Indeed, volatility is back. BTD may not be dead, and as I have mentioned here, I’m not convinced the bull market is dead and spoos are heading back to 2000 (yet). However, the systematic gamma sellers have taken a serious beating--and one that doesn’t seem to want to let up.

Beyond a couple of bullet point sized comments, I’ll again leave it to the peanut gallery to advance the discussion on where markets are going in the next couple of weeks. My take on the steel tariff move by Trump is that it is not a game changer for the economy at large but was designed by the administration’s trade negotiators as a tactic to make them look more serious in negotiations with China and NAFTA.

A lot of people ask me, “As a bond trader, what do you do?” Well ok, I guess nobody has ever asked me that. If fact, I find that most friends and family are pretty happy to not know what I do at all. But in the US fixed income world, one of the big asset classes is LIBOR spreads.

These trades can take on all kinds of forms, where you can bet on (or hedge) the spread between LIBOR and OIS, LIBOR and Treasury rates, or the individual components of LIBOR (1mo vs. 3mo, or 3mo vs. 6mo fixings, etc.). The people looking to hedge are often banks with various tenors of floating loans they want to match up, or asset managers that want to switch their liabilities from one benchmark (say, LIBOR) to another (like OIS).

Theoretically, LIBOR rates are the rate at which banks lend to each other, but nobody really does that any more. Today this rate is often set by bankers with an algorithm that takes into account various credit-driven short-term funding markets like repo, commercial paper and cross currency swaps. When credit tightens up, bank balance sheets contract, and/or capital leaves the market at large, these rates move higher relative to OIS, which is and overnight rate indexed to the fed funds rate that is more or less controlled by FOMC policy.

If the market is really scared--to the point where there is some question about the viability of the banks that are holding all of this credit risk and collateral for clients, LIBOR blows out to extreme levels. This is what happened in 2008-2009 and 2011-2012 during the GFC and European sovereign debt crisis. More prosaic spread widenings have occurred recently around the taper tantrum, China deval in 2015 and early 2016, and Brexit in 2016.

By contrast, these spreads contract when the market believes there will be more money to lend, which drives down interest rates. This is exactly what happened after Trump’s victory in the US election. After years or tightening balance sheets in reaction to Dodd-Frank regulations and a variety of Basel II reforms designed to increase bank capital, banks had less free capital to lend. When Trump won, his pronouncements about cutting regulations were seen as freeing up capital for banks to start lending again.

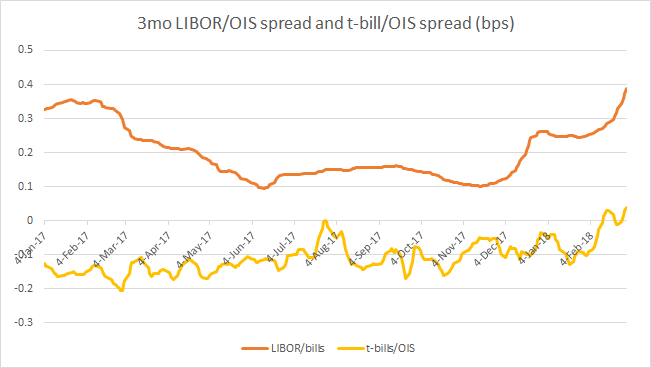

“Risk on” and tightening credit spreads didn’t hurt either. In mid-2017, the spot 3mo LIBOR/OIS spread went from the mid-30s to the teens, while forward spreads fell by 10-15bps too.

(Source: JP Morgan data; note: I used a 5-day MVA here to make the chart less noisy)

This trend reversed in style starting in December, when LIBOR fixings started to trend higher, taking all of the forward basis levels up with it. What happened?

This trend reversed in style starting in December, when LIBOR fixings started to trend higher, taking all of the forward basis levels up with it. What happened?

The answer lies in deep in the plumbing of the financial system. Back in December, two big things happened to impact short term funding markets:

- Trump and congress passed the tax reform bill. This gave many corporations with dollar assets offshore the incentive to repatriate those dollars and use them for share buybacks, dividends or M&A. The loss of that supply of dollars to lend out caused lending rates to increase,

- In the same tax reform, and in the subsequent budget deal with Democrats, the US decided to borrow more money. A lot more money. This will cause a big increase in t-bill supply, which will have the end effect of crowding out private borrowing--or at least causing the demand curve to shift to the right, also leading to higher borrowing rates.

For most of 2017, 3mo t-bill rates had been stable around 10bps tighter than OIS. Since the budget deal, that spread has moved 10-12bps wider. LIBOR has moved even wider, essentially taking in the impact of both the t-bill supply and the corporate foreign earnings repatriation.

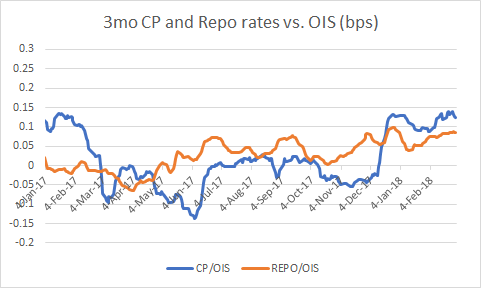

We’ve seen the impact in commercial paper and repo rates as well:

We’ve seen cross currency basis (the deviation between covered interest rate parity and where one can borrow or lend in USD in currency forward markets) has tightened as well, although not dramatically. The sum impact of these factors means LIBOR fixings are moving higher not because of any stress to the banking system, but because there is a greater shortage of USD funding, and fears of greater supply are forcing treasuries to cheapen.

In the end, I see the funding factor (offshore profit repatriation) and the supply factor (more t-bills) each having widened short-term funding rates by roughly 10bps--other measures that indicate pure (or more pure, anyway) expressions of bank credit risk (like 3mo/6mo LIBOR basis) are showing very little movement, despite the pullback in equity markets the past few weeks. That tells me this move is all about USD supply and t-bill issuance.

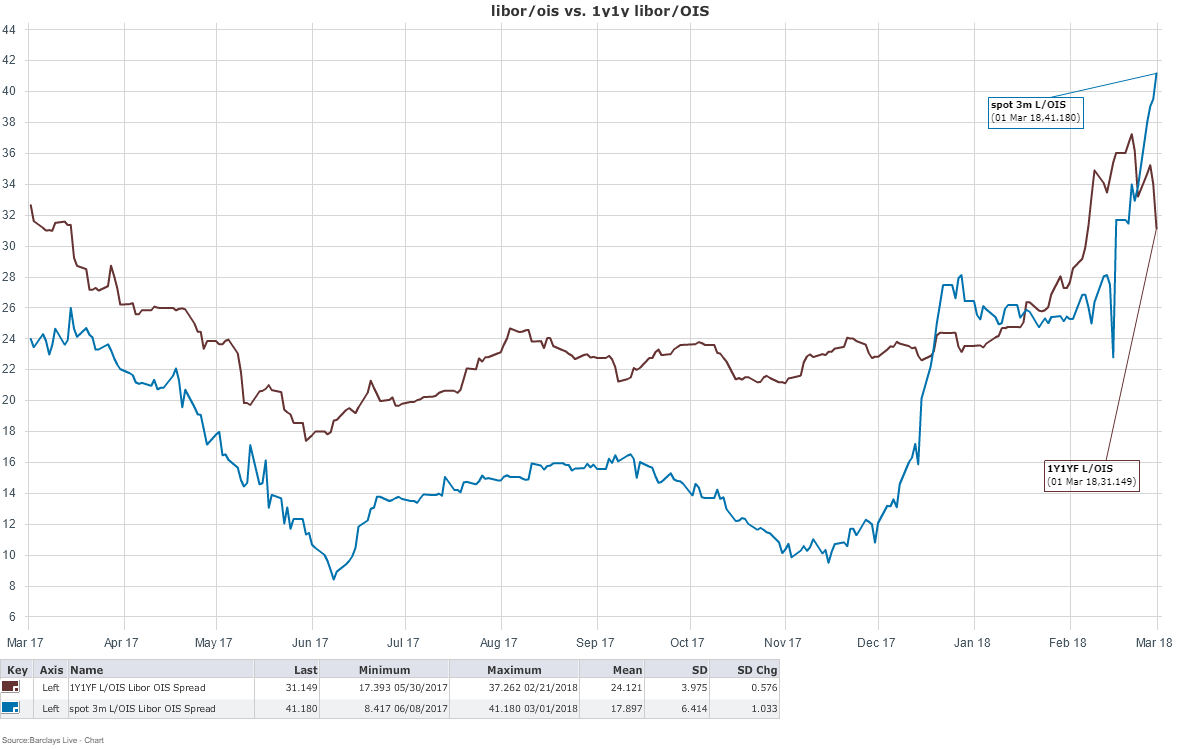

Where do these markets go from here? Here is a cleaner look at the LIBOR/ois forward markets relative to “spot”:

Put another way, the market is pricing a significant tightening in the LIBOR/OIS spread one year forward. 1y1y LIBOR/OIS is trading 5-8bps higher than it was for most of 2017. (Note also here that the market was set up for part of this move--presumably the offshore profits repatriation, but was caught with its pants down in the budget deal.) That order of magnitude looks about right to me--clearly hedge funds stepped into this trade in size this week. From these levels, I would look to pay forwards 2-3 years out vs. receiving front-end FRA/OIS (the short-term version of this trade in eurodollars), on the idea that 1) inversions in this curve are very rare, 2) there is no sign of credit stress, and in fact, short-term funding rates could subside soon as the Fed moves to reduce leverage limits for the banks, but 3) the long-term fiscal impact of the t-bill supply will likely be ongoing, and maybe worsen if the economy slows down and/or if credit markets weaken.

If you made it this far, you are either a basis junkie or you win the medal for getting through Professor MacroShawn’s Funding Markets 101 class. Either way, kick back with a Friday afternoon happy hour beverage of your choice. You deserve it.

Have a good weekend!

Shawn

TeamMacroMan2@gmail.com

@EMInflationista

No end to LIBOR manipulation....

ReplyDeleteAPRIL 10, 2017

Libor scandal

Barclays blamed BoE over lowering of Libor rate, claims BBC

Employees at lender discussed pressure from central bank, according to transcript

AUGUST 17, 2017

Libor scandal

FDIC sues Barclays, RBS and other banks over Libor

Agency claims failed US lenders lost money because rate was manipulated downwards

AUGUST 24, 2017

Libor scandal

Two SocGen managers accused of Libor manipulation

Prosecutors claim their actions caused roughly $170m of harm to financial markets

AUGUST 26, 2017

Libor scandal

US may struggle to extradite SocGen bankers over Libor

France has proved reluctant to surrender citizens in prior rate-rigging cases

SEPTEMBER 27, 2017

Business Book Club podcast

Business book podcast: ‘The Spider Network’

Investigative reporter explains how he unravelled the Libor scandal’s history

OCTOBER 3, 2017

UK financial regulation

Libor posed risk to UK financial stability, says BoE

Threat from markets’ reliance on benchmark set out in release of redacted judgment

OCTOBER 23, 2017

Banks

ANZ agrees to settle in Australia rate-rigging case

Move gives NAB and Westpac 48 hours to decide whether to fight allegations in court

fastFT

Deutsche Bank reaches $220m multi-state settlement over Libor claims

NOVEMBER 2, 2017

Financial & markets regulation

Libor nerves is sting in tail for perpetual bonds

Unintended consequences from demise of scandal-ridden benchmark causes debt concerns

NOVEMBER 24, 2017

fastFT

FCA fines RBS trader £250k over Libor riggingEx-Barclays banker calls for Libor-rigging conviction to be overturned

JANUARY 8, 2018

Libor scandal

Former RBS trader fined for role in Libor scandal

City watchdog bans Neil Danziger from working in any regulated financial activity

JANUARY 15, 2018

Libor scandal

Nine banks accused of rigging key Canada lending rate

Lawsuit alleges lenders manipulated the Canadian Dealer Offered Rate

Duly noted--but this is precisely why today's libor fixings are largely driven by model-based submissions from libor panel banks rather than subjective estimates. If I were a bank risk manager I would make this happen or get carried out on my shield. In this day and age there is absolutely no reason why some front office trader or back office manager should be the one making some finger in the air (or rigged) estimate of borrowing costs.

ReplyDeleteIf a bank devises a model-based approach and shows that to the regulator, the regulator can back test submissions at their leisure to prove out their veracity. Problem solved.

A great article. Thank you.

ReplyDeleteGreat piece. I DID make it all the way to the end because I'm a budding rates junkie. I would love to be an expert in this area.

ReplyDeleteGood Stuff Shawn. If I may, this is not your usual piece, you are among friends here so now that you have that therapeutic post out of the way, I look forward to your following pieces and we can rock in behind you-whatever it is that is niggling at you.

ReplyDeleteThank you, I'm heartened to know this is a swap spread safe space, or "SSSS". do check back on these spreads in 3-4 months, I expect a mean reversion to a more typical upward sloping libor/ois curve, moving from current -1/0 levels to +6-8. A good risk/reward compared to the probability this curve goes to seriously inverted levels.

ReplyDeleteBack to less esoteric subjects next week!

7.8% in 3-4 months, cool, Go for it!

ReplyDeleteWhat happens to other markets?

What's most remarkable about all the "reasons" I've heard from the street is that no one really has an idea as to what's going on. This analysis is about as good as any I've heard so far. One other possibility to think about is a tailwind of credit differentiation. Libor is going away, sooner than people (I think) realize. Many banks don't want the hassle or the risk of participating in the libor survey, yet lesser quality banks still have to borrow at libor-based rates. Letting the fixes edge higher by declining to participate works well for those higher quality banks who do so.

ReplyDeletethe most salient point, and the one that this case best illustrates, is that libor is a very different beast now. the rise in commercial paper rates is driving libor, not the other way around. In its weekly JPM went so far to say that FRA/OIS trading may be leading libor settings.

ReplyDeleteThat sounds a little rich to me. You can imagine the headlines if it came about that FRA/OIS derivative trades between banks and huge hedge funds influenced libor settings, and thus all manner of SBA loans and mortgages for Ma and Pa from Baudette. Elizabeth Warren would have kittens.

Re: differentiation in borrowing rates, there hasn't been a pattern of a spread developing between CP rates for libor panel banks and non-panel banks. That said, average bank CP issuance has been printing 5-10bps above fixings, so the mkt hasn't quite settled down yet.

Excellent piece, Shawn. Always impressed.

ReplyDeleteFrom what I gather, FRA-OIS likely stays wide for a while. Though net issuance pace falls off later this month, T-bill auction sizes will remain heavy until April. Wonder whether the size of speculative bets against ED futures also having a material effect on the spread. I haven't found a convincing case for the spread to revert soon and actually took off my little exploratory bet first thing.

Headline of the day for me was Salvani saying NL not available for "bizarre" coalitions. Unless we get 5S+NL coalition (which that remark suggests is unlikely as experts say, though weird things do happen, e.g. SYRIZA + right-wing Independent Greeks coalition), I guess the Italian election is a big nothing. IMO, time to pay attention to EURCHF cross again. If YTD action was mostly a positioning washout, then SPD + Italian election should clear the way for resumption of move starting last summer. But if the narrative of high current account surplus insufficiently recycled plus SNB starting a hiking cycle before the ECB is correct, then I'd expect the cross to fall back down back down. Or maybe I'm trying to see structure in a situation where there is little-to-none ...

Buying some COST puts on WMT and TGT earnings weakness picture. Target 185 & 179.

ReplyDeletenot the Minsky moment, but the Gary Cohn moment

ReplyDeleteonly Spoos under 2200 can spook Trump and send Navarro away

ReplyDeleteYeah Nico G, I spoke about Navarro here last year. He is a lunatic! It is important to point out that while market leaders, namely FAANNG (FB, AAPL, AMZN, NFLX, NVDA, and GOOG) have rebounded nicely (as cults usually die slowly) and SOX just made a new high, the transports are having a very tough time getting any traction here (pun totally intended). This is a no-brainer as the intermodal and cross-border traffic would take a huge hit on tariffs. Sell IYT and XTN.

ReplyDeleteEURCHF was having a nice move, but now has to contend with the "trade wars => alternative reserve currency bid" meme.

ReplyDeleteGary Cohn leaving plus section 301 measures (which are a much, much bigger deal than these steel and aluminum tariffs) "anticipated in coming weeks" is not a great backdrop for risk.

Flip side is Cohn's value was mostly in getting the tax cut done. So the worry is what his departure signals. Just jumping from the Titanic at first chance, or signalling an unavoidable, larger trade conflict.

ReplyDeleteFrom Team Macro Man to dear Gary Cohn.

ReplyDeleteWhat'd you think was going to happen. Did you think the traders on the desk around the ((oval)) office we're just going to say...

"All is well...you can pass on your sweat and tears onto the white house ...and in return we're allowed to back door you!"

Pretty difficult at the moment to trade ANYTHING. POTUS tendency to make announcements while the market is open, not to mention insane tweets, is just creating a lot of chop.

ReplyDeleteLeaving the noise aside, ADP was 230k. Whisper number for Friday is probably >200k now. More Treasury weakness between now and next week's 10 and 30y auctions seems likely.

Interesting that the dollar barely budged on the data, so we would have to assume FX punters are trading the Fed/ECB almost exclusively for now. We have a feeling we are going to see another run at EURUSD 1,25 and GBPUSD 1,40 before yet another failure. In the mean time, this is all getting a bit tedious.

EURCHF keeps going, despite 30Y rate spread going wrong way (the chart banks superimpose on EURCHF to explain this year's move). Interesting ...

ReplyDeleteIs Poland going Hungarian? Glapinski saying projections show no reason to hike by end-'20! And end-'19 would be earliest! Meanwhile, Hungary has done about everything it could to weaken the currency. Shorted some PLNHUF on all this. Seems interesting levels. My hit rate in these currencies hasn't been high, but worth a go.

Decided to take profit in EURCHF cash position here ahead of ECB. Probably a stupid move, given the momentum this has. Leaves me long KO calls I bought Monday ... were a very good buy.

ReplyDelete5 pips stupid since I started writing. Doh.

Pretty difficult at the moment to trade ANYTHING...

ReplyDeleteYou are joking right? Dax up +400pts Monday, up +300pts today. Nasdaq about to make ATHs, Russell close behind. FANG up over 1% every day...

If you're not making big money in this market then you need to get another job. This market has been putting dollar bills on a plate, and handing them to you. Doesn't get easier than this (unless you're a perma-bear and once again losing all your money).

sounds like words of someone who's never traded with a risk limit.

ReplyDeletesounds like words of someone who's never traded with a risk limit.

ReplyDeletesounds like words of someone who's never run risk.

Thank you so much.

ReplyDeleteดูหนังออนไลน์ 2021

รีวิวซีรีย์ฮิตติดกระแส

ดูหนังใหม่ 2021

ReplyDeleteรีวิวซีรี่ย์ใหม่

slot auto wallet เว็บเกม สล็อต ฝาก-ถอน ทรูวอลเล็ต ไม่มี ขั้นต่ำเว็บ พีจี สล็อต ออนไลน์ รูปแบบใหม่ พร้อม เกมมันส์ๆ สล็อต แตกง่าย ที่ทำเงินให้มากมาย ที่คุณไม่ควรพลาด ณ ตอนนี้

ReplyDeleteบริการ pg slot สำหรับค่ายเกมสล็อตออนไลน์ ที่มีนักพนันเลือกเข้าไปสมัครเป็นสมาชิก กันจำนวนไม่ใช่น้อยก็น่าจะจึง ควรยกให้กับ PG เลยเพราะว่าค่ายเกมที่นี้ จัดเต็มทุกความบันเทิง

ReplyDeleteเกมส์สล็อต สล็อตออนไลน์ หรือ พีจีสล็อต ถ้าหากพูดถึงเกมสล็อตแล้ว มั่นใจว่าคนที่พอใจการ เล่นเกมคาสิโนสล็อต ย่อมรู้จักกันอย่างดีเยี่ยม เพราะว่าเกมส์สล็อตเป็นเกมที่เล่นง่าย

ReplyDeleteทดลองเล่นสล็อต pp เกมสล็อตออนไลน์ รูปแบบใหม่ อัพเดทปี2022 มีเกมให้เลือกเล่นเยอะแยะ ไม่ว่าจะเป็น คาสิโนสด pg slot บาคาร่าออนไลน์เกมยิงปลาซึ่งสามารถเล่นผ่านมือถือได้ทุกระบบ

ReplyDelete