Some quick thoughts on EUR, after our brief off topic discussion in a comment thread last week.

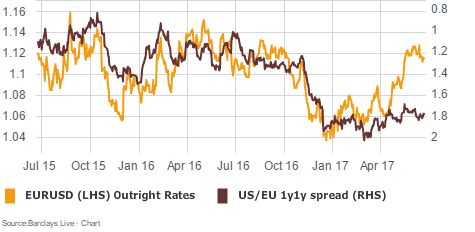

EUR has decisively broken out relative to the choppy, low-vol price action in front end rates.

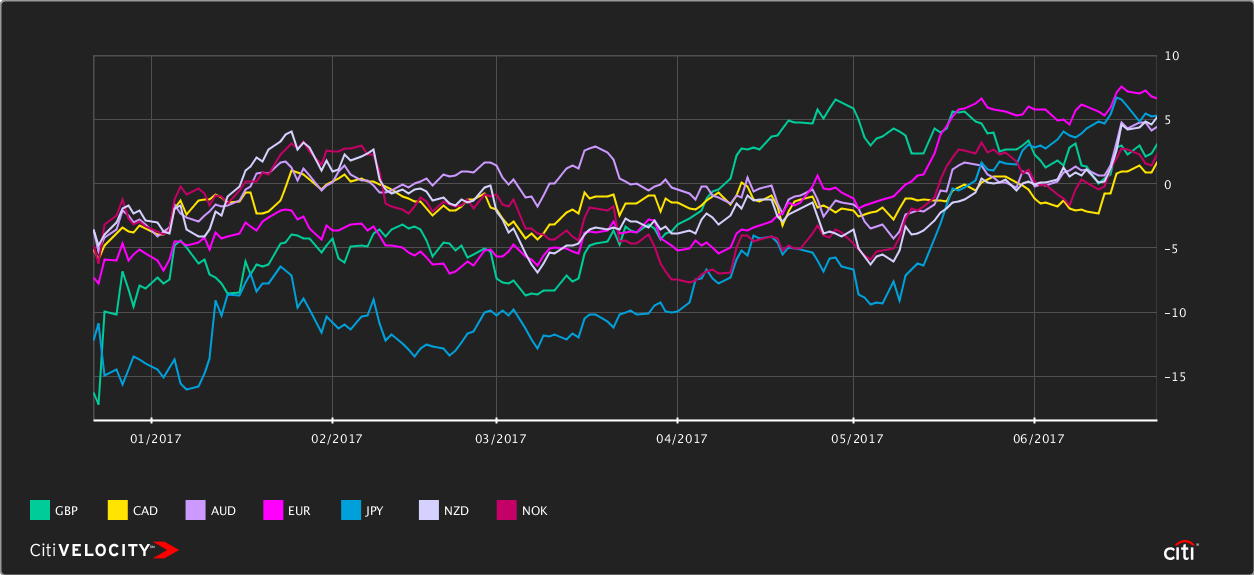

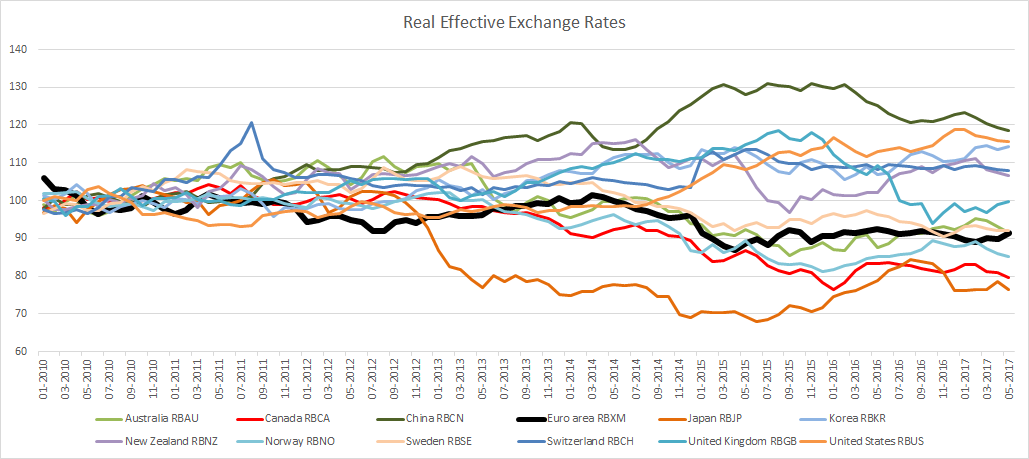

And it has broken away from the pack vs. other DM currencies--this is the rolling 6mo total return on some of the big boys.

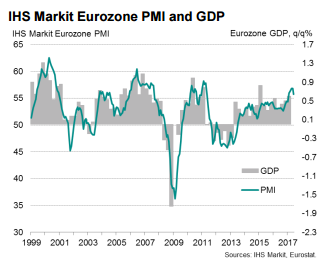

Some of this is due to better data, specifically PMI, which is at the highest level since 2011. This can plausibly be seen as a leading indicator of stronger growth...

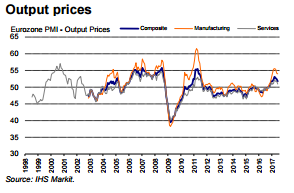

Leading to speculation about the end of QE and higher rates--but with core inflation is still stuck below 1%, it's just that...speculation. However, output prices in the PMI have moved sustainably higher after years stuck below 50. This moves the prospect of tighter monetary policy from “never gonna happen” to “better listen to Draghi.”

Despite the run from 1.05 to 1.12, EUR still looks cheap on a REER basis, and well below those at the top of the table...USD and CNY. In REER terms, EUR is cheaper than in mid-2012.

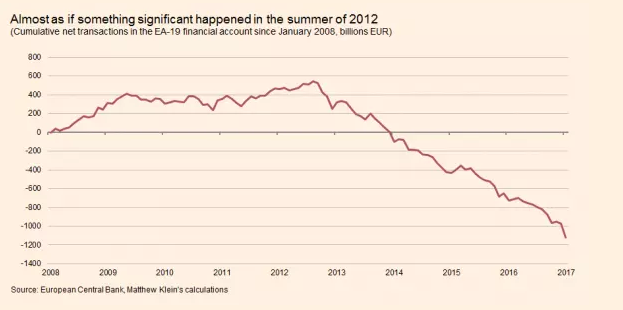

The potential for appreciation is there--the Euro area current account surplus has been trending higher for years, and is now sufficiently huge.

But as noted in an excellent article in the FT by Matthew Klein, the mirror image of the c/a surplus is capital flight. Part of the reason the ECB went to negative rates was to reduce appreciation pressure by incentivizing capital to go elsewhere--capital outflows further driven by the moribund economy and better growth and higher rates in the US held the currency back for years.

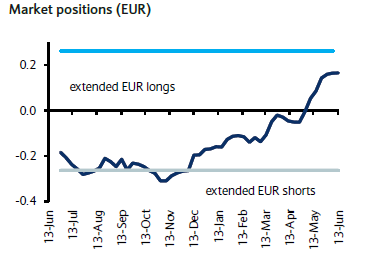

This is a battleship that could finally be turning. That possibility has lifted positioning by speculators from a multi-year period of EUR bearishness:

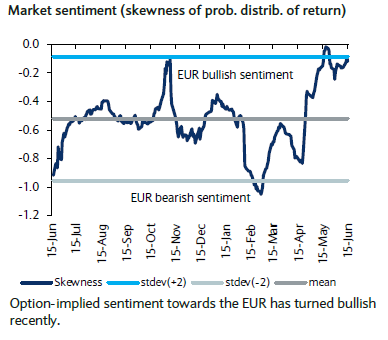

But there are some signs we might be getting a little over our skis in the short-term:

Piecing it all together:

- I have subdued view of US and Chinese growth and the Fed,

- A potential downdraft in Chinese export demand notwithstanding, European growth is at an earlier stage in the business cycle, and

- There is a potential for an enormous reversal of capital flows that were beared up on EUR for years, especially after the ECB went to negative rates

- All that said, EUR has gotten out ahead of rates--something’s gotta give.

A lot of things have to go right, and Italy still has to get its act together--but I think there is room for EUR to run in the medium term. I’d look to pick up some cheap gamma for a secular move while protecting against the short-term frothiness and build a cash position on a pullback below 1.10 if the technicals clean up and fundamentals remain intact. In rates, I’d pay EUR front end rather than USD given the lag in rate spread relative to the currency; selling Eonia greens (basically paying 1y, 2y fwd) has a nice entry point and hasn't steepened too much relative to reds, which sets up a good entry point.

Shawn

TeamMacroMan2@gmail.com

@EMInflationista

Shawn

TeamMacroMan2@gmail.com

@EMInflationista

18 comments

Click here for commentsNice summary, Shawn - and it dovetails well with a view that the FED is going to have to heed the data and start to talk about a slower pace of its rate moves during 2H '17, while perhaps shifting the focus to a glacial unwind of the balance sheet. If both of your views are correct (stronger EU, slow US) then EURUSD should indeed have room to run in 2017 and we may see an unwind of the USDJPY and associated trades (US equities and unicorns) as a softer view of US growth takes hold (in Q4?).

ReplyJust for the immediate future, dollar bears seem a bit over-extended, as does US fixed income. Expecting a reversal for a while as we are bound to bump into one or two pieces of decent US macro data soon, perhaps as early as this week. The Fed is clearly still on the road to incremental tightening unless something absolutely catastrophic occurs. Right now we have signs of the usual summer doldrums and a very flat curve, but none of the credit spread issues that usually signal a recession. Crude oil may also be about to form a bottom of a new trading range.

The TLT has now closed a gap that existed since the Trump election. It looks like it may be time to close that trade, and we will take it down during this week. TLT now sits here above 128, after entering in late November early december, at various points between 118 and 120. One of those swing trades that seems incredibly obvious in retrospect, in fact it was an absolute layup, but if we think back to late 2016 was very very unpopular as RSI plummeted to the low 20s….

Watching the XLE with great interest, with Kevlar vestments close at hand. That might be the next good swing trade, look out for signs of capitulation by bulls when the midweek data are released. We don't seem to be at a sentiment extreme yet.

Where do you get the Skewness from? I presume it's not just the volatility difference between out of the money and in the money options

ReplyWhat is the value in XLE, given the P/E? Is there any reason why one would prefer XLE to just buying Crude oil?

Reply@ Michael H, long story short, it is a measure that takes the implieds from across the curve to build a probability distribution, and evaluates which way the market is leaning based on the skew. I've posted the technical definition below from Nikolaos Sgouropoulos and Aroop Chatterjee at Barclays.

Reply"Using the option smile at each specific day, we have estimated skewness and kurtosis coefficient of the implicit probability distribution of the spot return embedded in the smile. One can interpret skewness (the third moment of the

distribution) as directional bias, or the market betting against the forward price...Skewness and kurtosis are better than risk reversal and strangle at providing information of the market’s direction bias and perceived fat tail risks as the former measures are not dependent on at-the-money."

Looks like we may have called the top in bonds yesterday, as today's yield jump looks like being a momentum changer. We suspect the long curve flattener has come to an end today.

ReplyThe prospect of a profusion of Fedspeak this week clearly raised the risk level for US fixed income, but the real market mover today was Draghi…. who also caused a spike in EURUSD and bund yields. Fischer and Williams remarks have had more effect on US equities than in FX and rates but there is some follow through in those markets also.

Tomorrow may well be a reversal day, if oil falls once more on supply/storage data then yields will drift downwards again - but the bond market's direction may already have changed, for the next few weeks at least. We would be inclined to sell strength for the time being...

I enjoyed over read your blog post. Your blog have nice information,

ReplyI got good ideas from this amazing blog.

goldenslot

gclub

gclub casino

ฟิลเลอร์มีคุณลักษณะ

Replyยังไง

?

คุณลักษณะ

ของฟิลเลอร์ ช่วยสำหรับเพื่อการ

เก็บกัก

น้ำของชั้นผิวที่ได้รับการปรับแต่ง

หน้าตอบ ร่องปน

ลึก ฟิลเลอร์จะช่วยเติมเต็มช่องว่างให้กับเซลล์ผิวหนัง หรือเพิ่มขนาด

ให้กับผิว เทียบเคียง

ได้กับการต่อว่า

ดสปริงให้กับผิว ให้ผิวยืดหยุ่น เต่งตึงกระชับชั้นผิวเรียบเท่ากัน

ลดริ้วรอยเหี่ยวเฉา

หย่นย่อ

ทำให้บริเวณใบหน้า

มอง

เด็กลงอย่างแจ่มแจ้ง

รวมถึง

การปรับรูปหน้า เติมเต็มรูปหน้าให้ได้ส่วนสัด

ได้รูปเพิ่มขึ้น

และก็

จะเสื่อมสภาพ

ไปได้อย่างธรรมชาติ สำหรับหมอ

ผู้ที่มีความเชี่ยวชาญ

จะสามารถนำฟิลเลอร์ มาเติมเต็มได้ทุกส่วนของผิวฉีดฟิลเลอร์ใต้ตา

ฉีดฟิลเลอร์ร่องแก้ม

Thanks for the good information And useful

ReplyดูหนังNetflix

รีวิวหนังแอคชั่น

Cool

Replyดูหนังใหม่2021

New Movie review

รีวิว หนังใหม่ชนโรง

หนังใหม่ Netflix

thank for good post and sharing

Replyดูซีรี่ย์เกาหลี

seriesfin.com

Thank you.

Replyดูซีรี่ย์เกาหลี

seriesfin.com

Thank you so much

Replyดูหนังใหม่ชนโรง

seriesfin.com

like we may have called

Replyดูหนังฟรี

seriesfin.com

Thank you very much for the information

Replyดูหนังออนไลน์เต็มเรื่อง

ดูหนังออนไลน์

Thank you so much.

Replyซีรี่ย์เกาหลี

seriesfin.com

Replythank you very much

ดูหนังชนโรง2022

dramaslist2u.com

Excellent post. I was checking continuously this blog and I am impressed!

ReplyVery helpful info specially the last part 🙂 I care for such information a lot.ดูหนังออนไลน์ฟรี

I was looking for this certain information for a long time.

Thank you and best of luck

Thanks for this article. I really like it. It's very helpful for me. Thanks again for this article. please contact me back. รับทำบัญชี

Reply