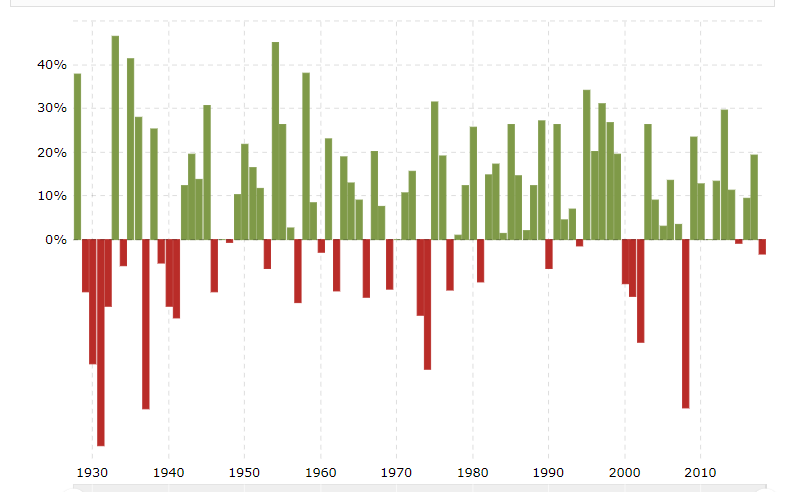

After a few go-go years in the stock market, it is easy to forget what a choppy market looks like.

Here it is folks. Simple as that. I can cite any number of reasons, valuations, growth underperforming-too-high-expectations, trade tensions, an all around bumbling US government from top-to-bottom, and a central bank that is bound and determined to take the punch bowl away.

In the end, nobody can tell you exactly why the market can’t get out of its own way. All we know for sure is that the momentum trade is dead--RIP Mo-Mo! Look, readers of this blog will know I am not big on short-term calls, technicals, or other forms of market prognostication. But the reason I posted this chart is because I do believe the market has a certain style of trading over relatively long periods of time. Some call them “regimes”. I believe the market saw a regime change with the short-gamma/short-vol implosion trade that started at the end of January.

That crushed the momentum traders--and to make matters worse, there have been a couple of times where it looked like stocks were finally going to get on the canvas and start trading like 2017 again--only to fall into another 50 point intra-day death spiral.

That is how equities trade in years when the market just kinda stinks for one reason or another. Look back at the chart above. There are years like 1994, 2008 and 2011, when various and sundry financial crises were crushing profits and market confidence. Similarly, in 2000, the market had finally run out of dot.com buyers. But then think about years like 2002, 2003, or 2015. The market simply couldn’t get over its various forms of anxiety.

Does that mean it is straight down the elevator shaft for equities? No, I don’t think so, not without a significant downside catalyst--a big drop in growth, a sudden cliff in employment, or some kind of credit event, or the dank roadkill-like stench of one ahead.

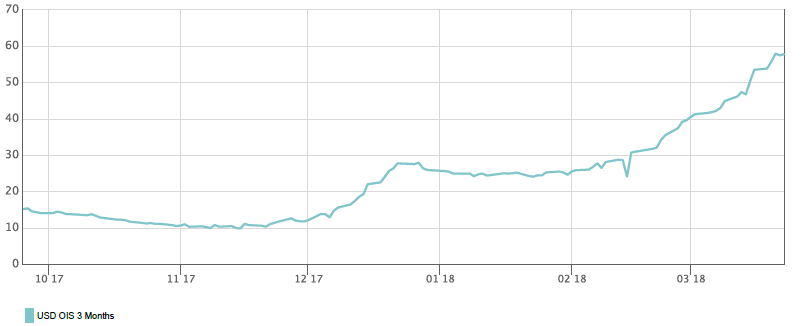

And yes, that serves as a nice segue into the latest update on the roadkill known as US money markets. No rest for the wicked...chalk up another 5bps higher in the libor-ois spread vs. this time last week.

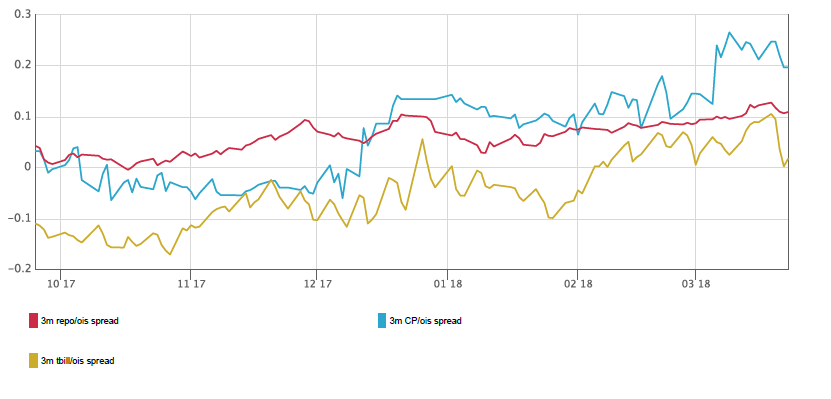

Yet...and yet!! I continue to believe we are seeing the beginning of the end of this move wider in spreads. Repo levels remains stable, indicating there is no broad grab for easy financing from big players that are desperate for dollars. And the chart below shows that the spread of commercial paper rates over OIS--and tbill rates over OIS, actually came down a bit last week.

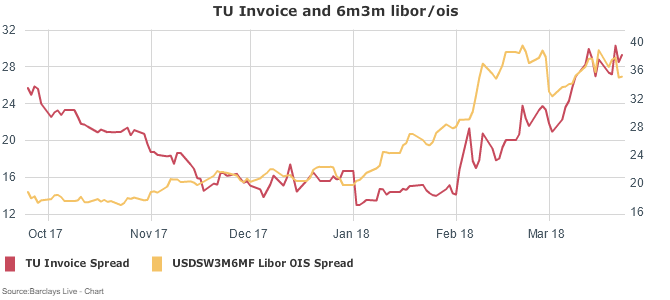

Which makes this week’s move wider in libor/ois spreads all the more perplexing--the market wasn’t fooled--front end swap spreads (proxied here by the 2yr treasury future vs. swaps, “TU invoice” and the 3m6m libor/ois swap) either chopped around or moved modestly tighter.

One of the highly respected analysts at one of the sell-side banks published a piece on Friday mentioning that a more arcane piece of the new tax code eliminated a tax incentive for companies--mostly foreign banks--to use the cross-currency swap market to fund foreign operations--instead pushing them towards other funding sources, like commercial paper. I don’t have the piece (teammacroman2@gmail.com if you have a copy!!), so I can’t opine on it--i’m not even sure I’m selling the thesis correctly from the headline I read--but it is a compelling hypothesis from a guy that really knows his stuff.

Either way--that leaves “just plain old credit” as the residual. The bloodbath in equity markets combined with “basically unch” risk-free rates led to a tit-for-tat widening in credit spreads.

Add this stress--or at least the return of some semblance of sanity--to credit markets at large, combined with some indications that the move in libor is hitting markets outside the US, and the picture starts to make sense. The latest catalysts are all modestly negative--and that has the power to unwind the positive narratives that supercharged stock markets throughout the past two years.

I like to believe that brings the market downdraft to a simple solution--an inversion of catalysts, a regime change, and a momentum break--all of which combines to cause a reversal in flows. Maybe it's more complicated--but I think it illustrates that the market will need a new narrative--and probably a lot of time-- to push to new highs.

Shawn

TeamMacroMan2@gmail.com

@EMInflationista

Shawn

TeamMacroMan2@gmail.com

@EMInflationista

https://www.bloomberg.com/news/articles/2018-03-23/higher-libor-ois-is-new-normal-but-don-t-fret-says-cs-s-pozsar

ReplyDeletehttps://www.realclearmarkets.com/articles/2018/03/23/global_dollar_conditions_are_escalating_the_wrong_way_103206.html

ReplyDeleteWhat's up with the Hong Kong dollar?

Speaking of choppy, is this a face-ripper I see before me? Spoos up 32, Qs up 100.

ReplyDeleteLooks like the 200 DMA is going to hold.

LB,

ReplyDeleteI thought IPA had it right for this week. Short holiday week backing into end of quarter squaring off doesn't look a good thing to bet against after a bit of a downdraft. In fact holiday weeks on theirown hasn't been fertile ground for being short like forever.

@Gus, I've had a HKD piece knocking around for a couple weeks....but have yet to clarify my view on the end game there. I guess it comes down to Chinese money--when cny was depreciating it made sense to sell CNY and buy HKD, leaving HKD pinned at 7.75....now with cny performing well, the money reverses back to either China...or USD so long as HKMA leaves rates below LIBOR. Forward points are deeply negative, not only indicating this isn't going to last, but also that there isn't a millennial version of George Soros banking on a break of the peg.

ReplyDeleteAnyone else out there have thoughts on the subject?

The HK real estate market is freezing with the number of transactions down to a trickle. At the current rate, it would take about 100 years to turn over once the real estate stock. The same thing is happening in Mainland China's major cities (BJ, SH, SZ, ...) by the way. HK banks are loaded to the gills with real estate credit that would take them down were real estate prices to correct significantly (total system debt in HK is over 10 times GDP, mostly real estate related). All mortgages in HK are floating rate, HIBOR indexed, hence the need to keep HIBOR low (3-month HIBOR quoted at 1.14786 today) even if the HKMA Base Rate was just hiked to 2.00% because of the USD Peg. The stark choice is whether to let the real estate market crash (it was down 70% from the peak at the 2003 through, but systemic leverage was lower back then), or let the HKD float and sink, risking outsized price increases in food stuff and other items which could undermine social stability. Not a pretty picture ...

ReplyDeleteFB first target hit @ 155. Still think 149 gets pegged. Gotta trail that stop! This was not an easy trade, FB has been an absolute freight train. Perfect example of technicals preceding fundanental news. Amazing heads up! Wish I took the trade earlier, still not bad.

ReplyDelete@hkpunter, do you have any sources for data on the HK real estate market? I find it hard to get any solid or reliable information there.

ReplyDeleteJust adding random commentary, the market ripped / bounced, now dipping. Given, this is sort of reading the tea leaves, but this does not look at all like a sign of confidence from market participants. Looks rather bearish.

ReplyDelete-BEAT tax makes US domeciled foreign affiliates unable to deduct interest in the US, so they are issuing more unscured domestic commercial paper. This is why LIBOR/OIS spreads r soaring, but cross currency basis swaps r tightening due to (unsecured funding preference)

ReplyDelete-A general over funding at the headquarters of of Japanese, European, and Canadian w/ branches in the US has occured. What was riased in the FX market in those countries banks headquarters FX market (rumors of 500-600B!!) Reduces demand for dollars via the swaps market

-General repatriation affect is stronger than anticipated. It went into effect Jan 1. 2018

-Debt ceiling avoidance caused massive treasury bill issuance (esspecially on the short end) Also recent budget agreement has been anticpated by markets for months now. CP dealers have to offer hgiher rates to compete w/ FFR.

It's tough to read the tea leaves. Did my own research into CP rates and issuance. Researched CROSS/RATES and LIBOR/OIS FRA/OIS spread behavior as well. The BIS and CS's Pzsar were helpful as well (Pzsar in aminor way I guess) I could be off or wrong (seeing the wrong things) it's happened before

@Checkmate. Correct. I don't think anyone here went into the weekend short. Fear tends to fade away into the holiday.

ReplyDeleteLB has been vol selling and dip buying since Friday's close (and again at 11am), but with tight stops.

@LB, that was a great call on Fri!

ReplyDeleteSometimes it makes sense to bet against the Apocalypse. If the 200DMA didn't hold, it would have been the end for this old bull. As of now, the jury remains out.

ReplyDeleteSimplest model here calls for a (noisy) bounce to the 50 DMA, now at around SPX 2740. First target the 100DMA, currently at SPX 2692. Roughly those levels are just below SPY 269 and 274.

know your timeframe and do not miss the bigger picture

ReplyDeleteItaly -1.2% and Europe red on a strong US bounce day tell you there is serious shit down the road

last time such a divergence was seen was late 2007

So trying to piece some things together...

ReplyDeleteHibor has Diverged from Libor over the past year, and this accelerated more recently. In the past week or so, as the USD/HKD approached the limit of the peg, 8.75, Hibor shot upward a bit. This is possibly a result of Hong Kong pulling in a bit of liquidity as the USD/HKD approaches the 8.75 peg.

Hong Kong is obligated to keep this peg, and if it goes past it (or in reality, keeps approaching it,) it will keep pulling in liquidity, causing HIBOR rates to rise significantly.

The question then becomes, why does Hong Kong care about Hibor rising a bit so much as they would let the USD/HKD approach the limit of the peg? To me, this screams they're scared shitless about what happens when interest rates rise back to a normal level in Hong Kong, which given outstanding debt there, is probably something worth being scared of.

So from that point, I wonder if there could actually be a chicken / egg scenario going on here. Could the Libor rates actually be partially a product of what is going on in Hong Kong with their currency PEG and interest rates?

Regardless of the situation, this tells me pretty straight up that if rates rise in Hong Kong, bad stuff will happen as HKpunter mentioned. I still wish I had a better overall understanding of things and data to pull from. If I'm wrong / offbase, please tell me.

No doubt higher ois rates and higher spreads are adding pressure to such a narrow band. The market doesn’t look too worried. If fwd points rose materially it might get dicey.

ReplyDeleteAgree with @LB. The way ES trades right now is very technical. If one missed today's rally and wanted to get in, and I think one should, there may be another opportunity at 2640-ish backtest. Tomorrow's pivot at 2638 looks like a great way to try and catch a possible pullback, which coincides with 38% fib from this morning's rth low and 200-hr ema.

ReplyDeleteThis comment has been removed by the author.

ReplyDeleteMy bad, 15-min 200 ema, and 1-hr 50 ema, that is. Anyway, 2638-40 zone is it, imho.

ReplyDeleteNo one wants the dollar or US assets any more. The movement out of the dollar and tighter fed is causing a reverse of flows out of all the momentum stocks and all the stuff that's been totally overbaked which is why this market is fading. If we think of the theme for this bear market its got to be the reversal of the FANG rally over the last year, the trump rally that lifted all US valuations, and of course crypto bollocks (one for the ages!).

ReplyDeletehttps://www.telegraph.co.uk/business/2018/03/26/hong-kong-first-global-firing-line-libor-shock-hits-currency/

ReplyDeleteJust saw this article, I feel it's pretty relevant to the recent discussion. You may need to register to read the article (you get 1 free article / week).

Inclined to think we see a little follow through tomorrow in the US, but having enjoyed a day of one of the juiciest squeezes in some time, punters might be wise not to overstay their welcome.

ReplyDeleteThere is something happening in Europe, @Nico. I don't know what it is, but the chart for DB and other EZ banks is telling us that there are funding pressures - all is not well behind the scenes. Can't believe EURUSD is holding up as well as it is.

As for the US, FANG is clearly being defanged. Defensives and things like mREITs have traded well lately. We did have a 3% rally in the NAZ today, perhaps that is already in a bear market. Spoos didn't qualify, so the jury is still out.

Hey lefty. When do we say goodnight to the dip buyers?

ReplyDelete"Say goodnight to the cases......you'll never see cases like us again!"

https://www.youtube.com/watch?v=dW37AGZ0Pj0

via https://contrariancorner.com/

ReplyDeleteAbove are a couple of good primers on the impending roll out of SOFR. Stringing out 3 month SOFR futures in deep and resilient packages will be an important step in the rate's rapid jump from infancy to benchmark.

As this roll out has approached, a steady march upward has occurred in the soon to be tar-pitted rate sets that bench-marked money rates for the last 35 years. Much ink has been spilled of late to explain the relentless rise ex-post. Even Seeking Alpha, on Mar 13, posted on the now nearly 6 month rise with a chart. The "deep dive" amounted to "I'm no technician, but this looks like a breakout !" Sad trombone. We have been yakking about this rate adjustment (and cheering on its arrival) since Q4 2017. Now, looking forward to the April SOFR roll out and the May futures contract, these wider and higher sets offer a cushion to the largest switch from an existing rate base to a new anchor in monetary history.

Even with the long lead time for participant adjustment, billions of dollar (and yen and euro) products could find themselves adrift after the disappearance of their underlying. Nearly 2 million Eurodollar contracts traded from Dec 2018 to Dec 2020 last Friday alone. Over $10 T notional amounts remain in open interest covering the same term. This is a BIG universe and its getting a new Sun.

https://blog.pimco.com/en/2017/11/the-thorny-transition-from-libor-to-sofr

http://www.cmegroup.com/trading/interest-rates/secured-overnight-financing-rate-futures.html

Hold on to your office chairs, I am going long DXY. Reasoning: 89 held with outside reversal on daily in progress, descending wedge possible breakout is only half a point away with stops just waiting to be taken out, WTI possible double top, gold possible triple top, euro is in possible failed bull flag breakout reversal. With a lot of "possibles" I am not married to the call, will drop hot potato if it goes under 89 and check my head, but will definitely add when/if goes above 90 and 90.50

ReplyDeleteTargets: 91, 93, 95, 98

I took profits on my bond calls when the market dropped last week. I was with you on the idea of a dollar / bond squeeze, and still am, but I feel like there is too much noise and uncertainty to personally want to get back in. It seems like a very binary situation which will reverse one way strongly regardless of the outcome.

ReplyDeleteA lot of the technicals and other signal items tell me that the dollar is going to rise soon, but a lot of the fundamentals seem to point the opposite way, which is probably why we have so many short. ¯\_(ツ)_/¯

We are out. We enjoy a good squeeze but the easy money is always made early. It was fun, though. Surprised that none of the 12 y-o has popped up to brag about their exploits (ex post-facto). Oddly they never seem to post the dip buy in real time.

ReplyDeleteHave been waiting on the dollar and bond squeeze and do expect to see it at some point. A powerful move up by the dollar and yen together will provide the ultimate macro signal for the end of the bull market in equities.

Bond trading reminds me a little of 2010, another false Spring of overblown inflation fears that ended in a long and painful summer of squeeze for the bond bears.

Oil trading, on the other hand, starts to remind me of 2008. I am half expecting to see a mini blow-off spike in crude ($85?), complete with a frantic catch-up rally by energy stocks, only to be followed by another deep slump.

When we see spoos kiss the 50DMA again, we'd be more inclined to sell than buy. Until then, watching and waiting. Daily calculations of 2s10s and 5s30s provide endless entertainment for the time being.

This is the kind of day when the media taking heads say "stocks began the day higher but have turned mixed". Most of us do well to avoid choppy days like this and do something more productive instead.

ReplyDeleteI may have spoken too soon on selling my long bond calls. 10y yield is approaching the magic 2.8 line once again. The interesting thing here, is that previous times it approached this line, equities were selling off. Today, equities seem somewhat neutral (albeit choppy as LB mentioned).

ReplyDeleteThat smells like risk-off to me, and is also notably flattening the yield curve in the face of short term yields dropping far less.

As for a potential dollar squeeze, my biggest issue is finding the fundamental trigger for a rise / squeeze in the dollar. Where would this come from?

I AM FINALLY FREE FROM FINANCIAL BONDAGE THANKS TO MOORE LOAN COMPANY (mooreloancompany@yahoo.com).

ReplyDeleteGood day everyone,I can’t hide this great testimony that took place in my life I will love everyone to know it and be a partaker of this, that is why I want to share it to the whole world by placing this advert on classifieds, I am Mrs Karen Brown by name, I live in Chattanooga, Tennessee United State, I want to thank ROBBINSON MOORE for his kindness upon my family life, I never knew that there is still a sincere and trustworthy lender like this on the internet and on earth. Just some days I was in search for a loan of $ 100,000.00, As I was running out of money for feeding, School fees, My business was really going out of capital and my rent. I was scammed about $15,000.00 dollars and I decided not to involve my self in such business again. But a Friend of mine introduced me to a loan firm due to my appearance and doings and also my complains to her. And I told her that I am not interested in any loan deal anymore but she told me that there is still a sincere lender who she will recommend me to, And she gave me the details of this man who is called MOORE ROBBINSON. And I really put a trial and I am most greatful and lucky today, I was given a loan amount of $95,000,00 Dollars by this great firm MOORE LOAN COMPANY. If you are in need of a genuine, Sincere, durable and a truth worthy loan lender or financial assistance and also you know you can be reliable and trusted, capable of paying back at the due / duration time of the funds I will advice you to send your contact to them via email @[ mooreloancompany@yahoo.com] OR Test (414) 454-9493 . And you will be free from scams on the internet. Please I am begging everyone on earth to help me thank Mr ROBBINSON MOORE. And I will always being sharing this great surprise and testimony that happened in my life everyday to all that need loans. Contact them now if you are in need of a loan: AS THEY ARE EFFICIENT,DYNAMIC AND RELAIBLE.....Again there contact email [mooreloancompany@yahoo.com OR Text (414) 454-9493.

Nice post Thank you for your post UFABET

ReplyDeletePlease allow comments. Your body, I think read it easily, ball click

ReplyDelete

ReplyDeleteThank you so much.

ดูหนังใหม่ชนโรง

รีวิวซีรีย์ฮิตติดกระแส

ReplyDeleteThanks for fantastic info I was looking for this information for my mission