TMM have noted the markedly weak performance of HSCEI and HSI recently ( HSI threatening the 100 day moving average which has been pretty good support/resistance over the last 2 years) following fairly indifferent macro data showing that not a lot has changed - retail sales are soft, CPI is trending higher and as usual it seems to all be funded by a very large expansion of wealth management products. The market is not impressed and not without good reason.

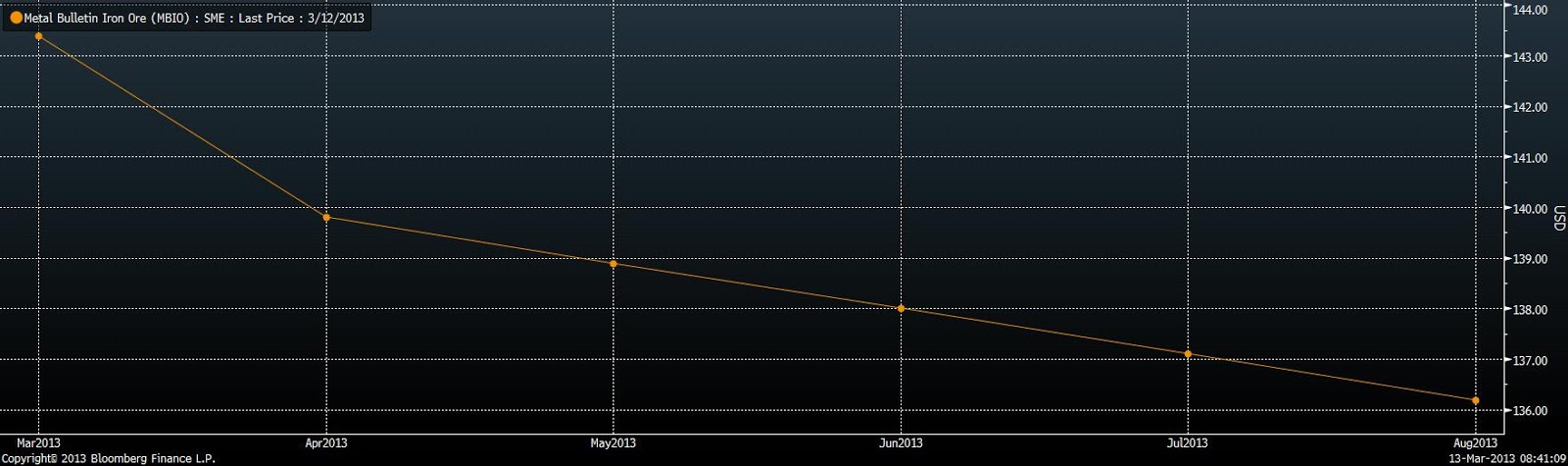

TMM have also noted that more high frequency data on power production from www.serc.gov.cn has also shown very weak power demand growth which is generally associated with weaker steel, cement and metals output. TMM don't expect the situation to improve and while betting on iron falling is pricey given the curve, it has not stopped people selling down metals and miners.

Now, while much of this is more the concerns of Australia, China and mining companies, it should be remembered that a lot of S+P earnings come out of China - enough so that comments like this from the March Beige Book gave us pause: "A contact that supplies material for filtration says the global picture is difficult to pin down because Chinese New Year and the seasonal Christmas shutdowns in Europe made year-on-year comparison particularly difficult in recent months. Finally, several respondents expressed uncertainty regarding China, with one saying that some of his Chinese customers reported dramatic reductions in sales, inconsistent with government statistics."

To that end, TMM are not that shocked at how certain parts of the S+P with large shares of non-domestic sales are having a tough time in a torrid rally - look at autos or caterpillar for example. TMM think that when putting on the "USA OK!" trade, a little more thought should be done before filling your boots with E-minis.

Going back to China, TMM think that China's seeming preference for controlling inflation is going to make this year a tough one for equity investors as liquidity gets scaled back to avoid another inflationary pulse. The more interesting trades are likely to be in markets where relative input price stability may make it possible to conduct deregulation and much needed reforms, most notably in petroleum products and energy, and ultimately more financial liberalization.

Back to liquid macro however, TMM think the recent strength in AUD in the face of this says a great deal about how much faith the market has in US activity's ability carry the world with it. We aren't so sure and especially not in Australia. TMM think that given the slew of rubbish earnings and outlooks from engineering companies and mining services companies in Australia that capex is coming off fast and that the RBA is unlikely to be a long way behind the curve.

So TMM are looking to short AUD on this bounce, but are very aware that short AUS has been a back pocket trade for the macro world for a while now. Whilst "long term investors" and rate differential players are squeezing some of those positions out in the short term, short Aud/usd spec positions still persist. So we may expand our Aud short thoughts beyond just usd and look for a counter that has great technicals - so why not ZAR? TMM are still of their "Township of the Damned" opinion on the country (and may we say - we nailed it) with its expanding current account and worsening terms of trade but, it has become a consensus now to the point of yennishness and is very crowded. The technical picture is also supportive with a very nice soothsayer signal in aud/zar suggesting now is a good time to counter the trend. We do, however, understand the risk of getting our comeuppance (Egyptian Pound longs style) for being contrary for the sake of being contrary but we think there is enough macro behind the China story to trigger a return to stronger old fashioned correlations in the markets and a wash out of some complacent positions.

Or in basic English .. "YOURS"

Finally, is it just our behavioural biases that are making us think that this week in March is particularly sensitive to turns or is there really something to it?

16 comments

Click here for commentsC says

ReplyFor technical I think the US/CAN$ is perhaps the best on offer. Not yet crowded,but longer term I really like the mix against the CAN$. RE,current low rates,and then trade shrinking factor with the US as the US develops more and more of it's own energy. CAN$ looks to me like yesterdays economic fairydust.Similar to AUD$,but the latter still has more room on rates and may yet still be geographically the better place.By contrast the CAN$ has limited options trade wise for surplanting any loss of trade with the US.

TMM, would be great if you could riddle the blog with Africa-centered post here and there once in a while. The black continent is where Alpha shall be generated over the next few years. What's your take?

ReplyOur (well documented) most recent experience in AUShort land have so far led us to relive our youth lipsyncing the aptly named "Oils".

ReplyThe time has come

To say par is par

To pay the brent

To pay our share

The time has come

A fact's a fact

It belongs to EM

Let's give it back

Why don't we dance while commos are turning

How do we sleep while our theta is burning

Why don't we dance while commos are turning

How do we sleep while our theta is burning

DD

Rampagingruss says:

ReplyIf China is rolling over the only alpha to be made in Africa in the short term will be in the short book.

We have been waiting for this data point and are not surprised to see the build in inventories:

ReplyBusiness Inventory Increases Sharply

Of course these data can be looked at in two ways: the bullish spin is that businesses held back ordering b/c of Fiscal Cliff, Storm Sandy, East Coast snowstorm or whatever you like.

The other way of interpreting this is to say, stores are pretty empty and stuff is piling up on the shelves b/c people and businesses aren't buying. Keep an eye on the I/S ratio. It always spikes up as the US enters a growth slowdown or a recession, and right now the first derivative is positive.

Bucky hits 83 today. The next big levels are 83,50 and the 52 week high at 84,05. That is a really big one as we haven’t been north of there since the 2010 version of Europanique. 85 is probably the area of severe distress for those whose livelihoods depend on putting on leveraged inverse USD trades, so we might expect to see a bit of serious unwinding if and when the resistance at 84 breaks.

ReplyThis strong dollar isn't good for companies like CAT. It means their goods are becoming more expensive just at the time when their biggest customers aren't in a mood to make big orders. In addition, it continues to crush the miners. Agree completely with C's comments on the CAD, btw. It's going to be taken out behind the Caddyshack....

II Bears now under 20. That usually marks.... well, LB will let Louis Armstrong do the talking:

ReplyYou're The Top

Of course these data can be looked at in two ways: the bullish spin is that businesses held back ordering b/c of Fiscal Cliff, Storm Sandy, East Coast snowstorm or whatever you like.

ReplyMedia Monitoring

Great post TMM, SHPROP is taking a real dive. As for short AUD, why not against MXN, another fan favorite.

ReplyI get the negatives on CAD but i dont see why AUDCAD is still so strong. China dropping is more negative for AUD vs CAD. RE in AUD is way more expensive and has further to drop IMHO.

As for ZAR, its just breaking out of short swing.

Spoo's will only wake up to the china slow down when the consumer companies slow down. Swatch sells more luxury watches in HK vs USA. These anti- cyclical luxury companies, who have seen a secular boom in demand may need to reset at some point..they are the best short IMHO, but probably not just yet

Abee,

ReplyWeak US oil and gasoline consumption + increasing domestic oil and gas production = lower crude oil and natty prices and lower US energy imports.

Draw your own conclusion regarding the relative strengths of USD and CAD.

This US domestic energy story is a secular trend that has legs. It is also happening against a slower global economy, with miles driven on the decline.

i havent done enough digging but I think the oil sands are only now starting to produce. By 2021, crude bitumen production is expected to more than double to 3.7 million bbl/d. (energy.alberta.ca)

ReplyUS is still importing close to 3M barrels. Sure the prices canada is going to get is lower bc the oil is crap and the country is full of oil. Anyways canada will be happier with the cad at 110 vs 95 but much lower than that and I am a big buyer

I want to be a market maker

ReplyI want to live a life of danger

On the LIFFE or DTB

Wherever there's cheap ecstacy

[My boyhood aspirations]

Occam's razor, TMM. Why overcomplicate stuff with zar? You don't like the Aud? Neither do I. Short into stops above 1.04 and walk away. You know it's not going much higher, and it might ping levels well below parity later on this year, once 1.01 breaks. So there's your perfect risk/reward, without being too cute with an African currency that scares the bejesus out of most reasonable macro guys, even when the rest of risk is performing well... i^i

ReplyAgreed on not being too fancy. If similar to past EUR frustrations, the explanation for AUD resilience is CBs are on the bid, one could try funding puts with AGB coupons. We partially do that.

ReplyWhen we are not busy Kevlar'ing muni funds, that is.

DD

Steel, steel

Replyhttp://www.scmp.com/business/commodities/article/1189510/mainland-china-steel-sector-facing-closures

http://www.scmp.com/business/commodities/article/1189510/mainland-china-steel-sector-facing-closures

Reply