Looking at the price action overnight it looked similar to Friday with Asia and EM getting in a panic over Europe and selling off and yet Europe calmly correcting most of it. Which leads TMM to suggest that the stories out there are not just solely Europe but are multiple and overlapping, yet the general euro wrapper is being used to encompass all.

We have had dumps in western equities over the past week, but if you were to listen to the press and hadn't seen prices you'd think we were 20% lower than we are by now. TMM's DPI indicator and newly launched WMMT indicator are certainly reflecting that with weekend conversations pointing to a disconnect between where prices are assumed to be and where they actually are with "well, we are only back to where prices were in early August" being greeted with disbelief. (WMMT = "What My Mother Thinks").

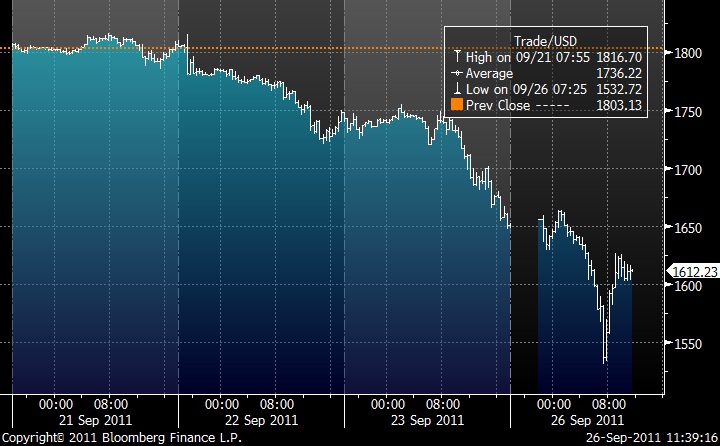

Gold meanwhile has had all the spam chuckers scrabbling in their coffers to buy the dip, though "with what?" we would like to ask, as we thought they'd spent every scrap of fiat currency on it months ago. Maybe it will be just a little longer before they can afford to return to society from the log cabins. Having said that though, the bounce does look solid. -100 and + 80 bucks of gold within 7 hours is a pretty good sign of a blow off and would have TMM normally looking to buy. But if this is a long term play we can afford to wait.

Gold meanwhile has had all the spam chuckers scrabbling in their coffers to buy the dip, though "with what?" we would like to ask, as we thought they'd spent every scrap of fiat currency on it months ago. Maybe it will be just a little longer before they can afford to return to society from the log cabins. Having said that though, the bounce does look solid. -100 and + 80 bucks of gold within 7 hours is a pretty good sign of a blow off and would have TMM normally looking to buy. But if this is a long term play we can afford to wait.

Meanwhile Asian and EM moves continue to show signs of greater self-fulfilling worries than the rest. This just adds to TMM's belief that all of this is just that deleveraging trade we have all been talking about for so long. Europe may be the story, but the effects are global deleveraging. Europe is already so deleveraged on the long side that it's now short, the UK and US appear pretty neutral, so we are left with the leverage residing in EM and particularly EM fixed income.

Meanwhile Asian and EM moves continue to show signs of greater self-fulfilling worries than the rest. This just adds to TMM's belief that all of this is just that deleveraging trade we have all been talking about for so long. Europe may be the story, but the effects are global deleveraging. Europe is already so deleveraged on the long side that it's now short, the UK and US appear pretty neutral, so we are left with the leverage residing in EM and particularly EM fixed income.

Now then, looking at this proposed IMF super package that has been the result of the Euro offsite in the States (lots of coffee, lots of networking breaks, lots of playing blackberry games under the table and plenty of trying to stay awake after too big a "get to know you" evening the night before). Well, on the face of it we have nothing concrete, but instead see the first phase of EU policy launch. Having obviously learnt this trick from the Labour Party in the UK, it involves leaking a potential idea and watching how the market reacts. If it's a disaster, then deny it ever existed, and if positive, then work in that direction. If there is one thing that TMM are learning from this crisis, it's that tape bomb shock has induced an inherent mistrust of anything being done until it is. But as we also know with this style of leakage policy, by the time it is announced it will be fully priced in, so we are therefore forced to consider the ramifications of this latest idea leak.

The €2trn has not been agreed yet but it could come either from the ECB or from just allowing the EFSF to borrow more itself. In the first case, the EFSF would issue bills that it would present to the ECB in exchange for Euro just like a bank-like financing, or it would sell those bills/bonds directly to the market. The Germans (cf Schauble) appear to be leaning in favour of that latter though at the expense of credit rating (it would act in a CDO-like manner). Which is fine as long as the German public don't notice.

On the German point, TMM frequently come across the view that the Germans, finally realising that they will have to pay, will just give up and re-adopt the DEM. The problem with this view is that both the economic and geo-political consequences of such a move - which, judging by how spookily similar the past few years' events have been to the post-1929 Wall Street Crash timeline, may well end in War - seem too much of a hurdle for them to be worth considering. Indeed, TMM reckon the Germans have overplayed their hand, and the leaks coming from the G20 suggest they have no friends. It's a case of "JUST SORT IT OUT, OK?!"

But back to the IMF idea, TMM reckon that with a fund that big, coupled with a broad based bank recapitalisation, the ECB and EFSF buying of bonds would be enough to convince markets that Italy/Spain will not suffer the Greek fate and that should be enough to give real money the nerve to reallocate.

So overall, TMM are encouraged that even if it did take the Americans to ram it down their throats, the Europeans are perhaps at last "getting it" and are actually discussing the policy responses we would want to be in place. Even the hardened Eurobears would have to take note.

But, back at home in Euroland the random word generators of the Eurocrats continue to spew out non-committal statements about what they haven't decided and what is possible with a frightening lack of what IS going to be done.

*GERMAN FINANCE MINISTRY SAYS NOT MULLING THIRD EFSF EXPANSION

*ECB'S MERSCH - WILD EXPECTATIONS ABOUT ECB RATE CUT SHOW SOME PEOPLE HAVE LOST DIRECTION, ECB HAS ONE NEEDLE IN COMPASS

*ECB'S NOWOTNY - ECB INTEREST RATE CUTS CANNOT BE EXCLUDED

*ALMUNIA SAYS MERKEL, SARKOZY KNOW WHAT IS AT STAKE

*DUTCH PM RUTTE SAYS NO PLANS TO RAISE AMOUNT OF MONEY IN EFSF

So maybe all the great ideas hatched in the Euro "offsite" in NY will evaporate, like most offsite action plans, on the plane journey home. We look forward to the follow up call from the offsite coordinator in 3 months time .. "Hi, we wanted to know how your progress plan we discussed at the offsite in September is going .. You haven't had a chance to look at it? .. Your line manager isn't supportive? I see.."

We have had dumps in western equities over the past week, but if you were to listen to the press and hadn't seen prices you'd think we were 20% lower than we are by now. TMM's DPI indicator and newly launched WMMT indicator are certainly reflecting that with weekend conversations pointing to a disconnect between where prices are assumed to be and where they actually are with "well, we are only back to where prices were in early August" being greeted with disbelief. (WMMT = "What My Mother Thinks").

Gold meanwhile has had all the spam chuckers scrabbling in their coffers to buy the dip, though "with what?" we would like to ask, as we thought they'd spent every scrap of fiat currency on it months ago. Maybe it will be just a little longer before they can afford to return to society from the log cabins. Having said that though, the bounce does look solid. -100 and + 80 bucks of gold within 7 hours is a pretty good sign of a blow off and would have TMM normally looking to buy. But if this is a long term play we can afford to wait.

Gold meanwhile has had all the spam chuckers scrabbling in their coffers to buy the dip, though "with what?" we would like to ask, as we thought they'd spent every scrap of fiat currency on it months ago. Maybe it will be just a little longer before they can afford to return to society from the log cabins. Having said that though, the bounce does look solid. -100 and + 80 bucks of gold within 7 hours is a pretty good sign of a blow off and would have TMM normally looking to buy. But if this is a long term play we can afford to wait.  Meanwhile Asian and EM moves continue to show signs of greater self-fulfilling worries than the rest. This just adds to TMM's belief that all of this is just that deleveraging trade we have all been talking about for so long. Europe may be the story, but the effects are global deleveraging. Europe is already so deleveraged on the long side that it's now short, the UK and US appear pretty neutral, so we are left with the leverage residing in EM and particularly EM fixed income.

Meanwhile Asian and EM moves continue to show signs of greater self-fulfilling worries than the rest. This just adds to TMM's belief that all of this is just that deleveraging trade we have all been talking about for so long. Europe may be the story, but the effects are global deleveraging. Europe is already so deleveraged on the long side that it's now short, the UK and US appear pretty neutral, so we are left with the leverage residing in EM and particularly EM fixed income. Now then, looking at this proposed IMF super package that has been the result of the Euro offsite in the States (lots of coffee, lots of networking breaks, lots of playing blackberry games under the table and plenty of trying to stay awake after too big a "get to know you" evening the night before). Well, on the face of it we have nothing concrete, but instead see the first phase of EU policy launch. Having obviously learnt this trick from the Labour Party in the UK, it involves leaking a potential idea and watching how the market reacts. If it's a disaster, then deny it ever existed, and if positive, then work in that direction. If there is one thing that TMM are learning from this crisis, it's that tape bomb shock has induced an inherent mistrust of anything being done until it is. But as we also know with this style of leakage policy, by the time it is announced it will be fully priced in, so we are therefore forced to consider the ramifications of this latest idea leak.

The €2trn has not been agreed yet but it could come either from the ECB or from just allowing the EFSF to borrow more itself. In the first case, the EFSF would issue bills that it would present to the ECB in exchange for Euro just like a bank-like financing, or it would sell those bills/bonds directly to the market. The Germans (cf Schauble) appear to be leaning in favour of that latter though at the expense of credit rating (it would act in a CDO-like manner). Which is fine as long as the German public don't notice.

On the German point, TMM frequently come across the view that the Germans, finally realising that they will have to pay, will just give up and re-adopt the DEM. The problem with this view is that both the economic and geo-political consequences of such a move - which, judging by how spookily similar the past few years' events have been to the post-1929 Wall Street Crash timeline, may well end in War - seem too much of a hurdle for them to be worth considering. Indeed, TMM reckon the Germans have overplayed their hand, and the leaks coming from the G20 suggest they have no friends. It's a case of "JUST SORT IT OUT, OK?!"

But back to the IMF idea, TMM reckon that with a fund that big, coupled with a broad based bank recapitalisation, the ECB and EFSF buying of bonds would be enough to convince markets that Italy/Spain will not suffer the Greek fate and that should be enough to give real money the nerve to reallocate.

So overall, TMM are encouraged that even if it did take the Americans to ram it down their throats, the Europeans are perhaps at last "getting it" and are actually discussing the policy responses we would want to be in place. Even the hardened Eurobears would have to take note.

But, back at home in Euroland the random word generators of the Eurocrats continue to spew out non-committal statements about what they haven't decided and what is possible with a frightening lack of what IS going to be done.

*GERMAN FINANCE MINISTRY SAYS NOT MULLING THIRD EFSF EXPANSION

*ECB'S MERSCH - WILD EXPECTATIONS ABOUT ECB RATE CUT SHOW SOME PEOPLE HAVE LOST DIRECTION, ECB HAS ONE NEEDLE IN COMPASS

*ECB'S NOWOTNY - ECB INTEREST RATE CUTS CANNOT BE EXCLUDED

*ALMUNIA SAYS MERKEL, SARKOZY KNOW WHAT IS AT STAKE

*DUTCH PM RUTTE SAYS NO PLANS TO RAISE AMOUNT OF MONEY IN EFSF

So maybe all the great ideas hatched in the Euro "offsite" in NY will evaporate, like most offsite action plans, on the plane journey home. We look forward to the follow up call from the offsite coordinator in 3 months time .. "Hi, we wanted to know how your progress plan we discussed at the offsite in September is going .. You haven't had a chance to look at it? .. Your line manager isn't supportive? I see.."

16 comments

Click here for commentsSo, like the Fed levered up to save over-leveraged banks in the US, we need the ECB/EFSF to lever up and issue some dodgy paper to solve the problem of dodgy EU paper.

ReplyHmm. I think I've seen this Athenian Tragedy before.

A strong rumour of a 50 bps ECB rate cut was out there this morning. Now that's what they SHOULD do, but no guarantee that they will do it. We were surprised how little fudge came out of the weekend at IMF.

ReplyLB is watching crude, which needs to descend further, especially Brent, to match weaker economic growth and softer US seasonal demand. We probably will not see a really sustainable bottom until crude finds a floor, if only b/c of the preponderance of energy companies, notably in the FTSE and the SPX.

I wanted to follow up on the discussion from prior days' threads about earnings. Here is some interesting commentary:

Replyhttp://www.businessinsider.com/morgan-stanley-the-terrifying-2012-bear-case-scenario-2011-9

I agree, LB, that my timing might be off, but keep in mind that this is NOT the business cycle that we are talking about. We are talking about a multi-decade credit cycle that is on the deleveraging side of the slope. Accordingly, earnings outside of (i.e. below) historical business cycle troughs should be expected.

C says'

ReplySome people and efinitely the media see the market in simplistic terms.Unable to understand the compex relationships they tend to ficus on whichever one may appear the clearest for them to understand and they give attribution to that for all things 'market'.

The reality is more complex than that with connecting themes interacting to create the conditions we are watching in real time. Indeed it often amuses me when I see a 'media.market' really heavily focussed on one issue.At times like that I have an habotial instinct to start looking over my shoulder for the connected stuff that's going to come out of left field and sandbag anyone not paying attention.

The rumour mill is good to get a rally going ,but I'll bet there will be no shortage of people lining up to short it because the economic context remains one of verge of recession in major parts of the world economy and the rest holding above it are being steadily dragged down by their connections to it.

Significant policy changes needed before that becomes a buy again although we will have rallies of course.

NO major arguments with you guys, just watching for the next significant rally. There are always rallies.

ReplyLong and interesting article that reflects our view of the potential fro recovery in a beaten down old dog that's been left outside to die, the Nikkei.

<a href="http://seekingalpha.com/article/295747-are-japanese-businesses-worth-more-dead-than-alive?source=yahoo?> Japan and Value Investing </a>

Japan and Value Investing

ReplyI could see how a levered up EFSF or a massive expansion of the ECB bond buying program might be effective (combined with a bank recap). I just don't see it as politically feasible, absent further pressure from the markets.

ReplyHaving said that European equities are clearly oversold and the potential double bottom combined with multiple bullish divergences appears interesting.

I am still inclined to sell rallies, for now, but in the markets that haven't clearly priced the 'growth' risk.

Thanks for the Japan link LB

ReplySetting up backstops for the banks and then letting Greece default is the scenario that is gaining traction. Of course this does mean there may be more such events later, but it buys us a year, perhaps? My guess is they will wait for one more market puke before the Bazooka/TARP comes out. So very Hank Paulson.

ReplyJust getting tired of the "we need to keep bailing whilst banks plug the holes in their capital structure" meme. It worked during the LatAm debt crisis but that was when banks were banks, not levered hedge funds. Over the last 25 years the results has not been healing but rather turning an acute condition into a chronic one.

Reply(Shitty boats should sink - that's just unconscious knowledge.)

As for possible value plays, if you like EU banks at 0.4 times book, you're gonna love 'em at 0.2.

LB, having watched a few competitors in my space (corporates / events / credit) try to bust out the knuckle duster over the years and get Japanese boards to try to do what is in the interest of shareholders all I can say is: caveat emptor.

ReplyAsk Warren Lichtenstein about how he feels about Tepco and the like. Japan is a mother of a value trap because the headkickers like Dan Loeb and Carl Icahn can never get control.

MM,

ReplySo you are cheering Europe going full Euron? Sticking it to taxpayers again in order to preserve the financial/parasite cohort. As U. Sinclair once saith: impossible to get a man to believe something if his livelihood depends on his not believing it.

I'm sure you are nice guy. Def. funny. But your profession is the problem.

The reason the world if fucked is primarily because the banking/hedge/trader class has killed its host--the real economy.

Anyone who works in the space, including MM, needs to take a long hard look at the larger evil you are participating in, and work to fix if from inside.

I'm sure a super levered EFSF helps the monied interests, but it doesn't help society, and will make the necessary flush of the bad debt more painful.

LET THE BIG BANKS GO

It won't be the end of the world. Promise.

Ditto Nemo's comments. SG released this report, stolen by ZH, more than a year ago: http://www.zerohedge.com/article/uncovering-liquidation-value-japan

ReplyAnd the Economist weighs in in 2008: http://www.economist.com/node/10698467

and I found this while looking for Steel Partners [notable failures] http://greenbackd.com/2010/02/11/activist-investing-in-japan/

Unless the Japanese magically turn into greedy Americans and load up on lawyers who will force boards to act all of this is just wishful thinking.

C says'

ReplyGovt safe haven trade about to be squeezed so Equity counter trend rally anyone.

Tool of the week

Replyhttp://www.bbc.co.uk/news/business-15059135

Nic.. agree such a tw@t we wonder if he was a crude propoganda set up by Ed Balls and Vince Cable. No bbg account.. runs "how to trade " courses.. web address www.leadingtrader.com/about/ for complete profile. Where the f did they find him? BBC really is going down the Swannee re reporting these days

Reply