It’s been a long time since we’ve covered any ground in Brazil--but it is great macro territory. Brazil has so much that other markets don’t:

- Liquidity--a super tight, regulated futures market for swaps and FX, stocked with a delightful mix of domestic and foreign real money, hedge funds, and rank speculators.

- Carry--where else do we still talk about double digit interest rates?

- Stories--there’s no limit to the narrative you can build around a trade idea in Brazil.

- Idiosyncratic, uncorrelated prices. Low correlation = alpha.

What’s not to like? For starters, when the top management of one of the country’s biggest banks gets hauled off to prison for corruption, and it is the same bank, if I recall, that paid rates in massive size ahead of a surprise central bank hike because one of the executives had a “dream” they would hike….well, you have to be pretty careful who you are trading against.

All that being said, Brazil has grabbed EM headlines this year as the “Car Wash” scandal drags on. Back in May, President Temer was implicated in a bribery/hush money scheme earlier this year, local markets gapped lower on the assumption that Temer would be impeached or crippled for the remainder of his term. If that were to happen, important structural and fiscal reforms would fall by the wayside, and the country would continue to stagnate and run up huge amounts of debt.

Amazingly, despite Temer’s complete lack of scruples and the moral compass of a wolverine, he has persevered, winning a vote earlier this week to avoid being put on trial by the Supreme Court. Temer was also able to jam through an important labor reform bill. That has increased the market’s optimism about the passage of the big one--a pension reform bill that would plug a gaping hole in Brazil’s off balance sheet liabilities.

In the past I’ve alluded to the EM metaphor that “energy reform only gets done in the dark”--well, in Brazil the lights went out last year. The country is in the third year of a depression...domestic demand has cratered...Rio is broke….crime is out of control...and pension costs are bankrupting the government. Even the crooked politicians know they have to act.

But will they? That is literally the million dollar question. I tend to think Temer has some cards to play this year, despite a popularity rating of 5% (fill in your own “he’s less popular than” joke here). This is what makes Brazil idiosyncratic, and a great way to generate alpha….or lose money. I’m positive on the story--valuations aren’t particularly attractive here but if you believe the structural story will improve, there is still good money to be made here.

With that, lets go to the charts.

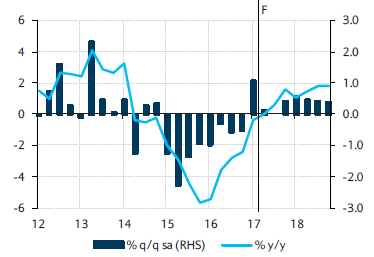

Indigestion from years of misallocated capital (to put it delicately), corruption scandals and the end of the commodity super-cycle have rabbit-punched growth for the past three years.

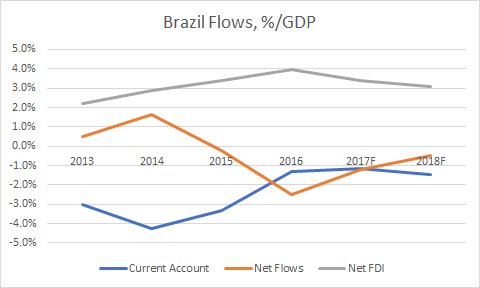

Yet the trend for growth is higher...domestic demand is recovering, and FDI never went away. As export growth has returned the flow picture has perked up quite nicely. A balanced current account and 3% FDI/GDP shows continued confidence in the country from abroad.

Most foreigners, at least in the real money “community”, express views in Brazil via external debt. This chart is a group of 5y CDS spreads on similar credits--with only Indonesia on the RHS. You can see here there is still some space between Brazil and Turkey and South Africa after the gap wider in May. Much better credit dynamics in those countries, but again--if you buy into the Brazil reform story, there is still some juice there.

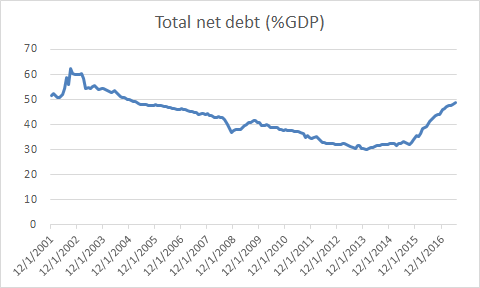

Indeed, the debt situation has gotten ugly fast...total net debt unwound ten years of progress in less than two. Keep in mind in 2002 there were fears that Brazil would be forced to default or restructure their debt!

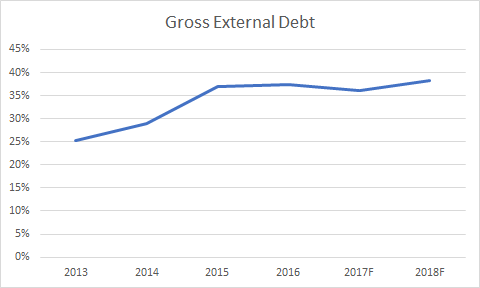

Another positive for the credit is that despite this huge acceleration in net debt, it has all been in local currency. Gross external debt/GDP hasn’t moved in three years. So a big deval in the currency doesn’t have the multiplier effect of making the debt more expensive to pay back.

A related point is that local markets really haven’t outperformed all that much over the past year, when markets had recovered from the depths of hell brought on by the depression and impeachment of President Rousseff. This chart shows equity markets have done well, but roughly in line with global markets--only with a heckuva lot more vol.

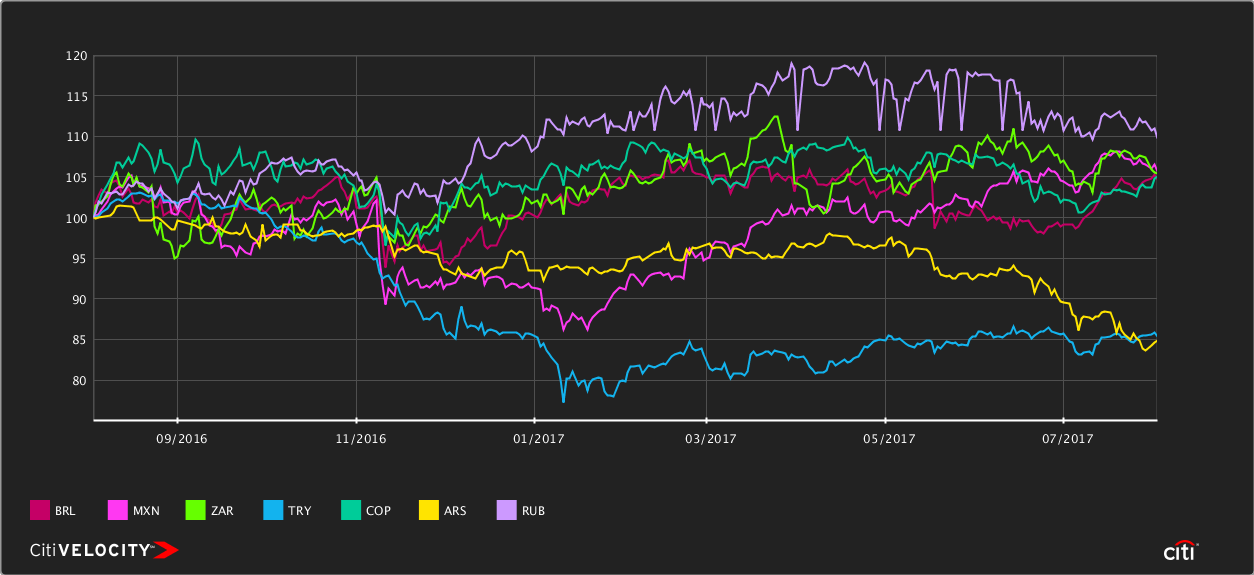

Looking to FX, BRL is in the middle of the pack for 1-year performance. Behind RUB, roughly in line with MXN, ZAR and COP (although WAY ahead of those currencies in total return, after you add in BRL’s tasty carry), and ahead of TRY and ARS. Again, good performance, but not disjointed from the EMFX rally theme of the past year.

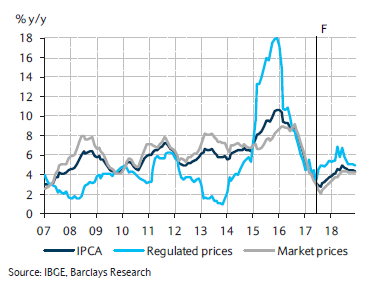

We had a little back and forth on inflation--the central bank’s target is 4.5% +/-1.5% (although it will purportedly be lower next year). If you draw lines through 3% and 6% on the chart below, you’ll see the dark blue line (IPCA = CPI) hasn’t spent much time in that interval since 2012, when a central banker by the name of Alexandre Tombini took over and slashed rates from 12.5% to 7.5%, despite no evidence of a structural decrease in inflation.

The government and it’s state-run banks took this cheap money as a green light to open the credit floodgates….a phenomenon which probably isn’t too far disconnected from the massive, endemic government/corporate corruption that metastasized throughout the economy during that time.

So yeah--while inflation has hit 3%, I don’t think this is the Volker trade. You can see in this chart that regulated prices have played a big role in sandbagging already high headline inflation in the past, and moderating it over the past two years. As the reform movement progresses there could be more hikes in regulated prices as subsidies get unwound--but on the other hand, a more competitive economy and stronger BRL would help keep the lid on inflation. Regardless...less vol in inflation, and thus overnight rates, would be massively supportive of asset prices. If a center-right reformist wins the presidency next year, that is a big possibility--similar to the renaissance in Argentina over the past year and a half since the Macri victory.

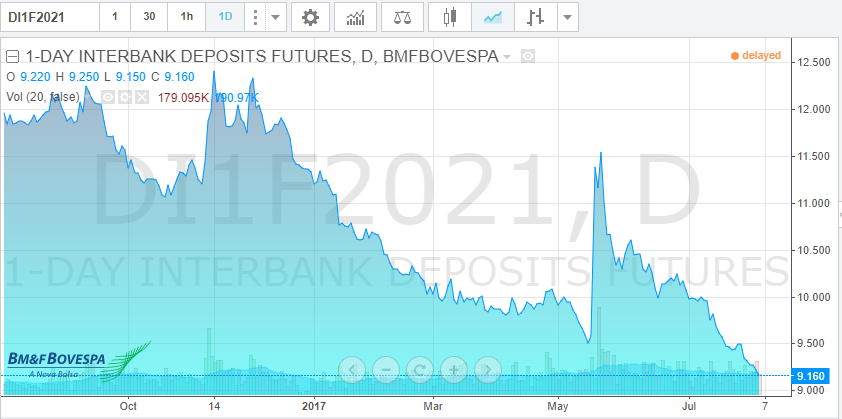

Indeed, the lower inflation figures and positive momentum on the politics has given the central bank the space to cut rates aggressively. This has led to a big rally in interest rates. The chart below is the pre-cdi Jan21, essentially Brazil’s version of a eurodollar contract.

I know, a 9-handle!! I can’t believe it either.

Similar picture in the benchmark Jan25 contact--I think there could be some value in the steepness here if we get more progress on reforms and Lula fades to black.

Putting it all together--I think there is still value in Brazil--I’ve been positive on rates there most of the year, but it is getting tenuous here with a 7.75% terminal rate by the end of the year. I’ll need more evidence of structural reform progress to buy into that--but as I mentioned I still see value in duration and real rates at these levels.

BRL...I don’t think we’re done--lay off some risk against the EMFX dog of your choice if it helps you sleep at night.

Credit--I think the first couple of charts are persuasive--while debt dynamics are still negative, and the country is likely to run a primary deficit for the third year in a row, significant reforms would fix problems other countries still have, and you have some margin for error relative to countries with problems of their own.

It all comes back to reforms. Do you buy into the story? Reforms get done, economy perks up, a centrist wins the election….Brazil is off to the races. But….Temer weighs on the reform movement like a concrete anchor, the economy stagnates, Lula wins the presidency….then we start back at square one.

I continue to be optimistic--but it is an alpha game--there will be a winner and a loser.

Shawn

TeamMacroMan2@gmail.com

@EMInflationista

Shawn

TeamMacroMan2@gmail.com

@EMInflationista

8 comments

Click here for commentsAwesome post, Shawn. Loving your work. Couple things I'm trying to form a view on in Brazil. 1) I see Meirelles saying a pension bill would generate 75% of savings originally planned while a doubter like CSFB sees 30%. A big spread! Any view where in that range a bill passes? 2) The DI curve sees about 125-130bps of cuts in the next year and then >100bps of hikes the following two years. You alluded to value in (fading) that steepness. Curious how you think about that. A call on prolonged slow growth, or structurally lower inflation and maybe lower real rates? If I assume the economy lifts, inflation stays in the middle of a target at 4.5% (a big IF given the history, as you point out) and real rates (BZSECLICA Index - BRFCPC12 Index, i.e. SELIC minus 12-month inflation expectations) go to the average since 2010 of 5.3%, then that's 9.8% nominal which doesn't make the curve look too steep. I guess the view is fiscal reform is going to improve the national savings rate and push down real yields well below the historical average. 3) How worried should we be about Lula? Last thing I read said a conviction by a higher court probably doesn't happen before the next election (so he can run) and that he's the leading candidate, with 30%. The same poll had his disapproval rate at 46%. Not sure how the process works there, but wonder whether that disapproval rate just kills his prospects (as Le Pen's disapproval rate made her unelectable in France)?

ReplyRandomness ...

APRN lays off 24% of employees 36 days after IPO'ing? What a joke!

Re the USD, some response today to NFP/AHE #s and Cohn's remarks on repatriation incentive being in the tax plan, but what most interested me was Mulvaney's flip on a clean debt ceiling bill. The sooner the debt ceiling is sorted, the sooner the USD may bottom out, IMO.

Interview of the day, for me, was Bloomberg's with former BoJ board member, Kiuchi. He's saying the banks (which have sold substantially all the bonds the BoJ has bought) will be out of bonds to sell by mid next year, at which point the BoJ won't be able to continue QE without "disruption," i.e. a massive squeeze on prices. Anyone have a view on that? Not the first time I've heard the argument, and now it's coming from this guy too. A lot of people are focused on the idea of unlimited printing to defend the 10Y ceiling in the event of DM rates rising a lot, pushing USDJPY much higher. But what about the possibility that sellers of JGBs run out next year (with all the insurance and pension funds hanging on for liability matching or regulatory reasons?) and the BoJ tapers QE? USDJPY at 90?

Paid KRW 5y5y. Will be fun to see how this loses me money, besides the egregious bid/ask I pay to play.

Yeah. Great story medium to long-term. Short-term, LB thinks we may get a face-ripper in the USD after the reversal candle we saw Friday - so this wouldn't be the most optimal moment to go Brazilian.

ReplyWe have owned some Brazilian utilities and miners since the last round of the sky is falling, and they were crazy cheap. Would be happy to load up again in the event of any local news that threatened a repeat performance.

Johno, great point there on BoJ. Punters need to get their heads around the fact that we can't have eternal buying of bonds by CBs because from time to time they are going to become the market, and thereby risk dislocation. At best the process will be cyclical, and right now both ECB and BoJ are going to be in difficulties if they want to buy more. With global financial conditions easing, it makes sense to take this opportunity to at least take their foot off the gas….

I love the idea of selling AUD or CAD against USD (or better, JPY) here. China is boxed in, can't ease, and is slowing. That's the economic driver of AUD and the source of hot money for CAD.

"With global financial conditions easing, it makes sense to take this opportunity to at least take their foot off the gas…."

ReplyWhat! What's this, LB. Noooooooooooooo, enjoy the bull market while you can. Beliiiiiiiiiiiiive meeeeeeeeeeeeeeeeeeeeeee; when this bull market is over those that stood in front of the steamroller picking up penny's on the dollar won't be heard of , or seen again I'm telling ya.

http://www.zerohedge.com/news/2017-08-04/hedge-funds-have-lagged-mom-and-pop-investors-2003

ReplyAmps-does this imply that "dumb money" will lose 300% more than hedge funds when the steamroller comes?

Skr,

ReplyDon't care. I'm to busy building my own VaR models. Once again.

Johno....I didn't get into the weeds on what's priced in, "fair value" or a neutral rate given the strength of reform, actual reform prospects,etc, ...I'm going to do a quick follow up post with some thoughts on that. Just an hour ago I got back from a trip to a huge cell phone dead zone where I literally had to use the setting sun to navigate to my hotel (there weren't even any gas stations to go old school and ask for directions). How did we travel before GPS?

Reply'Big swinging dicks' in Sweden! The end is nigh.

ReplyBrazil score big in many areas. Yet, there is potential for breakthrough. Need creative and concerted effort to reduce corruption and social problems, then hopefully would prosper.

ReplyRegards,

Susan

Internet Tv 247