Now that the market is taking a bit of a breather from shoveling USD and its fixed income products onto the bonfire, we can step back and take a look at one of the late 2017 themes that may--or may not--be starting to play out in 2018.

The US tax reform has exited the sausage-making process and gone into effect. We are starting to get the headlines about the impact: last week it was retailers like Walmart promising bonuses and wage increases, this week, Apple--that bastion of far-right economic conservatism--is pledging to Make America Great Again:

Did anyone check Tim Cook’s tax returns for donations to the Trump campaign? Just askin’.

Yet with all that money comin’ home, a funny thing happened on the way to making America Great Again. The USD has gotten whipped like a lame horse:

So what gives? Aren’t companies like Apple repatriating billions of dollars from overseas? Why isn’t the market pricing in that flow back into USD?

This theory--that cash held offshore was somehow by definition denominated in another currency--is an argument built on a sand foundation. Indeed, today an article on FT Alphaville noted something crazy--Apple manages one of the world’s biggest portfolios of corporate debt from an office in Nevada, but the custody of this massive pile of assets is in Belgium, Germany, or some Cayman holdco. And most of that is in or hedged into USD, even if it is in a metaphorical German bank vault.

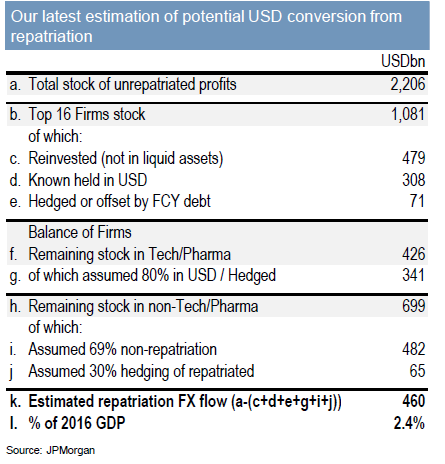

The particle physicists that keep track of these things at JP Morgan seem to agree. Earlier this week their research team published some estimates of the stock of offshore profits, how much could be repatriated, and where it is held.

By their estimates, of the $2.2trn held offshore, only $460 billion of could potentially be repatriated as an FX flow--15.5% of that would be lost to taxes--leaving $400 billion to come back over a number of years. For FX markets that qualifies as a drop in the bucket--especially when dealing with corporate treasuries that have no pressing need to do this trade tomorrow--they can take their time and drip it out in $10mm sell tickets every day for two years.

The bigger change that the Apple move illustrates--and alphaville highlights--is the potential for this “cash” to go back to shareholders. The offshore cash isn’t really cash anyway--more often it is held in high grade corporate debt. More than any potential change in the structural value of USD, these moves by corporate treasurers--combined with higher rates-- might mark a regime change for inflows into IG corporate markets, and a low in high-grade spreads.

Or maybe we’re in 2004….the point is not that this change in flows into corporates is going to blow spreads out to UST+300bps overnight, but the demand for paper to continue spread compression might have dried up. As FT Alphaville points out, there’s no reason why Apple--or any other company with billions of offshore profits-- needs to fire sale these assets, and there are still investors tripping over themselves to reach for yield in some of the world’s weirdest and fragile economies. (insert your own “Trump as EM bond portfolio manager” joke here)

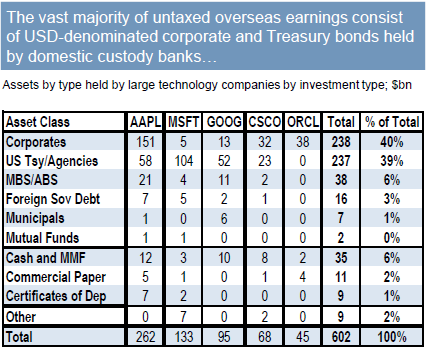

The bigger piece of the puzzle is indeed the quantity of foreign profits already held in USD--because this is what could come back and get sold into the market or allowed to run off into cash to be paid back to shareholders. JPM highlighted this chart for illustrative purposes--showing the known allocations of a few tech giants which are probably managing their portfolios in a similar way to other corporate treasuries.

These five companies comprise roughly ¼-to-⅓ of the total stock of offshore profits, meaning there could be $600 billion in corporate debt and and equal amount of US treasury and agency bonds that could--if not hit the market--not be available for re-investment at maturity. Sure, these are huge markets as well, but even if you parcel out $600bn in these markets over five years, you’re still talking about a significant amount of supply that will need to find another home.

So what’s the trade? I think this is another reason to flee high-grade credit risk, and while the tax windfall for the federal government will pad the fall for UST and agency borrowing rates, again--it is just another headwind for rates at large.

Sure, if global growth rolls over or if inflation catches fire later this year this type of flow won’t mean much for the direction of rates--the broader point is that the key flow from the US tax reform is in corporates, not FX. The long-term risk-adjusted returns for corporate credit are bad, and the flow outlook just got worse too. Sad!

Shawn

TeamMacroMan2@gmail.com

@EMInflationista

Shawn

TeamMacroMan2@gmail.com

@EMInflationista

41 comments

Click here for commentsBucky seems to have a foothold here. It is usually time to buy whenever the media begins shrieking about a falling dollar. No doubt that noted FX strategist Gisele Bundchen will demand that the Patriots Tom Brady be paid in € again.

ReplyOil is topping out. Wages are going nowhere, as the market for low-skilled US labor remains anything but "tight". M2V remains at historic lows. China is expanding in one area only - its capacity to lie about its economy. The latest round of the inflation scare will soon have run its course.

Cue a steady rally in USD and another round of the flattener in bonds as the short end of the curve remains relatively static but those delicious 10y and 30y yields prove irresistible to yield-starved European and Japanese investors. The last auction of 10s and 30s was rock-solid in the face of deafening media noise about a bond bear market blah blah blah.

The big losers will be cryptos, metals and miners, AUD/CAD, and a variety of your favorite reflation vehicle equities (e.g. banks).

well considering global QE is winding down, I couldnt agree more on a short credit story. even if growth stays strong, spreads are only going to tighten so much.

Replyand how many more stienhoff's or Altice's do we need to see how distorted rates make thier real effect.

A lot of global growth FX (AUD, CAD, KRW, TWD, SGD etc) arent moving as much as euro in the past few days, though MYR is on fire. BBDXY or trade weighted dollar hasnt broken new lows yet, though its right on it. Not holding my breath for a dollar bounce this time, but does seem a little too obvious. I havent heard anyone bullish the dollar. stock markets bull dont care and are more worred about growth and bond bulls and bears see a lower dollar too, at least from my take. Pretty odd.

hang seng looking to take out the 2007 top. thats the one to watch

I go back to the chart and I don't question how and why DXY is at a 3-yr low here. I do agree that it's getting a bit crowded in the room, but this alone won't change the thesis. I am not married to the trade either. If I get the call to let it go then I will. In the meantime, draw the lines and shoot for them until you are told otherwise. Connect the 2011 and 2014 lows for a trendline, then combine with 2009 and 2010 tops horizontal to form a laminate support @ 88 - 88.50

ReplyI ain't gonna piss against the market and look into a 2-handle abyss. Staying short and trailing the stop.

According to JPM, the last reading for G4 commercial balance sheets was at best 3trn. That figure was 5trn in 2005 and peaked over 8trn in 2007. With yesterdays' announcement that post crisis restrictions on US Banks' balance sheets were about to be rescinded, there could be plenty of places to park that debt. That announcement was a game changer, and just added another half life to the Fomomentum.

ReplyThe one sign you'll know when we're at the top of the "greatest bull market" in history will be when the Macro Man Team starts sanctioning "hedgefund managers" opinions on the matter. Back to work.

ReplyThe Fed announcement was indeed a game changer. My gut reaction was to think of the tugboat sized anchor that would throw onto swap spreads, but the impact on risk-taking, FOMO, credit, yield grab, etc. shouldn't be understated.

ReplyI've been blissfully outside the sell-side noise, but I would guess the banks don't want to make too much noise out of this clear chance to start juicing bonuses, especially during a govt shutdown.

An amusing morning of going through the futures indices , and I see the Sydney eastern suburbs gold market hasn't change a bit. Still man haters!

Replyhttp://www.dailymail.co.uk/news/article-5165877/My-Kitchen-Rules-2018-contestants-kicked-revealed.html

Hard to argue with under-weights in HG credit. QE winding down, repatriation flows, higher rates, and historically starts widening out before stocks top. Maybe an interesting space to look for hedges ...

Replyjohno, the players can argue all they like. Its amusing. The Morgan Stanley investor weightings are a waste of time in the "greatest bull market" in history. Why?.....that's easy, the players at the top end of the town have not, and will not do anything but invest in the lower end of the spectrum of hedgefund managers in the " greatest bull market " in history because that way they can undermined and control the direction of the portfolio delta hedges at a arms length as they holiday on the Gold Coast and aspens. Its that easy, if you can pull it off!

ReplyFull stop on WTI. That was a bad trade.

ReplyAnd I don't mind revisiting WTI short on a break of 63. No fighting new highs here. Should this be the stop scoop and a double top then 63 serves as a neck. Wishful thinking, let the chart develop. Trade what you see.

ReplyBid to cover ratio over 3.0 for the 2y auction today, very strong indirect bid for the first auction of 2y at > 2.00% in a long while. This comes on the heels of strong auctions of 10s and 30s earlier this month. That BTC alone might make holders of the enormous US10y short position a little nervous. 5y auction due tomorrow.

ReplyThe smart money can park there now anywhere along the curve in USTs and collect 2, 2.5% or close to 3% interest - while credit markets are wondering whether Greek 2y should really be trading at lower yields than US2y and the rest of us are watching the momo fomo show that is US equities, with or without popcorn.

IPA - you will be right soon, crude has rsi > 75 and everyone is long. That trade is going to run out of new participants.

Btw, does anyone know if there was vol (put) selling and then a spike in call buying in the late stages of the Nasdaq bubble? I wasn't involved in equity markets at the time, maybe someone here knows.

ReplyVix curve is flattening and spot is rising, even as the market drifts upwards. Very unusual.

What about 1987? Did anything like this happen before the Crash? Is this an old story of blow-off tops, or is the scale of short vol so large that it is now a brand new market dynamic that never existed before?

I hear you, @LB. Market can remain irrational longer than I can remain solvent. I will go short WTI on the reversal signal as soon as one presents itself. It was a tester, a wrist slapper, my bad. Agree with you on the last gasp look of it.

ReplyOn vol... This indeed may be the first widespread leveraged prolonged short vol occurrence (with LTCM partially in mind) and we'll get to witness (and hopefully successfully participate in) how it unfolds. I am not sure I can help to solve the puzzle though. Tried SVXY puts for a bit, got 1/3 off at a profit but the rest have expired worthless. Need to be patient here. Pretty much going back to the second sentence of this comment - not gonna piss against the wind. This being said, once the train derails it will make LTCM look like a walk in a park.

VIX calls are probably a better play than SVXY puts... capture more of the blowout.

ReplyLong SVXY + VIX calls is nicely assymetric.

There are some fairly frothy things in Australia at the moment.

Companies listing with 300k revenue and landing +$700m valuations. One came unstuck over the weekend.

Interesting to see crypto roll over, VIX slowly rising, the first of these hype plays unwind.

http://www.fraziscapitalpartners.com/getswift

Remember when we thought USDJPY was coupled to Spooz? That correlation went out of the window a while ago, apparently. DX down again this morning as Mnuchin forgot that the Treasury secretary is supposed to support a Strong Dollar Policy. LOL.

ReplySpoos up, VIX holding firm. Another (anti)correlation breakdown. The weirdness continues, almost as if nothing changes now - except that leverage and margin debt are tweaked incrementally higher every day before the market opens. It's getting late...

VIX now up 4% on the day, presumably as MOMOs and FOMOs scoop up calls… this is officially getting weird.

ReplyTaking off 2/3 of DXY short here. Splitting the remaining 1/3 in two with 88.25 as first scaleout and second half to run lower as long as 84 target or trailing stop is hit.

ReplyAlso, I am trying to short NQ at 6960-6970. Hoping for a quick retrace to that s/t resistance today or tomorrow. Time for equities to take a breather, imho. Things are rolling over a bit. Stop above the high and targets are 6850, 6790, 6690.

Well done on DXY, IPA. You're our hot hand!

ReplyI have been in a massively-agitated state the past weeks over the dollar. Reluctant to go outright short, but buying option structures like worst-of USD puts against non-USD reserve currencies (when the US is stirring trade frictions, non-USD reserve currencies historically do well). Worked today. Also re-engaged with USDJPY but covered just now. Sadly, I never traded the US 10Y / USDJPY hybrid I mentioned here. An absolutely awesome trade missed.

As an aside, USDTHB has been interesting. I re-engaged with that one after reading https://www.cfr.org/blog/thailand-really-and-i-mean-really-close-meeting-treasurys-manipulation-criteria

See mention of volatility above. Not my wheelhouse, but noticed UX1 vs UX3 spread (ie roll) has tightened and UX3 is around the lows of the last cycle, so I actually bought some of the UX3 (UXH8 yesterday) in tiny size, just to get me thinking more. If the market melts up and front-month starts going up driven by call-buying, owning something like UX3 becomes more compelling as a complement to my equity longs.

The big question for JPY is what happens when the 10Y (presumably selling off with global rates) pushes hard on the 10bps ceiling. So far, BoJ has been able to effectively taper, and taper by A LOT, without markets calling them on it. Will they step up the printing big-time when markets push, or will they just raise the ceiling, thereby cementing the idea that they've been tapering for >1 year without the market noticing (which would call for some kind of catch-down in USDJPY?). The other issues in Japan on my radar are the BoJ governorship (Abe still hasn't shown his hand, and if USDJPY collapses here, does he replace Kuroda with an uber-dove?) and the shunto/wages. Some have argued that the new incentives to raise wages are compelling.

ReplyBy the way, speaking of catch-downs in USDJPY, I love how everyone says "Japan is cheap" versus the US. Um, dude, if you accept that the JPY swings around PPP in the long-run and then adjust Topix earnings for that (and SPX earnings up for some over-valuation in USD still), I think you'll find there's no valuation arbitrage there.

Favorite quote of the day, as people step on each other to buy Brazil: Lula -- "I don't need the market." Eurasia, by the way, thinks all Lula appeals may only be dealt with in September.

Meanwhile, applications for SPD membership are surging ... to vote down the coalition?

Thanks @johno, I'm lucky to have a hand :)

ReplyCharts have been kind to me. Being rewarded for patience on the first 1/3 scaleout on gold here. Crazy animal is looking to go to 1400, imho. Like I said, it fakes a little and then explodes higher.

IPA, give me a break. The Dow index isn't faking anyone. You seriously think after this bull run when the dust settles down that I'm going to be invited to any "NY game" worth its salt. Come off it will ya! I'll be lucky to get the inside scoop on what island party Paris Hilton crashed last weekend! Stay strong, stay broke and f##k'em where it hurts.....money.

ReplyIPA, don't waste your money and energy on USA or UK investment schemes. There is nothing going on there. Thailand.

ReplyIPA , are you going to take investment recommendations from people that have already made their life coin , or coming out the other side of their investment journey. Their game , is not your game.

ReplyAny thoughts on a sustained VIX at the moment? Wondering if we see short-term liquidity event given that I only see news outlets talking about euphoria buying; anytime the VIX made a marginal move higher in 2017, the go to stance was "potential dip?" by mainstream. Now, with VIX move over past few sessions, still no talks of dips, only euphoria buying.

Reply@johno, worth noting on usd/jpy that eur/jpy hasn't done much. When looking back on what I wrote on the subject a couple of weeks ago, the point that there wasn't much reason for JPY to sit out the (already in progress) usd selloff was right, but the overarching theme that "JPY is cheap" has not. So yeah, i think the market caught on to the fact that there was, and should be a correlation between "stealth tapering" and higher global rates, even if that doesn't end in a material change in BoJ policy.

Replythere was a great article on Project Syndicate about Brazil earlier this week--the author, who has been following Latam for a long time, thought Lula would wind up on the ballot, basically reasoning "because that's how Brazil rolls." I think he is missing the forest from the trees--this is a generational sea change, the people, and to a large extent, the judiciary, are sick and tired of corruption and impunity and aren't going to do crooked politicians like Lula any favors. I'm sure his lawyers are going to throw the kitchen sink at this but I think the probability that he is in prison on election day is greater than him being on the ballot.

And from a broader perspective, in my opinion allowing Lula to run is not even the best political strategy to "beat him at the ballot box" as Cardoso suggests. Lula representing the left is going to push the opposition to the extremes to fight his style and rhetoric, which I think would greatly increase the chances that Bolsonaro makes the runoff. That scares the establishment....I think the political calculus would prefer to let Lula twist in the wind and count on a centrist to make a reform-minded, market-friendly case to counter Bolsonaro's populism. More on this subject next week.

p.s. I took a look at usd/thb after reading the sester article as well...I didn't see a good reason to be long USD there. Maybe a decent way to lay off risk against other APAC longs? Sure, but you lose the weak dollar theme and I think you'll be disappointed if you're counting on a policy-driven shock. I'm not a great mind of THB though, so if I'm missing something there, feel free to chime in.

ReplyHi Shawn,

ReplyThank you for the feedback. I'm looking forward to reading more of your thoughts on Brazil. Despite the tone of my comments above, I am short USDBRL via a digital put, which was a bet on the appeal court ruling swinging sentiment. Still a couple days left before expiry, so too early to celebrate that one.

Re USDTHB, was short USD / long THB but covered last night around where it's trading now. Big move in just a few days. But I generally think THB is a buy because they likely trigger Treasury's tests, which maybe affects their willingness to persistently intervene. Last I checked, the Thai central bank was in a net negative equity position too. The big picture view is simply that they have a huge current account surplus and locals, despite attempts by policy to entice them, don't want to recycle much of that surplus. They seem stuck and if they step up intervention, they will trigger scrutiny.

ECB today ... reiterate they need to see sustained adjustment to inflation path to stop QE and data have yet to show convincing signs of upward trend. I'm not expecting we see those signs in the next few months, so skeptical they can change language much when they update projections in March. My guess is higher EURUSD is going to offset any upward adjustment from the economy performing better in their projections. Also have Italy in early March. Looking on BBG, the highest analyst forecast is 1.30 at YE and the forward is at 1.28 now. You just had Mnuchin trash dollar sentiment further. Upside from here doesn't seem a great bet, though I struggle to find a bullish catalyst for USD (other than temporarily running out of sellers, which gives it some lift, which then gets rationalized with some narrative).

By upside in that last sentence, meant upside in EURUSD doesn't seem a great bet from here, but struggle for the catalyst.

ReplyOh, and to call me out on a losing trade -- EURCHF not performing. When the US sullies its reserve currency status, the non-USD reserve currencies are going to get a bid, which is a pretty big sentiment swing for CHF. Probably in the price, and USDCHF is bouncing here nicely.

https://www.brisbanetimes.com.au/business/the-economy/perfect-storm-global-financial-system-showing-danger-signs-says-senior-oecd-economist-20180123-p4yyr2.html

ReplyThose who took the NQ short at 6965... Price is now trying to break below the 116-point uptrend channel which has been established pretty much since the beginning of the year. This probably will be a very fast trade, so have your exits ready to go. At this point it looks like the measured move takes the price to 6800 (but there may be an overshoot). Hourly 200 is at 6860 with tomorrow's S2 at 6852 (currently). So I think the first scaleout may be achieved tomorrow @ 6850. After that I am looking to exit at 6790 and 6690.

Reply@amps, I don't know anything about Asia. I like to stick to US. Have been trading here for 18 yrs. Don't like to meddle with stuff I don't know well.

Aakash - does feel like a regime change with higher vol and weaker dollar (so motivation to pull out of usd assets), and incredibly complacent positioning, enough to want to own some blow up. Given high short vol positioning could be big bang, not sure market could handle it, would blow up a few people, once the equity move was more than 5% the feedback loop would be mental here i suspect, so it might happen, probably wont, probably wishful thinking.

ReplyNot sure quoting perma bear AEP is worth anything, but I hope you survived 2017 Nico

Nico, how's life in your Mom's basement? Did you have fun blowing up your account and losing your life savings trying to short spooz in size 1000 pts lower? LOL! Happy days.

ReplyMy initial read on the regime adjustment in CNY was wrong. Correcting, UBS: "Does a suspension of countercyclical factor imply a change in PBoC's FX policy? No. The introduction of the countercyclical factor in the yuan fix in May 2017 triggered a decline of risk premia across RMB assets. Will the suspension of the same reverse the fortunes of the RMB? We think not. The countercyclical factor dampened the pass-through of USD TWI moves to USD/CNY, but in both directions i.e. appreciation or depreciation. That suggests as long as USD is weakening, as we expect, the suspension of the countercyclical factor could in fact accelerate the RMB strength."

ReplyI'll say this, if you used the words "risk parity" in a newspaper article in my town your editor would have you strapped to your desk and given a taste of five lashes from each of your colleagues.

ReplyNot sure quoting perma bear AEP is worth anything, but I hope you survived 2017 Nico

Replymaxbet

แทงบอล maxbet

ทางเข้า maxbet

You have a awesome article in here! Your writing has helped me a lot, thanks!!... MM

ReplyYour Blog here is so wonderful. You're great just great! Cheers for this... MM

ReplyI admire the Valuable information in this articles. Many thanks to this info... MM

ReplyI just found this blog and Hopes it continue. Keep up the great work, Thankyou!... MM

ReplyIts hard to find good ones. I have added this blog to my favorites. Thank You... MM

Reply