This is why I try not to look at markets more than once a day. Just as I opine in the comments section, ringing the metaphorical “all clear” siren that there’s nothing but air between here from 17.5 to 13 in the VIX….it pops back up to 21.

….and equities roll over, sort of...spoos aren’t playing dead. At least not yet. Prior misgivings about the long-term health of the market notwithstanding, it is tough for me to see how this isn’t anything less than a beach ball held underwater.

Gamma driven mineshaft drops notwithstanding, we’ll just go ahead and call this a 50% retracement. Will equity indices drive higher? The burden of proof is on the bear camp again. Looks like a grind higher towards the 2800 level, maybe there valuation anxiety rises again and we get some chop.

I don’t like calling copper the world’s economic barameter, but I do think it strips out some of the noise in other asset classes. Earlier this month it fell roughly 5% from the low 3.20s to mid 3.00s. The beach ball has resurfaced….resume normal service. China.

The one market with a decent reversal today is USD:

I think EUR got a little over its skis above 1.25--but not expecting a change in trend here. I continue to prefer EMFX and EM local rates.

Now, while there isn't much to throw sand in the gears for risk assets in the short-term, I've been clarifying why I think the glory days for US equity returns are behind us.

I also mentioned in the comments that yesterday I sat in on a speech by Jim Paulsen, the ex-Wells Capital strategist that made a name for himself as the Minneapolis answer to Warren Buffett, regularly appearing on CNBC with folksy witticisms about the market.

I found his outlook pretty insightful--I’ve summarized his views below, along with some graphs I hijacked from his deck, interspersed with my own commentary.

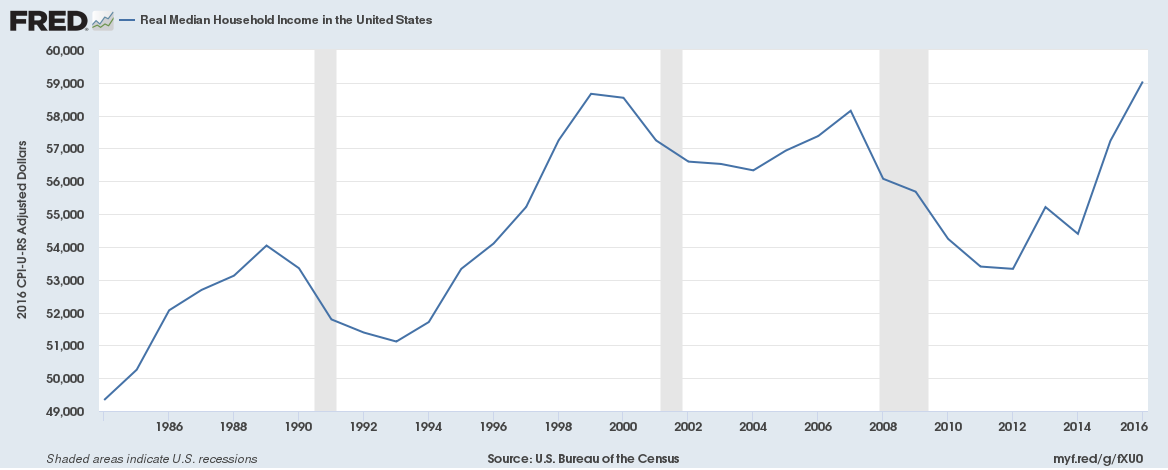

First and foremost was the broadening of the economic recovery. I’d argue this really started back in 2015, when oil prices crashed but employment stayed strong-- and suddenly regular Americans had more money in their pockets. The data hasn’t been updated for 2017 but it is solidly higher with the trend intact.

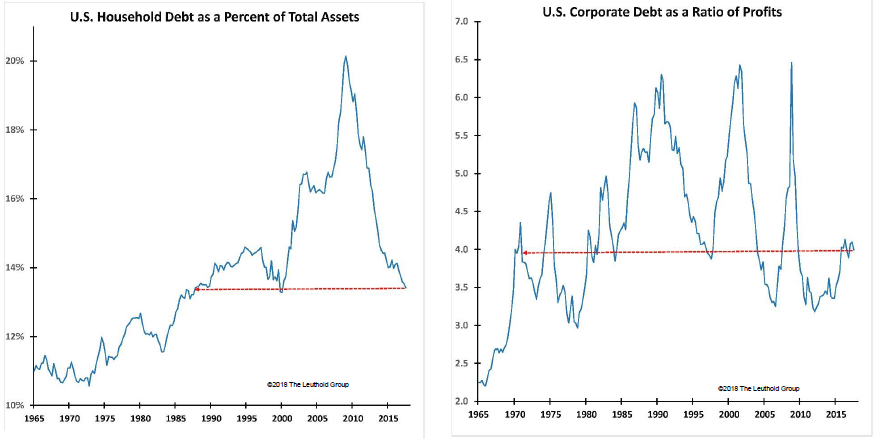

Yet, contrary to all history, and the very fabric of this country--the US consumer hasn’t levered up! There is plenty of runway for increases in areas like retail sales or home prices given the broad household balance sheet strength. Similarly, despite fears about massive issuance by US the corporate sector amid low rates and equity buybacks, Corporate debt relative to profits is far from overstretched levels.

Put another way...every dollar of the issuance avalanche (more or less) has been backed by an increase in profits. Is that a risk factor when profits eventually fall in a recession? Sure, but there’s little sign we’re there yet.

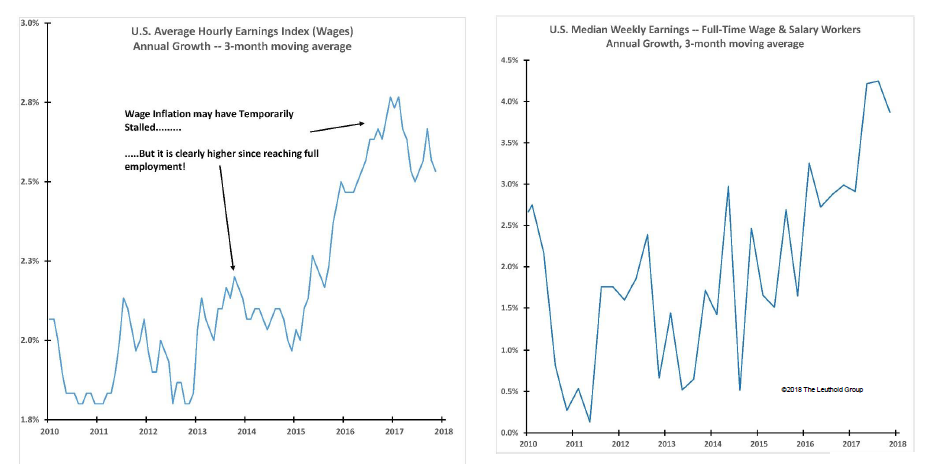

Earnings are also picking up. This is far from breaking news, but what I find fascinating is the trend. There’s little doubt we’re now at full employment--one can make a strong argument that wages have found a new, higher trend level.

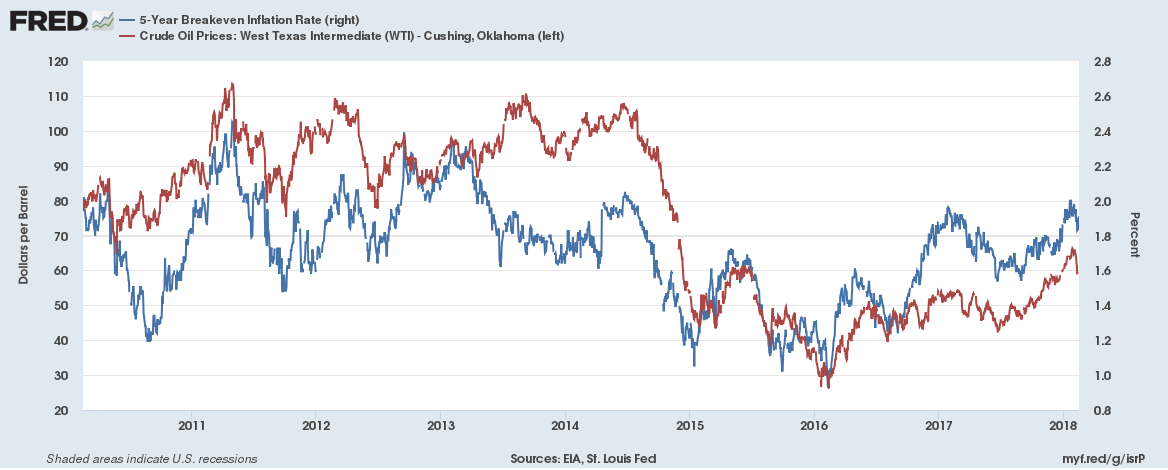

Which leads me to again look at US inflation breakevens. 5y breaks have risen to around 2%.... Yeah, I get it, it’s an oil trade. But it isn’t always. Looking farther back in history--not even ancient history--shows the 5y breaks/oil correlation doesn’t have to move in lockstep. If US producers indeed gun production amid higher prices in the next few months, breaks can move back towards the 1.80s but given the heavy volume in oil forward contracts that has come from US producers selling forward production, I think that’s not a big risk--or at least a two-sided one along with the potential for higher global demand to continue driving commodity prices higher.

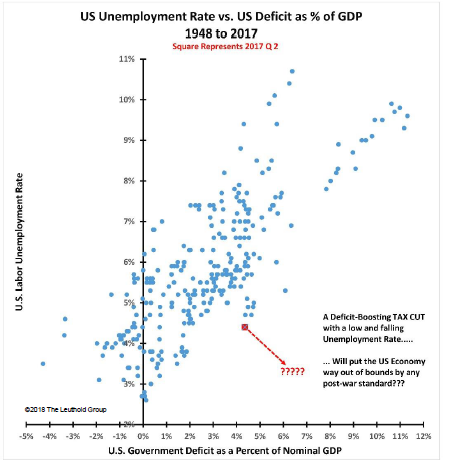

Given the supply side of the economy at full capacity and the government throwing fiscal fuel on the fire...a lot of fiscal fuel...i think 5y breaks can move towards 2.30%. Remember this would still be well inside of the new trend of 2.5-2.8% for wage increases.

Here’s a reminder of what the US government is doing. Spending a ton of borrowed money is the only way to ring in a new era of bipartisanship.

.

.

Indeed, on current evidence rates have to go higher--or at the very least, nominal rates need to continue to cheapen, even if the fed sticks to the low r* script.

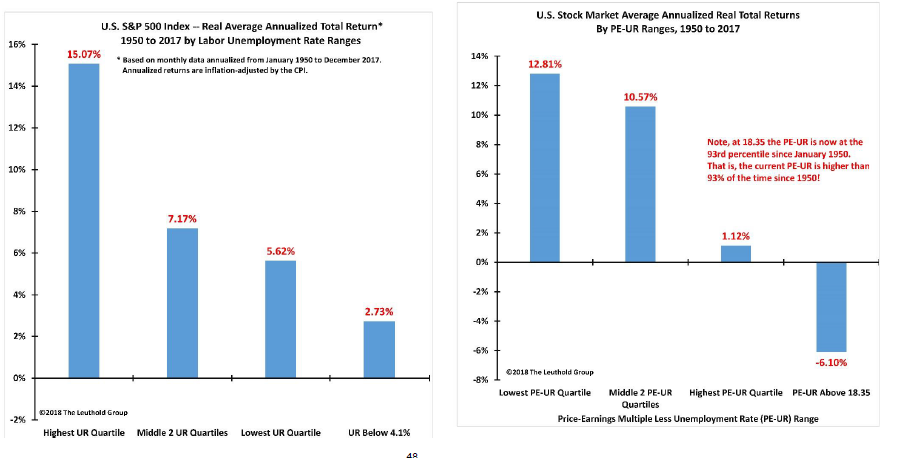

What about stocks? What I really liked about Paulsen’s presentation was his efforts to bring some objectivity to equity valuations.

In these two charts he breaks down annualized equity returns based on that month’s unemployment rate and by the ratio of price/earnings-to-U/E (a dubious number, sure, so take it with a grain of salt). Bottom line here is that it will take a lot...and I mean a lot...of game changers to drive and outperformance in equity returns from here.

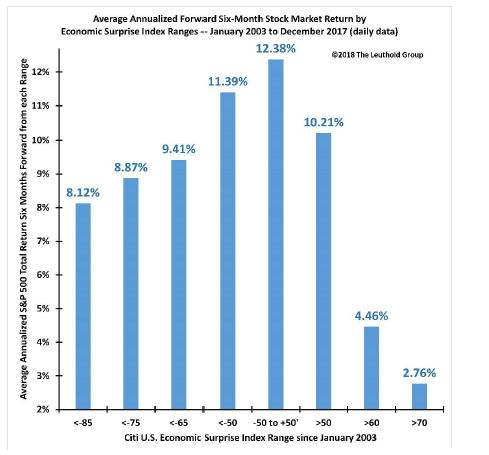

The Jeremy Grantham Fan Club, to which I count myself a member (although with the healthy cynicism of James Montier), will recognize the guts of the analysis here. Another way Paulsen looked at it was to look at six month annualized equity returns given certain buckets of the Citi economic surprise index. That index came into the year around 80 and while it has fallen back in recent weeks, the outlook after January’s equity melt-up isn’t good.

Unless the economy finds a miraculous way to outperform the high expectations already baked in, equity returns are going to be low, with downside risks. It’s the white goose walking merrily along, ignorant of the fact it is being stalked by a black swan and a gaggle of grey ones.*

Maybe one of the grey swans strikes--higher inflation, higher rates, lower equity valuations, or a simple slowdown in the economy-- but no shock. But as I've highlighted before, the market is ever more susceptible to the unexpected black swan.

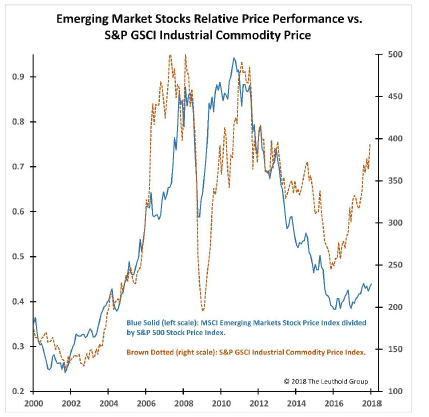

Put another way, the economy is good….it’s bad. If bond yields are heading higher and US equities are fully valued, where should you put your money? Again like Grantham….and me!....the answer is emerging markets.

Commodity prices and the value of the dollar are generally good proxies for the performance of emerging markets assets. Industrial commodities like aluminum and copper have been on a tear lately--and while EM equities have done very well since bottoming in 2016, their relative performance--especially beta-weighted--has been just ok.

I’ll save a few more charts on what I believe shows better equity valuations, growth capacity, and real rates in EM...you get the picture. Compra!

*If you have the photoshop skills to turn that white goose gold, please get in touch with TMM management immediately.

63 comments

Click here for commentsI think if you get the direction of the dollar right then you'll answer a lot of the questions about EMFX , commodities, Emerging equities. My issue with them all is the current weakness of the dollar.

ReplyI think the story on FX is the relative rate of return on capital, rather than interest rates. Some talk out there about allocation changes by reserve managers, but I don't think that can be a big long-term trend driver in this type of market.

ReplyThank you Shawn.

ReplyA few thoughts ... I was thinking back to the 70's inflation and its causes. There were the oil shocks, but there were also the Boomers entering adulthood with their incremental demand pushing against supply. Now we have the Millennials, an even bigger generation than the Boomers, who -- after a period seeking out "experiences" -- are all going to want houses, furniture, etc.. Doesn't matter if they haven't got savings since all the Boomers need to lend to them to fund their retirements. So, arguably there's this burst of demand coming from the (bigger) echo of the demographic that gave us the big inflationary burst of the 70's. At the same time, Boomers will retire but I note 1) Millenials are a bigger demographic, 2) Boomers consumption fell already once their children left for college, and 3) they're going to go from saving to dis-saving their wealth with implications for term premium (set against Millennials who won't be saving, but borrowing to fund massive consumption/housing investment). I haven't worked this all out, but I'd like to see the above argument disproven because it seems plausible. Anyway, all that to say that inflation could surprise for reasons other than fiscal stimulus at full employment.

I agree on EM. The US has some must-own companies, IMO, so I own those. The rest I allocate mostly to EM.

If you want to look for inflation drivers starting back in the 70's I would suggest you look at the massive societal change that took place when women entered the workplace en masse. Following the oil energy supply shock of the early 70's we initially saw a lot of adjustment via the reduction of the working week.When that finished around the mid 70's we were just in time to catch the 2nd oil shock and through that period onwards we saw huge change in families going from single person to two person working units. Changes to disposable incomes via that channel was to drive inflation for years to come. That real rise in income saw inflation rise to ever higher peaks. I really doubt we ever see such a driver again if only because I cannot see where the impetus could possibly come from unless we start to see child labour again :)

Reply@johno, US must have companies? Which are they?

Reply@Shawn: the recent reduction in the Fed balance sheet was quite nicely correlated with the market correction. Keep an eye open for any repeat of that dynamic as we go forward.

ReplyLast week's ~50% retracement brings us to an interesting juncture. Will dip buyers and vol sellers be rewarded as in the prior regime? Or is there something different about the market after the collapse of the explicit short vol trade?

There was more than a hint of "short covering into options expiration" about last week's rally. Now that an obvious source of buyers is exhausted one wonders if this market will drift upwards, or turn down again to probe the early February lows?

We are also going to suggest that EURUSD has put in a short-term top, and that we may now see an episode of firmer dollar (and Treasuries), lower commodities, EM FX and equities. Positioning remains extreme, so those on Shawn's side of the ship are either going to continue to make money, or we may see a few fall out and get wet if the greenback finds its feet.

US markets closed Monday. EZ inflation data out Friday. FX punters will have that on the radar all week long. US auctions of 2s, 5s and 7s ahead. It's all about EURUSD this week, we suggest.

well PMO index is still squashed to the ground

Reply@Leftback: To what precise mechanism do you tie balance sheet reduction to market corrections?

Reply@Johnno: My research on the 70s inflation (I wasn't alive at the time to speak from first-hand experience) tells me that it was the one-two combination of headline inflation from the oil supply shock and the relatively high percentage of wage contracts with COLA provisions that led to the wage/price spiral. In fact, I would love to see/do a study on something like Union penetration and core/wage/services/(something) inflation. Off the cuff, of the US, EU, JP, and UK (selected arbitrarily) the UK has by far the highest percentage of union membership, at 25, and by far the highest post-crisis inflation rate, at 3. Point being that with the bargaining power of the US labor market being what it is, and with trends in market power of firms, I'd think the previous cycle's max inflation rate is the upper bound.

Oh, and I covered the predictor I watch for CPI here: http://www.globalmacroblogspot.com/2016/05/06/the-deal-with-us-wage-growth/

Reply@William: I think the implications for market liquidity of the Fed's open market operations have been widely discussed. Fed purchase of Treasuries ("QE") pushes other investors out along the risk spectrum and provides liquidity. Balance sheet reduction via sales of Treasuries ("QT") puts this process in reverse.

ReplyI do agree with your view of a limited upside for US inflation.

@Leftback: I haven't gotten deep into this since the Krishnamurthy paper back in 2013, but I've always been skeptical of this particular transmission mechanism. I'm with Woodford in that to the extent QE worked it did so via policy-commitment-signalling. After all, and maybe I should do a post on this, the evidence from Japan as far as QE driving equity returns is pretty weak.

ReplyWhile supply and demand clearly do affect prices, the general price level over time should more closely reflect monetary policy, i.e., the relatively value of fiat units compared with some basket of real goods. This has been proven wrong by the rounds of QE over the past ten years not resulting in the inflation feared/predicted/hoped for, but if it's really wrong then there is a free lunch to be had from just printing money. I am still waiting for this to be fully resolved and for economists to have some explaining to do ...

ReplyThe auctions all seemed to go off, despite the astonishing amount of supply. 2s not wildly enthusiastic, but not a disaster. 5s and 7s still ahead this week. The high yield for the day in US30y was just prior to the auction.

ReplyIn other news, equities may have stalled after the ~61.8% retracement of last week, as we and others had suggested. Many thought the bull was about to resume, but perhaps Mr Market was just Fib-ing.

The dollar is firmer as yen weakness adds to the momentum generated by the Euro's recent reversal from 1,2500. Dollar strength is now viewed as a risk-off factor. Not all of the trapped longs made it out last week.......

Quiet day. Markets were never going to go straight back to highs a week after the hit they took. Peeled off some exposure late last week. Re-entered a EURSEK cash position today. We'll see ... have a major level, dislocation on model, seemingly transitory factors causing today's CPIF miss, a mean-reversion economic setup (FX => inflation => rates => FX), etc., so worth a stab.

ReplyMarch 4 is the day. Less for the Italian elections than the SPD vote results which are due then. Apparently bookies put odds of upset at 25%.

what do you mean dislocation on the model? I mean, I suspect I know what you mean, just curious what model, what magnitude, etc. EURSEK is kinda a pet project.

Replyalso circling back to old news, interesting to me that VIX is chopping around at these levels. We're getting some realized intraday vol that would have been notable in the first half of this year. Seems like some gamma is still getting worked through the market, leading to choppy markets. Short positioning might catch up with rates.

ReplyTMM2 is gonna have the gone fishin' sign out most of the rest of this week. Good hunting.

@nevjev It's maybe not a free lunch, but not much of a lunch at all?? What happens if the Fed prints $10tr then buries it at sea?

ReplyI'm still short ZT, Schatz, and long euro and yen, both in dollars. Core Positions.

All I did today was sell a little Cable vol. Premium is rich.

Hey Shawn, good question! I don't have a very satisfactory answer (not to me and certainly not to any econometrician). On a 5Y rate differential model, it looks very dislocated. When I throw in changes in the Valueguard housing index, the fit is a lot better and arguably there's no dislocation (depending on the comparison, 3m, 6m, 1y changes). Throwing in differences in the JPM forecast revision indices seems to improve explanatory power over longer data sets. Happy for anyone to chime in and school me.

ReplyIf I had to single out one headline today, it's Reuters Corporate Survey in Japan. Looks like companies are not raising base wages. Labor market tightness and Abe's tax incentives not making a material difference, it would seem.

ReplySA budget looks good. The 30Y bonds I mentioned here when at 87 are now >98.

Nice one on SA, @Johno, and interesting note about the (lack of) Abeflation and the implications for USDJPY.

ReplyWe closed our EURUSD short before the FOMC minutes and took a profit from entry at the 1,2500 area, but in the end DX barely budged in response to what some viewed as "hawkish" minutes. We will mull that over before any more FX punting.

The jury is still out regarding equities: "fib and fade" v. "Buy the dip and ride to ATHs". "Fed days" often start weak and finish strong during QE (Yellen, QE era) but they can also start strong and finish weak (QT era?). The action in the small caps today looked like short covering early, as IWM out-performed, but there has been no follow-through after the initial (stop-hunt) spike, which we faded. The EEM has more or less the same dynamic today, that's potentially a good short right there. The reversal action in HYG after 2.10pm looks quite nasty.

Looking at Treasuries, we are almost all the way through a week of $0.25T supply, and things haven't completely fallen apart, with the 5y sale over and the 7y auction still ahead of us. 10y still comfortably < 3.00% and 30y just touching the 2017 high yield of 3.20%. We suggest you have to be a buyer at these levels, and we think the wider spreads will continue to attract Japanese, Swiss and European (German) fixed income managers, especially when the evidence suggests the USD has stabilized.

One would have to guess that the Fed wouldn't choose this week to sell a shedload of USTs into the market, and most people seem to fancy the first week of the month for open market operations. But we won't know for sure until after the fact.

Further to some of my earlier posts, has anyone looked into the effects of double income familys (Some still struggling), and the social impact of children growing up with little or no parental guidance for long periods of their yout(often rared by different nationally).

ReplyAny pointers welcome.

Wow: https://www.wsj.com/articles/the-robots-are-coming-for-garment-workers-thats-good-for-the-u-s-bad-for-poor-countries-1518797631

ReplyWhen the cycle turns down, people will replace "favorable demographics" with "demographic time bomb" in their South Asia narratives (and when back up, "favorable demographics" again).

2% down move in last 1.5 hours of trading after faking a rally all day? This aint 2017 chaps.

ReplyIndeed. Ugly reversal candle for Spoos and a nasty looking close. If I was a JBTFDer, I probably wouldn't have enjoyed that much. Fading the 2pm spike in equities turned out well on the day. EEM and HYG looked horrible late in the session.

ReplyToday didn't resolve the debate between "fib and fade" v "to the moon, Alice", but you'd have to say that was not terribly bullish. SPX 2750 area seemed to draw sellers not buyers. Did algos get reprogrammed to sell the rips and turn bearish?

Not sure I would want to be a crude oil long tomorrow. Warmer weather, US production spike, firm tone in the dollar. The magic ingredients for next month's lower inflation data are already being added to the pot.

This week I've been unplugged from markets while I work on some other projects. About 1pm I checked in on the market and saw it was up smartly. I went back to reading a book with a chapter that recounted the equity quant fund debacle in August 2007. The basic story was that all of these funds had a great run of performance, experienced massive inflows, and were all locked into many of the same trades. When one saw a big outflow, they were forced to liquidate a big chunk, which triggered a chain reaction of outflows and position unwinds. While these were market neutral funds, the ensuing panic blasted the equity indexes which were already listing as it was becoming clear that something might be amiss in the US subprime mortgage lending business. Equity markets recovered given the lack of any overarching change in economic fundamentals, but with the benefit of hindsight, it was clear that this was a signal of what was to come.

ReplySound familiar?

Back in 2018, two hours later I'm in line to pick up my kids from school and the radio guy says the S&P closed a nifty 40 points below where it was when I checked it at 1pm. Indeed, our contemporary version of the equity quant debacle isn't quite over.

As I noted last week all of the plates can keep spinning if growth, and thus return on capital, stays high. But it is tough not to see the parallels with prior market accidents.

Know what you mean Shawn - It's GRReat

ReplyGlobal RIsk Readjustment

https://polemics-pains.blogspot.co.uk/2018/02/grreat-great-risk-readjustment.html …

Perhaps it would be best to refrain from comment, in the light of the recent editorial advisory. Regular readers are free to think for themselves, of course, and are invited to look at today's chart and inspect the timing of the comment by "BS".

ReplyOne is tempted to invent a character called "Sell Stocks" that simply repeats, yet inverts, all of the BS comments into a stream of anti-parallel "SS" comments… but that would be infantile. :-)

Jorda, Knoll, Kuvshinov,Taylor paper suggesting residential housing has been a better asset class than stocks being contradicted by CSFB 2018 Yearbook. Will be an interesting debate to follow .. would be nice if they made the full analysis available ...

ReplyMaybe lost my nerve, but don't like how EURSEK grinds through 10.00. Don't like that it's February and we're here, either. Took off cash position, for now, and will wait for tomorrow's minutes.

Replythe best thing to do when you don't understand what is going on is to get out. - Or blame the Russians

Reply@Johno, i looked up that paper, I haven't read it yet but here's the first sentence:

Reply"This paper answers fundamental questions that have preoccupied modern economic

thought since the 18th century."

It's only been 250 years, it's about time some university professors finally got around to doing this.

https://www.bankofengland.co.uk/-/media/boe/files/working-paper/2017/an-interdisciplinary-model-for-macroeconomics.pdf

Replythat is the best piece I've read in Eons.. sorry old..

BAsically points out in a formal way, how economics has got so far up its own arse its detached from reality.

I am amazed how many economists have no clue how people behave in the real world when economics is all about behaviour.

just look at this from teh economist - The Economist (Bagehot): “It’s a truly depressing mystery of modern politics: all the signs suggest that leaving the EU will cause economic hurt, yet voting intentions over Brexit remain unaltered.”

Because you ignorant economist in your economist bubble .. not all decisions are taken to maximise financial gain

@johno, agree, very interesting subject. The point a lot of people miss is that the ease and speed with which one can get in and out of stocks and equity derivatives outweighs the "safety" label attached to real estate (with that label obviously being somewhat tarnished after GFC). I realize that a long-run rate of return is being discussed by the economists, but in the current instant gratification society I would think that the new, inexperienced money is flowing into stocks solely and Wall Street participants will come up with a million reasons in their yearbooks to entice the source of funds to continue a perpetual flow into equities. Note that I am invested in both and have zero skin in this debate either way. YES, I BUY STOCKS TOO. See, all caps to appropriately underscore the fact that most adults here are already holding equities position in their long-term portfolios (thru IRAs, 401Ks, HSAs, and other tax-deferred instruments) and don't need to be reminded by children on daily basis to add to that gargantuan position, while they trade around the core.

ReplyPersonal thanks to Shawn for taking a stance. Back to sleep...

IPA, if you have not done so already, check out the weather in Europe...

ReplyIPA ranting after losing money on equities again :)

ReplyMeanwhile Nasdaq is pushing back up to all time highs (as I predicted). I don't wanna say I told you but... I told you! Talking of which, I wonder where Nico etc have got to? They must be hemorrhaging money right now...

@Skr, Europe is large...

ReplyThought troll was banned...

ReplyOil backend big outperformance, it’s a change. Are we entering phase 2 of an oil mega bull?

Bear in mind we doing this whilst us production rising and inventories declining.

Given comments here re pension fund vol selling, I thought we might want to check out this brief piece from GMO:

Replyhttps://www.gmo.com/docs/default-source/research-and-commentary/strategies/equities/global-equities/the-value-of-short-volatility-strategies.pdf?sfvrsn=2

My reaction: https://www.youtube.com/watch?v=kNDPIGSPdFA

After a mixed week in which we ended up more or less flat, LB decided it was time to sit out for a while. From here we can either enter another period of vol selling and spoos making new highs (as Buy Stocks would suggest) or experience another wave of selling and re-test the early February lows. It's just hard to read the charts definitively at this point, and indeed Friday's late trading gave the impression of people quietly covering their shorts and going home. We could easily see another 2-3 weeks of chop and slow upward drift into the March expiration.

ReplyRetaining a small position long UUP for now, and awaiting what seems like an inevitable rebound in fixed income, but with no need to over-commit one way or another right now. Going flat into the weekend guarantees a peaceful Monday morning.

Btw the comments about everyone here losing money are asinine, since several made handsome profits on the brief inverse vol debacle that would provide a good return for an entire year. Of course, we all know that some punters Never Lose Money - that in general they are Always Winning Big - because Bertie Big Bollocks only Shits Gold Coins.

We will be back when we have a better handle on something worth trading, but it might be a few weeks.

Re: Leftback's comments about "profits", let's look at some numbers:

Reply- Macro funds averaged +3.6% returns this past year.

- The SP500 has averaged +15.8% pa from 2009 to the end of 2017 (inflation adjusted).

- In addition, we just suffered a circa 10% dip in US equity indexes. Those who BTD have now made 5-8% on one trade (unleveraged), in addition to the +2.7% return the SP500 produced in Jan 2018.

Macro and other asset classes would struggle to beat "buy and hold" in equities. For an active equities trader, the returns are substantially bigger again.

Buy Stocks, please address your hate mail to Brevan Howard, Moore, Caxton, PTJ, etc.. I think you have us (and our returns) confused with them.

Replyjohno thinks he's better than Paul Tudor Jones HAHAHAHAHA

ReplyThanks for the laugh johnyboy! Did you manage to turn a profit in your demo account in 2017?

PTJ and others play a different game. They have to because of the size they have to trade to move the needle on multi-billion AUM. Certainly couldn't say I'm better than them, but my returns are superior because I can play a different game.

ReplyAs for thinking I trade a "demo account," well, you're just clueless.

@johno

Replynot a polite way to start a conversation here, but how do you manage to look at pretty much everything? EM/DM stocks, IG credit, South African long bonds, Scandie FX, probably more that you never mentioned yet? Are you the dreaded macro tourist? Genuinely curious, not trying to be acrimonious.

re your earlier WSJ link about automating jobs in Bangladesh, potentially robots can hit voice-concentrated BPO industry too.. which has been one of the econ drivers along with remittances in the Philippines. At the same time the Chinese have plans to enter this industry too. Curious how this story is consistent with PHP borrowing in USD at 3.65% for 10 years and 4.10% for 20 years at BBB rating. More broadly, remittance growth has been strong enough to offset the widening trade deficit, and goods exports composition looks solid too with high share of semiconductors, unemployment rate is low, budget deficit within 3%, big infrastructure plans, debt/gdp under 40%, so I guess investors like that. No one minds the political climate or murky borrowing of unknown and potentially large sums from the Chinese, though.

https://www.ft.com/content/93a984e8-7772-11e7-90c0-90a9d1bc9691

https://www.bloomberg.com/news/articles/2017-07-31/philippines-vows-to-defend-outsourcing-empire-as-china-rises

MPT, there are plenty of people who look at more than me. Speaking for myself, time management, check lists, access to research, Bloomberg. I actually don't look at corporate credit nor single name stocks, except for the big technology names (technology is macro, in some sense) and merger arbitrage (where I don't have edge vs most HFs, so spend little time and run a diversified book to collect risk premium). Duration is tricky and I trade it infrequently, equities are mostly index funds in a buy-and-hold book, so that leaves FX and STIR, which is doable for one person in the liquid markets.

ReplyAlso, I "grew up" in the HF model of grinding out 1-3%/month and never having draw-downs >2%. Some people are comfortable with a lot more vol than that. I'm not. Consequently, I HAVE to follow many markets to populate my macro book with enough (hopefully independent) bets to get the returns/vol I'm comfortable with. I just do it, because I have to. Anyway, enough about me. I'm just some dude ...

Replythnx, appreciate the response.

ReplyIt is getting unbearably hot in this room. Perhaps it has been for a while but I have enjoyed the days (few and far between lately) when people ran in here to voice their informative and educated opinions rather than offend us with some garbage. I guess one has to take the good with the bad and ignore the nonsense. But folks, how about some quality commentary to support this blog and prolong its existence? I urge the regulars to continue with what has been a long tradition of respectful debate and friendly exchange of strategies. Please remember that we are here to help each other and not destroy the profession. It's bad enough we are being called the dinosaurs by little children who just left the playground to run in here, interrupt our deep thoughts, and tell us that we will not see a stock market correction in our lifetime. Study the economic cycle, please, before you shout nonsense like that in the room full of professionals and have the audacity to tell us to bet on it too. Let's hope that some adults here plan on living longer than a few years to finally see these children learn their life lesson.

Replysome folks are getting distracted indeed

Replyam surprised the Chinese house of cards recent bankrupcy events are not mentioned at all

HNA/Anbang

Reply.. and Yonghong Li now feeling the heat from loan sharks sorry, from in-house shadow banking

Otoh, if you want to buy some high end property just call the China Insurance Regulatory Commission. The marketing started already, fire sale prices are almost guaranteed.

ReplyUgly stuff in housing, guys. We have back to back very weak new home sales, somewhat of a s/t trend starting to develop. And those who will be quick to discount NE slump due to bad weather should look at South where the weather was much better. If it wasn't for Midwest, this number would have been down double digits. Also, supply is up half a month. I hate to draw a trendline on such a number, but folks, it is getting near a possible s/t break if we see another month of ugly numbers like today. Median sale price was up within historical norm. The truth is rates are rising faster than many would like. Look at mortgage applications - ugly, ugly, ugly. Refi market is dead and puchase market is coming to a screeching halt. Existing home sales were weak for two months in a row as well. Time to look at ITB and XHB as possible shorts? Those two charts have developed a s/t top, looking much weaker than the rest of the equities on this recent rebound. I say short the bounce to s/t resistance levels.

ReplyNasdaq almost back at ATHs - just like I told you.

ReplyI may be "disrespectful"/unpopular, but I am right.

Remember when people here thought US equities were gonna re-test the lows? Or when people here predicted that this dip was the next 2008 crash? #goodtimes

ReplyHalf this blog really needs to go buy "Trading for Dummies" asap. As a bonus it'll increase AMZN's profits, thus boosting Nasdaq to new ATHs and making me even more money! Win-win! Bwahahaha

delete the troll...

ReplyWe are approaching multi year highs in longer dated WTI (but still in 50s) and I don't see what derails it. Saudi wants 70-75 brent back end ahead of aramco, a good 10-15 higher than today, and the back end needs to be there in my view for supply to keep up with demand. EIA and IEA remain in denial - their longer term US supply forecasts do not stand up to scrutiny.

i think there is, and will continue to be some momentum in the housing market despite higher rates. Where are we in a 30yr fixed? 4.375%? Don't think that is going to put and end to the entire project. Time will tell, I guess.

ReplyI feel like I'm beating a dead horse on this subject, but for the remedial class, let's go over this again:

1) Macro and HF returns are not analogous to equity returns. I know that's tough to understand, but don't sweat it, it flummoxes every nearly journalist at Bloomberg too.

2) the benchmark for macro and HFs is--I repeat--short-term or intermediate bond yields or some spread over LIBOR.

3) Yeah I know, crazy, huh? Think of it this way. What is the duration on your average macro or HF trade? Sure, there may be a few different flavors. But in macro, let's say generously it is six months. Sounds kinda like a short-term bond yield, eh? So I better do significantly better than that to pay for the significantly higher volatility and liquidity risk I pass to my investors, the rent in midtown, my bloomberg terminal, compliance department, an analyst from Penn State to book my trades, sort through research, and fetch my lunch, rent on the upper west side, my kids' tuition and my wife's spending habits.

If you think that's too big a rock to roll up a hill every year relative to short-term bond yields, by all means, fire away. But it has nothing to do with equity returns.

Sorry for the content outage, normal service resumes tomorrow.

Shawn, you forgot the hookers...HFMs are now mostly divorced ;)

ReplyBack to serious matters... So while it may be the consensus thinking at first on the housing (who throws themselves out the window at 4.5% on a 30yr fixed?) one needs to take into account the complexity of the post-GFC housing recovery. It began with investors, above-mentioned "stupid" HFMs, scooping up the SFRs at close to pennies on the dollar (in huge packages too). Cash transactions reached just under 50% at the bottom of the trough. Fast forward, cash buyers are stepping back en masse (we are in mid teens for investor cash purchases), as foreclosures are at the lowest since then (only 5% distressed sales), courthouse steps are all but empty (there are no deals to be had, baby, don't even show up), and what do we have left now? Mr. & Mrs. Smith are our new heroes again, unemployment lowest in ages, and wait, wages are starting to rise now. With DTI restrictions at a new low since GFC (FHA to the rescue), they may be increasing their spending on home improvement stuff at HD and LOW, right? Look at those charts coming way off the highs and still sitting 10% below, just as resident children are about to scream in here that we at ATH on spoos yet again. Stock market is a discounting mechanism (I hope we all agree). With January new homes starts shooting up and builder confidence in its highest level since GFC why are ITB and XHB having such a hard time catching a bid? Something is definitely amiss here, and I agree with you, Shawn, time may be needed to figure this one out, but with cash buyers declining, liar loans and cash-out REFIs gone, the ARMs resetting in droves and no good second mortgage rates to be found, this is a totally different market even with the employment at its lowest in ages. Let's also not forget that prices are creeping up quite a bit (about to see it tomorrow in Case-Shiller) but wages are mostly not, at least not at the same rate, not even close. LOW reports this week, sell the news? D.E. Shaw accumulated a big chunk for an activist play. I dunno, I smell a rat. Sell XHB.

IPA,

ReplyI get it, but why not pick a few select shorts within XHB? If your thesis is correct, wouldn’t the risk/reward work out better? Or is that too “micro” an approach? Thanks.

ha, I guess I ran with a boring crowd! certainly alimony and "expenses surrounding new 25-yr-old GF" could be in the picture and accelerate the cost curve accordingly.

Reply@Great Unknown, I like XHB for retail components which should also take a hit on home improvement, appliances and furnishings side. Certainly not opposed to individual names but would need stronger conviction. Mostly playing the inevitable slowdown in the sector due to accelerated rate hikes and prices at the moment, hence painting with a broad brush vs threading a needle.

Reply@IPA, I think we are only now catching up with pent up demand from the 2010-2015 period. You're absolutely right about private equity running head long into SFH investment properties--not sure if I brought this up a few weeks ago, but if you look at the publicly traded ones, they are looking at cap rates around 5%....when 10y ust is closing in on 3%! Not too different from any number of credit trades or local rates in certain high quality commodity-based EM countries with specious histories of inflation volatility (I'm looking at you, Chile).

ReplyBut the GSEs are just now getting on board with securitizing their holdings there so there could conceivably be quite a bit more runway before it all crashes and burns.

IPA thanks for the thoughts.

Reply

ReplyI hope you will be adding more in future.