Unless you like in a desert or arctic tundra, it is probably a cultural norm to make small talk about the weather. And eventually, it will come back to the forecast. Weathermen can get tomorrow’s temperature right (most of the time), maybe predict if there will be rain or snow two days out, and maybe get a general idea of what the weather will be like five days down the road. While forecasting has improved over the past few decades, it is a complex system: medium-term forecasting is still largely educated guesswork at best.

Yet we persist in maintaining the myth of inflation targeting. Do central bankers have any better idea of what inflation will be a year for now? Do they even know how to measure it accurately? Has the craft of forecasting inflation a year forward improved over the last thirty years? Consumers in Mexico, and countless other countries just in the last twelve months, can answer with a resounding, “no”.

And even the monetary chieftains did know how to forecast inflation, would they know what buttons to push to move it to their “target” without unleashing a series of potentially catastrophic unintended consequences?

This issue stepped to the fore on Monday when the great monetary minds of the world converged on Washington DC for the Brookings Institution Central Banker Jamboree. The title of the event was, “Should the Fed stick with the 2 percent inflation target or rethink it?”

San Francisco Fed President John Williams was on the tape in the WSJ supporting price level targeting, which is the idea that if you undershoot the inflation target, no worries...you can just make it up later. A previous speech he had this to say about price level targeting: “In a nutshell, the big advantage of this approach is that any surges or drops in the inflation rate need to be made up in the future. This assures that, over the medium term, inflation stays on track, even if policymakers have a very imperfect understanding of the levels of natural rates or other structural changes affecting the economy.”

But what if they have a very imperfect understanding of inflation? What if they are measuring, just to pull a random example, the annual change in US personal consumption expenditures, but low interest rates are driving crazy amounts of borrowed money into a wide variety of assets, both real and imagined? Would the Fed still be madly shoveling fuel into the QE blast furnace?

Yet the central bankers of the world look at the world, stroke their beards, furrow their brows, and think about how they can solve this problem--and manipulate the price of money so they can get it just right. In a 20 trillion dollar economy comprised of a system so complex it can scarcely be measured.

And then there’s the “look through”. How many times have we heard the Fed--or any central bank of your choosing--is going to “look though” this spike in oil prices, or the fall in telecommunication prices, or the rise in medical costs, or the transitory pass through inflation from the depreciation of the currency?

As if on queue, after the price level targeting trial balloon took to the skies on Monday, the BIS published a working paper with this clickbait headline: “Global Factors and Trend Inflation.”

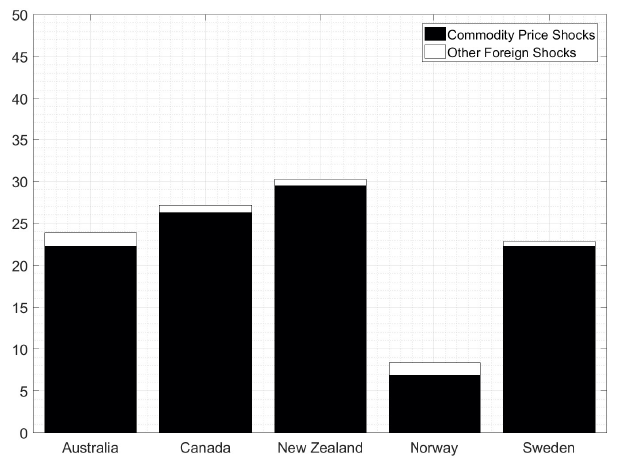

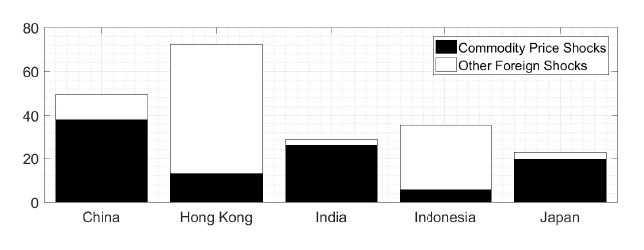

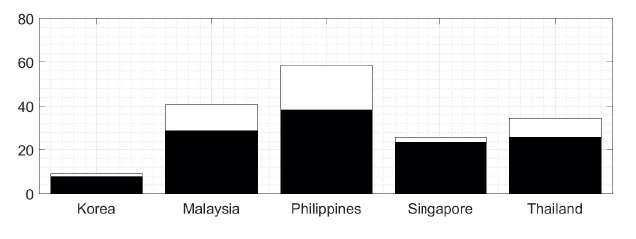

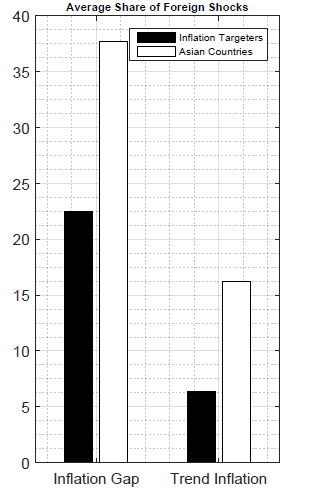

The paper seeks to quantify how much foreign factors--mainly commodity prices--impact domestic inflation in an handful of inflation-targeting countries and Asian exporters. Here are the results:

Put another way, with a couple of exceptions, foreign shocks drive 20-40% of inflation depending on which country you’re talking about. While these shocks have less of an impact on “trend inflation”--or the long-term inflation average we might expect to see priced in breakeven prices--they are a huge, and completely exogenous, factor for domestic monetary policy within any predictable growth and inflation forecast horizon.

The authors of the paper see this as a victory for inflation targeting: price shocks hit short-term inflation, but have little impact on the trend. So you can ignore them. I find it disconcerting--how confident can you be in a trend when 20-40% is indisputably a random variable beyond your control? And doesn’t this approach implicitly assume the random variable of foreign shocks is 1) random, and 2) mean-reverting? Both of those assumptions are tenuous at best.

Yet 2% inflation, or 2% annualized over time immemorial, or some other number chosen from on high, is the right number to manage to.

John Taylor got into the mix later in the week as his Taylor Rule got batted around like mouse in a village of feral cats. And it bordered on the sensible:

“First, there is a danger in the way that the numerical inflation target has come to be used in practice. It seems that even if the actual inflation rate is only a bit below the 2% inflation target—say 1.5% or 1.63%—there is a tendency for people to call for the central bank to press the accelerator all the way to the floor. This is not good monetary policy; it is not consistent with any policy rule I know, and it could create excesses or even bubbles in financial markets….”

Price stability and financial stability. That is a better recipe for keeping the Fed from blowing bubbles rather than anything I’ve heard from John Williams, Ben Bernanke or even the “screw it, let’s just raise the inflation target for a while” argument made by Larry Summers.

Look, I’m an economist by training. I respect what these guys do, and I admire their quest to improve monetary policy. I’m also a trader who sought to make a living with a 60% hit rate on my predictions and forecasts. Macro trading, weather forecasting and central bankers will always have gods and liars that claim or promise a higher hit ratio than that. But being “right” a lot is really, really hard. As Nobel Prize Laureate Richard Feynman once said,

“I might be quite wrong, maybe they do know all this ... but I don't think I'm wrong, you see I have the advantage of having found out how difficult it is to really know something. How careful you have to be about checking the experiments, how easy it is to make mistakes and fool yourself. I know what it means to know something. And therefore, I see how they get their information and I can't believe that they know it.”

We should take it easy on the weathermen and the economists. They are seeking to quench the very human need for control. Central bankers are doing the job we ask of them--maybe we just put to much on them. Like with most things in life, a little humility can go a long way. Take Taylor’s advice and manage around rules, not numbers.

Shawn

TeamMacroMan2@gmail.com

@EMInflationista

Shawn

TeamMacroMan2@gmail.com

@EMInflationista

9 comments

Click here for comments"Should the Fed Change blah blah blah"

ReplyThe ((FED)) should stick to the weather. Some have learnt, and some are learning, and the rest are about to find out how our ((fed)) bubble market ruins investors and traders lives first hand. Welcome to main street ((assholes))

glad we agree! Not just the Fed though. It is central bank gospel.

ReplyMaybe it is the subject of another post, but I do think there is value in inflation targeting for EM central banks, especially those with an imprinted history of monetary recklessness.

You see that weather man. His recklessness was a laugh a minute. I think I was having dreams on that level when I was ten! If I told you the dream I had last week you'd have triplets! and being hitting the casino with the houses.

ReplyInflation targeting most definitely causes policy errors; Stanley Druckenmiller spoke about this on the teevee last year.

ReplyHowever, one needs to understand the mentality of central bankers... Look, these are guys who spend most of the day sucking each other's dicks - if you're expecting forward-thinking macro-economic policy, or even good old fashioned common sense, then a central bank is not the place for you. Also, did their mothers never tell them it's rude to speak with your mouth full?

Those who took the gold trade on a breakout above 1,326... I am scaling out of 1/3 here and moving the stop up. I think it is going way higher on the US dollar dump.

ReplyI note the Spoos gains last couple of days are now against the backcloth of some tapering off in breadth. Doesn't usually signal an immediate reversal for Spoos ,but it is the first signal that some profits are getting banked and remaining gains are getting more narrowly focussed.

ReplyI remember running the numbers on the contribution of FANG stocks to overall performance in the spring and it was disturbingly high--what marks this most recent move higher in stocks since about November is the macro factors: tax cuts, strong consumption, high profits, higher commodity prices, higher investment. It is the type of confluence that we haven't seen in a really long time. Bloomberg wrote an article headlined something like, "Wall Street is Gripped by FOMO". I could see a reversal/consolidation in that environment--and I don't doubt the technicals might show that-- but I think this rally has to be killed, not die of old age.

ReplyStocks are never going down again in our lifetimes.

Replyglad we agree! Not just the Fed though. It is central bank gospel.

Replysbobet

ทางเข้า sbo

ทางเข้า sbobet