(UPDATE: I initially posted this on February 27, but it was missing the Peru 2011 analysis and more depth on the potential downside of an AMLO victory. What follows is the edited and updated version I re-posted on March 1)

After broaching the subject in a post last week, I've been wrestling with how to think about, and price, Mexico political risk. After spending some time digging through more polls and recent electoral history, I want to give you folks a quick walk through the details of how I will be thinking about the Mexican presidential election in 2018, and my admittedly cursory attempt to model the market’s implied probability of a victory for Andres Manuel Lopez Obrador--AMLO.

After broaching the subject in a post last week, I've been wrestling with how to think about, and price, Mexico political risk. After spending some time digging through more polls and recent electoral history, I want to give you folks a quick walk through the details of how I will be thinking about the Mexican presidential election in 2018, and my admittedly cursory attempt to model the market’s implied probability of a victory for Andres Manuel Lopez Obrador--AMLO.

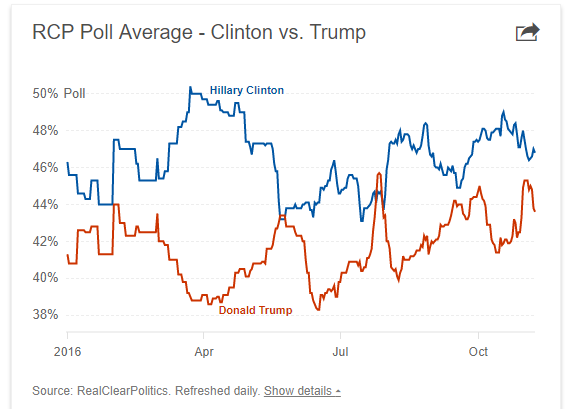

First, let’s look back at the US election in in the summer of 2016, which was a similar stage to where Mexico is now. Before the conventions in July, Hillary led by 5-8 points.

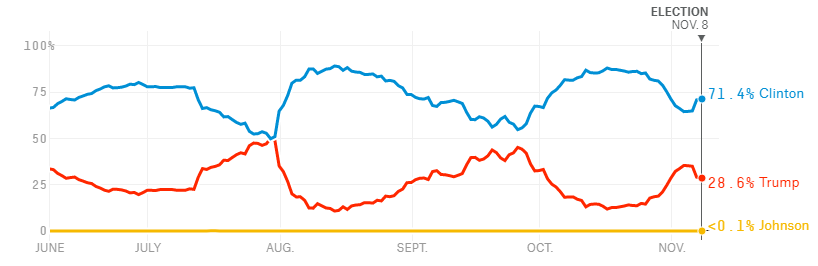

According to the folks at fivethirtyeight.com and most prediction markets (this chart is from my old friends at the Iowa Electronic Market), this translated into a 70-75% probability of Hillary winning the election.

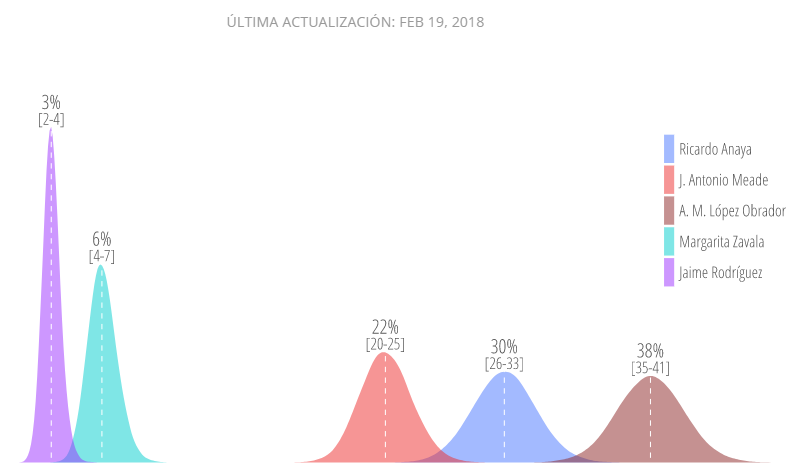

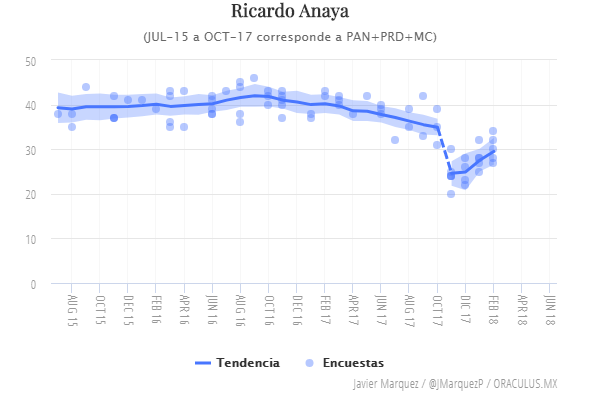

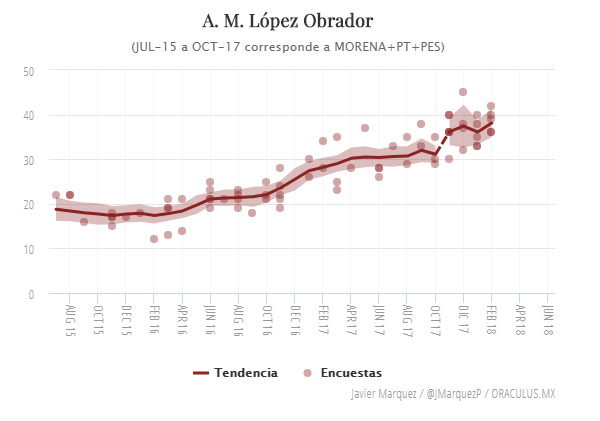

Now, let’s turn our attention to the polls in Mexico. AMLO leads the competition by a similar margin to where Hillary was in July 2016--all data and charts here from the people at Oraculus.

Thanks to @horaciocoutino for the excellent data visualization

In their brilliant poll of polls rendition, AMLO leads by 8 points, with the lower bound of the 90% confidence interval of 35% (the numbers in brackets), while the upper bound of Anaya’s confidence interval is 33%.

Where does that leave the implied probability of an AMLO victory? Just looking at this polling data, one might say it is pretty close to 70-75%, just as it was for Hillary in July 2016.

The race seems more likely to tighten from here, rather than AMLO running away with it. First, support for the PAN candidate in polling data cratered last September with Margarita Zavala broke with the party to run as an independent. But Anaya has started to recover as he is now looking like the #1 “anti-AMLO” candidate. If he continues to run a “clean” campaign and performs well in the debates, one can envision him converging towards the 40% levels of support generic PAN candidates were receiving in mid-2017. That’s not a done deal--Zavala has gained some support lately and continues to troll Anaya on Twitter--but right now it looks like the path of least resistance.

Meanwhile, AMLO has had a very good run. He has consolidated the support of his base and made some inroads to the middle class that was lukewarm at best during his previous campaigns. So far, he has won the battle to re-cast himself as a kinder, gentler, cuddly version of AMLO.

Where does he go from here? I believe AMLO will gain more support as a second choice from “strategic voting” than he has in the past, but he is still a divisive figure. It is tough to believe this chart is going to continue to trend higher towards 50%. Are we at Peak AMLO? Peak implies a summit and decent--I’d lean towards “Plateau AMLO”, even though it doesn’t have near the same ring to it--and it is certainly plausible that he hits some landmines between now and July 1. As the front runner and an outsider, he’ll be the target of an unstoppable barrage of negative ads, media coverage and opposition camaigning.

There is a good probability that Anaya and AMLO will converge around the 35-40% neighborhood and battle for victory right down to the wire, but Anaya still has a number of challenges to cobble together a cohesive coalition. To make a sporting metaphor, AMLO won game 1 of the seven game series...but there are still six games to go.*

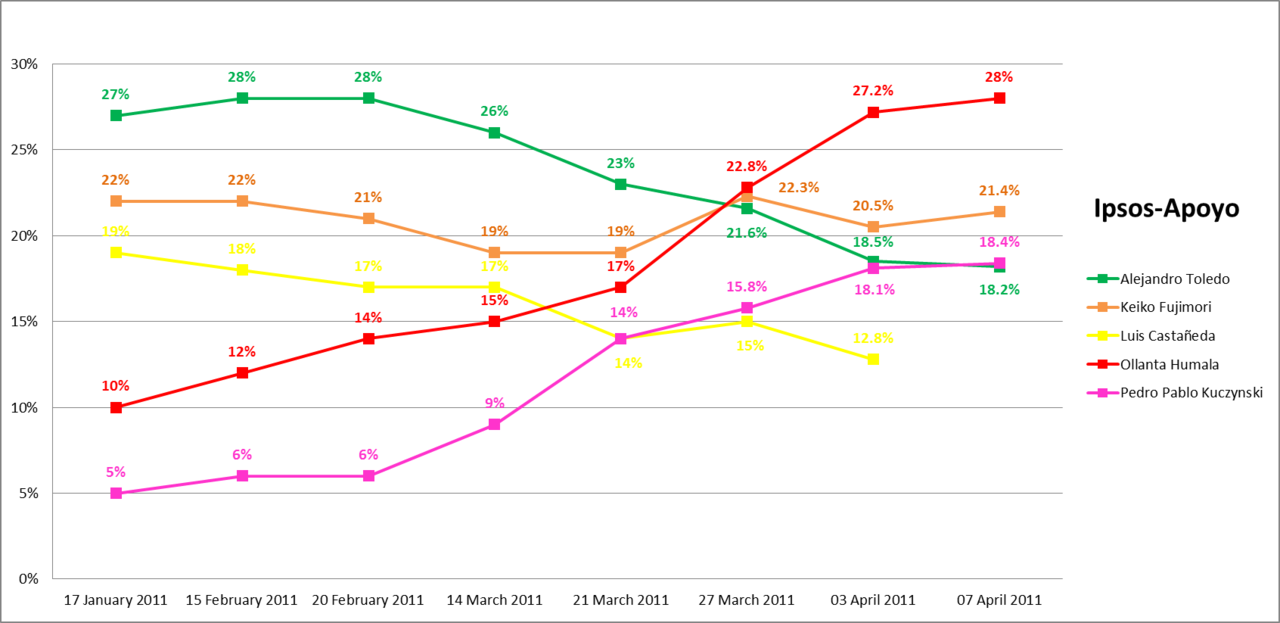

Now, what does the market think? First, to judge the potential impact of an AMLO victory, let’s look back to a similar situation in Peru, during their presidential election in 2011. Leftist candidate Olanta Humala was again running for president after narrowly losing the 2006 election to Alan Garcia.

I think the Humala analogy is a good one. Humala was a known quantity--and after losing the 2006 election, he spent years in the political mainstream softening his image. His politics were certainly of the left but it was unclear just how much of a leftist he would turn out to be--and he had made significant inroads among intellectuals and the middle class. Again, similar to AMLO, some are saying “he really won’t be that bad”, while others continue to see him as the reincarnation of Hugo Chavez--either way, both candidates were considered far more mainstream than in their first runs for office.

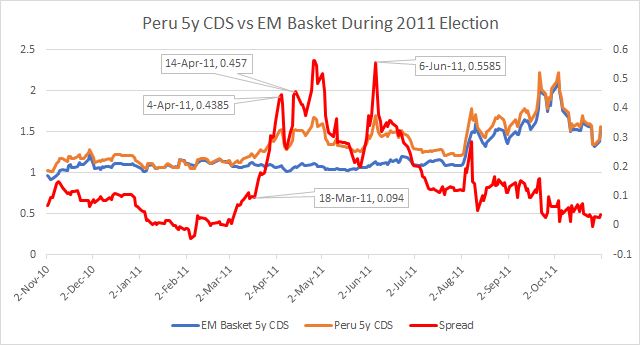

With that, let’s take a look at how Humala’s candidacy, and eventual victory, impacted credit risk in Peru. This is a chart of Peru 5y CDS vs. an equally weighted basket of Colombia, Chile, Mexico, South Africa and China in 2011 during the Peruvian presidential election campaign.

This shows the spread of Peru CDS vs the basket bobbed around zero, even as the campaign got into full swing ahead of the April 10th first round.

CDS spreads and the market at large only took notice when Humala made a strong run higher in the polls in late March, shortly after the March 18 data point I flagged above. The spread in the basket went from single digits to 44bps on April 4, and held around those levels after Humala decsively won the first round with 31% of the vote, compared to 24% for the second place center-right candidate, Keiko Fujimori.

In the runoff, polls between Humala and Fujimori were a dead heat right up until the election on June 5, which Humala won by about three points. As you can see in the first chart, the market had convinced itself that Fujimori was going to emerge victorious, despite the lack of supportive polling data.

The takeaway here is that an investment grade credit with a solid history of fiscal stability and orthodox policies can blow out by 40-50bps compared to its peers when a leftist candidate--a solid leftist, not a rank socialist--wins an election.

While the dynamics of campaigns in Peru 2011 and Mexico 2018 might be similar, AMLO isn’t surprising anyone like Humala did in March 2011. His lead in the polls has been relatively stable, 5-8 points since the other candidates became clear in November. Really nothing much has happened to move the needle since then, and you can see it in the spreads.

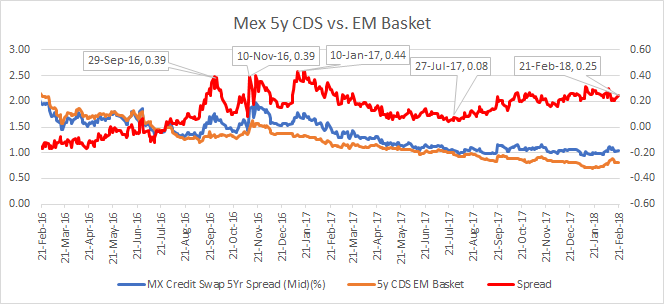

Mex bears a good resemblance to a basket of BBB industrials, and I have used that as the benchmark and potential upside in the case of a victory by Anaya (or in another dimension, Zavala or Meade).

This chart shows the levels at which these two spreads have traded over the past year or so. The Mex/BBB spread is around 25bps now, it traded flat back in September, when Mex was priced for perfection--and as wide at 55bps shortly after Trump’s victory.

On the downside, there are a few scenarios to how Mex 5y CDS could trade if AMLO wins. My first gut reaction was that it could trade flat to South Africa, which also ties out nicely with the wides vs. BBB industrials after the US election. That would be a huge move, but looking at the chart from Peru 2011, it might not be so outlandish, especially when you consider the positive flow/momentum in South Africa since Ramaphosa took over.

Maybe that’s too much? 10 tight to SOAF would be more conservative--but we also don’t know just what an AMLO victory would look like. Could he win a decisive victory by 8-9 points, and take a significant bloc, or even a plurality of Morena representatives with him into congress? A block big enough to build a coalition with PRD, PANAL, and some rebellious, disenfranchised union types in PRI? Sure, it could happen.

Mex/SOAF has been all over the map thanks to the political fireworks in South Africa. But even forgetting that, you can see here that the spread moved 84 bps between October 12, 2017 and January 10, 2018. So a move from -40bps to flat over the course of four months when the two credits are (theoretically) moving opposite directions isn’t out of the question.

I plugged some of these levels into a simple probability model based on the following assumptions:

- Mex can trade down to near flat to the BBB industrials index (which would also be flat to Peru and roughly 5bps tight to Indo) if Anaya wins,

- and that Mex can trade up to SOAF levels in an AMLO victory.

While we don’t know exactly what that victory would look like, flat to SOAF is a median approximation between a “weak AMLO” win (no power in congress, concilitory statements towards financial markets, encouraging signals about cabinet appointments and maintaining energy, education and labor reforms), and a “strong AMLO” win, where he carries big numbers into congress and has the political capital to push a more nationalist platform--one that might further complicate or even scuttle NAFTA negotiations.

Given those inputs, and taking some assumptions for carry/roll into account, I get a “AMLO wins” market-implied probability of 41%. If you toggle my assumptions a bit you can get something around 38% to 50%.

Given the above examples of how a political race can progress, I think the probability that AMLO wins is materially higher than that, probably closer to 60% (my personal opinion is that it is even higher than that, but I’m taking an objective attitude here). If I plugged in a Mex CDS spread to back into 60% probability, it would be about 10bps wider.

If you assumed 10bps wider is the right figure, but the upside is 10bps tight to SOAF rather than flat, the implied probability is 70%. Still not outlandish, in my opinion.

Bottom line, as the race picks up speed, even if AMLO doesn’t move much in the polls, there is good reason to believe Mex CDS could leak wider as investors hedge their significant exposures to an AMLO victory. That sets up an attractive risk/reward to buy Mex CDS outright in the case AMLO does indeed win, or if there is a surprise in the stalled NAFTA talks sometime between now and mid-summer.

Shawn

TeamMacroMan2@gmail.com

@EMInflationista

*In the big data/internet age, we have sports nerds that calculate this stuff. The theoretical probability if there is a 50% chance of winning each game is about 66%. In reality, the team that wins game one of a seven game series wins 68% of the time in the NHL, 64% of the time in MLB, and 76% of the time in the NBA. All in, the probability of winning a seven game series after winning game one is 71%.

25 comments

Click here for commentsGood question. Dunno. Here is Goldman's take for the end of year target for the S&P500. Personally I think its because its going to be faded.

Replyhttp://s346.photobucket.com/user/13579photo/library/

Those who sold XHB, trail the stop. Those who sold LOW, open a bottle of champagne ;)

ReplyLook at those pending home sales, ouch! We are in a bear market territory on most of the big builders now. This is not crash and burn yet but it's definitely getting ugly.

Powell did not help yesterday either. The minute he opened his mouth ITB and XHB took a dive. Never stopped since...

amps....confounding, even for you. nothing photoshop/qe couldn't fix.

ReplyUS breakevens took a dive today, along with oil prices, and the yield curve is flattening once more. Until (cough) US wages start to rise in a meaningful way, inflation expectations look to be primarily a function of fuel costs. As Dame Janet often reminded us, fuel costs may fluctuate and give rise to inflation spikes that are "transitory". Nevertheless, the Fed seems determined to hike and hike and hike again, ceasing perhaps only once the asset bubbles that are of its own making have been well and truly popped.

ReplyThis will be massively entertaining.

Nevertheless, the Fed seems determined to hike and hike and hike again, ceasing perhaps only once the asset bubbles that are of its own making have been well and truly popped.

ReplyOf course as rate hikes increase, Nasdaq just moves toward ATHs. Won't it be funny if the Fed proceeds to hike rates for the next 2 years and US equities increase 50%?

@leftback, posting something on this subject now--i think it argues for a steepener, even if the short-term impact of an aggressive hiking cycle are obviously to flatten the curve.

ReplyI like your article very much. If you are interested in the web, watch movies, online TV, online TV through the great IPTV system.

Replyboy585

The article is very useful. Try reading my article >> ข่าวฟุตบอล

ReplyPackers and Movers Pune Provide High Quality ***Household Shifting, Home/Office Relocation, Insurance, Packing, Loading, ###Car Transportation Service Pune and High experiences, Top Rated, Safe and Reliable, Best and Secure Packers and Movers Pune Team List. Get ✔✔✔Affordable Rate Charts and Compare Quotation and Save Money and Time. @ @ Packers and Movers Pune

Replyทดลองสล็อต pg เล่นฟรีทุกค่าย PG SLOT รองรับเล่นผ่านมือถือทุกระบบ ไม่ว่าจะเป็น IOS และก็ Android ผู้ใช้สามารถเล่นได้ในทุกเกมแบบไม่ต้องสมัครก่อนใครที่เว็บ PG-SLOT.GAME

ReplyFantastic post! Please keep sharing post like this. Thanks, have a good day.

ReplyHi there to every body, this webpage contains amazing and excellent data.

ReplyGreat post! We will be linking to this great post on our website. Keep it up

ReplyGreat delivery. Great arguments. Keep up the amazing spirit.

ReplyKeep up the good work. Check out more posts. Very good starting, goodjob

ReplyI have read this article; it is very informative and helpful for me. Great job you did... MM

ReplyThis is an excellent post I seen, thanks that you share it with us very good... MM

ReplyThank you ever so much for your blog post. Really thank you! Really Cool... MM

ReplyAppreciate you sharing, great article post. Much thanks again. Fantastic... MM

ReplyMuchos Gracias for your post. Really looking forward to read more. Want more... MM

Reply

Reply"The clarity of your writing is phenomenal! Everything is so easy to understand."

Reply"Your use of examples is spot-on. It really helped me understand the concept better."

Reply"You’ve mastered the art of making content both informative and enjoyable to read."

Reply"I love the way you build your arguments. It’s clear, logical, and persuasive."

Reply"Your attention to detail is amazing. Every part of this post adds something valuable."