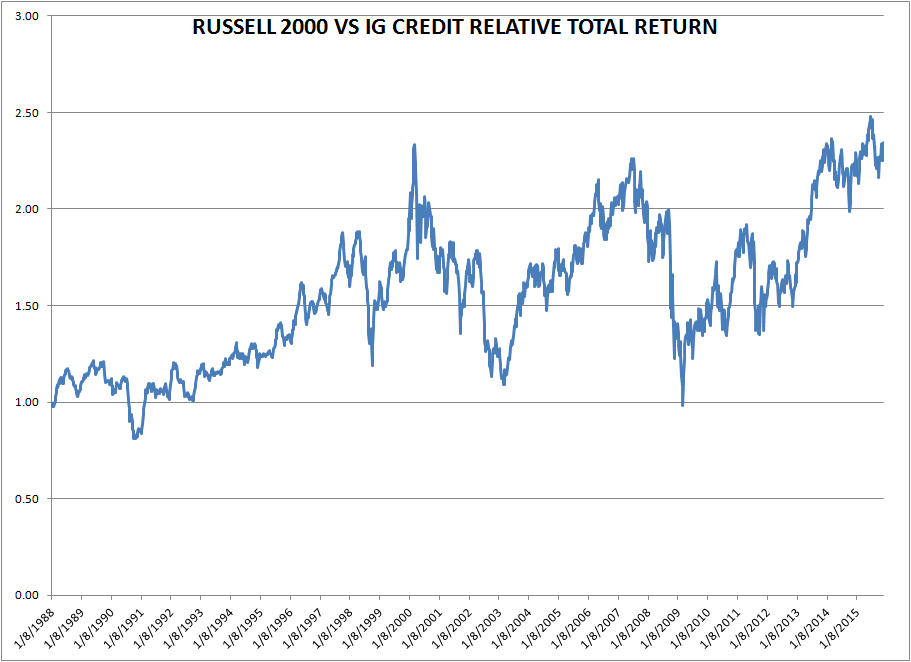

1) Further to yesterday's post, Macro Man did a little more digging on relative credit valuation. Small caps have been something of a red-headed stepchild for US equity markets this year, with the Russell 2000 down nearly 4% in price terms. If equity markets are moving to a quasi-late 90's analogue (narrow leadership, rest of the world in turmoil, commodities in the dump), that would clearly suggest more weakness ahead. Macro Man plotted a similar "relative value" indicator with his IG credit index to that posted yesterday, and while the shape is rather different the message is if anything more ominous:

As a relative value trade it certainly looks like there's something there and strips out at least some of the energy exposure present in high yield. To date, however, there hasn't been a solid Sharpe ratio trend in shorting the Russell to own IG. Interestingly, that has not been the case for high yield and energy. Owning high yield and shorting oil (at a ratio of 5-1 in terms of face amount) has actually been a pretty good trade for a number of years, delivering an information ratio in excess of 1 (the basket below is sized to target 5% vol):

It should be noted, however, that that 5-1 ratio is not vol-neutral; there is a decent beta to short oil. Sizing the trade to be vol-neutral would require a 10-1 ratio, and reduces the information ratio over the last year by 50%, though over the last four years the IR actually improves slightly.

2) China. Macro Man didn't have time or space to write about it yesterday, but oh dear. The hemorrhaging in FX reserves reignited last month, with only part of it attributable to the decline in non-dollar currencies....

Meanwhile, the trade account didn't really deliver the goods last month; imports were slightly stronger than expected but exports were weaker, leading to a $10 billion shortfall in the surplus versus expectations. Macro Man's real time China growth proxy looked like it was leveling off a few months ago, but no longer; it's now emulating one of those gold-medal Chinese divers:

Perhaps coincidentally- but probably not- PBOC has responded to the recent bout of euro strength by...marking USD/CNY higher; higher, in fact, than it's been since August 2011. While it's dangerous to pay the top in USD/CNH given their recent predilection for jamming the market lower to squeeze specs, it does seem like having a bit of long USD/CNH in the bottom of a drawer somewhere makes a lot of sense (Macro Man's earlier suggestion to take some profit notwithstanding.)

3) There's little holiday spirit at Morgan Stanley, where more job cuts were announced today, trimming a quarter of the global workforce in FICC (ie, macro) products. No doubt Elizabeth Warren and Mark Carney, the real life Dolores Umbridge and Dean Wormer of the modern political economy, will be delighted. Not quite as delighted, mind you, as they'll be when all financial institutions operate as utilities.

On an exclusive basis, Macro Man is pleased to present a clandestine look at a recent presentation on "the future of banking" given by Umbridge and Wormer at a recent meeting of the Financial Stability Board:

Alternative link here.

Edit: Non-US readers, try this one.

As a relative value trade it certainly looks like there's something there and strips out at least some of the energy exposure present in high yield. To date, however, there hasn't been a solid Sharpe ratio trend in shorting the Russell to own IG. Interestingly, that has not been the case for high yield and energy. Owning high yield and shorting oil (at a ratio of 5-1 in terms of face amount) has actually been a pretty good trade for a number of years, delivering an information ratio in excess of 1 (the basket below is sized to target 5% vol):

It should be noted, however, that that 5-1 ratio is not vol-neutral; there is a decent beta to short oil. Sizing the trade to be vol-neutral would require a 10-1 ratio, and reduces the information ratio over the last year by 50%, though over the last four years the IR actually improves slightly.

2) China. Macro Man didn't have time or space to write about it yesterday, but oh dear. The hemorrhaging in FX reserves reignited last month, with only part of it attributable to the decline in non-dollar currencies....

Meanwhile, the trade account didn't really deliver the goods last month; imports were slightly stronger than expected but exports were weaker, leading to a $10 billion shortfall in the surplus versus expectations. Macro Man's real time China growth proxy looked like it was leveling off a few months ago, but no longer; it's now emulating one of those gold-medal Chinese divers:

Perhaps coincidentally- but probably not- PBOC has responded to the recent bout of euro strength by...marking USD/CNY higher; higher, in fact, than it's been since August 2011. While it's dangerous to pay the top in USD/CNH given their recent predilection for jamming the market lower to squeeze specs, it does seem like having a bit of long USD/CNH in the bottom of a drawer somewhere makes a lot of sense (Macro Man's earlier suggestion to take some profit notwithstanding.)

3) There's little holiday spirit at Morgan Stanley, where more job cuts were announced today, trimming a quarter of the global workforce in FICC (ie, macro) products. No doubt Elizabeth Warren and Mark Carney, the real life Dolores Umbridge and Dean Wormer of the modern political economy, will be delighted. Not quite as delighted, mind you, as they'll be when all financial institutions operate as utilities.

On an exclusive basis, Macro Man is pleased to present a clandestine look at a recent presentation on "the future of banking" given by Umbridge and Wormer at a recent meeting of the Financial Stability Board:

Alternative link here.

Edit: Non-US readers, try this one.

17 comments

Click here for commentsThx for those thts MM - one would guess the credit vs oil trade will act more or less like an oil trade, since the credit tends to move rather spasmodically.

ReplyThe ECB gong show continues with the nowotny comments - given how oblivious EURUSD has been to the post ECB hail marys, I would hazard a guess that the year end long bucky trading carnage is far from over - in its future I see 1.11, which is a rather tame prognosis given its proclivities for monster moves lately.

The Yen has been mostly forgotten in all of this - will it do anything - ever? Next move up? or down?

In the meantime greek equities (referenced via GREK) have been on a slow death march for the last 3 months, and no one seems to have noticed - the last time there was a resolution to the greek drama, there was a massive move up - not sure if this is a dumpster diving opportunity, or a siren call to doom.

Its funny how the markets cares about china when it conveniently fits the narrative, but that is not all the time. Chinese Capital outflows are NOT a good thing for global markets, IMO as they are destabilizing to the current system. Short sing banks are a good play on that I think. But I'm curious to hear other thoughts

ReplyChina money supply numbers out tonight. But EM is still driven more by the oil story than that of china, day to day, at least, IMO

Rabobank to cut 9000 jobs - BBG

ReplyWho needs finance staff when we have Central Banks & HFT?

Any thoughts on Sensex? India still nursing the Modi loss hangover? I think its a very interesting market longer term. yes it got to consensus but Modi is smart, he does all the heavy lifting in the early years then presses the foot on the accelerator to get the economy buzzing by the elections in 2019.

ReplyAgree with WashedUp ... if the ECB wants to climb on a high horse, my bet is the market will oblige ... all the way to 1.20ish if need be!

ReplyI like India Abee, I just think it ran a little ahead of the Modi story ... it remains the most solid single EM story though. It's a CA deficit, that I am happy finance in other words. Investment still weak though! The cut in financial sector jobs is scary ... difficult to believe in 'wage pressure' stories when you hear those numbers.

@washedup,

ReplyGood question on JPY, I have the same question, and on CAD as well.

My 2 cents are since Japan now revised GDP to positive number, so they got out the recession using statistics, BOJ lost a major reason to do any further QE for now. They probably won't do anything before Fed meeting anyway.

Then CAD looks like to further depreciate due to 1)oil price back to pre-2005 level and 2) slowing US economy.

its about to get ugly. Carry trade liquidation and oil rejection after inventory numbers. Equities are a lame duck short here. Bye bye.

ReplyMM you mentioned SX5E support at 3280, well we are below that. Any thoughts?

If oil closes at lot lower on the day I assume lots of CTA's will pile in, if they arent already

2040 is key for SPX. If we are still in a bull market, it certainly looks a lot like a bear market price action to me. Calendar and positioning doesn't help a lot: most asset managers are probably still OW equities, and EMU equities in particular, and will maybe decide to start the new year more neutral .... i. e. some selling going through.

ReplyMyself still UW from early October (80% of the benchmark), suffered a lot, relatively speaking, and now back in shape. Will probably cover some at around 3180 for calendar purposes, but overall feeling not many reasons to buy equities.

Agree with AL and MM. If this is a bull market, then it's a pretty ugly one, with all kinds of credit and equity indexes having clearly rolled over. Yet there will be more sharp squeezes and rip-roaring rallies before one day something causes the bottom to drop out, perhaps some significant high yield credit defaults that force some liquidation in other markets.

ReplyCharts for US fixed income are equivocal in some cases but can still be read as a continuation of the bull market in govies that apparently never ends. You can certainly extrapolate to a 1% 10y and a 2% 30y, and it's happened before, not only in Japan but also now in Germany. This is the Gary Shilling position, and you can get Gundlach and LB on that train quite easily.

There just doesn't seem to be anything preventing oil from falling further. MM made the point about supply, storage is full at Cushing and production hasn't been cut back even in the US as much as had been expected. A mild winter and this can just go lower and lower and lower. Not very inflationary, as we have pointed out here many times, and it's bullish for bonds as it locks in lower headline inflation numbers for months ahead.

We are still predicting a rebound for REITs, EMs and some commodities in 2016. The dollar may well have peaked for the time being. What else ya got, Bucky? Just Dame Janet with 25 bps?? Pffttt....

with immense carnage in commodities (first warning) throughout the year, a sell off in credit later on (second warning) and classic flight to safety onto USD (cf. last financial crisis), with EM equities decimated, EU shares printing lower highs and lower lows, and yes, Greece back to hell (and oblivion) it still puzzles me that people would expect US equities to be UP on such annus horribilis

Replyamid such investment environment and calls for caution folks who did not sell at 2100 4th attempt because they hoped Santa would handle them money (again) deserve every bit of pain. Have you noticed the silence of the lambs i.e. FM and all his anonymous. Never believed in Santa but looking to mount the biggest short position since 2007 at year end

agree with nico- been harping here about credit and equities (US esp) have a lot of catching up to do....

Replygiven crazy algo action and illiquidity keep some teeny puts handy....might not be able to sell em but will be able to lean against and buy if it gets really crap( though like i have said before what spoos are doing with a 2 handle is beyond me- expecting last octs lows to be cracked between now and march)

The S&P 500 chart looks sh't for sure, but I still think new highs are in store in Q1. Can't and won't argue with price though, and the ECB seems bend hell on huffing and puffing. Not liking the smell at the moment, that's for sure.

ReplyCV/anon - who knows what q1 brings, but for new highs in spoos you need tech to do the heavy lifting - a 30-40% further rally in FANG would do it, but the environment doesn't seem particularly ripe for that kind of an exuberant push a la q1 2000. Of course, I could have made the same statement 30% ago!

ReplyIt's a really tough call - I'd firmly be in the bear camp if nasser broke down conclusively instead of acting like a toddler on caffeine.

Hmm, Washed ... if China doesn't implode and the Fed delivers a dovish hike EM and its derivatives could take over the leadership board and push the indices higher. Also, a lot of dollar strength has been priced into key U.S. companies (PG etc ... they could go on a run if bucky slows its rise slightly).

ReplyRotate them sectors! ;)

But I concede, that this only happens in the best of worlds ... 40% cash up here in Retail R'us LLP, 10% Gold and even some ags too. Not donning the kevlar in FANG here! ;)

"Have you noticed the silence of the lambs i.e. FM and all his anonymous"

ReplyNico, excellent call on EU equities, but as a reminder, you advised the "FM anon" to close out Dax near previous highs:

Anon 9:12 said...

@Nico - You make a good point. I closed my entire line in Dax following the poor reaction to PMI data this morning (avg price 11375 FDAX Z5). I am tempted to short some here too, but will hold fire for now.

December 1, 2015 at 10:27 AM

I would thus regard "the silence of the lambs" as participants being on the sidelines pre-FOMC rather than any contrarian sentiment indicator.

two thumbs up

ReplyRight.. ok.. it is late in at night and i'm a little wirse for wear. 2am US time.. where i am..

Reply1. Whats thd ratio to produce flat returns re oil vs HY

2. China. Remember when this whole thing was triggered by China deval in Aug and that was the cause for chinadevalmania? Or should i say chinadevalbollox? China deval was as hinted back then a complete red herring. China slowdown.retrenchment.econoswitch ok.. but deval fears ahhmm.

3. Err what was 3.. ah yes. I really dont know how much Ineed to repeat this having said it copious times as the author of this space and as author of my new space... so again.. society and government wiĺl not be happy until banks are returned to the status of social utilitues such as post offices. Until then keep expecting reg vs social blah blah to continue. Banks snd their employees are fkd. Get out while you can Oh banktraders and salesfolk before you are algoed or retailed. GAME OVER.

Was there a 4th? ..ah yes. Sum up the above and apply Parkinson's law to finance. The amount of time available in redundancy will be filled with the application of new skills which will make you look back on finance and ask "why did I ever think what I stressed about was so important" Actually let's call that Polemic's law.

5.. tgere was no 5. But to cover all bases. It is 2am NY timr and I have cured my jetlag with ETOH to the point I ahould be in China. So I sm not going to spell check any of that.