On Monday, I brought up what 2018 could bring from the Fed, and the possibility that the FOMC might have to react to higher headline inflation, even if it is being driven by higher commodity prices. This is likely to have been a factor in the 20bp selloff in the front end of the us curve since early September….but the long end has been solid as a rock, leading to an epic flattening.

I questioned what would steepen the curve--the catalyst is unclear, but after a little more digging, the strength of the flattening move looks more disjointed from global trends that I had previously believed. Subdued volatility, complacency and a ton of flows into long end bonds and inflation-linkers look to be behind the move over the past couple of months.

I questioned what would steepen the curve--the catalyst is unclear, but after a little more digging, the strength of the flattening move looks more disjointed from global trends that I had previously believed. Subdued volatility, complacency and a ton of flows into long end bonds and inflation-linkers look to be behind the move over the past couple of months.

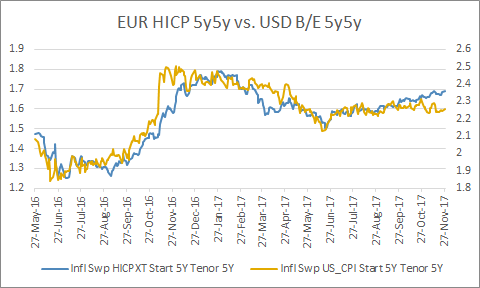

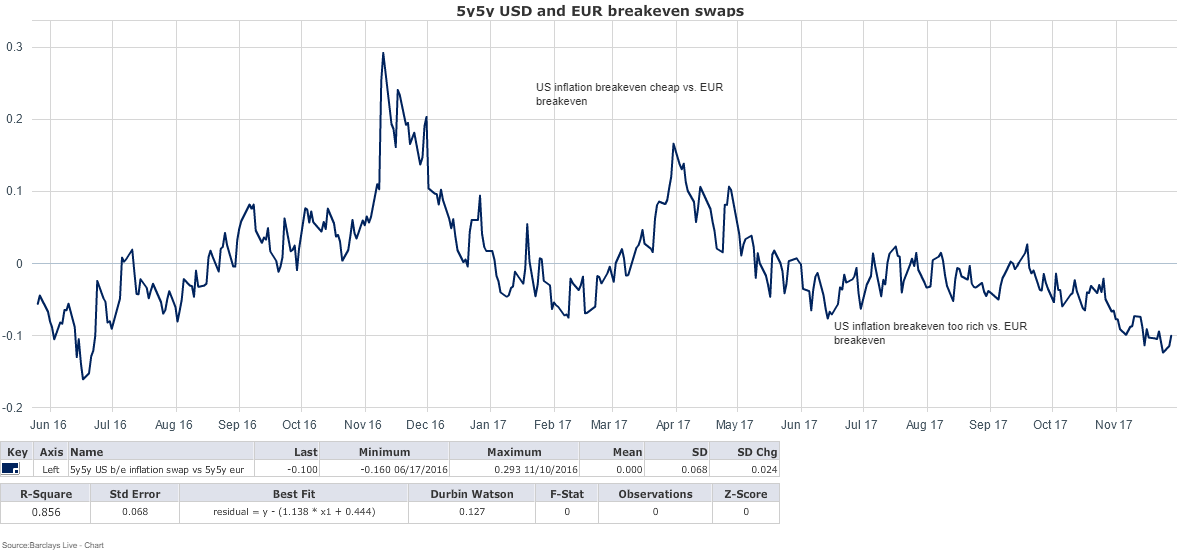

Back in October, I also posted that there has been a strong correlation between EUR and US inflation premiums, and the lack of a breakdown in that correlation illustrated that additional supply and potentially higher growth and inflation resulting from the proposed US tax reform hadn’t been priced in.

Well, I was right, that correlation was about to break down….it just broke down in the opposite direction. Don't let anyone tell you making money in these markets is easy.

Since late September, 5y5y EUR inflation swaps have moved roughly 15bps higher, while the US CPI inflation swap has done nothing.

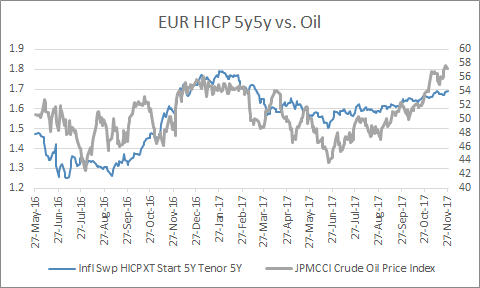

This increase in EUR inflation expectations has been driven by the increase in oil prices...

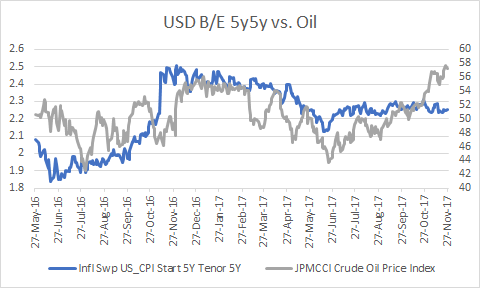

Yet the US inflation swap has ignored the oil move completely.

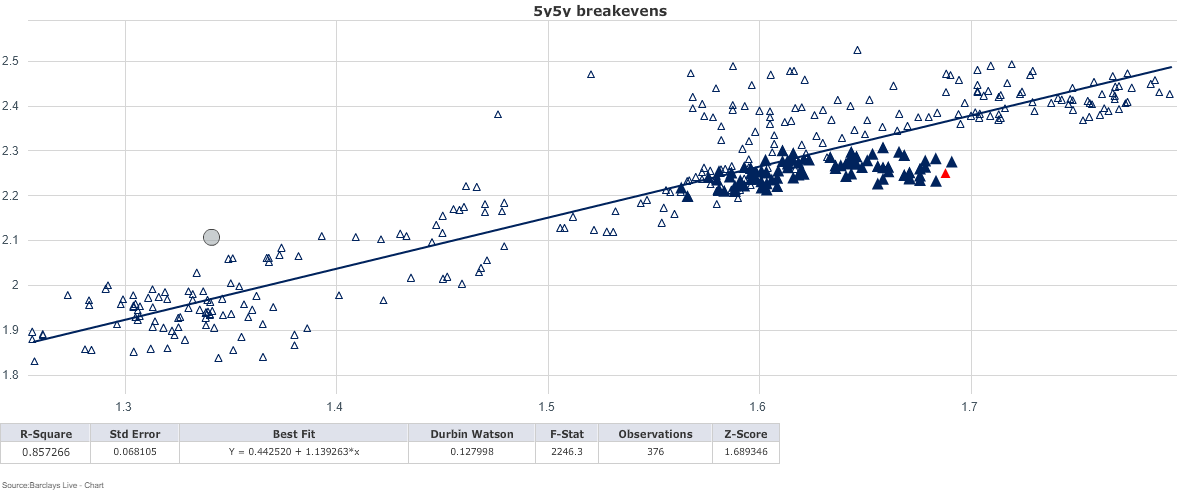

Is there a trade here? Let’s look under the hood. A simple regression analysis shows US breaks are too low.

And the diversions here have been linked to macro events--the Brexit shock in mid-2016, US election in late-2016 and USD strength/ECB tapering move in April 2017. I’ll save some space and a couple more charts and just say the real rate and nominal rate regression components are skewed in opposite directions, which is what leaves the inflation breakeven component looking roughly 10bps too rich in the US.

Oil is higher, labor markets are tight, and we have more evidence that transitory factors on core inflation might lighten up next year, although not totally mean revert. These should all be supportive of paying 5y5y US breaks. What else might push us inflation, and thus long-term inflation premiums, higher?

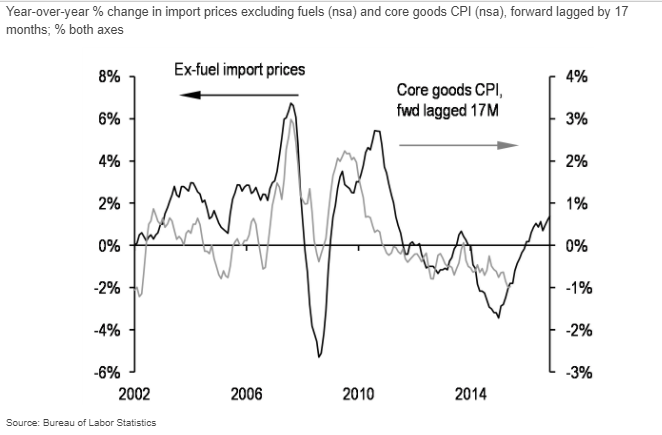

USD has been choppy, but import prices have been rising. I nicked this chart from JP Morgan showing there is a lagged relationship between higher import prices and an increase in core goods CPI. The smart guys at JPM think this will contribute to higher inflation next year.

Then there is the factor that I alluded to back in October: Supply. If Trump’s tax reform passes there will be more bonds and more duration for the market take down. The fiscal stimulus will also be inflationary at the margin--perhaps not a big impact on headline figures but certainly supportive--something the market has ignored completely.

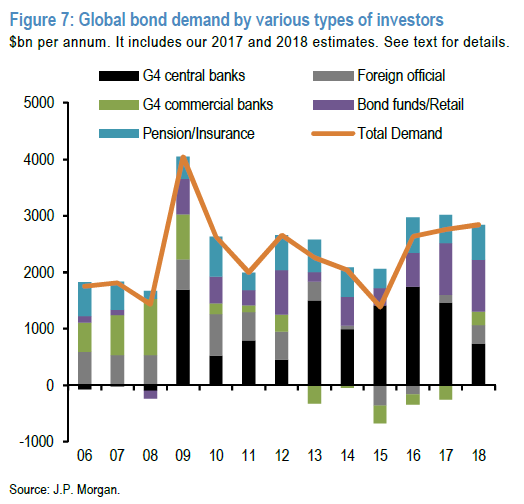

Backing up to the global picture, 2018 will be another year where a ton of bonds will need to find a home...and central banks are closing their doors.

The big buyers will again be central banks, commercial banks and pension funds...

But the supply/demand balance in that chart assumes retail demand equal to the estimated $900bn in inflows for this year. That would be an extremely surprising event in the context of the current macro fundamentals. Even a small downtick in retail flows is going to be a painful event for global fixed income curves.

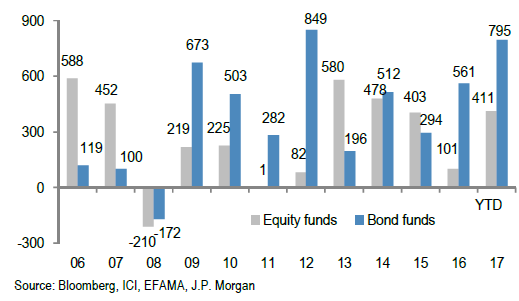

And while I don’t have higher frequency data, inflows over the past two months have been very strong. Moreover, the richening of long end swap spreads amidst the rally in oil, advancing tax reform plans, and stability of long end breakevens argues there has been a very big buyer in the long end soaking up natural sellers of duration. It all adds up to long-end US rates simply looking too rich.

One might be able to write that off to Treasury’s plans to issue more short-term bonds, or the Dudley’s ”r* lower/flattening forever” speech that I alluded to on Monday. But it all seems a little too perfect. Long end US term premiums and inflation expectations are simply too low given the macro factors that supports them.

Shawn

TeamMacroMan2@gmail.com

@EMInflationista

40 comments

Click here for commentsGreat post bro. I just talked with a colleague about this last night. I don’t think the tax reform in totality is priced in at all. Reflation, IMO was always just sheer exuberance from the markets. This includes retail. You’d be surprised how powerful 350 million people coming alive and having a bit more of real hope for the future and their kids can be on group think. I think this was muddled in with tax reform being priced in. The republicans, l either as a part of their plan or by accident have really been keeping their big moves secret and they’ve shown they will listen to markets via “leaked WSJ reports” and get back to the drawing boarding need be. Their including overhauling US higher education along with ACH repeal all w this tax reform!!! Markets havent priced that in man. I think investors have been sort of subdued by bullshit Russian collusion charges...schemes conjured up to ruin this administrations mandate of changing shit. I feel that story is loosing steam fast. I’ve also heard crazy (super stimulative tax reform ideas) about education, training, trade, and finally apparently Trump plans to march ahead in 18 w infrastructure plans. I mean dudes, throw in QT, new treasury issuance, a global hunt for bond buyers (and a collateral shortage also) and our rates will be attractive as fuck as a safe place for money. BOJ, ECB, SNB, BOC still (for now) buyers of bonds and the flows into the US w/b silly. I could be wrong of course, but if this all comes through in 13-14months...it will be fiscal rocket fuel. Which would power a GOP ass beating of the DNC in the senate and the house (yup I said it...house too) then POTUS would have free reign to do the people’s bidding. Many things need to fall in place sure, but it’s far from improbable. I’d say odds are about 50/50 at this point it all works out. I’m unsure about the timing, but fx swap spreads r showing dollar shortage signals again. So IMO this move happens soon. (Also, Relatively speaking, plans don’t have to b perfect just productive) The synergy of all the other factors coming together will be more than enough to put a real charge into markets in. In both a short-term and long-term way. I agree Shawn, the macro factors, geopolitical factors, monetary authorities decisions, and sweeping domestic reforms, all show that the long end of the curve might be where we see big moves. Those factors support higher rates and a fade opportunity. We’re currently deciding if we feel confident enough to take a position...who knows in these markets anymore, but I like the thoughts @shawn. I agree for the most part!

ReplyNo idea why it didn’t give me paragraph breaks...my bad guys...doing this from th phone

Replyi agree with the dollar shortage theme. should be supportive of a steepener, if anything. And to your broader point--the combo of retail flows and complacency around fed hikes, low vol/low inflation at large has led to the turbo-flattening.

ReplyWhat I wanted to include in the piece but couldn't find was some epfr data on inflation-liked bond fund flows. I've heard they've been huge, which ties out to what I highlighted in the piece. if anyone has access to that data (from the weekly BofA piece or wherever), ping it over to me!

BoC isn't buying bonds and neither is SNB.

ReplyThe main reasons for the recent richening of the back end of the US have been, IMHO, the following:

1) TBAC suggesting reduced long-end issuance to focus on 3 - 5y.

2) the ongoing record demand from domestic real money, which is evidenced by the stripping activity.

TIPS are not really particularly relevant, as evidenced by the persistent flattening of the US breakeven curve (I am aware this is all a little bit circular).

Ultimately, the meme that's driving the whole thing is a curious mix of secular stagnation and "end of cycle" ideas.

While I have sympathy with being short the long end, the persistent outperformance of duration has been a theme across a lot of markets (e.g. GBP, CAD and now EUR). There is a possibility that some of it is seasonal.

Duration is really tough to call. Thank you for the post.

ReplyGBP really interests me here. Banks whose research I read are all bearish. A positive outcome at this stage doesn't seem to matter. Market will just start fretting about transition agreement talks, etc. I just don't buy it. Meanwhile, Dec sterling futures are now trading about where they were before the dovish (interpreted) hike. I think there's a good shot perceptions flip, fast, and GBP rips higher. Maybe me just wanting excitement where there will be none. Even the bears now concede that a deal by the Dec summit is likely.

Re Turkey, how bad is this Zarrab case, really? Judging by the hyperbole of Turkish politicians leading up to today, you'd have thought the whole government and whole banking system would be implicated (which, yes, would have been bad). Instead, it's some former ministers and a banker at one bank, all of whom reside in Turkey and are not going to show up for trial (unless they take their kids to Disneyland too). On the monetary policy side, you do have to worry the central bank thinks its announced measures are enough to tide markets over until inflation (hopefully) turns in Q1. If the Zarrab case doesn't look to metastasize from here and CBRT hikes in-line with what's priced in the short end, the currency could get a bid here ... still, I worry the central bank is going to be stupid and wait until USDTRY surges through 4.00 before doing anything.

So, does this missile test mean "completion" of testing and everything goes quite now in the Korean Peninsula?

Well I forgot to mention the pacific is essentially on a dollar currency. Chiba can’t function without it. I agree with Bass on this point the treasuries are their best collateral. They’ll be buying. BOJ and ECB will buy, I’m not specifically knowledge about SNB saying it’s kot into bonds, but I’ll take ur word. They buy everything else. Shit even Russia is hurting for basic dollar funding. Ext they work something out w trump. Treasuries for unincumbered access to LNG markets. Simply spitballing is all boys. Anyone ever think of the massive collateral shortage were about to see??? Finally those TIPS they are quite the mystery. I have a great recent white paper on white off the run tops are underpriced and it’s costs the bc fed 100’s of billions annually. Fascinating, but I might think longer dated TIPS would be n demand simply because of your point about treasury issuance and the focus on front end rates. Who knows if that goes through tho...wild stuff watch HKMA, HIBOR, yuan repos by the PBOC. That’s always where I see disruptions first (in the wholesale markets) mostly at least

ReplyYeah the narrative from Korea is suspect. I mean no disrespect but, it seems this all of the sudden impressive launch and the Japanese are finding shipwrecked boats (Japanese) with dead bodies in them...they blame Korea...is enough to buy but it just seems scripted or something...I don’t know just a weird vibe...@Johnno like the interest in GBP also markets seem not to represent the every day Englishmans take on the future...I think it will (eventually) be an empowering moment for UK. The opposite of the drab headlines

Reply@LB, I may have an answer to your question on what else cryptocurrencies may take down with them - SOX. It should be no surprise to many but to some may be less obvious that GPU makers would take a major hit. NVDA was down 6.8% and they smacked SOX for 4.4%

ReplyWeird day... Rotation was somewhat of a theme (so SOX could also be down in sympathy with Naz) as old economy got a bid - look at Transports @ new ATH. But some things were head-scratchers. Like I expected Gold to get a bid when Bitcoin was sold hard. Nope, did not happen. Part of it may be to @johno's point (hat tip) that KJU is done ejaculating for a while, hence both got sold hard. Again, I hardly believe cryptocurrencies are safe haven.

More on rotation... XRT is ripping - a pardoned turkey in celebratory flight. I think it does a bit more damage above $44 to the ones who thought bricks would be done forever. Thanksgiving foot traffic was just fine. AMZN got smacked hard, feeling WMT breathing down its neck online, I bet.

R2K got a bid. Why? Tax cuts? I don't get it. This was a weird day, indeed. One day does not a trend make.

@Shawn, it's my pleasure to contribute here. I drop an f-bomb way too few times to even notice but an imbecile got the worst of me. To me he writes with an invisible ink from here on :)

About your post... I think it's been hard to correctly interpret the dynamics of the treasury market, especially since CBs are still swimming in the pool in size. This being said, TNX (10-yr yield) likes to fool traders like no other vehicle. The most illusive chart pattern it trades is inverted head and shoulders. It fails all the time, without exception. If you look at weekly chart you will see exactly what I mean. There is one unraveling as I type. Broken dreams...

@Martin, so yeah I hear you on the TBAC move--I don't think it was a game changer but gave some big accounts another bullet point for pushing the move. I'm not sure what to make of the second point--that flow has compressed the long end, and while I don't think it has accelerated in the past couple of months, it has continued and seems to have coincided with a big flow into TIPS, which is what created this regression/mean reversion trade.

ReplyRe: Turkey, I've avoided shooting my mouth off on this one--the issues you bring up are real, but also why I don't like the market--the weaknesses are institutional rather than economic, or even political in some ways (ZAR and BRL so sane and textbook, by contrast). The only thing I would say is that TRY has gotten bad enough some bloomberg journalist had to write up the obligatory "Japanese retail panicking in TRY carry trade" article. This is the next frontier for AI/machine learning--writing and publishing boilerplate bloomberg articles in real time as the EMFX dog of choice takes out another set of barrier options.

Spreads between RoW {bunds, JGBs and gilts} debt on the one hand and US 10s on the other hand will continue to provide a bid at the long end. The greying of the US boomer population will provide another constant bid via pension funds. Even 401k 'ers might start to think about fixed income a bit more if/when the "market" ever suffers a reverse.

ReplyInflation watch - PCE today 1.4% ... yawn. Hourly wages, going nowhere. Crude, probably at the top of the range, about to drift lower. "Fiscal Stimulus" (aka tax bill), not a given that it will pass and not clear that a corporate tax cut is stimulative (in fact, history says it isn't). Most importantly, China, probably slowing (I mean, GDP 6.2% y/y COUGH), as revealed by recent moves in Dr Copper.

OK, we are done here. Bond bears are wrong again. There will be another monster short-covering rally in the long end before the end of January. Technical analysis for TLT suggests that the outlook remains constructive. Lower yields, weaker dollar, the latter especially after the next FOMC meeting but possibly also Sell The News if/when the tax bill is passed.

Even as Spoos and R2K ascend to new heights, the VIX is climbing alongside them, stealthy making higher highs and higher lows over the last 4-5 trading days. A gradual and initially orderly unwind of short vol positions might be something to keep an eye on today, and vol would provide an interesting ingredient in the trading mix if, for example, the Senate doesn't pass the tax bill.

ReplyChad, Brad and Thad left the pension fund a while ago and have opened a hedge fund specializing in vol selling. Serenity Capital, trading as Placid Asset Management, is basically long SVXY [+135.9% YTD] with a bit of added leverage.

Performance, bitches! It's all plain sailing ahead, as far as the eye can see.

Oh look, Dow is up another +100 points since my previous post 30 mins ago. You amateurs have no fucking clue.

ReplyBoth the short vol ETFS are now trading at a 5% premium to NAV. Premia like that are usually a good indicator that it is a crowded trade. Or to put it another way, Amateur Hour. Just sayin'.....

ReplyC, B and T are not making any money today, or yesterday, btw. If we are keeping score. :-)

http://vixandmore.blogspot.com/2007/05/high-positive-correlation-between-vix.html

ReplyGod! I understand why you would want to place him in the highest office and let him tweet. Humanity needs a wake-up call. But why you would also allow him to write the same comment on this obscure blog is way above my pay grade. Please tell me you have a master plan!

ReplySo we have the ext of the oil production cuts (with Libya and Nigeria quotas agreed) and a missile flying towards Saudis? Oh my, I better go buy more stocks. Oil stocks, that is. This is hardly the top of the range on crude, imho.

ReplySorry for multiple notes, a bit scatterbrained today... So while Wharton graduates and "alike" are jubilant about the Dow, I'd like to look at another index and see how we could play it in the event of sell-the-news (tax cuts bill passage, whatever) case taking place. So we have a 139-pt uptrend s/t channel on NQ. There has been no breach of the channel for the entire month of Nov. It's quite fitting for the mo-end momo chasing after a successful test of the lower trendline y/day and we are dead smack in the middle of the channel right now. This being said, 6376 (11/22-23 lows) is an important resistance level to overcome. We stopped right there today. Should it not let in for a few days we may have a case of minor exhaustion forming. You could start putting fib extensions on this but I would simply measure 139 points below the break of the channel for the target. That's roughly 3-4% below ATH, depending on when and where the actual break occurs. In case you are wondering, the last four Dec were all down months for NDX with an avg decline of 1.3% on monthly closing basis and avg decline of 2.4% below ATH at a low print in Dec.

ReplyPound call is working (switched to EURGBP in delta-one and now very long GBPUSD in options as I'm getting into/closer to my strikes). So is EURCHF. The mean-reversion trades, EURSEK and EURNOK, are not. Somehow I scalped the hell out of EURNOK in the early morning. One of those rare instances, very rare, where I'd give myself an A+ for trading. Have kept the position small enough to be able to take that trading risk. Not sure where we go from here. NOKSEK seems to give some support at these levels, so it's maybe a question of EURSEK steadying/reversing (a Riksbank meeting and PPM pension money distribution to contend with) and EUR not ripping. Any regression model of EURNOK is broken and gives no comfort. That we're 1% from 10 on the cross (which was last seen in the depths of the GFC) I suppose is helpful. There's no narrative for hikes in 2018 to get excited about, but this currency weakness should boost inflation and maybe bring forward a hike (first not fully priced until 2019 currently). Also, OPEC has now passed without a debacle which is incrementally positive.

ReplyHard to argue with Shawn on Turkey. Today Zarrab implicated Erdogan, but didn't sound like that was enough (I mean, this guy who bribes prison guards says some guy - presumably not Erdogan directly - told him Erdogan approved the scheme. Maybe true, but doubt that passes the standard of the court). Maybe I'll get lucky, the Zarrab thing doesn't blow up and the CBRT hikes as Erdogan's adviser suggests they might by the next meeting. Of course, getting lucky is not a great strategy when it comes to Turkey ... so many own-goals by these guys.

Anyone care to explain how Simon Coveney's comments today are consistent with a successful meeting between Tusk and May on Dec 4? What I'm struggling with currently ...

Reply"Chad?

ReplyIt's Brad, I am at the Serenity trading room.

Do you know where Thad is?

We just lost, ah, 8%, 9% of our AUM in 5 minutes."

"Double down, bro.

Snort another line, dude.

INCREASE THE LEVERAGE.

Turn it up to ELEVEN, Nigel!"

I love the smell of napalm in the morning!

ReplyThe yen surged 1% in 15 minutes.....

Reply10s have fallen 9 bps, 30s fell 10 bps or more.

ReplyProbably that's the last comment on the long rates topic for the time being, eh?

Those who took the NQ trade... While the channel is still intact on hourly closing basis, it has indeed been breached by roughly 60 pts and the 139-pt trade distance from YH to today's intra-day low was almost achieved (less 8 points). You are being handsomely rewarded here so taking scaleout profits is a great way to protect the profits. I took 1/2 off and moved the stop to b/e. We are seeing a quick bounce on senate bill passage but I suspect the fear of holding into w/e and all the noise to come out of Flynn story will take over, imho. In any case, my ultimate target is 6160.

ReplyTrue for you IPA - few have gone broke taking a profit.

ReplyThe excitement/putting the boot in, on here is telling. For those of us who like to keep our cocks tucked in our socks most of the time(or care not if the market is up or down) , can I ask the simple question, Is volatility back?

Hard to call a winner here guys if it is,as is evident this week.

Ok ,so it's the weekend and I can post one that I found funny today. In effect, a guy told me he's gone major US$ assets so that when Corbyn tanks the £ he will be hedged the political risk. I thought without commenting at all maybe Corbyn will be Trumped !

ReplySo educated friends where would you start trying to quantify whether Trump is a greater threat to your wealth than Corbyn? Actually , I am beginning to wonder if the so called political risk in emerging markets is a reality any longer in terms of exceeding that of our so called developed economies.

Brad here (from Serenity Trading). We doubled down as per LB's transcript:

Reply"Double down, bro.

Snort another line, dude.

INCREASE THE LEVERAGE.

Turn it up to ELEVEN, Nigel!"

Obviously the dip was bought (Trading 101) and we have captured a massively leveraged +30pts in ES, +300YM in YM etc in several minutes. (Yep that 1900 ct order that pushed ES 11 ticks in one order was us). So biatches, we've now made a higher percentage return in one day than most macro funds have made for the year. Watch and learn.

Whoresome !

Reply"can I ask the simple question, Is volatility back?"

ReplyToo early to say, for sure, Skr, but one thing is clear; if a 2% drop in the Spoos can induce a VIX spike large enough to briefly wipe 10% off a vol selling ETF, just think what a 5% move over 2-3 days could do. This depends on reflexivity being a phenomenon that works both ways, not only on the way up, but also during a risky asset price move direction that we refer to [according to historical precedent] as: "DOWN". This market feels like it has one really big puke in it, and we expect to see it before the FOMC meeting. The interesting thing is how strong the underlying bid in vol has been this week. It's forming a base.

It will be interesting to see how many of today's dip-buying 12y-o fighter pilots (that was a decent short-term trade, btw) would be willing to go home long spooz and short vol into a weekend of unknown news flow, or whether they were happier to sell during the lunchtime pool of shallow liquidity to unknowing and unidentified knobs and noobs in order to go home flat. We suspect the latter.

Spreads for curious curve watchers: 2s10s 59 bps, 5s30s 64 bps; 10s30s 40 bps and 2s30s 99bps (TWOs-THIRTYs - yup, one percentage point!!!). Not only is the flattener not dead, it has returned with a vengeance. We hear a lot from the 12 y-o punters about how the bond market is wrong, the yield curve doesn't matter, etc. - but those of us with a long memory know what's coming.

Thanks leftback. Back in January I was sure volatility was going to happen big this year."Early, wrong same thing" it has cost me.

ReplyJust want to point out that WTI is holding its own and is closing at a second highest level this whole yr. How important is this? Look at your momentum indicators hooking back up and then go back to price. It is King, it is ripping, broke out of a bull flag and it's back to the races in a steep 5-point wide uptrend channel. Take a quick measurement and it's not hard to see this baby blowing through $60 within the next two weeks, stops will do the trick. My ultimate target is $62. I will be a seller.

ReplyA quick note of caution to those who think they are larger than the market. It does not care how many contracts you trade. It can take you out on the stretchers like you can't ever be prepared for. It teaches you to be humbled and never tell anyone (let alone those who do this for a living) that you in fact moved it. The market is unforgiving and sends you to the dumpster as many times as it takes for you to start hating to bathe in your own puke. As soon as you learn this, then it is time to throw big phrases only around your toilet, because you never move away from it for longer than an inch. Be safe and stay away from the moronity well you've been drinking from. It is so poisonous.

Have a great weekend!

@Shane, looking at 10-day weather forecast makes me think that my bones will hurt really bad come second part of next week. Nothing gets traders to buy Nat Gas more than seeing national TV news anchors throwing snowballs at each other in the middle of Manhattan (trumps my caterpillars anecdote by far). A short-covering is how all previous spikes began but I think this time it'll be new longs who will take over and hold for much longer than just a few days. Huge resistance above to overcome between 3.15 and 3.30 but once we clear that it's smooth sailing all the way to 3.50 - a nice gift for us just in time for holidays.

Reply@IPA...comment on the year on staying humble and climbing out of the dumpster....and re: the weather forecast, don't forget the run up in energy prices we've already seen! that will contribute to a greater divide between headline and core, which will become more problematic for the fed.

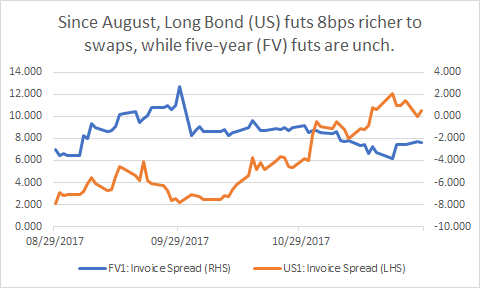

ReplyNot to add insult to injury but would point out that last graph showing that US invoice has been rich vs FV invoice may be getting it wrong way about. The persistent curve flattening is directly fueling the steepening of the swap spread curve, and in particular driving 30y spreads the multi-year highs (headline 30y spread last at -19.50). With lofty equities and rates trading sideways, the beta of back-end spreads with respect to pension/insurance driven receiving needs has lessened, so back-end spread widening are increasingly coupled with USTs 5s30s curve flattening. As Martin hinted above, Treasury refunding likely helped this coupling. Decoupling would require, likely, a less complacent market with the accompanied bidding up of risk premia, perhaps as the Treasury eventually shifts its views on concentrating issuance in the front-end USTs curve.

ReplyNice 2y swap spread call a few posts back, hope you sold ahead of refunding.

R2k is lagging again today. Small caps lead bull markets and then quickly become small craps when the tide turns. Despite positive noises out of Japan, the Nikkei looking weak over the last 4-5 trading days. Maybe Kuroda is stealth tightening, after all?

ReplyLong bond continues to trade constructively; yield curve continues to flatten. There are more than a few signs out there (Copper, China data, yen hanging in there when it shouldn't) that 2018 growth forecasts for the US and globally may prove to be optimistic.

Spreads between RoW {bunds, JGBs and gilts} sbobet debt on the one hand and US 10s on the other hand will continue to provide a bid at the long end maxbet. The greying of the US boomer population will provide another constant bid via pension funds

Replyแทงบอลออนไลน์. Even 401k 'ers might start to think about fixed income a bit more if/when the "market" ever suffers a reverse แทงบอล sbobet.