And so here we are.

This blog is more than nine years old, and has never had the pleasure of commenting upon a Federal Reserve rate hike. While that damning statistic says much about the world we live in, it also says something about the institution and its biases over the last several years. Regardless, after 493 weeks (nearly double the previous record) we should all finally have a hike to talk about today.

Given that this is quite possibly the most anticipated rate hike in human history, there is little that Macro Man wishes to add to the veritable Everest of previews, thought pieces, moans, and cheers that have inundated anyone with even a cursory interest in economics or markets over the past days, weeks, and months.

Instead, he will leave you with some data to put the current situation, and perhaps the future, into context.

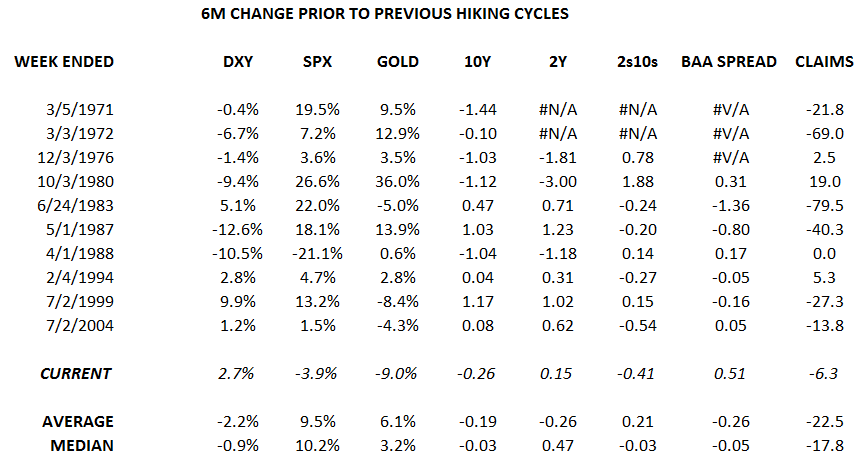

Table 1 displays the net change in several variables over the six months preceding every tightening cycle in your author's lifetime. (A "tightening cycle" was actually quite ill-defined before the 1990's; Macro Man has been quite conservative in his definition of a cycle.)

Table 2 displays the six month change in the same variables after the commencement of a new tightening cycle.

Table 2 displays the six month change in the same variables after the commencement of a new tightening cycle.

There are a few points worth noting:

There are a few points worth noting:

* Over the last three cycles, the USD strengthened into a rate hike and weakened after it. The DXY has once again strengthened into this one.

* This is only the second time that stocks have fallen going into a tightening cycle. The other was the rebound hikes five months after the '87 crash. On average, stocks are flat for six months after a new cycle begins.

* This is the worst-ever performance for gold heading into a hiking cycle.

* This is only the second time in the last 35 years that 10y yields have fallen in the six months heading into a rate hiking cycle. The last cycle was the only one to see 10y yields decline in the six months after tightening began.

* Perhaps not coincidentally, the last cycle also demonstrated the largest flattening in the 2-10 curve before the hike. The curve has flattened nearly as much this time around. After tightening begins, the curve typically flattens more.

* This has been the worst performance for credit in the run-up to a tightening cycle in your author's lifetime- or at least as far back as the data goes. Interestingly, spreads have tightened after the start of a tightening cycle on six of the seven occasions for which we have data.

* Labor markets (proxied by claims data) tend to perform as well after a tightening as before. You probably don't need Macro Man to tell you that if the labor market breaks the pattern, the Fed will abandon its tightening.

All in, this looks like a fairly atypical run-up to a new cycle...which suggests that the follow-through could also be atypical. Of course, there's a selection bias at work here; rate hikes that are swiftly unwound don't get counted as cycles. Macro Man still thinks that this will turn out to be a cycle...but confesses that he would have been more confident in that view has that pulled their finger out 12-18 months earlier.

Good luck, and we'll see you on the other side.

This blog is more than nine years old, and has never had the pleasure of commenting upon a Federal Reserve rate hike. While that damning statistic says much about the world we live in, it also says something about the institution and its biases over the last several years. Regardless, after 493 weeks (nearly double the previous record) we should all finally have a hike to talk about today.

Given that this is quite possibly the most anticipated rate hike in human history, there is little that Macro Man wishes to add to the veritable Everest of previews, thought pieces, moans, and cheers that have inundated anyone with even a cursory interest in economics or markets over the past days, weeks, and months.

Instead, he will leave you with some data to put the current situation, and perhaps the future, into context.

Table 1 displays the net change in several variables over the six months preceding every tightening cycle in your author's lifetime. (A "tightening cycle" was actually quite ill-defined before the 1990's; Macro Man has been quite conservative in his definition of a cycle.)

* Over the last three cycles, the USD strengthened into a rate hike and weakened after it. The DXY has once again strengthened into this one.

* This is only the second time that stocks have fallen going into a tightening cycle. The other was the rebound hikes five months after the '87 crash. On average, stocks are flat for six months after a new cycle begins.

* This is the worst-ever performance for gold heading into a hiking cycle.

* This is only the second time in the last 35 years that 10y yields have fallen in the six months heading into a rate hiking cycle. The last cycle was the only one to see 10y yields decline in the six months after tightening began.

* Perhaps not coincidentally, the last cycle also demonstrated the largest flattening in the 2-10 curve before the hike. The curve has flattened nearly as much this time around. After tightening begins, the curve typically flattens more.

* This has been the worst performance for credit in the run-up to a tightening cycle in your author's lifetime- or at least as far back as the data goes. Interestingly, spreads have tightened after the start of a tightening cycle on six of the seven occasions for which we have data.

* Labor markets (proxied by claims data) tend to perform as well after a tightening as before. You probably don't need Macro Man to tell you that if the labor market breaks the pattern, the Fed will abandon its tightening.

All in, this looks like a fairly atypical run-up to a new cycle...which suggests that the follow-through could also be atypical. Of course, there's a selection bias at work here; rate hikes that are swiftly unwound don't get counted as cycles. Macro Man still thinks that this will turn out to be a cycle...but confesses that he would have been more confident in that view has that pulled their finger out 12-18 months earlier.

Good luck, and we'll see you on the other side.

40 comments

Click here for commentsFT: this hike will probably be described in history books has the biggest blunder ever by the FED (on par with the easing in the late 1920's to accommodate the british treasury) .

ReplyThey should have hiked more than a year ago and probably should be ready to ease in Q1 of next year.

I think that once the hike noise is behind us and the dust hit back the ground we will see within 2 to 3 months:

1) equities lower by 10 to 15%

2) 10 y lower by 20 to 25 bp

3) EUR / USD above 1.16

4) HYG below 70

5) Gold above 1200

....

Now, having said that, one can't exclude a marginal new high by the spooz. As an example of equity exuberance I always like to mention the high post summer of 2007.

BUY GAMMA

LOL you guys read too much ZH. Equities have been rallying for the past few sessions and are rallying again this morning. Won't it be funny if the FOMC hikes a few times and stocks make new all time highs? Frankly I can see it happening.

ReplyFT @ anon 10:39

Replyequities might have rallied for the past few sessions as you said but are basically unch in over a year

I fail to see the connection with ZH as the rare times I have a look for a good laugh they seemed to always call for a crash, gold at 5000, teotwawki and WWIII .....

At Anon 11:06

ReplyWell, if Washington doesn't find a way to flush the neocon vermin out of its foreign policy establishment, WWIII is not an unlikely outcome.

Two words: backward guidance.

ReplyThat's when a CB let's it be known that it now realizes where in the rate cycle they should be by now and jump directly to that phase with the benefit of perfect hindsight.

For example in today's meeting they move rates +250 bp. Then they make the statement that they don't know what will happen until it happens and that the markets should look forward to more backwards guidance once everything has happened.

This should grab the initiative back from the markets and prevents complacency from settling in, at the cost of some market volatility.

(Although this probably won't happen, I do think Fed has the twice in a cycle opportunity now to pretend it has some control and hike 25 bp + some really tough talk OR even 50 and a promise never to do that again.)

Not sure The Fed looks at labor and wage metrics the way they should be...

Replyhttps://research.stlouisfed.org/fred2/graph/?g=2VCD

https://research.stlouisfed.org/fred2/graph/?g=2VCE

The cake that is being served in this era of growing neo-feudalism tastes great though.

MM - IMO, the interesting wrinkles in this tightening cycle are:

Reply1. When did it begin? Wasn't it the end of QE purchases last year that heralded tightening, was followed by market induced deflation, and this move can therefore be seen as the equivalent of the 3rd or 4th one in a 'normal' tightening cycle?

2. What matters to risky assets? Haven't the previous risk on moves into a few quarters of hikes been a reflection of an economy that has ostensibly been quite strong even as people puzzled over the signal (that later proved prescient) being sent by yield curve flattening? Is it fair to say we don't have that this time?

3. Are we still in a world where only the Fed matters? What beta can be ascribed to ECB and BoJ - if the Fed hikes but these others continue or expand their QEs, should it be counted as half a normal hike? Isn't their QE not the same as Fed QE anyway because of the daily nature of Fed purchases as opposed to their more sporadic, liquidity challenged ventures?

Good luck everyone, could be an interesting few days - expect extra wide 2 ways on everything you buy and sell after the decision!

We have a little bit of long JPY today, nobody fancies that much but it is the pain trade for a lot of people. USDJPY looks kind of toppy here, to be honest. We are not seeing the weakness in USTs that we had expected this morning. Perhaps it will develop as the day progresses and Bucky makes a little run.

ReplyTo be honest the people calling for 50 or 25 + Hawk Talk are frankly delusional. This is a piss weak economy at the moment with manufacturing numbers in recession. Dame Janet needs DX > 100 like a hole in the head. La Paloma Blanca will stick to the script. 25 + softer dot plot. Buh-bye Bucky, at least for the next month or two.

It's going to be a bit volatile this afternoon, he said, laughing.

how 'bout that bitcoin. Regarding gold weakness I can't help but think that bitcoin is in many ways a better gold.

ReplyThis hike is crazy. IOER is crazy. I'm old and confused and none of this makes sense to me. Excess reserves are a problem, not something that should be rewarded with higher rates. Surprisingly noone consulted me but the tightening should come from a gradual reduction in balance sheet and reserves. I see these 2 as the elephant in the room that the fed continues to ignore.

In light of my confusion and in an unsporting effort to protect my yearly marks I'm positioned as defensively as I can be.

@Anon 1:08

ReplyAverage and median wage growth is quite healthy -

https://research.stlouisfed.org/fred2/graph/?g=2VJO

https://research.stlouisfed.org/fred2/graph/?g=2VJW

And full-time employment growth has been about as good as it gets ...

https://research.stlouisfed.org/fred2/graph/?g=2VK7

Mr. T,

ReplyThe Fed funds market is a closed system (determined by Fed's B/S), so with excess reserves being present due to QE, IOER is necessary if you want to lift Fed Funds Rate (or you should drain all reserves via reverse repo facility, but that seems to cumbersome). So in the short term it's impossible to lift off without increasing IOER.

We are long some TLT calls here at the Hammock. Just for fun. The Kevlar gloves are in the drawer, but we still think they will be deployed in the next week or so, perhaps in the EM, energy, REIT or even credit space, we will see. We have no position in Spoos at all, so the anions can just call each other names all day.

ReplyGood luck to all punters, brave and timid alike. We would be counted on the timid [or even disinterested] side today, it's been a decent year on a relative to the benchmark basis and we are already Parking The Bus here.

Anon 4:04PM

ReplyUS Real Average Weekly Earnings printed at a measly 1.6% YoY

Average wage growth is only 2.3% YoY. And real median household income is still below pre-recession levels.

Booger, how are you feeling on AUDCAD, its going bananas. I'm trying to look for uncorrelated trades here.

ReplyAs for the first comment, the end of the world is comming for equities and markets. Well it depends on Oil! Oil is driving the spread between momentum names & value. Get oil to bounce and the stock market breadth can improve and we are off to the races. On the otherside, if oil plummets and Nasdaq rolls over, I'm with you.

I think equities find a way to rally. Monetary tightening is not something that works right away, it takes time. Perhaps many have forgotten that and I feel like markets will frustrate those who dont remember that. Good luck.

LB I am with you with the JPY, nice call

@Abee,

ReplyWhen you look at AUDCAD, it totally is moved by CAD, which might follow its pattern for the past three years. If the pattern holds, then USDCAD is likely to go to 1.45-1.5, not that unthinkable if you go back to 2002-2005 period.

And, while we all agree that this IS the first rate raise in this cycle. It might not be comparable with previous cycles due to the 3 QEs. The end of QE3 IMO is equivalent to the previous first rate raises. And equity always had postive returns after the 1st rate raises in old times, which had already been here: after QE3 we have several all time highs already and today it might be the same as the 2nd or the 3rd rate raises in old monetary cycles.

If this is true, then the end of the equity bull cycle is much closer than we previously thought.

"Good luck to all punters, brave and timid alike. We would be counted on the timid [or even disinterested] side today,"

ReplyIndeed, not doing anything here either, just watching the show. Have fun everyone!

Well, as I stated a couple of weeks ago, I am waiting for equities to break 17k..when they do I will put as much as I can reasonably risk on the market continuing to go down. Until 17k, I will do nothing, as Lucy has controlled the football every time heretofore. I am encouraged that the yield on treasuries is going up the last few days, as that should help my thesis. BUT, I am trying not to think about where the market Should Go, I have merely thought this out, and will have enough willpower not to make a mistake too early.

Reply..My 2 cents as a non-professional investor..

AUDCAD = no reason why multi-ressources Australia shouldn't keep or even increase its premium over one-trick pony Canada (oil)

ReplyCanada is fried - just booked the ski tickets, cheap like dust

Bruce

Replyinteresting input on trading style: you value your mental comfort at precisely 550 Dow points, not willing to suffer snafuesque price action until 17k is broken with momentum. 17k WILL be broken, but you are 'paying' (i.e. forgoing) 550 points today to wait.

i operate completely differently - on the same view as yours (17k will be broken) - 'pocketing' the extra 550 points today with the risk a lot of heat on a squeeze

personally throughout the years i found out the pain of getting in too early is never greater than the frustration of being too cautious and left out in a game that you clearly predicted. So I price frustration at a greater mental price than actual market loss - not sure if this is mentioned in any trading traité, trading style is crucial to ponder and never debated enough imho

Anon 5:08pm here

Reply@Nico Great comment on trading psychology. I think everyone has different mental set dealing with these uncertainties.

And on AUDCAD, I couldn't say it better.

Nico,

ReplyI look at the markets this year, and this is just too choppy for a non-pro like me. I will share with you that back in the tech bubble, (as Lefty already knows) I invested every nickel I had in techs and sold in April, 2000. I made >400% in 18 months, and got out at the top. I do believe in bigger bets, but 1998-2000 changed my entire life, so I have not had to make bets of that massive risk profile.

I look at the news behind the markets, and the best way I parse that is that equities should go down, especially here in the US with a stronger dollar and global weakness if liquidity dries up. I see on CNBC that the Fed suggests 1.4% Fed Funds rate by the end of the year. Still fits my thesis. Unlike you I don't mind being patient (frustrated in your terms) as long as I make money.

I don't care if somebody beats me for half a year. At this point in my life, investing has become more about how can I maximize the bet at the least risk. I was probably the poorest kid in my high school class. Now I am not. I try to make the bet as close to a sure thing as I can. That translates into patience...

My 2 cents...

congrats Bruce

Replyforecast places rates at 1.5% at the end of 2016 and 4% at the end of 2018 - so plenty of room for repricing discounted flows on equities

so this is dovish???with the frigging dot plot twice the market rates??wtf is gradual?

ReplyLOL you guys read too much ZH. Equities have been rallying for the past few sessions and are rallying again this morning. Won't it be funny if the FOMC hikes a few times and stocks make new all time highs? Frankly I can see it happening.

ReplyDecember 16, 2015 at 10:39 AM

et voila... we are on our way...

I promise this will be my last IOER rant, I can tell noone cares. Yellen says balance sheet stays until rate normalization done. Whats that - 2%? IOER with 2% rates is ~$90B/year in transfer payments from US taxpayer to moneycenter banks. Thats like 8% of the total US discretionary budget - greater than education, veterans benefits etc. I don't see how this mechanism scales at all.

ReplyAnd then what will it look like when there is a financial shock? Dropping rates on IOER would mean less cashflow for banks. Compare this to previous mechanism that would provide immediate relief to banks.

Just looks like a huge gift to NIM's and whatnot.

These questions are brutal...everyone trying to get her to be super dovish. One wonders if the fungi that pop up every time stocks rise 50 bps higher are, in fact, all Fedwatchers...

ReplySP500 up over +1% on Fed rate hike - looks like the shorts here were badly, badly wrong...

ReplyLMAO on the questions - they can all be replaced by 'Hey - can you tell us something optimistic? Pleeeeeeaaaase???'

Replynew year resolution for MM: no more anonymous posting

ReplyBruce, what will you do if Dow breaks 18k?

ReplyI liked the one question they had on inflation expectations. The Fed has been consistently wrong on them (along with lots of others) and not sure how they see them stabilizing next year. But anyways they dont seem to care.

HYG has now had 2 days of rallies, after a brutal sell off. In the past this was a reliable sign of a bottom for a swing trade at least. Not saying it is set in stone, especially if oil makes new lows, but something to keep in mind.

new year resolution for equity shorts: go long ;)

Replystill waiting for Dec 28-31st window to go short

Reply4% rate in 2018 has nothing against Santa

EURUSD remarkaly meh today

Nic G No more anonymous posting? OK, so who are you?

ReplyHave to admire Funny Money/anon as he persists in baiting the "shorts". Goes quiet when we erase ecb gains from Dec all the way back to Oct 22nd. As if the "shorts" don't know when to cover or think the market could possibly rally.

ReplyFED must feel oretty happy with itself this evening. About as uneventful as they could have wished. At least trading economic data will be more interesting in the near future. Yellen discussing an oil base was laughable. She has a number, even though she is surprised how it went from $60 to $36, transitory.

There is no incentive to get short here aside from Russia /Turkey pot shots.

Do MM contributors think 2016 will throw up as many events as 2015?

S&P up <1% YTD for 2015. Is that better than the mattress? Will 2016 throw a repeat?

ReplyFunny, listening to the JBTFD'ers I'd have thought it was up 35% or so....

ReplyAnon 10:14

Replypick up an alias at least and we can introduce ourselves. It is plenty rude and despicably cowardly to engage people on this forum behind an anonymous mask, thus it makes you completely untraceable.

you gotta love it when an anon claims they have made the right call one hour one day or one month ago. You could pick any anonymous market call and claim it when it worked c'mon it's bullcrap

my real name is actually Nico i hope you find it sexy now you can go wank your anonymous self.

Nico G "wank your anonymous self."

ReplyYou have a filthy mind sir.

now back to market - some common sense from Charles Hugh Smith

Reply> There’s no upside left–not just in the real economy, but in jobs, politics or policy tweaks. Yes, there will be huge relief rallies in the stock market–relief that the Fed is still omnipotent, that the Fed didn’t destroy the world by withdrawing liquidity, etc., etc., etc.–but in terms of sales and profits, there’s no upside left: an increasingly nervous upper middle class is reining in profligate spending, while everyone below the top 10% is running out of credit cards, student loans, etc. to tap.

Whatever surplus the real economy generated has been skimmed by financiers, lenders and the central state. Stock buybacks have boosted the wealth of corporate managers and institutional owners while creating zero jobs; lenders have feasted on high-interest credit cards, federally backed student loans and subprime auto loans that are immediately spun off to credulous suckers (Widows and Orphans Fund of Norway, et al.) as high-yield securitized debt.

Anyone working for Corporate America or government has little upside but plenty of downside: bonuses are being slashed, divisions closed, sold off or privatized in the case of government, all to cut costs.

State and local pension funds, bloated by seven years of speculative frenzy, are about to start bleeding from every orifice as reality and risk intrude on the central banks’ fantasy of never-ending asset bubbles.

From CHS all I see is plenty of opinion couched in the usual mildly derogatory terms, but none of it backed up with data. Could he be right? Who knows. Could he be wrong? Who knows. Has he got any real argument ? Now on that question I can certainly say ,none that is evident.

Reply