Ok stick with me gang--I'm sorry to go deep on Mexico again but I think it is worth a drill down. While there are some super-talented analysts on the sell-side their incentives to not stray too far from the herd. When big moves happen, cognitive biases can blind people to the big picture. Often times you can extract value by getting into the weeds.

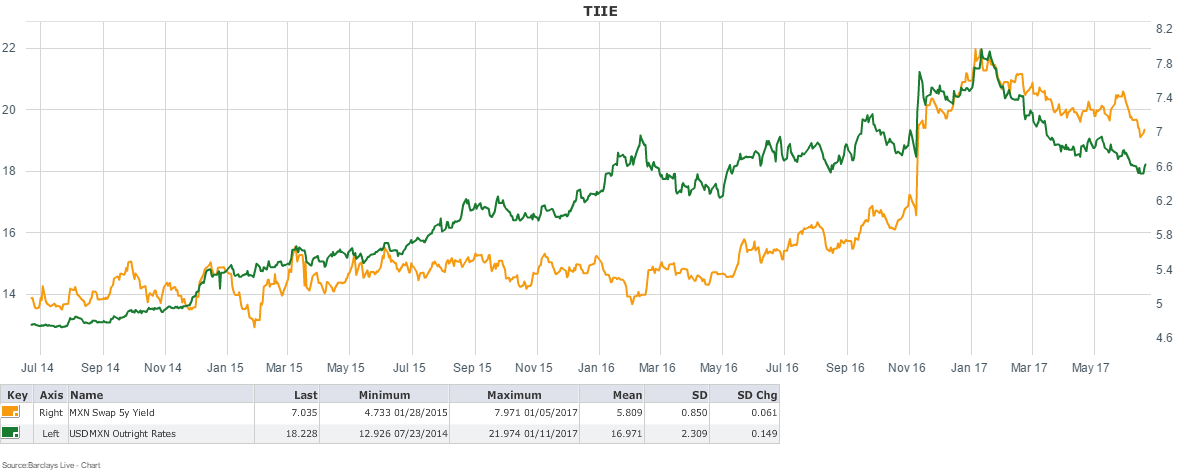

As I noted last week, Mexican local rates rose dramatically in reaction to a spike in CPI, one which was driven in part by the depreciation of the peso and 375bps in hikes from Banxico. Today, rates have rallied well off the highs, but are still sticky at levels above late 2016 levels, both in absolute terms and relative to US rates. For its part, MXN has come all the way back thanks to a weak dollar, EM inflows and higher local rates.

My thesis is that these rates can continue to come down because Banxico can, and will, cut the overnight rate aggressively in 2018. I believe markets are underestimating the magnitude of a rate cut in the same way they underestimated the size of the hiking cycle.

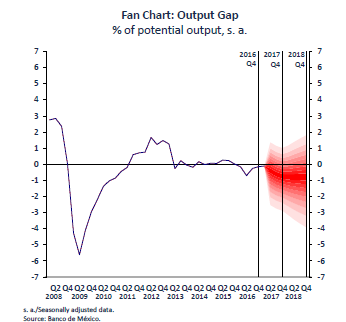

First is this chart. There is an output gap, and one that I don’t think is going to be soaked up by tepid US demand in the manufacturing sector (note the channel cramming in the auto industry), or domestic demand when interest rates are high and there is uncertainty around the 2018 election.

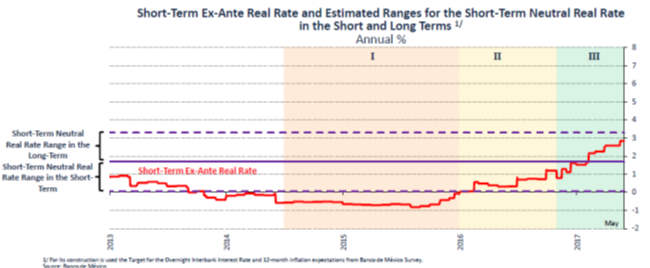

Similarly, we see that real interest rates are high--Banxico hiked aggressively to stabilize the peso during the EM selloff and Trump-mania.

A more “neutral” real rate, as much as I hate that term, is likely to be around that 2% level--that is still high by historical standards and stands as a relatively conservative estimate given the 5y5y real rate in the US is still stable well below 1%.

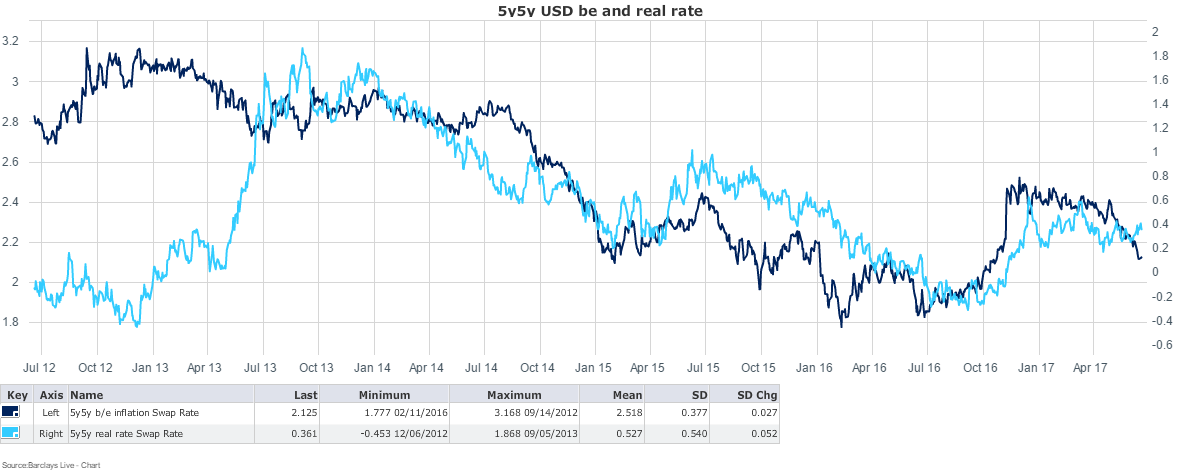

This chart also shows that breakevens have been falling consistently since the US election as the “Trump-flation” trade unwinds. While Mex breakevens have been falling too, they are still at elevated levels. As I noted last week I think there is at least 25bps in value in nominal curve built into the breakeven rate (roughly from 3.75% to 3.5%).

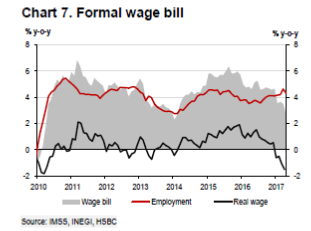

What makes me so sure that breakevens shouldn't be permanently higher given headline CPI is currently above 6%? Among other things, wages haven’t shown any sign of secondary impact from that inflation shock--in fact, quite the opposite. This argues that 1) there is slack in the labor market, and 2) businesses are recognizing this spike in inflation as transitory and underlying inflation probably isn’t too far from Banxico’s 3% target.

Next is a similar chart from Banxico for inflation. They expect inflation to top out this quarter and come down relatively fast until it reaches the 3% inflation target in late 2018.

I agree with their path here, in fact I think it could come in on the low side. Let’s look under the hood of the Mexico CPI figures.

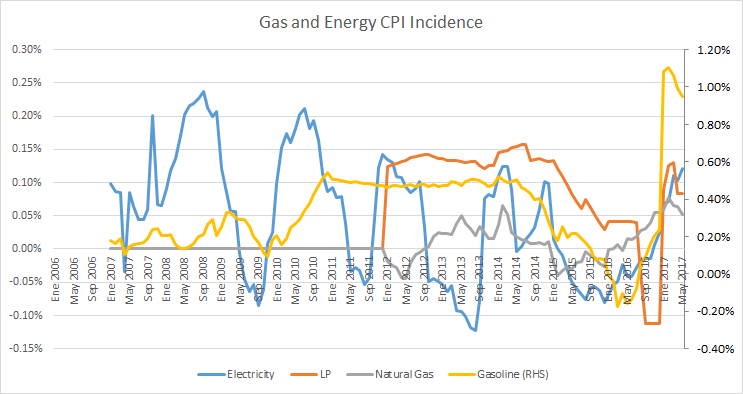

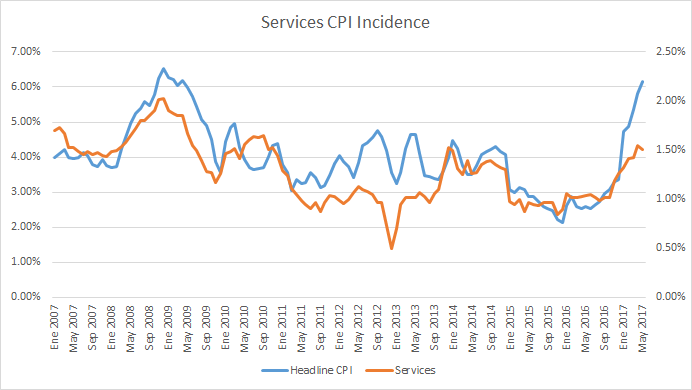

A big portion of the increase in inflation came from a hike in gas prices back in January. This was big enough to bring people in the streets in protest. The chart below shows the increase in gas prices alone--not counting second-round effects--has driven headline CPI roughly 1% higher (this is the “incidence”, the increase in the price times the weight in the index). Similar hikes in LP, natural gas, and electricity have had an effect too. Note that all four are near cyclical highs.

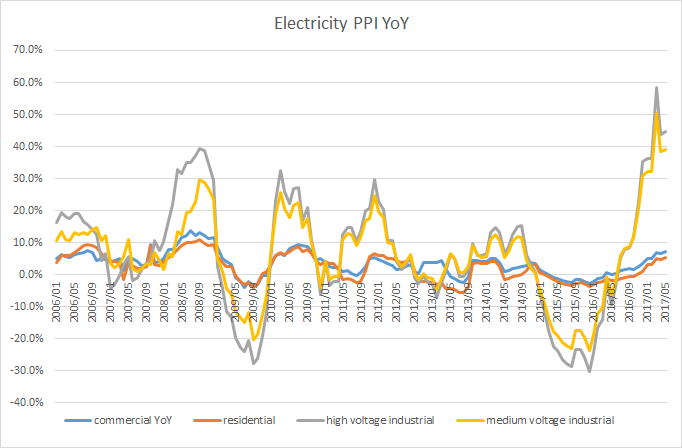

Another indirect impact from higher electricity prices is built into the producer price index: industrial, commercial and residential prices. Industrial prices have skyrocketed as the government passes along higher fuel prices and pressures heavy users to increase conservation measures. Just as importantly, commercial electric rates were up over 7%. More on that later.

Three big stories here:

- After a history of gas subsidies, gas prices will be set by the market throughout the country by the end of the year, and international companies are now free to open service stations to compete with state-owned Pemex. There are some new independent stations that are already selling gas cheaper than Pemex stations, and several international service chains have big plans to expand. This effect combined with lower oil prices could result in 5-10% lower gas prices nationwide.

- The electric industry is in the process of deregulation. Outside capital is coming into the market, and the industry in is in the process of switching from dirty, expensive oil, to cheap, clean natural gas. The recent spike in electricity prices is likely to swing negative in the near future.

- Natural gas is also undergoing a transformation. Thousands of miles of pipelines are going live this year and next to import cheap US natural gas. Again, the price increases here are unlikely to be structural.

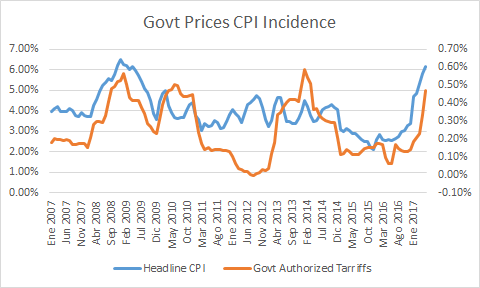

Government controlled tariffs are another big element of CPI. As the name implies, these are prices that are controlled by the federal government. One of the big ones here is hikes in public transportation prices. This is a total one-off, and as the historical chart implies, is unlikely to be repeated.

Moving on to “core”--Merchandise inflation has contributed over 2% to headline inflation. I see this as a mean-reversion--the still slow economy and MXN coming back to mid-2016 levels will cause this component of CPI to head back towards the historical mean, if not below. Lower fuel prices would be supportive here too.

Similarly, the contribution of services inflation to headline CPI is also near historical highs. This is particularly unusual given the low wage hikes over the last year. No big outliers here but given the strength in MXN I think this is another sector that can mean revert, with downside in areas like education, restaurants, airfares, and tourist packages.

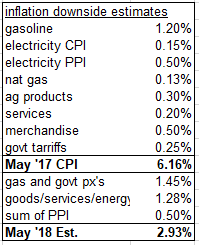

Putting it all together--I’ve noted below what I think are conservative estimates for how much inflation can revert from each sector.

Some of this analysis I owe to a paper written by Federico Kochen and Daniel Samano for Banxico. They estimate between .043% and .073% in “pass through” inflation given a 1% change in the usd/mxn rate. My estimates for a reversion in CPI that “unwinds” the impact from the peso deval of late 2016 and early 2017 is broadly consistent with their figures.

Kochen and Samano also had data to show there was a 7.2bp “pass through” to headline CPI from a 1% change in the producers’ electricity price index. Given the 7.3% YoY increase in commercial electricity prices, I’ve attributed a 50bp decrease in the headline CPI rate should electricity prices remain flat over the next twelve months--again, given the impact of reforms and lower natgas prices, I think this is a conservative estimate.

There you have it--what I believe is a plausible forecast that would get inflation back to 3% by mid-to-late 2018, and largely due to structural factors, while one-offs are unwinding. I would allow that the 50bps in electricity PPI might double count some of the factors I account for individually, but I estimated conservatively to allow for that, and assumed no indirect second-round impact from flat to lower gasoline prices.

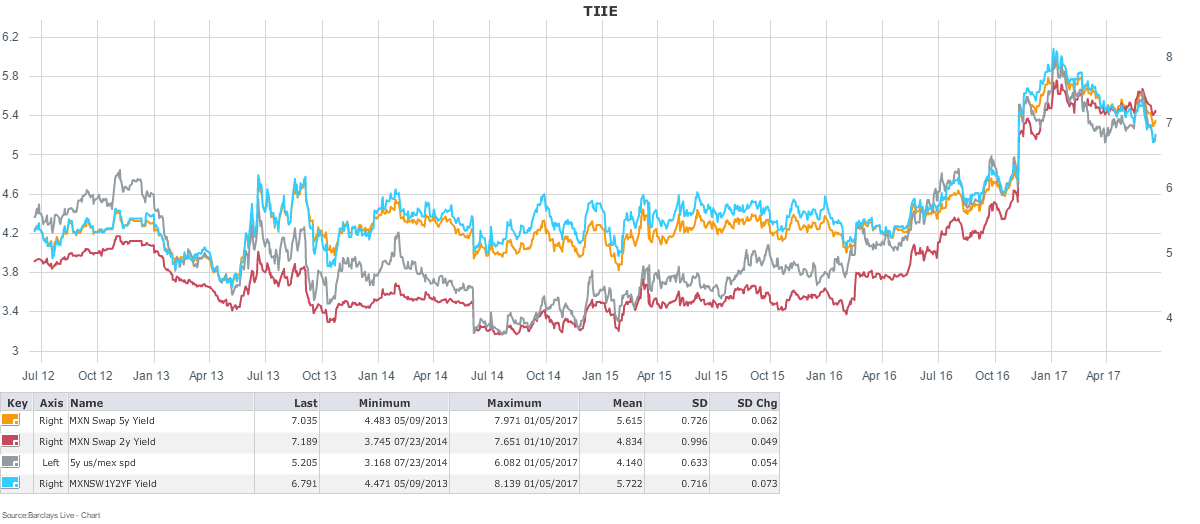

What would 3% CPI in 2018 mean for rates? First breakevens would fall by at least 25bps. More importantly, I think Banxico would cut aggressively, consistent with the charts showing a stronger MXN, high current ex-ante real rate and negative output gap. If we were to assume a 2% real rate combined with 3-3.5% medium term inflation, it would not be out of the question to see the overnight rate cut to 5.5% from the current level of 6.75% (or 7%, if Banxico pulls the trigger on a 25bp hike tomorrow). With the entire TIIE curve gravitating around the 7% level, we might see another 50bp move lower if the market buys into the easing cycle.

The 2-5yr segment is the sweet spot of the curve, specifically the 1y rate, 2yrs fwd, which is hanging around 6.80%, implying the overnight rate will be just a touch below current levels by that time. Should inflation return to a 3-handle, that would imply real rates still near current levels, which is out of step with labor market slack, a negative output gap, and a continued trend of low global interest rates.

The 2-5yr segment is the sweet spot of the curve, specifically the 1y rate, 2yrs fwd, which is hanging around 6.80%, implying the overnight rate will be just a touch below current levels by that time. Should inflation return to a 3-handle, that would imply real rates still near current levels, which is out of step with labor market slack, a negative output gap, and a continued trend of low global interest rates.

Certainly the Fed and the presidential election are risks. The election is particularly tricky, because it is tough to see Banxico cutting aggressively in front of that event in July 2018. But what I think is the real driver here is the reluctance of investors that got burned over the past year to buy into the idea that rates can come back down, especially with structural reforms bearing fruit, listless growth, and commodity prices grinding lower. We’ve seen it happen already in Brazil and Colombia--next it will be Mexico’s turn to cut.

Shawn

TeamMacroMan2@gmail.com

@EMinflationista

10 comments

Click here for comments"Ok stick with me gang"....Your sweet, Shawn. No worries about the rates. I just want to know for tomorrow at Ascot what was the B grass like this morning when sprinting up with the markers out 20 meters. Is the B grass still for kids even before sunlight? With the 'noted' riders going around Sydney at the moment how can you follow the form and bet with confidence if they turn up at Ascot for the day if they cannot even get around the B grass for "kids" track without pulling a horses mouth through its ass.

ReplyFabulous work, Shawn. Thank you for this, especially the breakdown/analysis of CPI.

ReplyQuestion on UK politics. I read the following commentary: "A leadership contest in the current circumstances would be savage and rancorous, leaving the Conservatives dangerously weakened in another general election that would soon follow." Is it clear to anyone here why another election would soon follow? After Grenfell, it would seem suicidal for the Tories to hold another election now, and I don't see the DUP forcing one (since they detest Corbyn). Please set me straight.

Thanks Johno--I read that as well, I could see where there could be another election but not under the circumstances where the Tories are "dangerously weakened". Even if polls suggest a new PM has more credibility and Corbyn again steers the Labour ship into the rocks, it seems unlikely a new PM would push his luck with another election to consolidate power after this last fiasco. Most likely scenario looks like this government limps along through an ugly spell of Brexit negotiations.

ReplyOn a related note I'm going to take a look at the move in EUR. I've been noting a lot of articles like this one lately...anyone have a view there?

https://www.bloomberg.com/news/articles/2017-06-20/remember-the-stunning-dollar-rally-in-2014-now-it-s-euro-s-turn

Re EUR, I have some thoughts. The "stunning dollar rally" of 2014 had more to do with EUR rates going negative and the BoJ doubling down on QE than US rates doing anything (went sideways). The taper tantrum of 2013 moved the intermediate-to-long end of the curve, but didn't move the dollar much -- it's short rates and not long rates that move FX (at least in post-GFC regime). That's worth bearing in mind when people suggest an ECB QE tapering in 2018 will drive EURUSD higher.

ReplyI do think there’s an incipient narrative shift, where perceived superiority of the Anglo-American model to Continental European one will flip. Edward Luce wrote a good editorial on this in last week’s FT. As I think about it, the deficiencies in the Anglo-American social contract are coming into view now and a desperate middle class is prey to populists. First they try the populist on the right, Trump and hard-Brexit Tories/UKIP, and when those fail, who’s to say they won’t try Sanders/Corbyn-type populists of the left. That makes the Anglo-American countries almost un-investable on longer time horizons. (PS: anyone have a good, capital efficient way to bet on much, MUCH higher top bracket tax rates in the US from 2020?) Now look at Europe. Arguably, France can only get better and the untapped human capital there is amazing. You have Macron. In Italy, 5-star got clobbered in local elections, and its politicians are now saying they’re not really serious about a euro referendum. In Germany, you just had a big shift in Merkel’s rhetoric (“could support the appointment of a Eurozone finance minister and a common budget if certain conditions are met)”. See the latest WSJ article on that. A euro-zone breakup – which would be a Lehman-like event and is the biggest strike against investing in Europe long-term – will look much less likely if Macron delivers on reforms this fall.

That incipient regime shift is arguably in the EURUSD price, however. It’s now trading above what regressions on short-term drivers imply. I took my long exposure off at 1.12-ish. Any favored bets on the French domestic economy?

Crude – looks like market is just going to push lower until OPEC deepens cuts?

I better get this one out of the way. If any horse trainers out there that I knew personally or thereof, back in the day when I was able to ride one and lead one than...NO, I'm not interested....YOUR PART OF THE REASON I LEFT THE F$#kIN industry!

ReplyNeed to put in a few words on retail here before I go completely off grid, unable to post with very little internet reception. I am going to shock the gang here and say I covered most of my retail shorts (XRT, ROST, TJX, WMT) at close today, reversed and actually went long XRT leaps and also shorted AMZN via put spread. Still short ULTA and LOW.

ReplyNo, I don't think all troubles are behind the industry. But I think that today's WMT's anti-AWS announcement is a warning shot to AMZN, a beginning of a large-scale assault on their bread-and-butter biz. I expect many others to follow WMT's lead and attack AMZN cloud svc. I expect the brick-and-mortar execs to form a pact (quiet one or public, doesn't matter) to fight the internet goliath. Win or not, I expect them to take a huge toll on AMZN and its ability to: 1) gain the meaningful cloud market share from here on (hit them where it hurts the most), 2) continue to be viewed and valued as an exclusively online retailer (especially after its sudden foray into the actual brick-and-mortar segment it was supposed to destroy altogether), 3) and not being asked a single question about its profit margins (which there are NONE right now) once their "gaining of market share" game is over.

The Prime Wardrobe is nothing new, btw, there are bunch of companies which already do that (TryOuts, Ayr, JackThreads, Cocodune) and now AMZN is competing with those folks, who (like I said before) have nobody to report to, nothing to be accountable for, and have no public investors who at the end will care about the bottom line. The service is a flawed thinking that ladies will not return much stuff and keep the most. Wrong... Ladies like to wear a piece of clothing only once and return it. AMZN is giving them a dress for a night! Many dresses, that is. Tags can be removed and/or hidden while the item is worn and then put back on the item to be returned. This is plain silly. The only reason they are doing it is to put the competitors out of biz, it's clear as a day and night. Or throw the stuff up the wall to see what sticks, something they've been doing for 20 years.

The possible NKE announcement to sell directly on AMZN is a big mistake (on Nike's part if they decide to do it) and will drown NKE in fake stuff sold online and AMZN sports line which is still coming full steam and will compete with NKE side-by-side. Meanwhile NKE spot will be taken on the local shelf by someone else and retailers will not return to them no matter what as the customer's perception of brand will be diminished with less sellers and representation. So short NKE on this (target $40).

Groceries... What a big bunch of garbage! No margin biz about to get even worse. AMZN buys WFM's retail pads for $32M each and calls it a drop-off/pick-up location for online sales? What in the world of madness is everyone smoking? I am on my third drink here but I am still sober to understand this is a huge load of crap only possible in this la-la land stock market. No details at all on how this acquisition helps the online strategy, zero projections on numbers, absolutely no explanation what the plan is and if there is even one at all! I am not sure anyone has any freaking idea what will actually happen and the overlap of their own customers who they would acquire in WFM, but because Bezos is involved we don't dare to even ask. I mean the guy is about to fly off the face of the earth. Just give all your money to him, go home, lock yourself in a dark room with an internet device and never leave as he will deliver everything, including hot coffee for all I know, right to your door. I am pretty sure this will end badly. I am loading up on KR here and have GTC orders to buy more below $20. And who says WFM is not going to listen to a possible rival bid? Bought some WFM calls. Someone will make it very expensive for AMZN to acquire WFM and there goes the whole food strategy (pun totally intended) or lack thereof.

I'll see you all at the end of August.

Nice move in Shawn's MXN rate trade, today.

ReplyI'm getting bearish, guys. Cue the trolls. Have been cleaning up the book and now starting to look for bearish trades in IG credit space.

Fed is going to start shrinking b/s in Q4. ECB has tapered and will start "tapering" if they get just a couple improving core inflation prints. Arguably issuer limits mean they'll be forced to taper sovereign QE in 2018. BoJ is stealth tapering. BoE is done. China is tightening and the credit impulse has peaked, its banking system is arguably too stretched to support higher credit growth, and if there were a time to persist in cracking down on excess, it's after Xi consolidates power this fall. And back to the US, once the debt ceiling is resolved, Treasury likely rebuilds reserve balances, sucking out dollar liquidity.

At 9.49, shorted EURNOK with tight stop. We'll see. Not sure who's more tired -- you hearing about this cross or me trading it.

Most likely scenario looks like this government limps along through an ugly spell of Brexit negotiations.

Replygoldenslot mobile

GCLUB มือถือ

Berkshire Hathaway got a big discount on the Home Capital placement and the C$2B loan was in part to replace an existing credit facility. The only thing that doesn't completely match up with Buffet's moves in 2008 is that he didn't buy some hybrid equity.

Replyดูหนังฟรีออนไลน์

ดูหนังใหม่

รีวิวหนังแอคชั่น

whoah this weblog is wonderful i like reading your posts.

ReplyStay up the great work! You know, many people are looking

around for this info, you can aid them greatly.

ดูหนังออนไลน์