I guess I’m not much of a Fed watcher. There’s something I don’t like about the Kremlinology aspect of parsing a Fed governors words. Sell side economists, financial media, and no small amount of fin-twitter opine on every speech as if it is potentially a game changer for monetary policy, rates, and the value of the dollar. However, when you have a new chairman of the Fed, it pays to sit down and listen to the guy for his first speech in front of congress, because he is going to bring his own style to the proceedings--and ya never know….maybe some new substance.

So this passage stood out:

“In gauging the appropriate path for monetary policy over the next few years, the FOMC will continue to strike a balance between avoiding an overheated economy and bringing PCE price inflation to 2 percent on a sustained basis.”

I can’t remember the last time a Fed chairman used the words “overheated economy”, and the unequivocal statement that they will manage monetary policy is such a way to avoid it.

What is more peculiar about this statement is not just the hawkish implications--but the clear implication that the level of PCE price inflation is potentially mutually exclusive from an overheated economy. When you consider that in the context of a dual mandate--it illustrates what I think is a big trend in central banks around the world since the financial crisis: There is a stealth mandate to maintain financial stability, or at the very least an implicit one embedded in the stated mandate of all central banks.

What does that mean for the hiking cycle, and for rates at large? Clearly it is hawkish. It is also argues that Powell is looking at:

1) an economy at full employment,

2) inflation somewhat convincingly, but not conclusively, ticking higher,

3) higher commodity prices ( mandate is HEADLINE inflation, not core...so this matters, even if they don’t say so), but also importantly

4) a government that is bound and determined to borrow and spend money like a drunken sailor on leave,

5a) financial conditions at increasingly easy levels, 5b) credit growth starting to tick up, and 5c) financial markets showing some signs of froth, reaching for risk, etc.

Add those factors to a Federal Reserve that has the institutional memory of a financial system that exploded at the end of a three year hiking cycle, despite modest upticks in inflation, and you can paint a picture of a chairman that might look to be more aggressive in reigning in excess than his predecessors--even if the past several years of central bank policy history seem to imply that monetary authorities shouldn’t pump the brakes too fast as economies recover and financial markets recapitalize.

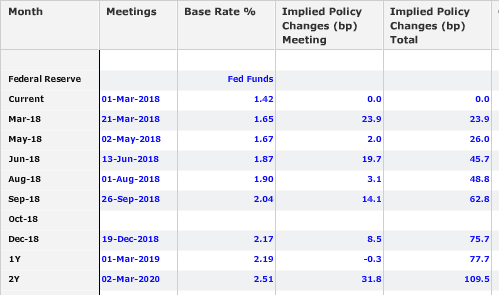

Which leads us back to what we all really care about, WIPI. What Is Priced In?

The Powell testimony put paid to the front end again….but took levels pretty much in line with “the dots”:

75bps this year….yes three hikes, on the screws with what was in the December SEP. But the cycle peters out after that, with roughly 30bps priced in for 2019.

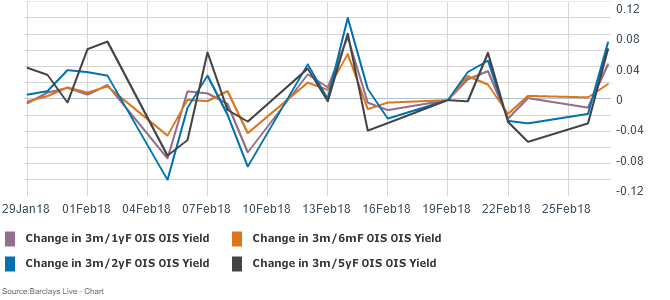

Here is a mockup of the impact from Powell’s speech, using 3m OIS rates at various forward tenors.

More simply, the front end 3m rates were far more stable than the 3m rates one year, two years and five years in the future.

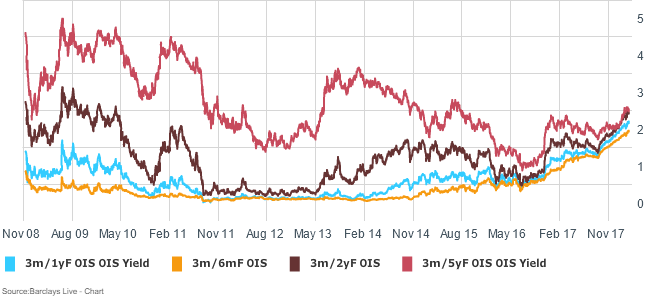

It’s a bear steepener in the front end--but consistent with the type of policy shifts that can put a bid into the long bond--higher front rates amid stable long-term flows. And looking at the outright levels of those 3m forward rates, the levels five years out-somewhat consistent with where the market’s estimation of a “neutral rate” might be-- are only just now reaching that seemed sorta normal-ish between 2011 and 2014.

Bottom line, the market isn’t counting on a bear steepening in the front end relative to the belly of the curve, but the combination of fiscal stimulus, high commodity prices and a hawkish FOMC chairman might just do it---and shepherding the curve slowly but surely in that in that direction might be the best way for Powell to let some air out of this balloon global central banks inflated over the past decade.

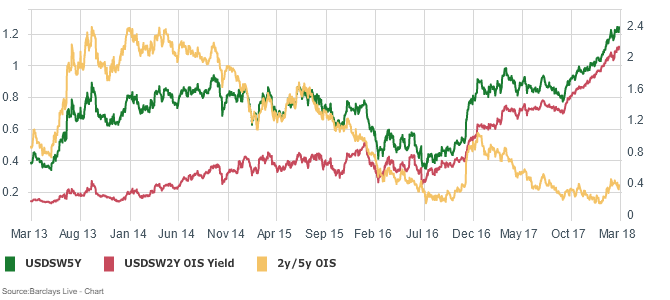

2y/5y OIS is sitting at 25bps--unless Powell moves decisively towards four hikes this year, the market might shift towards higher rates later rather than sooner...especially if it is appearing that wages are taking more time to accelerate than many seem to expect.

Yeah, I know….US economic data is already starting to tail off...commodities have seemed to find a level here...and yes, maybe there is something to the impact of higher rates on the housing market. And I believe the most convincing argument in favor of lower rates from these levels is the unwavering commitment of the ECB and BoJ to keep rates right where they are. Suddenly nearly 3% in dollars doesn’t sound so bad. As such I don’t think the long bond is going to far. But when the long-term neutral ex-ante real rate is at 50bps, there is still room for that to move higher.

Why did I use OIS rates here? I wanted a clean picture of Fed-implied policy rates since LIBOR and swap spreads have undergone some big policy-driven changes over the past couple of months...who said US rates are boring!! Stay tuned for more on that subject on Friday.

ShawnTeamMacroMan2@gmail.com

@EMInflationista

29 comments

Click here for commentsPowell is not going to stop until he and the rest of the Fed get a louder message from the market. I mean it usually does not take much for these folks to get scared, but they are not even close to that point. This being said, some here are quite clueless while calling for cyclical stocks, namely Nasdaq, rising 50% from here into what is clearly a hawkish Fed in a damn looong time. Let's not worry about cash on hand for those stocks and their diminished dependence on borrowing (even though that thesis could be highly contested lately in some cases), let's worry about the cyclical nature of their business and a possible slowdown in orders. We are not too far from it if Fed is going full steam ahead with their rate hikes. We are not at the very beginning of the rising rates cycle any more.

ReplyAnd as for stock market overall, the last few days were not pretty and you will see how worried equity investors will be every time Powell will open his mouth. I would like to point out that we have a trendline break galore in REITs here. Pull any of these ETFs up and you will see exodus en masse in progress and massive head and shoulders formations: IYR, RWR, XLRE, SCHH, I could go on... Some would say what's the big deal? As I drive around the local shopping centers and office parks I am starting to see more unfilled holes again, and the anecdotes from res/retail/office/warehouse landlords are that the rents are starting to fall hard. You tell me how and what company will go for that big tech upgrade if their visibility is getting bleak? You are lucky they don't break their lease. I don't see 50% rise in Nasdaq from here if the rates are moving higher at this pace, tech orders will dry up fast. Let's just not get into this "calling for a bear market" thing here again, please. Let the price tell you what the heck is going on right now. Look under the hood, some sectors are flashing a possible regime change.

Thanks, Shawn.

ReplyThinking of what threatens central bank independence most, allowing another financial bubble to inflate (and inevitably burst) seems a bigger threat than inflation undershooting target by zero-point-something percent.

Took off last of EURNOK short today, leaving some puts cheapened with barriers. Very light macro book this moment.

Sorry I didn't comment on yesterday's Mexico piece. I still haven't got a trade yet there, but focused on other things.

yes! I meant to mention that point about cb independence--that is the driver for the move towards the "third mandate"-- but spaced it entirely.

ReplyI've tuned up the mex model a bit more actually--I looked back at the 2011 election inn Peru where Humala won, a very similar candidate to AMLO. CDS moved about 50bps wider. So I think the potential for a 30-40bp widening from current levels is probably about right, which would mean the implied probability of an AMLO win is in the low 40s, and makes Mex CDS look about 10bps too rich and a good risk/reward here, IMO.

And a heck of a lot cheaper than FX vol!

from the same January impulse it's a very fast market compared to 2008

Replythe 2500s bottom looks like 2008 MLK globex low (1250)... the 2790 looks like the 1430 reached in... May 2008 - it took 4 months to build a lower high before the bear market began. i am calling 2790 the Powell lower high and the bear market may begin from here. I am curious to see where long only 'strategists' would go 100% cash if mister BS would ever let us know of his strategy 'before' and his execution 'as' it happens.

Meanwhile Japan is the slo-mo train wreck that noone is talking about. As i've said earlier, Japan balance sheet will go bust with 100bps up move in rates. The failure of Abenomics will be atrociously spectacular.

Good luck to Powell and his soft landing concept, really

Let's not forget that Nico has been calling for another 2008 bear market for the past 6 years. Every 6-12 months he emerges to tell us he's shorted x million notional of SPX. When the market rallies several hundred handles against him, resulting in losses of ~$10m he vanishes. Then repeats the whole charade again... Best of all is he then tells people who are long US equities that they are "BS". Gotta love the internet :)))))

ReplyPS Japan will just monetize it's debt slowly, & not allow rates to rise to any substantial degree (easily done when the BOJ owns the entire JP bond market).

i was trying to have a constructive discussion with you to understand your method and see what triggers your trades - if you prefer to just write days after you 'bought' the dip to tell us you were right, and disappear everytime the market hits lower without even airing downside targets etc then you have no value to us and i call that bs

Replysince you have a lot of time to waste online check my posts of February 2016 - i was buying the double bottom with both hands. In March 2009 too, but you did not know how to read yet

lastly i'm sorry if this annoys you, but i can have $10m drawdown on that $50m notional. It is not pleasant but i can live with it. You probably trade 1/300th of my size but this ain't the point. Anyone trading any size with ideas and gusto and method is valuable here. Any troll like you ain't

ciao

Nico,

ReplyI have an aversion to quoting todays action in terms of action seen many years ago. Whilst it might end up being right, for every one of those I could shown you many more that were not.

So , I try to avoid making comparisons like otherwise ?, when I saw this headline , 'Gas crisis: factories prepare to cut their use amid big freeze ' I might have thought holy 'buy stocks' it's 1972 all over again and once we get past that we'll have the mother of inflation cycles to chase once again. Fortunately, I try to avoid making comparisons like that otherwise I might prepay for my casket.

P.S. Talking about monetising debt of course one only needs to keep inflation running ahead of rate rises and hey presto eventually you do manage to do that, and as far as japan goes they 'own' the market for govt debt so who wants to fight that except of course via currency trades.

Not to bang on endlessly about the same stuff, but breaks were lower again today, suggesting that the Great Bond Bear Market might not really be on the way. Interestingly the dollar remains firm. Some punters are clearly starting to think that the Reflation Train isn't running on time. Perhaps it is merely delayed by the Great British Blizzard.

ReplyDoes anyone here ever pay attention to things like advertisers forward guidance? WPP isn't painting a very pretty picture, and that often precedes recession. IPA is correct about retail REITs, Manhattan is awash with empty storefronts, and malls everywhere are struggling. It is widely assumed that this is "structural", i.e. Amazon effect, but what if it is ALSO cyclical?

A decent trade here might be long mREITs and short retail REITs - or stocks like GGP and VNO. If the economy slows and long end rates "unexpectedly" fall, then the mREITs will do OK this time, while the retail REITs will be battered.

Still on the sidelines for now, next week is jobs week and so likely to be much more interesting.

This is a great post. Can you tell me why it's important to look at 3m forward rates as opposed to the... errr... outrights? FI newb here.

ReplyNice Post

ReplyLearn a new way to gamble.

Replyhttps://menuufa.com

ReplyI think this article will help you make a lot of money.

เป็ปทีน

วิธีเล่นบาคาร่า

ทีเด็ด

ตารางหวย

รีวิวสล็อต

I like your article.

Replypest control

Thanks for sharing, I think this article is useful to everyone. Visit crystal shops near me here.

ReplyHey, that's a clever way of thinking about it. fuckin amazing article

ReplyOh yeah, fabulous stuff there you are! plss write more like this, you're awesome

ReplyArticles like this are an example of quick, helpful answers.

ReplyThat insight's perfect for what I need. Thankyou for sharing!

ReplyNo complaints on this end, simply a good piece you made in here

ReplyThe style is so unique. Thanks for publishing this kind of blog, Keep blogging!... MM

ReplyExcellent site you’ve got here. I appreciate individuals like you! Take care!!... MM

ReplyLot of interesting information here. Thank you for sharing. keep it up... MM

ReplyThanks for a very interesting blog. Waiting for the next blog updates... MM

ReplyIts full of information here that I am looking for, Great work you have in here!... MM

Reply

ReplyAppreciate how organized this is.

ReplyYou explained it in such a simple way.

ReplyA great breakdown of the topic.

ReplyVery relevant to what I’m working on.

ReplyYour tips are always so practical.