Greetings Macro Man Community--thank you to the new contributors who have done well taking up the TMM mantle. It’s great to see that the Macro Man tradition is carrying on.

This isn’t me coming out of retirement, so much as wrapping up some loose ends. My departure coincided--nearly to the day--with a firestorm in emerging markets that hasn’t quite been put out yet. A combination of local factors, higher US rates, outright USD strength, and the subsequent reversal of portfolio flows has crushed a few EM currencies like BRL, TRY and ARS.

Argentina is an especially compelling case--it was the prodigal son of emerging markets in 2017, having not only come back to the market in style, but also plugged the market in size with the famous century bond, a 100-year issue that gets financial journalists squealing with delight every time they think about it.

Fast forward to, well, only later in 2017...and Argentina started to backtrack on inflation targeting, central bank independence, free movement of capital, and was experiencing a historic drought that was crushing soybean production--the country’s biggest source of export revenue.

It started slowly...and then as ever in EM...all at once:

Bang...in only a couple of weeks, the peso was 20% weaker and the central bank hiked three times in the space of a week, taking the overnight rate to 40% to stem the run on the currency.

Having written about the subject in the past, I feel compelled to look back at my work and see what I missed, what I got right, and what was simply a big surprise:

Back in September, I wrote this on Argentina:

“I continue to believe global trends will buy time for Macri’s agenda to work--and while an Argentine election is always a bit of a crapshoot, the trend in Latam favors center-right candidates”

Grade: B. Global trends did NOT give Macri time for his agenda to work--but he did win a big midterm in October. So I got the theme right--Macri was engaging in a risky strategy to use cheap short-term funding and not cut spending quickly, hoping growth would eventually bail him out. It didn’t work.

“Beyond the political risk, the fiscal situation is far from healthy--and will require a bout of austerity and likely significant spending cuts. The 2017 primary balance is a nasty -4%/GDP, which means the government is going to be running up a larger debt load for the foreseeable future. “

Grade: A-. Many real money folks were simply enamoured with the story, and didn’t really check under the hood. Macri cut the deficit, but ignored his addiction to short-term financing.

“Either way, as the charts below show, an acceleration of public debt at this pace for a sub-investment grade credit is simply unsustainable….I expect Cambiemos will win in October, which should provide a short-term tailwind, but the medium-term is fraught and highly dependent on local and international factors that could throw the reform movement into a state of chaos.”

Grade: A. Maybe there’s a spot for me at Hacienda when Macri finally cleans house. Or a cushy consulting gig with the IMF?

I’m feeling pretty good so far. Now, let’s talk about the currency!

“Similar to the credit, this is an attractive carry trade if you buy into “the story”, but not without its risks. I think ARS will appreciate over time, but it won’t be quick.”

Grade: D. I was clever enough to note the risks, and an abundance of evidence ARS had to weaken. Then had to add a throwaway line about about “ARS will appreciate over time”. I blame my editor.

Then I get into the lebac/NDF cross border trade. “The lebacs and ndf hedges mature every one to three months, so you have the opportunity to get out if the fundamentals or political situation deteriorate. That is unlikely...Long story short, at 500bps this spread is well in excess of the risk that the government will again implement capital controls over the next 3, 6, or 12 months.”

Grade: D+. In classic “crystal ball” fashion, I made the forecasting assumption that Macri wouldn’t have a real mess on his hands if the economy went south. That’s what happened. Now the IMF is in town and capital controls are most certainly on the table. It wasn't just that I was wrong, I was wrong about the downside of being wrong.

Yet, in the end, if you followed my trade here you just might weasel away with your profits intact--and I was right that you have numerous exit doors to get your money back. You’re still up TTD, and at last check this spread is in decent shape--but there’s going to be some sleepless nights and pepto-bismol between you and maturity.

To summarize, I think this shows that there are no easy routes to investing success. TBH, I think I got more stuff right than wrong--yet the stuff I got right here was relatively tough to monetize, and the stuff I got wrong had the potential to be a first-class ticket on the fast train to EM Crazytown that ends in a smoldering pile of twisted metal and an uber to the unemployment office.

With that, a quick post-mortem on how Argentina got to this point, and where they may go from here.

First is this one--not the ARS chart, but the real effective exchange rate. I alluded to this but didn’t realize just how important it was and is.

You can see here that the deval the country experienced when Macri let the peso float in 2015 was enough to get back to a competitive level, but high inflation and *not high enough* interest rates let the real value of the currency appreciate back to unsustainable levels.

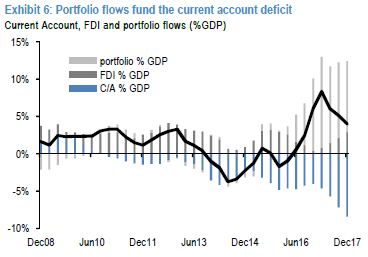

Hand in hand with that chart is this one:

When Macri won in 2015 the country experienced a huge increase in portfolio flows and FDI--enough to fund the budget deficit and start re-accumulating international reserves. But what else do you notice? A significant acceleration in the current account deficit.

That’s what came back to bite them in the back--especially after the central bank backtracked on the 2018 inflation target in December and inexplicably cut the overnight rate earlier this year--two measures that slashed real interest rates and waved a red flag in front of weary local investors that now might be the time to take their money out of the country.

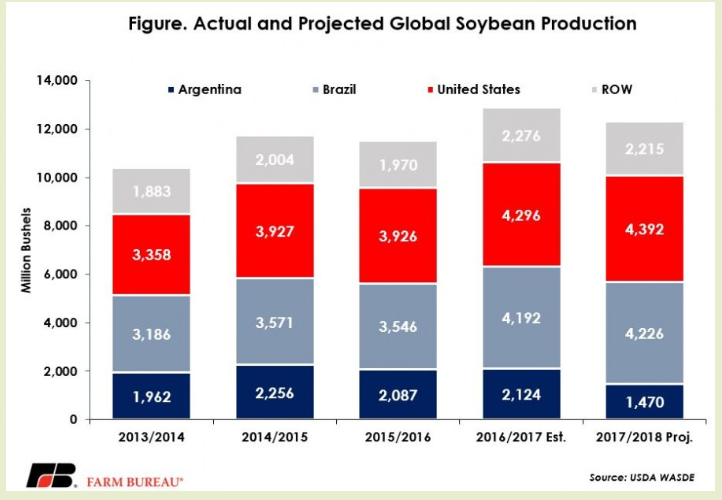

Then came the unpredictable. This is a chart of global soybean production, with Argentina on the bottom tile.

What you see there is a drop in production by roughly a third, which adds up to roughly $7 billion in lost export revenue just in soybeans alone. Add a couple more yards from corn and other agricultural products, and this is a pretty big event.

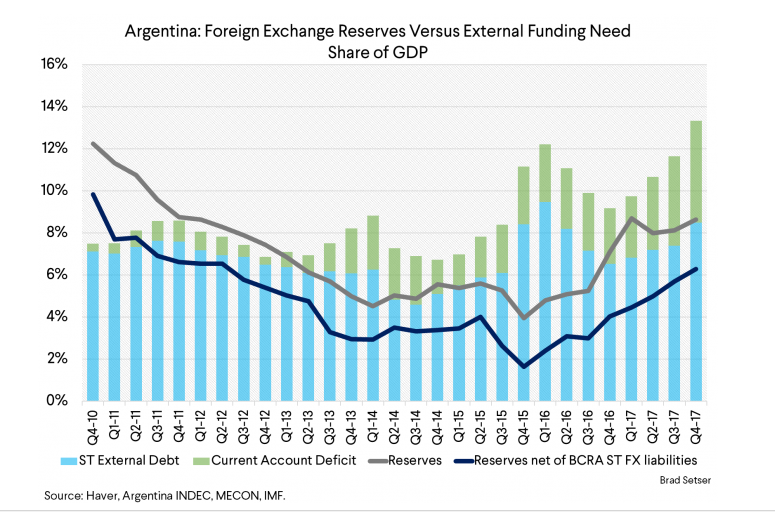

This is why EM countries build international reserves, so they can use them to fund their short-term USD liabilities when times get tough or there is an unexpected hit to export revenue. That’s where Brad Sester comes in...the High Prince of International Capital Flows (I had a short debate on Twitter on this subject last week...it was an honor getting worked over by him)

Brad noted just how inadequate Argentina’s reserves have been, owing to not only their rapid increase in short-term debt, but also the relatively small size of the local banking sector. This chart is particularly telling:

The spread between the dark blue lines and the top of the bars are the key. Short-term external debt and the C/A deficit were accelerating much faster than net reserves. I’d add that the government was also dependent on short-term local financing in the form of t-bills and Lebacs...from foreigners!! That doesn’t show up in these figures, but Macri eliminated all restrictions on incoming and outgoing capital in early 2017...when the economic situation got sticky this year, that hot money was looking to leave as quickly as it came.

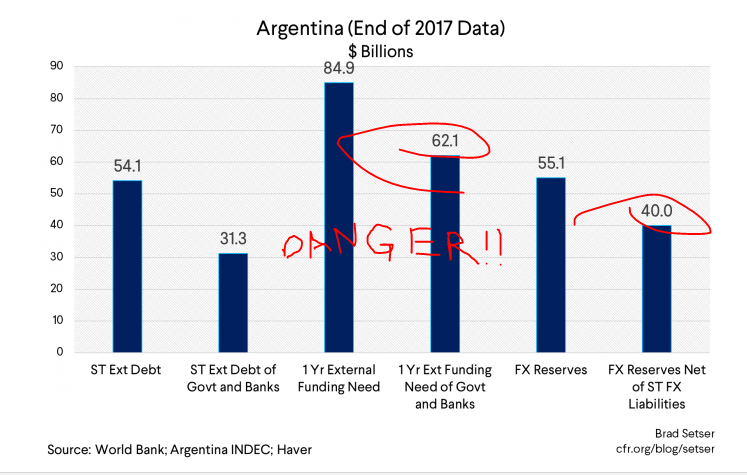

That culminates in this chart, which shows just what kind of figures were dealing with here. (the pathetic color crayon is my emphasis, not Brad’s)

With all that, an appreciating USD, a reversal in global EM flows, and a debt-gdp level approaching 50%, you can see why Macri had to call in the IMF. I’m still not convinced that is the right political decision, but would be willing to stipulate he made a sound decision to go to them, before they came to him.

Where does that leave us in the market? Would you be surprised to hear...not very far from previous levels?!? This is a chart of the spread over UST for the Argentina 33s, a dollar bond that has been around forever. 100bps off the lows?!? 470bps over? Really?

Yes folks, that’s where we are in the global credit cycle. A low grade credit with a documented history of being “debt intolerant” rolls over and requests an IMF bailout AFTER A 100BP SELLOFF IN THE CREDIT.

Where does Argentina go from here? I don’t know. Part of me says they are going to pull a Houdini and get out of this mess. Another part says this is just the beginning of an ugly Greek-like cycle of austerity, reform, and the resurgence of leftist politics.

What do I know for sure? Given the magnitude of the global credit binge, we’re going to see a lot more of this kind of thing. To avoid tough economic measures, Argentina exchanged safety and flexibility for cheap financing and fragility. All it took was a drought, a couple of bad political decisions and a 100bp selloff and it was game over.

Argentina lost. Others will too.

Shawn

TeamMacroMan2@gmail.com

@EMInflationista

57 comments

Click here for commentsHey Shawn, this place is like a magnet, can't stay away.

ReplyDXY is looking toppish here. Price is in a rising wedge and making higher highs on lower highs in momentum - never a good thing.

Speaking of magnets...SPX 2752 is one. Let's see what happens up there but I think it would be rejected hard. Would love to short NDX @ 7020 - a selfish wish.

Great post Shawn. Will be interesting to watch this going forward.

Reply@IPA, are you selling out of DXY? If so, did you have fundamental reasons for a rise in the dollar? I tend to think that the dollar views depend on what your fundamental reasoning for its rise. I tend to wonder if we have entered a bit of a stronger dollar feedback cycle here, and if that's the case, I tend to think any pauses will be consolidation more than reversals.

A very important note on DXY is that it started its breakout towards higher values on the same day that the HKMA saw a huge buy-down down to defend the peg.

https://www.tradingview.com/chart/USDHKD/Ws7DNev9-DXY-Rise-correlation-w-USDHKD-peg-being-defended-on-April-18/

I feel like the above is not getting nearly as much attention as it should. I tend to believe there is an implication here that this is more of a fundamental $ funding problem that has legs to continue forward, thus I don't think we can just look at this as a technical rise in $DXY or something short-lived.

Agree with the latter.

ReplyWe are in a secular dollar bull, which is likely to have different legs up - first, we may have had the (Fed tightening) DXY rally, then a pause that refreshes, followed by the usual (emerging markets meltdown) DXY rally and then maybe another (Eurodollar squeeze and panic short covering rally) with a possible commodity meltdown to boot...

Note that these three phases are not discontinuous. We are ending (1) but it looks as though (2) has already started (ARS, TRY, etc..). It will take a bit longer, and some unexpectedly soft US economic data to really start (3) rolling and then those historically massive short positions in ED, 5y and 30y will all unwind in a way that might not remain orderly.

Reply@Cbus, yes, I am locking in profits here at 94 level. I am a technical trader, mostly looking for swings I can take from mid to longer term perspective. I went short at 94 (wrong) and 95 (right) and rode the "secular bull" down to 88.50 - 88.25 and then reversed and went long. Major levels are a key to my entries.

ReplyI give no particular damn about what HKMA is doing in the middle of my sleep. If I did, I would lose my freaking mind. I do however care about important levels: 94 and 95, draw a lot of lines on charts, take a look at overall technicals and fundamentals, and then apply my own Micky Mouse stuff to the picture. I am a no nonsense trader with very little tolerance to BS.

Please excuse my nonchalant approach to macro on this subject ;)

Thanks for the response, just was curious. Obviously there are a lot of different time lines at play here. I appreciate the more technical insight actually.

ReplyBy the way, just a note here based on my above comment regarding China / Hong Kong being the primary source of the rising dollar... If we assume the following is true...

1. Hong Kong is the primary intermediary source for Chinese mainland $ funding

2. Hong Kong Defending their PEG and Chinese $ funding demands are the source of rising dollar

3. Rising dollar increases the dollar funding demands on emerging markets, and more specifically China.

You basically end up with a death spiral for China if all the above is true (which looks to be the case from my amateur viewpoint). The only thing holding this all together are the reserves of the Hong Kong Monetary Authority defending their PEG, and the ability of the HKMA to defend that peg without bursting the massive Hong Kong real estate bubble. But given the relationship of the dollar rising with EM funding requirements, I think we may already be in a bit of a feedback loop here.

This sounds like crazy tin foil stuff re: HK stuff. The size of the HK interventions are less than minute in the global scheme of things, low numbers of bn....

Reply@unknown, I know this obviously sounds tinfoil-hat-ish, and to a degree, it is a little bit. I'm definitely not an expert, so that's part of why I'm putting some of this out there to be critiqued or discussed.

ReplyWith that said, keep in mind that I don't think most of the dollar rising is a result of the HKMA withdrawing liquidity. I believe it's more likely a result of $ funding requirements from Chinese mainland (along with obvious other causes of rising $ whether domestic or outside China). Overall, I believe the USDHKD peg is more of a visible barometer of dollar funding needs for mainland China. It also is a thread in which Chinese mainland needs to stay in tact for this trade to work.

You can see this in chart-form here https://www.tradingview.com/chart/USDHKD/DG7w7l0k-USDHKD-Dollar-Inverse-Correlation/ . DXY seemed to be positively correlated to USDHKD before 2017. Something changed in 2017 however, and USD suddenly became a perfect inverse of USDHKD, and go figure, the dollar started to rocket upward once USDHKD hit the peg. Is that really tinfoil hat?

The USDHKD hitting the peg is, as I believe, representative of funding requirements that are channeled through Hong Kong. The big defense of the peg that occurred around April 18 was concurrent with the announcement that China was cutting their reverse repo rate so that they could reduce bank reserves without cutting liquidity (read more about that here - http://www.alhambrapartners.com/2018/04/17/chinas-monetary-shell-game/ ).

I definitely don't have all the answers here, but USDHKD alone hitting the peg is a really significant macro event in my opinion, and a pretty big signal of a regime shift (only ever happened on this side of the peg in 1997).

I totally agree, mess is only starting for the weaker EM players.

ReplyWe are seeing reverse osmosis playing out with rising USD and yields. This is what I wrote on my blog Macronomics in 2013:

"In a normal "macro" osmosis process, the investors naturally move from an area of low solvency concentration (High Default Perceived Potential), through capital flows, to an area of high solvency concentration (Low Default Perceived Potential). The movement of the investor is driven to reduce the pressure from negative interest rates on returns by pouring capital on high yielding assets courtesy of low rates volatility and putting on significant carry trades, generating osmotic pressure and "positive asset correlations" in the process. Applying an external pressure to reverse the natural flow of capital with US rates moving back into positive real interest rates territory, thus, is reverse "macro" osmosis we think. Positive US real rates therefore lead to a hypertonic surrounding in our "macro" reverse osmosis process, therefore preventing Emerging Markets in stemming capital outflows at the moment." - Macronomics, August 2013.

More liquidity = greater economic instability once QE ends for Emerging Markets. If my theory is right and osmosis continues and becomes excessive the cell will eventually burst, in our case defaults for some over-exposed dollar debt corporates and sovereigns alike will spike.

Best, Martin

@IPA: LOL. I forgot the obligatory use of inverted commas on MM, for example, in "secular bull", denoting irony…. I agree that for swing traders a "secular bull" market is meaningless - that can mean "it has been up for two weeks". Still there are reasons to suspect that USD may be the stronger of a lot of the majors for some time.

ReplyPossible reversal candle again for crude oil today. Brent has now completed a double top at about $80.50, and was rejected from that level again before price fell amid some speculation about OPEC increases in production. Energy stocks were very weak today and lagged the indices. There may be a significant turn in the works.

2y auction was decent. Treasuries seem to be finding a bid at these higher yields.

@LB, no doubt in my mind on the dollar being stronger than some majors going forward. But I think there is a pause in cards here and a possible formation of a cup handle on DXY may be under way. So with that in mind, a pullback to 91.50 - 92 area is my current view.

ReplyI also agree with you on energy stocks. XOP reversal is giving me a reason to sell most of my remaining position into a possible bounce to 43.50 - 43.65 level. I can always buy it back. This has been a crazy trade so far!

Speaking of reversal candles... Check out XHB and XRT. Is there a problem with US consumer? Smacked down for 1.98% and 1.75% respectively. XRT engulfed four trading sessions like they were not there. XHB is threatening to make a new 2018 low if 38.60 is not held. So I think the price may be looking for 37.20 level next: it is an extension of 38.60 - 40 box, a projected touch of the lower trendline of the 3.25-point downtrend channel, and 8/2017 swing low. New low in homebuilders will send a shockwave through the markets. It's all about the rising interest rates.

Just like that, volatility and de-risking are back, in a small way, but it's not one of those new-fangled sell-offs where bonds and stocks together.

ReplyToday looks like Olde Style risk-off, with USD and JPY firmer, and EURUSD, EM everything red and yields lower. IPA called this one well, with regard to a turn in those sectors above. Last thing I looked at last night was USDJPY and there was already evidence of the usual coupling of stronger yen and lower spoos. This morning spoos, oil and yields all lower. It will be interesting to see how the oil supply data is interpreted against the rare background of macro risk off.

We have been chirping quietly since last Wednesday about a swing lower in rates and oil prices, but have been largely ignored and feeling fairly idiotic, wearing the dunce cap and sitting in the corner of the blog. Regular readers will be aware of LB's history of being early to sensible yet lonely trades. Long TLT, short USO, long vol all looking a little bit more interesting today. With speculators having established record short positions in 5s and ultras we could see a decent squeeze here.

Reply--

Good Day.

We are Christian Organization formed to help people in needs of

helps,such as financial help,So if you are going through financial

difficulty or you are in any financial mess,and you need funds to

start up your own business,or you need Loan to settle your debt or pay

off your bills,start a nice business, or you are finding it hard to

obtain capital loan from local banks, for the bible says””Luke 11:10

Everyone who asks receives; he who seeks finds; and to him who knocks,

the door will be opened”so do not let these opportunity pass you by

because Jesus is the same yesterday, today and forever more,Please

these is for serious minded and God fearing People.

Contact (Jacksonwaltonloancompany@gmail.com)

You are advise to fill and return the Details below..

LOAN APPLICATION FORM

Name of applicant:…………….

Country:…………………………..

Occupation:………………………

Sex:…………………………………

Purpose of loan:………………..

Age:………………………………..

Phone:…………………………….

Amount needed:……………….

Loan Duration:…………………

Monthly income:………………

Have You Applied For A Loan Before?

Email Us On (Jacksonwaltonloancompany@gmail.com)

Hello Everyone,

ReplyWelcome to the future! Financing made easy with Rey Johnson Home Loan.

Have you been looking for financing options for your new business plans, Are you seeking for a loan to expand your existing business, Do you find yourself in a bit of trouble with unpaid bills and you don’t know which way to go or where to turn to? Have you been turned down by your banks? Rey Johnson Home Loan. says YES when your banks say NO. Contact us as we offer financial services at a low and affordable interest rate of 2% for long and short term loans(Secured and Unsecured). Interested applicants should contact us for further loan acquisition procedures.

Services include:

* Car Loan

* Home Loan

* Truck Loan

* Mortgage Loan

* Debt Consolidation Loan

* Business Loan

* Personal Loan

* Students Loan.

With Rey Johnson Home Loan. you can say goodbye to all your financial crisis and difficulties as we are certified, trustworthy, reliable, efficient, fast and dynamic.

Email: reyjohnsonloans@gmail.com

Regards,

Dr. Rey Johnson

Thanks for share Xfinity Router factory resetsteps.

ReplyCAPITAL LOANS LLC

ReplyWe provide personal loans for debt consolidation, bad credit loans, secure loans, loans for bad credit and instant secured loans with cheap rates. Do you have a firm or company that need loan to start up a business or need a personal loan, Debt consolidation? We will provide you with loan to meet your needs.

Note: We offer the following loan services

*Commercial Loans.

*Personal Loans.

*Business Loans.

*Investments Loans.

*Development Loans.

*Acquisition Loans .

*Construction loans.

*Business Loans etc

For more information contact us through our Email: capitalloansllcfunding@gmail.com

Hello Everybody, I live in Cuba and i am a happy woman today? and i told my self that any lender that rescue my family from our poor situation, i will refer any person that is looking for loan to him, he gave me happiness to me and my family, i was in need of a loan of $20, 000.00 to start my life all over as i am a single mother with 3 kids I met this honest and GOD fearing man loan lender that help me with a loan of $20, 000.00 Dollar, he is a GOD fearing man, if you are in need of loan and you will pay back the loan please contact him tell him that is Mrs Ruth Walls, that refer you to him. contact via email:(infoloanfirm8@gmail.com) Thank you.

ReplyThank you so much.

Replyดูซีรี่ย์

moviehd222.com

Its a great pleasure reading your post.Its full of information I am looking for and I love to post a comment that "The content of your post is awesome" Great work.สล็อต ฝาก-ถอน true wallet ไม่มี บัญชีธนาคาร

ReplyHey what a brilliant post I have come across and believe me I have been searching out for this similar kind of post for past a week and hardly came across this. Thank you very much and will look for more postings from you.สล็อตxo

ReplyI admit, I have not been on this web page in a long time... however it was another joy to see It is such an important topic and ignored by so many, even professionals. I thank you to help making people more aware of possible issues.เว็บสล็อตเว็บตรง

ReplyPretty good post. I just stumbled upon your blog and wanted to say that I have really enjoyed reading your blog posts. Any way I'll be subscribing to your feed and I hope you post again soon. Big thanks for the useful info. สล็อตแตกง่าย

ReplyEconomy of Argentina

ReplyThe national currency is the Argentine peso. The symbol used for this currency is $ and is abbreviated as ARS. 8.5% of the country's population is unemployed. The total number of unemployed in Argentina is 3,798,553. Argentina exports about US$85.08 billion and imports about US$71.3 billion each year. The country's Gini index is 43.6. Argentina has a Human Development Index (HDI) of 0.808. The Global Peace Index (GPI) for Argentina is 1.865. Argentina has a public debt equal to 118% of the country's gross domestic product (GDP) as estimated in 2012. Argentina is considered a developing country. A nation's level of development is determined by a number of factors including, but not limited to, economic prosperity, life expectancy, income equality and quality of life. The country's main industries are food processing, automobiles, durable goods, textiles, chemicals and petrochemicals, printing, metallurgy and steel.

Total Gross Domestic Product (GDP) in Argentina calculated in Purchasing Power Parity (PPP) is US$964 billion. Every year, consumers spend around $406,677 million. The ratio of consumer spending to GDP in Argentina is 70% and the ratio of consumer spending to world consumer market is 0.95. Corporate income tax in Argentina is 35%. Personal income tax ranges from 9% to 35% depending on your specific situation and income level. The VAT in Argentina is 21%. In 2013, Argentina received US$178.9 million in foreign aid. In 2014, foreign aid totaled $86.9 million.

อยากเป็นสมาชิก ที่ autobetcasino ใครที่กำลังมองหาช่องทางการทำเงินที่เพิ่มโอกาสในการได้เงินแบบง่ายๆไม่ยากบ้างตอนนี้มีเว็บที่น่าสนใจกันแล้วคือ autobet

Replypgslotvip ใหม่ๆเข้ามาเรื่อยทางพวกเรามี Blog Games ให้อ่านข้อมูล รวมถึง tips เกมPGเข้าระบบ เพื่อสมัครผ่านเว็บไซต์ มีแนวทางเล่น ดีๆหรือ Tips ชี้แนะสล็อตแมชชีนที่พวกเราเคยได้เห็นในแบบอย่างตู้เกมส์

Replyเว็บ สล็อต ออนไลน์อันดับ 1 ในทวีปเอเชีย เป็นเว็บออนไลน์ ที่ดีเยี่ยมที่1ของไทย พีจี สล็อต ระบบน่าไว้วางใจ เล่นได้ จ่ายจริง ไม่มีต่ำ ฝาก-ถอน เร็วทันใจเล่นง่ายไม่ยุ่งยาก ทำเงิน ได้จริง

ReplyPg slot แตกง่าย เกมแจ็คพอต PG SLOT เป็นอีกหนึ่งต้นแบบเกมทำเงินยอดนิยมเยอะที่สุดในปี 2021 นี้ มีเรื่องราวชักชวนติดตาม และก็มีภาพกราฟิกที่ชัดเจนงดงามสูงที่สุดอีกด้วยเล่นเลย

Replyผลบอลสดในปัจจุบัน มากที่สุดของประเทศไทยคือการแข่งขันในทางเดียวกับการแข่งขันในลีกไทยทั้งหมด โดยผลการแข่งขันจะต้องรอดูในเวลาต่อไปเนื่องจากไม่มีการแข่งขันในช่วงเวลานี้ PG SLOT

Replypk 789 เป็นผู้พัฒนาเกมสล็อตออนไลน์ที่มาจากทวีปเอเชีย ที่นิยมในประเทศไทย รวมทั้งเอเซียอาคเนย์ ตั้งแต่ตั้งมา pg slot ได้สร้างชื่อสำหรับการเสนอเกมที่มีคุณภาพสูงดีที่สุด2023

Replyสนุกไปกับ pgslot999 กำลังมองหาความสนุกและความตื่นเต้น? มาลองตื่นเต้นกับโลกของ และสัมผัสประสบการณ์ในการเล่นเกมส์ออนไลน์ที่ไม่เหมือนใคร PG ค้นพบทุกสิ่งที่คุณต้องรู้เกี่ยว

ReplyReally amazed with your writing talent. Thanks for sharing, Love your works

ReplyFantastic website. A lot of helpful info here. Thanks to the effort you put into this blog

ReplyExtremely pleasant and fascinating post. Continue posting. We're waiting Thanks

ReplyI really like your post, I always like to read quality content and you have one

ReplyThanks for sharing. It is such a very amazing post. Great job you made in this post

ReplyThe website style is perfect; the articles are great. and you are great Thanks

Replyit’s really cool blog. D.

ReplyLinking is very useful thing.you have really helped D.

ReplyI want you to thank for your time of this wonderful read!!! D.

Reply

ReplyI really enjoy reading and also appreciate your work. D.

Appreciate you spending some time and effort to put this wonderful article. Goodjob!!... MM

ReplyGreat web site. A lot of useful information here. And obviously, thanks!... MM

ReplyI found this post while searching for some related information its amazing post... MM

ReplyEnjoying reading this well written articles. Lot of effort and time on this blog. thanks... MM

ReplySo wonderful to discover a unique thoughts. Many thanks to author... MM

ReplyFantastic blog, This is kind of info written in a perfect way. Keep on Blogging!... MM

ReplyA lot of useful information here. And obviously, thanks in your effort!... MM

Reply

ReplyIt’s really a great and helpful piece of information.

ReplyI’m glad that you just shared this helpful information with us.

ReplyPlease stay us informed like this. Thank you

ReplyThis website and I conceive this internet site is really informative ! Keep on putting up!

ReplyHello Dear, are you really visiting this web site regularly, Thank you!

ReplyThis feels written with intention.

ReplyYou handled complexity without losing clarity.

ReplyA strong example of behavioral analysis done right.

ReplyThe writing feels deliberate and precise.

Finding a life partner is an important journey, and Alliance Matrimonial made that journey much easier for our family. The staff understood our requirements clearly and consistently shared suitable profiles. What impressed us most was their prompt communication and willingness to assist at every stage. The service felt personalized, and we never felt like just another customer. We are extremely satisfied with the experience and appreciate the team's sincere efforts.

Replyhttps://alliancematrimonial.com/