Stocks are partying like it's 1999. Bonds are selling off, well...like it's 1999. And yeah, real estate in the US is having a good run too, finally showing some signs of life after a long period of something between ok-ish and abysmal returns.

What’s really going on? This is anecdotal evidence--but let’s take a look at the anatomy of a real estate deal from the depths of the financial crisis and cashed out in today's feeding frenzy.

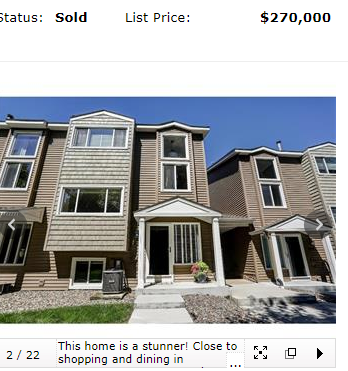

This dandy townhome just sold a few months ago in a neighborhood a few miles from my house. It is a beautiful place...1700 square feet, three bedrooms and three baths, enough space for a small family with great schools. You see the list price above….after a little bit of haggling it sold for $263,000.

In early 2012, the same place sold in foreclosure for $193,000. The buyer bought it with cash and rented it out for an average of $1750 per month over the last (roughly) five years.

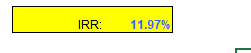

I ran the costs and revenues through a real estate spreadsheet I built and got this:

An unlevered compounded return of nearly 12%. Not bad for what is really a fixed income asset.

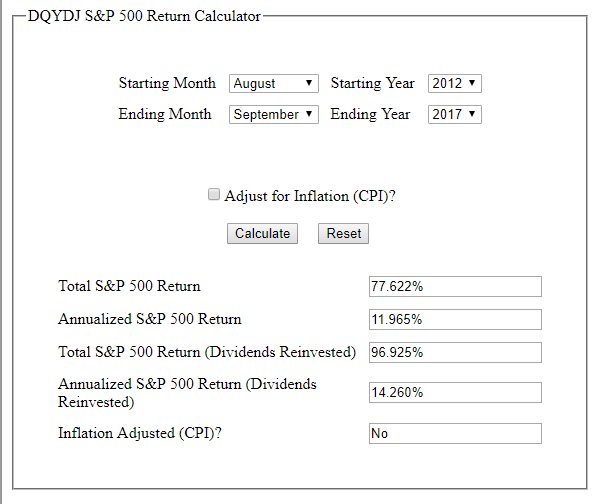

But what was our benchmark? I ran a similar calculation through a calculator I found online for the S&P 500, which considered the total return of the index with reinvested dividends. Here was the result:

Over the same time period, that money would have returned 14.26% in a simple S&P index fund with reinvested dividends. Equities outperformed….

Not so fast, you say. You’re comparing a fixed income asset to an equity asset. Yep, apples to oranges. Real estate, especially if unlevered, has certain equity and fixed income characteristics. I took a look at the total return on a JP Morgan credit index over the same time period. It was right around 4%.

So if I were to have some mix of stocks and bonds and maybe some REITs that had high single digit returns, the return over the last five years looked a lot like the return on a chunk of Minnesota real estate.

Then I think about the implicit returns built into the price of the assets when they were purchased. Five years later, those prices should be able to tell us something about the returns we can expect (or have realized) in the future.

For the townhouse, the implicit return, or the cap rate, at the time of the purchase was about 7.25%. That’s a pretty spicy return in these parts--this townhome is in a tony neighborhood, and one that has only gotten more exclusive in the last five years as more high-end condos have been built in the area and the city has become a destination for fancy restaurants and brew pubs. In short, more rich people want to live there now than did five years ago.

Today, the cap rate on the same property is about 5.7%. So the future cash flow you can expect from the property at current valuations is roughly 150bps less than it was five years ago. That represents the confidence in current values as well as the relative attractiveness of the asset---people are willing to pay more for the same thing today versus five years ago, when the US was at the nadir of a the credit cycle.

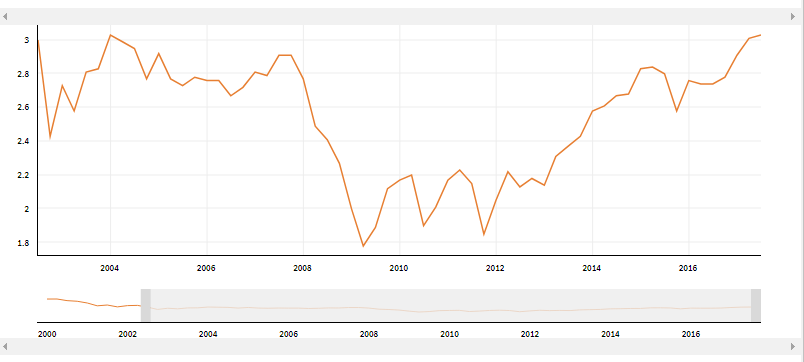

Now look at stocks. In 2012 the S&P sold at a price/book ratio of roughly 2.2. Today that ratio stands just above 3. To put it another way, not unlike our chunk of Minnesota real estate, buyers of stocks today are putting much more weight on the future profits on their assets relative to the book value where they could be sold on the open market.

S&P 500 Price/Book Ratio.

Ok, so maybe I’m not telling you anything you don’t know already--assets in the US are worth much more than they were five years ago. But what struck me about this analysis was just how close the returns were. This is a piece of real estate that was clipped in foreclosure at the bottom of the market, and then punted into a red-hot market five years later, in a neighborhood that was a good one in 2012, but now is one of the most exclusive you’ll find anywhere in flyover country. You could hardly ask for anything more as a real estate investor.

And you compare that to stocks--where the same argument applies! US stocks in 2012 weren’t exactly dogs...now they are the a red hot, multiple offer property that brokers salivate over because they know people are tripping over themselves to buy them.

Throw in a few high-yield USD bonds, which have benefited from the same lust for yield, and you can see a pattern: there is no small amount of financial engineering and monetary steroids that have led to a such a wide array of assets having such a similar rate of risk-adjusted return.

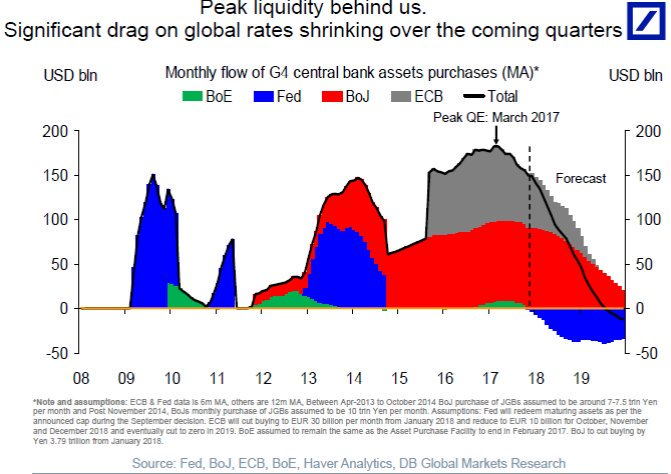

Then I look at a chart like this, follow the path of appreciation of those assets, and wonder what the future might hold as the slope of the line turns negative:

I agree with the camp that argues that the global economy is coming out of a long period of dormancy--one not uncorrelated with the chart above. I think the recession in the US didn’t really end in late 2009 simply because the economy started growing again--it lasted well into 2012 as capital writedowns and a Schumpeterian creative destruction slogged through the American landscape.

Where does that leave investors today? Many would argue the implicit returns baked into metrics like the real estate cap rate or the equity price/book ratio cited above will be pathetic. That may well be. But as investors we have to consider where there could still be some upside.

I’ll put my two cents in for emerging markets. Last week, Jeremy Grantham made a great case for EM equities. I’ll throw in my two cents for EMFX and local fixed income at large, which are driven by very similar dynamics around the global manufacturing cycle and commodity prices.

I think it comes down to this: the benefits of the crash in oil prices combined with increased domestic energy production was a positive supply shock for the US. This caused a huge re-pricing and redirection of flows out of EM and into the US, despite continued massive quantities of global monetary accommodation.

US assets, real, fixed income and equities, were winners throughout the past ten years, but especially since 2015 as this positive supply shock spread throughout the economy. But EM assets hit a huge wall during the same time. Now, with a pro-growth, deregulatory environment in the US and Chinese demand still positive, there is plenty of space, from "macro" as well as valuation influences, for EM to continue to outperform--while much of that positive tail wind is already priced into US equity values.

You can argue that something will change to cause that theme to crack (China slowdown, US grinds to a halt, quanatative tightening, some black swan, etc.) but I think that's the environment we're in for the foreseeable future. The returns from the past five years have been predicated on a monetary sugar high--and one could make money by simply chasing that ball from one jurisdiction to another.

Today, investors are getting back to fundamentals: relative rates of growth and productivity rather than the potential, or reality of artificial stimulus.

Shawn

TeamMacroMan2@gmail.com

@EMInflationista

Today, investors are getting back to fundamentals: relative rates of growth and productivity rather than the potential, or reality of artificial stimulus.

Shawn

TeamMacroMan2@gmail.com

@EMInflationista

42 comments

Click here for commentsto our long only Buystocks who was asking in previous discussion i am well, thank you, and congratulations to everyone riding the US equity blue oyster cult. Remember it ain't about the entry level but the exit - it will be informative to know when all of you Don Quixotes get out of the bubble for good. I fear you might not get out at all, unless you are forced to.

Replythe short spoos is a disaster - at 2300 average - some guys i really respect joined the short at around 2440 (misery loves company), some were more patient and shorted the tax cut news - we are all underwater. But you'd be surprised how fast a 20% correction can strike. One day. I will get out at a small loss, i will certainly not get out before reality hits the fan

i just sold my Brazilian position - yes the one bought in January 2016 when i was going apeshit long oil and anything oil related. It is hilarious to see people cheerleading EM equities now after they have doubled from their capitulation low. Noone wanted oil exposure back then. I don't understand why people refuse to buy low but love to buy expensive shit like the Louis Vuitton equities of America today

some of you may recall i went 100% GBP denominated after Brexit 1.30 and after the 1.14 dip (i caught a lucky 1.18). That currency decision alone, when everyone declared the death of the Pound, pretty much offset the pain on Spoos. I am not sure if it's been mentioned here but if you bought US equities from Europe when Trump took office with no currency edge, you practically made zero. Likewise your short Spoo is sterilised when held in GBP over the period (thank God and the Queen)

regarding recent market calls (Grantham... Dalio... hit peak hubris right now) peeps are trying to pick up whatever is not as extended as US equity universe. This is not proper investment process. Even Italian banks and Greek equities are catching a bid.. as you read already Greece is currently deemed less risky than the US. I spend 6 months a year in Greece, i can tell you that this is pure madness. Nothing has changed there, it is still all about how Iannis and Costas and Yorgos can fuck each other and the government

unless it's the other way around and they now downgrade the US to Greek bananaki republic level - 2.60% be like, 12.60

anyway

markets are slowly starting to behave like markets again, so i might try to contribute some old school thoughts here. i spent most of the time offline explaining bitcoin to my sister and telling peeps who asked, that they were too late for it and most crypto. the same family and friends who sold their US equities in 2009 knowing some of them finally bought them back.. last year. They will not survive when a correction finally hits because the record short convexity will make a 5% grandpa correction extend to 20

i have no idea what goes on in my mom's basement besides my old stamp collections rotting, but i will send you my best regards from a most gorgeous beach retreat in Zanzibar

good luck and keep your eyes wide open

Gotta love the internet. Nico who wrote here of his short spoo position much lower than 2300 (avg), has had the biggest equity ramp in our lifetimes prove him wrong yet pretends he hasn't blown up. Why? Because FX magically 'saved' his losses LOL !

ReplyGuys, here's how you become a "pro-trader nico-style":

1) Pick tops & bottoms. Scream on the internet that you're right and the market is wrong.

2) F*ck risk and trade mgmt. Double, triple down!

3) Keep changing your cost-basis to make your trade appear better.

4) Disappear for 6 months when your trade blows up, and return 4000 ticks higher saying "I was hedged"...

5) Finally, brag of you millionaire beach lifestyle - all paid for by demo account virtual dollars.

I'm off to talk to the bitcoin forums with the kids to engage in some more adult discussion. Ciao!

1) Hearing that Trump US equity rally amounts to zero in EUR or GBP terms really hurt you. Now you are all shouting and bullying like a Harvey Weinstein of financial blogosphere who cannot take 'debasing' as an answer.

Reply2) Obsessing over one asset in one currency makes trading look like Trump's junk food diet. This forum teaches about diversifying amid a world of many trading opportunities throughout the equity/currency/credit/govie/commo spectrum. Learn or die.

3) All the aforementioned trade entries - the good, Brazil, EM currency basket, Brexit, GDP and myriad of others - the abysmal spoos 2200 entry, 2400 double down to 2300 average - are documented in this present forum, back in the days when i participated.

4) You ought to know i made more money shorting European (Italian, mostly) banks and China Q2 2015 and trading Brexit, further helped by favorable currency tailwind than i will ever lose on Spoos when it trades at 5000 tomorrow.

5) Finally, you don't need to be a 'millionaire' to travel and ironically most 'millionaires' don't travel much when they can afford to, too afraid of discomfort far from home. You mostly find normal people in the most interesting, remote parts of the world. I have visited 150 countries and speak 9 languages. What about you? Exactly, fuck you.

I'm off to enjoy my life now reminded that this online pissing contest is a waste of time.

Nico, thanks for the lolz; you're an even bigger fantasist than the bitcoin HODL'ers. Whilst it would be easy to pull apart your puerile response, I frankly can't be bothered to argue with a fantasist.

ReplySure, I've bragged about big wins with long equity positions, but I'll never understand why people find ego satisfaction in pretending to make money when they clearly don't. Enjoy your Walter Mitty charade!

(PS Don't bother replying, this really is my last post).

What I find most surprising about this is the rental yield. Coming from the UK where houses are renting at sub 3% yield this is >7%.

ReplyNico, nice to hear from you and even if the unidirectional single asset short term traders don't appreciate you, I do.

ReplyI especially like your buy doom sell ecstasy basis and I agree with you that the market is currently weighted on the tips of its skis. I just don't know where the lump of ice on the piste is.

Pol

@Blackraven, just to be clear, the rental yield *was* +7% at the bottom in 2012, and now is somewhere on a 5-handle, which is consistent with the broader spectrum of high-quality real estate around here. Just for laughs I looked at a few places in the famously pricey San Francisco suburbs a while back, and while I never did the math on the cap rates/yields, the rents were noticeably cheaper relative to buying a house. I would expect yields are in that 3% neighborhood, and price in an expectation for returns from a juicy capital gain rather than income/carry.

ReplySame story as stocks, just California style.

NQ short is a scratch. Let's revisit after FANG party next week. No need to force a trade that came back to entry twice.

Reply@Shawn, the most interesting (from boom to bust and back to boom standpoint) aspect of real estate recovery may not even be on the improved side. Vacant land has handsomely rewarded (by many multiples in some cases) those who stepped in to buy from defunct builders and banks which ended up holding the bag.

The problem I have with EM of any asset class is the dollar.

Reply@IPA, I'm sure you're right on land--but I wonder if it isn't quite the same as my examples above? Could I have bought five acres of land around here and doubled my money over the past five years? I imagine the answer is probably yes in many places, although far from a no brainer here where the marginal development land is agricultural, and back in 2012 ag prices were nearing the end of a very good run and farmers were busy levering up to buy more land, equipment and tractors (which is now turning into a bust--the the subject of another post).

ReplyBut take a look at that S&P500 return calc--98%. That's tough to beat if you had to pay cash for the land. if you could have found some bank crazy enough to give you leverage, yeah, you made an absolute killing; it was the vaporization of that credit channel that created the opportunity in the first place.

@Shawn, agree, the buys had to be strategically correct in order to return more than SPX. I am with you on the ease of it as well, just acquire the SPY and sit on it while collecting div, dumb enough, no offense to anyone here. My thought was more on builder distress and the infill (and sometime tract, albeit looks like not in your area) land deals that ensued. The idea was to show up at every trustee and tax lien sale with a blank checkbook (more like multiple cashier's checks) and snap the deals of the century while they lasted. Fast forward, today you can't even get your bid in, the room is full of amateurs and the prices are outrageous, that's if the lot is even buildable at all. This trade is over by all definitions.

ReplyIf one believes the ironic path is the path events take, then ... China soft-landing after the National Congress leads to a huge bull market there ... and QE ending without causing markets to collapse causes the stock of still idle liquidity created through QE to pour into stocks. The absence of the bad gives green light to sidelined buyers to step in. Just a thought ...

ReplyQE cash/liquidity pours into stocks >>> Lack of a blowup as QE unwinds causes cash/liquidity to pour into stocks.

ReplySounds about right. Sure, why not. Still space for Draghi, Koroda, Bernanke and Yellen on Mount Rushmore?

johno...."The absence of the bad gives green light to sidelined buyers to step in"

ReplyNo ones buying anything. It's not working for anyone , especially some unknown that comes along with a bid and chain and ball.

johno....."The absence of the bad gives green light to sidelined buyers to step in"

ReplyThe rich and famous bullshit is over.

Has everybody here capitulated on shorting the market?

ReplyNow may be the time

Interesting stuff. Your analysis does support the general thesis that you can buy anything at the start of QE and it will make money as the process of asset price inflation proceeds. Good observations there about the change in housing market participants, it feels more like 2005 than 2009, with mini housing bubbles appearing in some of the most surprising places.

ReplyPCE headline and core prices, 1.7% and 1.5% y/y. Not exactly screaming hot, makes you wonder whether break-evens are already ahead of themselves. Yields spiked ahead of the numbers but are now pulling in. Of note, the long bond has resisted any and all efforts to drag the yield to 3.00% and above.

DX is firmer today and equities and crude oil are lower, following China overnight. That's a change from the pattern we saw in 2017 when USDJPY and Spoos were in lockstep much of the time. In fact this morning, if sustained, is a good old-fashioned risk off recipe. This might be a one day wonder, but we'll see. EURUSD move really seemed over-extended for a while now, there are some signs of FX regime change here, and that has often preceded a turn in market momentum in the past.

If we do get an unexpected USD bounce from here, then you wouldn't want to be in EM equities, debt, carry trades like AUD. We are still looking for weakness to show up first in US high yield and small caps, but given the vol selling trade it's possible that everything moves together this time. It is notable how the VIX has been moving sideways or "building a base" as equity bulls would usually describe such a chart, even as spoos have drifted up.

We are long UUP and short IWM and SVXY, for the time being.

I'm going in. 60% short SPX with stop at the highs. Wish me luck. Stop is so tight it can only lose a fraction of the monthly gains in Fiat, Brazil, Afterpay etc.

ReplyThis is as singularly bullish as I've ever seen the market

Crypto well and truly rolled over. First fraudulent darlings going down. Sydney real estate rolling over. Record speculative longs in the euro and crude.

ReplyMeanwhile 2 million Walmart employees getting a 10% pay rise. I'm sceptical of doom mongers on inflation but maybe even for the US that moves the needle. USD down too. All somewhat inflationary, no?

Might try and get ahead of the data on this one.

Agree USD seems over-done here. My bullish EURUSD structures actually get short from ~1.25 and I just got long USDs with tight stops here within the hour.

ReplySee different accounts of what reserve managers might be up to, but interesting to see custody holdings in the US falling while EMs that report daily/weekly have been adding reserves, i.e. suggests diversification away from USD. That's something to watch. JPM argued the opposite in F&L piece this weekend, but unconvincing. GS meanwhile has some interesting analysis suggesting bond fund managers are still long USD relative to history, which I can believe (but then, why wouldn't they still be, given carry). Despite all that, feels like we can rally a bit.

Interesting that the narrative in JPY last week was all about hawkish interpretations of Kuroda's comments while the JGB market keyed off very different (dovish) remarks in his post-meeting press conference. Two markets at odds.

With markets +7%+ in less than a month, I wouldn't say your trade is crazy adamantic. I've tidied up my book a bit and am long April VIX small (which has worked in different conditions the last week).

Guys, let the FANG party pass. No better blow than the one to the hangover head. I hate violence, by the way ;)

ReplyOn US dollar... Nothing ever travels in one line.

In a "straight" line, I meant on US dollar.

ReplyYou want to have some credible tops develop on risk here, imho. Take WTI below 65.19 and NQ below 6924 on daily closing basis and it gets interesting. Until then, you are not supported by charts but simply by the notion that this has gone too far too fast. I tried last week, ain't working. Let the charts develop. Plenty room below those breaks.

http://thereformedbroker.com/2018/01/24/stock-market-reversals-can-cause-recessions-too/

Replyonce in a lifetime contrarian thought from the excellent Josh Brown (whose bullish acumen has always been painful to read when short)

we must remember:

in March 2009 the stock market bottomed amid the greatest fear, while Roubini called the S&P to fall further to 400 and minutes before Goldman was meant to go bankrupt. It took one earning surprise from Citigroup to get the machine going

i had bought 720, and 700, and when market broke 700 with force i had to switch machine off hoping to not get liquidated by a crash. It was unbearable. Then market bounced 30%. Of those who bought the bottom i know noone who trailed further because awful news on the economy kept coming and pretty much every technician was calling for a retest of the low.

We must remember this: the stock market bounced AHEAD and never looked back. Ahead of TARP, and pomo, and the QE saga. We must remember that. The bull market began amid horrible news.

We have the mirror situation of March 2009 today with Finviz 100% complacent. Davos 2018 imnsho will prove to be the peak of self congratulation and beatification of Greed for years to come. Fine technicians today write that if you miss the top, you just wait for a lower high and check for RSI divergence to short or not. I very much doubt the market will be that cute. The max pain is gap, crap and never look back.

The way Josh writes it today, it could take just 24 hours for fear to come back and for doom gloom to populate finviz headlines. To read everywhere that nothing can go bad 'because the economy is strong' is wrong on so many levels. It gets the causality/reflexivity of markets totally wrong. And almost noone is doing their anticipation homework of what happens to balance sheets and discounted flows (earnings) and ultra leverage economies when rates are going higher

Noone has written anywhere that Japan Inc. would go bust if rates shot up 150 basis points. Noone has written anywhere that the minute Draghi goes QT, Italy goes bust and the euro follows (that should give colours to long term EURUSD traders)

at some point smart money sees all those problems and executes accordingly - the stock market tanks without any warning from the 'economy' and like Josh writes, the recession feared becomes self fulfilling.

good luck adamantic and you are not alone

Nico G, I hear you... No disrespect to those fortunate enough to feel the tops and bottoms like none others and go all in to break the bank. I am of an opinion that one stays in business while remaining humble and nimble in order to avoid repeated blow-ups and stay confident enough to continue to trade and actually have the dry powder to apply in cases of absolute u-turns you precisely mention. I am no "fine technician" you brought up, but I am a student of price. It simply represents the balance of buyers and sellers that I can see right in front of me in real time. I can't see far in advance all other (mostly anticipatory and/or anecdotal) things you said until they are somewhat apparent (for the most part). Hence I rely on charts for most of my trading. Please excuse my dumbass approach but it's this one simple technique that keeps me in business and until it fails me I'll have to use it. Believe me, I will not be far behind the heros laying on the side of the road with arrows through their hearts. I just don't want to be one of them.

ReplyNo technique no method is wrong because there is no perfect trading system either. Even the best algos are self learning. Even Rentech has to hire more and more phds to stay ahead of everyone else.

ReplyAt our humble level, following price as main news like you do is all but a dumbass approach and probably the best one. It takes a lot of discipline to keep emotions and personal conviction out of one's trading.

If you let emotions and conviction dictate your trading (here), only the exit level matters. You can be underwater for a very very long time. The key is to keep on trading other things on shorter timeframes than the one you're trapped in in order to stay sharp and motivated.

If you keep your initial punts fairly small, the arrows bounce off, even if they do sting a bit.

ReplySpeaking of Price… keen observers of the inverse vol complex will have noted that SVXY is now 10% down from its highs. These punters are being killed softly as the VIX drifts upwards almost imperceptibly. It's not the spikes that kill you… although if and when the VIX spikes the vol sellers will all be carried out en masse.

Is the Top already in for vol selling? Peak Complacency, anyone?

You'll know where at the top of the "greatest bull market" in history when news media , advertising and casino CEO's lobby networks start going in to bat for the fiddlers of high frequency trading networks. Where there now.

ReplyYou know what really is amusing with this finance market. It is trying to learn your trading craft at UNI and having to translate the current market conditions from the finance textbooks. You get to feel around the finance literature and ultimately decide.....weeeelllll.....this current macro economic climate doesn't fit in with this billion dollar company's specialization so we'll have to cut that out. Aaaaaaaaaaaaand this company's seems to be heading in a direction that has no coming back.....weeeelllll.....we'll have to leave that out. Very amusing!

ReplyToo true, Amps, too true.

ReplyThe VIX hit 14. It's been a long time since we have experienced the F word in this market. Yeah, that one. FEAR.

Can't help wondering if there will be a whiff of it in the air before long as punters in the short vol complex are forced to cover. The SVXY is now down 15% from its peak. A little more of this and it's a "bear market" for vol selling.

OTOH, Spoos down 16 handles isn't a big deal, unless a disorderly unwind of the short vol complex unleashes the kind of forced selling that observers have often postulated might occur. If it does happen, a lot of people are going to find out that their portfolio is "not diversified" after all. :-)

Personally I would love to see that pompous prick Dalio with egg on his face after his recent pronouncements. How about a nice drawdown in AUM, Ray, before the PC police come to Westport and cut you up into little pieces? I am sick to death of the Cash on the Sidelines arguments from him and all the other carnival barkers.

I have to say I didn't really understand Dalio's whole "nice delevraging" spiel while at the same saying that after another 1% in rates it'll be dicey, ie having real rates of ~25bps is close to the end of the world, but having cash you'll feel foolish. Sure we all talk our own books but he's clearly married to the leveraged long treasuries position.

ReplyIn one of the first, and more regrettable pieces I ever wrote on the markets was a letter to the editor of the local newspaper blasting their reliance on a local equity manager's quotes that "there is cash on the sidelines" waiting to buy this market. I even cited a lexis-nexis search where I tagged that quote nine times in six years from the same guy. It's a great multi-purpose tool. And yeah, I agree totally on Dalio.

ReplyAlso today as we look fearfully at a market that is down 27 handles, I remember ten years ago this month that Jerome Kerviel nearly blew up SocGen. I remember the day--it was US holiday so I was in just to catch up and tidy up spreadsheets--I walked into the office, dumb and happy--looked up at the scoreboard-style ticker on our trading desk and it said S&P futures were down 58 points! Off a base 60% lower than today's near-2900 level.

What marked that day was not only the kick off of the second movement of the GFC concerto, but also the move in treasury futures. They rallied BIG.

Today S&P down not even 1%--there's short vol fear....but no bid for fixed income. So is there really any fear? I'd argue no.

Glad you called me out as Amps, Lefty. Anyone reading my musings here over the last 5 years could easily call me out as "Blue Jasmine".....but they'ed be wrong on this occasion, as I'm not the one getting bent over by hedgefund managers.....not anymore.

ReplyBut they have had me talking to myself on park benches, quite often!

ReplyOne does what one says. Unless WTI rallies into the close and settles above 65.19 this trader will be looking to short it on the move to backtest 65 level during Globex, especially if API report is "rosy" and helps to achieve the entry.

Reply@Shawn, I remember that MLK day vividly. Historical moment indeed. Led to the largest Fed Funds rate surprise cut ever the next morning. Those were the days...

Yeah, Shawn, agree we're not seeing fear yet. (Temporary) buyer's strike seems a plausible description of what we're seeing.

ReplyStill trying to catch a short-term bottom in USD. Market keys off EURUSD where the EUR 5Y5Y inflation swap trend has arguably broken trend in place since June. Also, Bloomberg citing officials saying even the ECB hawks favor a 3-month taper after Sep. And then there's today's German inflation data, which under-whelmed. Draghi's communication still links QE to some evidence between now and tapering of inflation lifting. So far, nothing on that count. Meantime, dollar shorts are eating negative carry. All this might put a break on how fast EURUSD can appreciate. Some people will say markets will just move regardless of central banks, now that the Euro-zone expansion is sustained, which is all very nice, but tell it to the people who have been short EURSEK these past years. The ECB can screw you by pushing out timing and letting speculators twist in the wind. The other observation I bring in support of a slowing in EURUSD appreciation is a long-term chart of the 10Y EURUSD forward. We're not at peak levels but we're getting there.

All that said, I think the USD bull is over and to play a USD bounce, TWD, SGD, and CHF have been more interesting to me.

Thanks, I'm glad to work with all of them.

Replygoldenslot

Great post.Thanks for sharing this wonderful information. Useful for everyone. This is a very informative blog.

ReplyMortgage Rate Calculator

Please keep us up to data like this. Thanks for sharing and Keep on writing... MM

ReplyYou provide the correct information here I really bookmark it, awesome... MM

ReplyKeep up the Excellent quality writing, It is rare to see a nice blog like this... MM

ReplyThanks for sharing excellent informations. Your web-site is so cool. lnformative site... MM

ReplyThank you for all your valuable labor on this web page. You have a fabulous job... MM

Reply