TMM have recently been bemused by the strength of equities and industrial metals in the face of some pretty dire developments in the Middle East and amused by the antics of Charlie Sheen. On the face of it, they do look rather similar in some respects: both hopped up and energized on forces known (QE and being able to date two women in their early 20s) and unknown (how China maintains an entirely investment driven economy and for Mr Sheen’s secret ingredient check TMZ). However, every silver lining has a cloud and TMM are growing increasingly concerned about what $100+ oil means for US consumers and what the National People’s Congress means for Chinese growth.

Let’s start with something everyone agrees on: $200 oil would put us into a double dip and then some. How odd it is that out of the money equity vols seem to be a long way from out of the money crude vols, which have gone all bid out all the way along the curve. It is nice to see that investors have picked up on the fact that middle class discontent in the Middle East is about as well contained as the collapse of the shadow banking system circa 2007. TMM are not so sure about being long oil here as a fair bit of risk is priced in even out to December now, but one-step-removed trades like being long energy assets in good jurisdictions or ones with high costs (Hellllooooooo Alberta….) do seem to have less downside despite a good run –PetroCanada Suncor PE (light blue) and stock price (dark blue) below. Suffice to say it doesn’t look that crazy to TMM, given that Saudi Arabia blowing up will make this the mother of all cash cows and it has only about 25% downside on valuation assuming all is well. It’s certainly cheaper than crude vol!

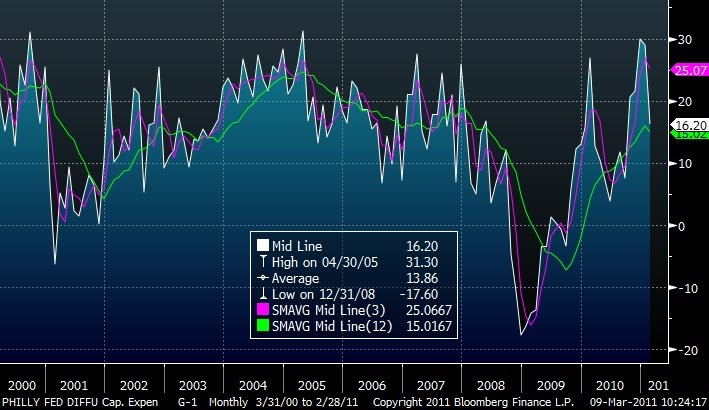

That of course assumes that it does not kill US consumer spending which has been a fairly important part of the recovery and will be more so once the government gets serious about deficit reduction. The problem is that this is coming as the 100% depreciation allowance for capex for 2011 expires and 6 month ahead capex intentions from Philly Fed seem to be rolling over (see below). Watch this space – channel stuffing can be driven by tax policy too. Without much “I” or “C” and assuming “G” gets under control, GDP is going to have a tough time recovering, which makes you wonder whether the deflation trade has breathed its last.

Which brings us to the subject of China’s 5 year plan and recent macroprudential changes. The big change in macroprudential regulation is to move from loan quotas, i.e. window guidance to bona fide M2 targets. This is a subtle distinction, because it covers not just bank lending, but general credit creation: bonds, commercial paper, and those trust loan structures that were all the rage for anyone who wanted to fund a massively loss-making local government investment vehicle. While this sounds all well and good, TMM are well aware that loans are still under the CBRC and trust loans are somewhat CBRC covered, as many are originated by banks, but many are also securitized and thus would come under the purview of the CSRC. Similarly, the bond market is pretty tightly regulated, but is under the CSRC, so TMM knowing a little about regulatory fiefdoms in emerging markets are wondering how well this will all be implemented. Time will tell, but we are more than a bit skeptical at this point in time. In the meantime though, TMM are noting that the channel checks were right and vehicle sales are slowing sharply in China – cue a run of people’s stops in Platinum and Palladium.

Which gets us onto the Five Year Plan and let's just say that one thing is abundantly clear: China’s going to have an awful lot of electric cars sooner rather than later. As a belated response to the 2008 oil spike and current events China is moving aggressively to roll out electric cars and reduce its dependence on oil. This is not particularly good for Platinum and Palladium, as we discussed previously here. While China is planning on continued urbanization (and iron demand along with it), growth is expected to be on the order of 7-8% vs mid teens growth in demand seen previously. Given some of the aggressive capex programs in the mining majors TMM feel that it might be high time for a fade of recent metals prices with the US seemingly close to rolling over, a large supply response coming along in iron and copper and prevailing tight policy in EM. Iron ore has come off, since it figured in our non-predictions, but TMM feel that now might be a good time to take a swipe at copper too. Lead in particular looks rich to TMM – according to some fairly exhaustive work done recently we are looking at the entire China E-bike battery market going to lithium over the next 3-5 years. That's about 45% of world lead demand. Gulp. There’s nothing quite so obsolete as an obsolete technology.

Pulling together all these micro strands TMM feel that the long commods game has likely seen its best days for the year until policy loosens up in EM. Or, we could take some inspiration from Mr Sheen and say, “if you’re still in commodities, you’re with the trolls”.

The only other alternative is that this run breaks just about every historical pattern TMM know and, even though we know that is exactly what some are hoping for, TMM just can’t see it.

Let’s start with something everyone agrees on: $200 oil would put us into a double dip and then some. How odd it is that out of the money equity vols seem to be a long way from out of the money crude vols, which have gone all bid out all the way along the curve. It is nice to see that investors have picked up on the fact that middle class discontent in the Middle East is about as well contained as the collapse of the shadow banking system circa 2007. TMM are not so sure about being long oil here as a fair bit of risk is priced in even out to December now, but one-step-removed trades like being long energy assets in good jurisdictions or ones with high costs (Hellllooooooo Alberta….) do seem to have less downside despite a good run –

That of course assumes that it does not kill US consumer spending which has been a fairly important part of the recovery and will be more so once the government gets serious about deficit reduction. The problem is that this is coming as the 100% depreciation allowance for capex for 2011 expires and 6 month ahead capex intentions from Philly Fed seem to be rolling over (see below). Watch this space – channel stuffing can be driven by tax policy too. Without much “I” or “C” and assuming “G” gets under control, GDP is going to have a tough time recovering, which makes you wonder whether the deflation trade has breathed its last.

Which brings us to the subject of China’s 5 year plan and recent macroprudential changes. The big change in macroprudential regulation is to move from loan quotas, i.e. window guidance to bona fide M2 targets. This is a subtle distinction, because it covers not just bank lending, but general credit creation: bonds, commercial paper, and those trust loan structures that were all the rage for anyone who wanted to fund a massively loss-making local government investment vehicle. While this sounds all well and good, TMM are well aware that loans are still under the CBRC and trust loans are somewhat CBRC covered, as many are originated by banks, but many are also securitized and thus would come under the purview of the CSRC. Similarly, the bond market is pretty tightly regulated, but is under the CSRC, so TMM knowing a little about regulatory fiefdoms in emerging markets are wondering how well this will all be implemented. Time will tell, but we are more than a bit skeptical at this point in time. In the meantime though, TMM are noting that the channel checks were right and vehicle sales are slowing sharply in China – cue a run of people’s stops in Platinum and Palladium.

Which gets us onto the Five Year Plan and let's just say that one thing is abundantly clear: China’s going to have an awful lot of electric cars sooner rather than later. As a belated response to the 2008 oil spike and current events China is moving aggressively to roll out electric cars and reduce its dependence on oil. This is not particularly good for Platinum and Palladium, as we discussed previously here. While China is planning on continued urbanization (and iron demand along with it), growth is expected to be on the order of 7-8% vs mid teens growth in demand seen previously. Given some of the aggressive capex programs in the mining majors TMM feel that it might be high time for a fade of recent metals prices with the US seemingly close to rolling over, a large supply response coming along in iron and copper and prevailing tight policy in EM. Iron ore has come off, since it figured in our non-predictions, but TMM feel that now might be a good time to take a swipe at copper too. Lead in particular looks rich to TMM – according to some fairly exhaustive work done recently we are looking at the entire China E-bike battery market going to lithium over the next 3-5 years. That's about 45% of world lead demand. Gulp. There’s nothing quite so obsolete as an obsolete technology.

Pulling together all these micro strands TMM feel that the long commods game has likely seen its best days for the year until policy loosens up in EM. Or, we could take some inspiration from Mr Sheen and say, “if you’re still in commodities, you’re with the trolls”.

The only other alternative is that this run breaks just about every historical pattern TMM know and, even though we know that is exactly what some are hoping for, TMM just can’t see it.

14 comments

Click here for commentsGlad to see TMM is also long bi-winning jokes

Replyvery well thought out at a number of levels ... none of which seems very positive for AUD ...

Reply1255 GMT [Dow Jones] U.K. January trade data look good, but they were distorted by the weather, says Alen Mattich in Wednesday's Money Talks column. The longer-term trend remains grim, argues Mattich. Manufacturing is too small a part of the economy for sterling's 25% devaluation in 2007 to make much difference, he says. Either the U.K. needs another big devaluation or consumption needs to be crushed in order to get rid of the deficit, Mattich says. (alen.mattich@dowjones.com)

ReplyI'm tired of hearing that tightening in EM will drive commodities lower. The position of EM's given just about every fundamental measure suggests tightening is possible and that they are in a lot better shape than the US given the complete mess it's made of it's balance sheet. If we want to debate where commodity prices go it needs to involve an analysis of the Fed balance sheet...

ReplySorry, Jim*, you are definitely going to be hearing that tightening in EM will drive commodities lower. For the time being, and until it stops working, selling the rips in China and buying the dips in the US, feels like the easiest way to make money in this choppy period.

Reply* (Hmm, Jim, fan of Emerging Markups, are you perhaps a famous Man Utd fan? Enjoy the game Sunday?)

Thanks Polemic, another great post.

ReplyI have one question though, from what I remember China's e-bike driven lead demand acccounts for about 20% of the country's total lead consumption, p.a. Where is the 45% of aggregate demand number coming from?

MW, credit due to Nemo on that one. It was posted under my name for administrative convenience. I'll leave any questions e-bike and lead to him.

ReplyAs for whether it is positive for AUD or not, there have been many things that "should" have been bearish for AUD and its still only just below its lows.

sorry Jim, it is a debate that will roll on no matter how tired we are.

RBNZ did the 50 bps today, as forecast here a few days ago. Long NZD/AUD from here?

Replyhttp://www.xtranormal.com/watch/11071592/

ReplyNot everyone thinks copper is going up forever, or that every Chinese pig farmer is building a monorail.

Ok so on lead demand about 97% in DM is recycled (Euro, and US) so when I build a lead model I look at where marginal demand for mine production is- and that's basically all e-bikes and starter, lighting and ignition batteries for autos. Numbers do vary (there's nothing good and definitive out there) but we are looking at 35-45% of marginal mine demand. Hope it helps. Eurozone and US data is good (check USGS) but other data is a serious hassle.

ReplyWell well, as we be sure you all know, team Pimco appears to have come to the conclusion that the Ts (besides TMMs Platinum, Palladium, metals in general, EMs, euro but not lithium) are toast too… Which makes us wonder, whether the deflation trade will be spun differently?

ReplyThis time.

Anonym at 11:22.

Reply"whether the deflation trade will be spun differently? This time."

Interesting. Seems to me the Irish deflation isn't being accompanied by particularly low bond yields. I guess whether you want the bonds or not depends on whether you think you'll be paid back. Ok, so they're not in control of their own currency. U.S. deflation accompanied by high bond yields is not likely to be a stable state of affairs. But that it couldn't happen at least temporarily?

Thanks Nemo, that makes it more clear and I can do some further digging via USGS. I appreciate the further info.

Reply"Sorry, Jim*, you are definitely going to be hearing that tightening in EM will drive commodities lower. For the time being, and until it stops working, selling the rips in China and buying the dips in the US, feels like the easiest way to make money in this choppy period.

Reply* (Hmm, Jim, fan of Emerging Markups, are you perhaps a famous Man Utd fan? Enjoy the game Sunday?)"

Certainly don't disagree that if you're short term you should make money when you can but my point is the trade will not last post 1Q11; and the trade has been a poor one at best recently...