The whiplash continues.

Just when it all looked like going horribly wrong for just about everything, the benign US trade figure prompted a surge in the dollar, and the subsequent upward revisions to Q4 growth (gee, 3%-ish growth seems awfully high for a recession) helped spur a recovery in stocks and risky EM currencies.

The overnight session has featured a continued rally in high yielding currencies (thanks in part to a strong employment report in Oz) and a concomitant collapse in funders. The yen is particularly interesting in this regard, as so far this year USD/JPY, EUR/JPY, NZD/JPY, etc. have all eclipsed their 2006 highs. For the past twelve months, 120 has been a severe resistance for USD/JPY, and after a significant battle this morning, the level finally went.

Just when it all looked like going horribly wrong for just about everything, the benign US trade figure prompted a surge in the dollar, and the subsequent upward revisions to Q4 growth (gee, 3%-ish growth seems awfully high for a recession) helped spur a recovery in stocks and risky EM currencies.

The overnight session has featured a continued rally in high yielding currencies (thanks in part to a strong employment report in Oz) and a concomitant collapse in funders. The yen is particularly interesting in this regard, as so far this year USD/JPY, EUR/JPY, NZD/JPY, etc. have all eclipsed their 2006 highs. For the past twelve months, 120 has been a severe resistance for USD/JPY, and after a significant battle this morning, the level finally went.

What is interesting is that a rising (risk) tide does not appear to lift all boats, as Asian currencies other than the CNY have generally fared poorly overnight. There appeards to be differentiation going on, with high yielders substantially outperforming their low yielding brethren. However, Macro Man wishes to wait a bit before plunging into the beta plus carry trade. If 2007 has taught us anything, it is that we cannot rely on yesterday's "break" to follow through today. This time yesterday, everything looked horrible. Today, everything looks great. The reality? Probably somewhere in the middle.

2 comments

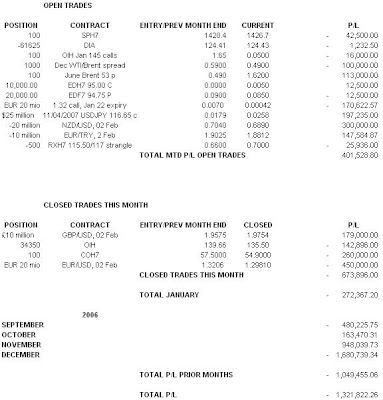

Click here for commentsI get a kick reading all these "savants' who forecast a recession

ReplyRitholtz , Roubini and their merry band of knucklehead followers , who lie in cash and stay out of the markets thinking a real-estate inspired depression will crush all asset classes

they get duped and end up losing $ by being out of the markets

so sad

Well, there is no crime in being wrong; I am wrong on economics and markets all the time. Ritholtz and Roubini are both smart guys who have done some thoughtful and interesting work.

ReplyWhere I think they can be fairly criticized is a) for sensationalism in forecasting, though I suppose no one pays for a guru who delivers boring forecasts; but more damningly, b) for failing to consider alternative outcomes despite the emergence of evidence that such outcomes might in fact occur. There appears to be relatively little "what could I be missing" from those guys, and a lot of "isn't housing awful."

I try and never get angry with myself just for being wrong; if I have weighed the evidence carefully and simply miscalculated, so be it. Where I am hardest on myself is when I persist in error through willfully ignoring danger signs, whether it be economic data or price developments.

In my experience, the best traders and forecasters spend more time figuring out where they can go wrong then high fiving themselves when they're right.