24-mt6261-official-firmware.html

While the whole plant produces THC and cannabinoids, cannabis typically smoke the flowers to get high. Different names for different consumable from of marijuana have sprouted from various regions and age groups on top of that there are scores of slang words that have evolved over the years. Below you can learn about all of the different strains we've come across to date.

Replycanna cavi moon rocks

ice moonrock

moonrock pre rolled joints

animal gas for sale

gelato #33

buy super lemon haze cannabis oil

bichon frise dog

dankwoods pre roll

dankwoods for sell

pre rolls for sale

teacup poodle puppies for sale near me

sour gushers

raw garden live resin

shrooms for sale

mushroom for sale

stiiizy gelato

choice carts

krt carts

oneup

bicons puppies near me

jungle boys

trufflez

zushi

frosted flakes

ice cream cake

pineapple express

white widow

meth kopen

ReplyKøb Crystal Methamphetamine

crystal Meth kaufen

amfetamine kopen

køb amfetamin

amfetamine kopen

You must know about the premium luxury services in your area when you are going to get in touch with the Delhi Call Girls. These girls are highly demanded by the clients because they know about the importance of these services.

ReplyI am one of the sexiest Lajpat Nagar escorts. I am a bold and hot girl with good experience in this field. Through this, you can book me for the whole night or even for a few days. You can get intimate with me and get the satisfaction you want.

ReplyI am one of the sexiest Lajpat Nagar escorts. I am a bold and hot girl with good experience in this field. Through this, you can book me for the whole night or even for a few days. You can get intimate with me and get the satisfaction you want.

ReplyWHO ARE WE?

ReplyWe are an online maltese puppies sales site. All maltese pups recorded on our site are altogether reproduced and brought up in the United States. The selling procedure is totally dealt with by us Making sure that pups are thoroughbred and match all depiction as recorded on our site.to know more about us visit

maltese puppies for sale

maltese puppies for sale craigslist

maltese puppies for sale in florida

maltese puppies for sale in ohio

maltese puppies for sale in Texas

maltese puppies for sale in Near me

teacup maltese puppies for sale

teacup maltese puppies for sale near me

teacup maltese puppies for sale

teacup maltese puppies for sale under 500 near me

<a

Find the best Dating girls and housewife with Jalandhar Escorts she was complete all your requirement physical and mentally desi bhabhi also available for your entertainment purpose way west time book now more visit the website,

ReplyHello. I am a naughty girl, one of the best-looking girls in all Manali escorts. I am in high demand among tourists and businessmen visiting Manali as I know how to make my customers happy and completely happy. I am a very attractive and beautiful Manali escorts girl in this field because I want to enjoy free sex and earn some easy money. If you fancy falling in love with big boobs hot bhabhi, then hire my services and fulfill your fantasies.

ReplyI believe animals should be treated more like humans because they are much more like humans, respectful, honest, and playerful. if you like to know more about us. please visit our website.

Replymaltese puppies for sale

maltese puppies for sale craigslist

maltese puppies for sale in florida

maltese puppies for sale in ohio

maltese puppies for sale in Texas

maltese puppies for sale in Near me

teacup maltese puppies for sale

teacup maltese puppies for sale near me

maltese for sale

teacup maltese puppies for sale under 500 near me

<a

Hello, you have shared magnificent information, Basically I have gained some new useful knowledge on your site. You guys do a great blog and have some great contents,I’ve found something that helped me.

Replymaltese puppies for sale

maltese puppies for sale craigslist

maltese puppies for sale in florida

maltese puppies for sale in ohio

maltese puppies for sale in Texas

maltese puppies for sale in Near me

teacup maltese puppies for sale

teacup maltese puppies for sale near me

maltese for sale

teacup maltese puppies for sale under 500 near me

<a

Your attitude is your battery. Just in case you need to charge your battery right at the lucky spot, contact the escort association to aim for a way that will ensure you a hot and extravagant relationship because of sex. These are the big things for booking Manali escorts which you absolutely cannot miss just click on the link of Manali call girls

Replypenis envy

Reply<a hr

ดูซีรี่ย์เกาหลี

Replyseriesfin.com

penis envy

Replyalbino a

amazonian cubensis

b cubensis

blue meanie

malabar cubensis

pf classic magic mushroom

transkei cubensis

vietam cubensis

z strain

burma cubensis

fiji cubensis

golden teacher

buy liquid lsd online

buy mdma crystals online

buy dmt online

buy 4 aco dmt online

Psychedelic Dispensary online store is one of the best in the supply of rare and high-grade (Mushrooms, Edibles. Psychedelics, and more)with absolute purity. All our products are tested to guarantee potency after production, during distribution and even storage. We ship globally in discreet and undetectable packaging using our network of trusted partners. Every one of the items is firmly fixed and anchored to shield the item from any sort of altering over the span of delivery. Our prices are friendly and heavily discounted for repeat and bulk buyers and we have a no questions asked money-back guarantee / full refunds.

We pride ourselves on providing 100% legitimate and high-grade products. Our focus on quality standards & scientific integrity and commitment to delivery excellence has earned us the reputation of being the leading Psychedelics, Mushroom, and Edibles vendor in the online market. We work hand in hand with independent testing laboratories to confirm the purities of the products listed on our website

เทคนิค แทงบอล

Replyไฮโล hilo

สูตรรูเล็ตฟรี

เกมสล็อตออนไลน์

Replyคาสิโนออนไลน์ คือ

แทงบอล คาสิโน

We provide the best loan at low interest rate without any extra burden that comes along with high rate debt. Do you need a quick loan for business or to pay bills at 3% interest rate? We offer business loan, personal loan, home loan, auto loan, student loan, debt consolidation loan e.t.c. no matter your credit score. We are guaranteed in giving out financial services to our numerous clients all over the world. contact us now on email: financialserviceoffer876@gmail.com

ReplyWhats-app us on +918929509036

Thanks for such a nice content. Apppreciate it :)

ReplyCheers

If anyone interested similar one's have a look here thanks

Glock 17 for sale cheap online without License overnight delivery (glockgunstore.com)

shih tzu puppies for sale near me

listateacuppuppies for sale online

führerschein kaufen

shih tzu puppies for sale near me

listateacuppuppies for sale near me

führerschein kaufen

how to buy weed online

have also something to share here.

Nice article with good information , thanks for sharing this with us.

Replytraining for devops

Good jobs, thanks for this articles. This is really a nice and informative, some points are very interesting in your article. its very helpful for me.

Replyif anyone wants packing and moving services so contact Om international packers in Gurgaon Its very informative article sir, and very easy to understand.

Excellent read, Positive site, where did u come up with the information on this posting? I have read a few of the articles on your website now, and I really like your style. Thanks a million and please keep up the effective work,If anyone interested similar one's have a look here thanks

Replylistateacuppuppies for sale online

shih tzu puppies for sale near me

fuhrerschein-kaufen-schweiz

Awesome post.

ReplyBuy nembutal with bitcoins

Buy red liquid mercury with paypal

Buy red mercury with bitcoins

Replyextraordinary data...

Buy red liquid mercury with paypal

Buy pv8 online with bitcoins

our blog is educational and effortlessly your rule is very good.Thank you

ReplyAlpha-PV8 for sale online

Buy pv8 online

ดูหนังออนไลน์ หนังซีรีย์เกาหลี Netflix ดูหนังฟรี บอลสด หนังชนโรง หนังคมชัดระดับ HD ดูหนังใหม่2021 หนังใหม่ชนโรง

ReplyChiappa Rhino for sale

ReplyChiappa Rhino

Chiappa Rhino 30ds

Chiappa Rhino 40ds

Chiappa Rhino 50ds

Chiappa Rhino 60ds for sale

british longhair kittens for sale

สล็อต wallet

Reply*I really like your writing style, good information, thank you for posting.*

*my web page; ..........*

สล็อตwalletRule number 1 of life. Do what makes you happy.

ReplyAddสล็อตเว็บตรง

Reply.Wallet slots, of course, many online gamblers. Must be familiar

with the best online gambling games. that can make money These

online gamblers are definitely the highest. Number one online slot game

that many online gamblers find a way in order to

play online slots But there was a problem because no bank account

Buy Ksalol 1mg

Replyis used to treat anxiety and panic disorders. It works by enhancing the effects of a certain natural chemical in the body.

Hi There,

ReplyThank you for sharing the knowledgeable blog with us I hope that you will post many more blog with us:-

Buy AYAHUASCA POWDER FOR SALEAyahuasca Powder For Sale is indigenous to the Amazon basin, where it was prepared as a drink by shamans.

Email: info@thespiritualtrip.com

Click here for more information:- more info

The Shih Tzu, also known as the ‘Chinese Lion Dog’, ‘Chrysanthemum Dog’ (because its face resembles a flower),

Replyshih tzu puppies for sale near me

shihtzupuppies-home-blogspot have somrthing to show here

Click to exchange information. 10 คำศัพท์ สล็อตออนไลน์

ReplyCountry of Origin: The Shih Tzu, also known as the ‘Chinese Lion Dog’, ‘Chrysanthemum Dog’ (because its face resembles a flower),

Replyshihtzupuppies-home-blogspot have somrthing to show here

shih tzu puppies for sale near me

Excellent! I love to post a comment that "The content of your post is awesome" Great work. Thanks for Sharing This Article.

ReplyIt is very so much valuable content. I hope these Commenting lists will help my website.fnx™-45

Buy Clonazepam 2mg tablets Online belongs to a group of medicines called benzodiazepines. It's used to control seizures or fits due to epilepsy, involuntary muscle spasms, panic disorder and sometimes restless legs syndrome.

Reply

ReplyOur site Shroom2gostore is pleased to welcome you. Organic Magic Shrooms has the best and most comprehensive variety of Magic

Mushrooms, Microdoses, Mushrooms, Psilocybe Cubensis, Psilocybin, and Edibles on the market.shroom chocolate bars alice in wonderland

Great post. 25 06 ammo bulkVery satisfactory and the very helpful blog commenting sites listing which you have published. I really like it very much. please hold on to doing this great work. Thanks for sharing with us.

ReplyCountry of Origin: The Shih Tzu, also known as the ‘Chinese Lion Dog’, ‘Chrysanthemum Dog’ (because its face resembles a flower),

Replyshih tzu puppies for sale near me

shihtzupuppies-home-blogspot have somrthing to show here

shihtzu puppies

I am unable to read articles online very often, but I’m glad I did today. This is very well written and your points are well-expressed. Please, don’t ever stop writing.สล็อต แตกง่าย