Another month has passed the post, and markets are now entering the home stretch of what has proven to be an interesting year, to say the least. August's ruptures in equity and currency markets proved to be surprisingly short-lived; while money markets continued to prove challenging, particularly for the good folks at Northern Rock, a number of risky asset markets reversed prior losses with stunning speed.

Also getting its boogie on was the dollar, as the DXY crashed to all-time lows. While the surge in EUR/USD dealt a crushing blow to Macro Man's powerball strip of downside one-touches (more on this later), he at least had the sense to recognize that a "bubble of dollar weakness" was a logical outcome of Fed reflation. Ben Bernanke decided to have a breakfast party, and (dollar) toast featured prominently on the menu.

Equities, meanwhile, also surged both before and after the Fed easing. It is remarkable to think that a quarter in which the ghosts of 1998 haunted financial markets (Merrill Lynch and UBS both announced 4 billion worth of local-currency losses due to subprime) and non-farm payrolls turned negative, the S&P 500 would generate a positive price return. And yet it did!

Equities, meanwhile, also surged both before and after the Fed easing. It is remarkable to think that a quarter in which the ghosts of 1998 haunted financial markets (Merrill Lynch and UBS both announced 4 billion worth of local-currency losses due to subprime) and non-farm payrolls turned negative, the S&P 500 would generate a positive price return. And yet it did! Macro Man faced an uphill p/l battle for much of September. The powerball strip, which had contributed handsomely to his success in August, performed an about face. A combination of a sharp rise in the 10 year forward and a reasonable decline in implied volatility spelt big losses for the strip, leaving Macro Man peering out from behind the p/l 8-ball for much of the month. However, a strong performance by the beta plus portfolio and a recouping of some of the FX alpha losses propelled him back into the black, and he finished September up just over 1%.

Macro Man faced an uphill p/l battle for much of September. The powerball strip, which had contributed handsomely to his success in August, performed an about face. A combination of a sharp rise in the 10 year forward and a reasonable decline in implied volatility spelt big losses for the strip, leaving Macro Man peering out from behind the p/l 8-ball for much of the month. However, a strong performance by the beta plus portfolio and a recouping of some of the FX alpha losses propelled him back into the black, and he finished September up just over 1%.

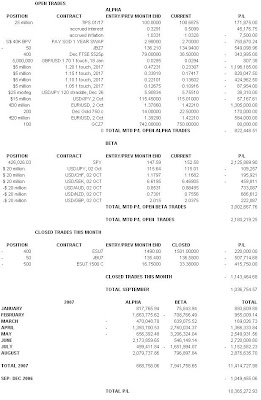

The single largest contributor was the equity beta-plus portfolio, which kept him involved with equities throughout the bounce of the past six weeks. It is a testament to the utility of simple models as part of a diversified investment process; broadly speaking, conditions remain favourable for equities, so the model kept Macro Man in, earning 2.1% last month.

The single largest contributor was the equity beta-plus portfolio, which kept him involved with equities throughout the bounce of the past six weeks. It is a testament to the utility of simple models as part of a diversified investment process; broadly speaking, conditions remain favourable for equities, so the model kept Macro Man in, earning 2.1% last month.  Fixed income trades weren't much better. While the long-standing TIPS position made money, it was only via capital appreciation- he actually lost some inflation compensation on the month. The real turkey was the SGD payer position; having tickled his target at 3%, it proceeded to drop more than 30 bps in close to a straight line, taking substantial profits with it. It is a reminder that non-core positions that are close to their price target should be risk-managed more carefully. The JGB short broke more or less even on the month, though has dropped a bit this morning after a mixed Tankan. All in, fixed income alpha trades dropped half a percent.

Fixed income trades weren't much better. While the long-standing TIPS position made money, it was only via capital appreciation- he actually lost some inflation compensation on the month. The real turkey was the SGD payer position; having tickled his target at 3%, it proceeded to drop more than 30 bps in close to a straight line, taking substantial profits with it. It is a reminder that non-core positions that are close to their price target should be risk-managed more carefully. The JGB short broke more or less even on the month, though has dropped a bit this morning after a mixed Tankan. All in, fixed income alpha trades dropped half a percent.

Also getting its boogie on was the dollar, as the DXY crashed to all-time lows. While the surge in EUR/USD dealt a crushing blow to Macro Man's powerball strip of downside one-touches (more on this later), he at least had the sense to recognize that a "bubble of dollar weakness" was a logical outcome of Fed reflation. Ben Bernanke decided to have a breakfast party, and (dollar) toast featured prominently on the menu.

Equities, meanwhile, also surged both before and after the Fed easing. It is remarkable to think that a quarter in which the ghosts of 1998 haunted financial markets (Merrill Lynch and UBS both announced 4 billion worth of local-currency losses due to subprime) and non-farm payrolls turned negative, the S&P 500 would generate a positive price return. And yet it did!

Equities, meanwhile, also surged both before and after the Fed easing. It is remarkable to think that a quarter in which the ghosts of 1998 haunted financial markets (Merrill Lynch and UBS both announced 4 billion worth of local-currency losses due to subprime) and non-farm payrolls turned negative, the S&P 500 would generate a positive price return. And yet it did! Macro Man faced an uphill p/l battle for much of September. The powerball strip, which had contributed handsomely to his success in August, performed an about face. A combination of a sharp rise in the 10 year forward and a reasonable decline in implied volatility spelt big losses for the strip, leaving Macro Man peering out from behind the p/l 8-ball for much of the month. However, a strong performance by the beta plus portfolio and a recouping of some of the FX alpha losses propelled him back into the black, and he finished September up just over 1%.

Macro Man faced an uphill p/l battle for much of September. The powerball strip, which had contributed handsomely to his success in August, performed an about face. A combination of a sharp rise in the 10 year forward and a reasonable decline in implied volatility spelt big losses for the strip, leaving Macro Man peering out from behind the p/l 8-ball for much of the month. However, a strong performance by the beta plus portfolio and a recouping of some of the FX alpha losses propelled him back into the black, and he finished September up just over 1%. The single largest contributor was the equity beta-plus portfolio, which kept him involved with equities throughout the bounce of the past six weeks. It is a testament to the utility of simple models as part of a diversified investment process; broadly speaking, conditions remain favourable for equities, so the model kept Macro Man in, earning 2.1% last month.

The single largest contributor was the equity beta-plus portfolio, which kept him involved with equities throughout the bounce of the past six weeks. It is a testament to the utility of simple models as part of a diversified investment process; broadly speaking, conditions remain favourable for equities, so the model kept Macro Man in, earning 2.1% last month.However, what really turned Macro Man's fortunes around was the trigger to get back into the FX carry basket. He was absent from FX carry throughout the month of August, and as such missed the concomitant substantial drawdown. While he did not "buy the low" on the month, he frankly did not need to; in the short period of time that he held the basket in late September, FX carry added 0.88% of return. All in, the beta strategies made 3% month; coming on top of a positive return for August, Macro Man feels justified in his faith in KISS strategies.

Macro Man's alpha performance, on the other hand, was less impressive. The albatross around his neck was the powerball strip, which declined precipitously in value for reasons noted above. Together, the four one-touches subtracted 2.53% from his return for the month, leaving him in quite a hole. However, a couple of timely purchases of EUR/USD, more than hedging the powerball delta, helped compensate for the option losses, making back 1.9%. Other FX option positions were down modestly on the month, taking the FX alpha return to -0.74% for September. Overall, however, he made money in currencies last month when the carry basket was added back in. It would have been pretty galling to have correctly called a sharp dollar decline and lost substantial amounts of money in the process!

The equity alpha portfolio was also down on the month, courtesy of short SPX exposure via futures and options. While the underlying view (the Fed wouldn't be aggressive with equities rallying) was dead wrong, Macro Man at least had the sense to cut his losses as soon as Bernanke opened the hatch on his helicopter. Still, the losses were considerable, as equity alpha trades shed 0.98% on the month.

Fixed income trades weren't much better. While the long-standing TIPS position made money, it was only via capital appreciation- he actually lost some inflation compensation on the month. The real turkey was the SGD payer position; having tickled his target at 3%, it proceeded to drop more than 30 bps in close to a straight line, taking substantial profits with it. It is a reminder that non-core positions that are close to their price target should be risk-managed more carefully. The JGB short broke more or less even on the month, though has dropped a bit this morning after a mixed Tankan. All in, fixed income alpha trades dropped half a percent.

Fixed income trades weren't much better. While the long-standing TIPS position made money, it was only via capital appreciation- he actually lost some inflation compensation on the month. The real turkey was the SGD payer position; having tickled his target at 3%, it proceeded to drop more than 30 bps in close to a straight line, taking substantial profits with it. It is a reminder that non-core positions that are close to their price target should be risk-managed more carefully. The JGB short broke more or less even on the month, though has dropped a bit this morning after a mixed Tankan. All in, fixed income alpha trades dropped half a percent.Ironically, the only profitable sector of the alpha portfolio in September was the only losing sector for the year: commodities. Macro Man slapped on some long gold exposure as another means of playing the "misguided reflation" theme. Given earlier missteps in the commodity space, position sizing has been relatively conservative; nevertheless, the 0.25% positive return represents Macro Man's best commodity effort of the year.

All told, the alpha portfolio shed 1.97% in September; combined with the beta return of 3%, this took September's return to 1.04% (courtesy of rounding.) Given that the SPY position went ex-dividend at the end of the month, October will see a 0.30% bonus on Halloween. For the year, Macro Man is now comfortably into double digit returns, ending September up 11.4%.

October should present its own set of challenges, as it has historically been a very poor month indeed for equity and carry strategies. That having been said, and despite a bout of profit-taking this morning, Macro Man remains confident in the view of dollar weakness as an emerging theme. While the press may be all over it, risk takers are not, and it wouldn't surprise Macro Man if EUR/USD trades towards the equivalent of the all-time low in USD/DEM (roughly 1.4575 in EUR/USD) by the end of the month.