So the BoC went ahead and did it. That’s two hikes, and unwinds the cautionary/pre-cautionary hikes of 2016 when oil prices were code blue.

“Recent economic data have been stronger than expected, supporting the Bank’s view that growth in Canada is becoming more broadly-based and self-sustaining.”

They’ve been telling us that for the past two of three years, is it really happening now? Poloz and Co. go on to mention that the global economy is picking up, and more synchronous than in the past--which is also consistent with some of the strong, or at least persistent, growth data out of China, and the spectacular move higher in base metals, which portends continued strong manufacturing growth.

But we haven’t seen much outperformance in CAD….at least not compared to its commodity currency brethren.

The 1.2% stronger move today should put a little space between the loonie and AUD...

And NOK...

And this should leave behind the newly resurgent CLP, which has again crawled out of its low-real-rate grave thanks to the amazing run in copper prices.

As I mentioned yesterday I thought we would see a slowdown in China and metals prices by now that would cause commodity currencies to give up some of their YTD gains. John Maudlin had some good points on this from one of his buddies at “China Beige Book”, a research outfit I’ve never heard of but one that made some very good points on the resilience of the China credit/growth re-boom:

“A lot of this now seems consensus – as all good assessments should in hindsight – but if you recall at the time (mid-to-late June) there was growing sentiment that (1) the economy had already peaked for 2017 and was now starting to slow; (2) deleveraging was having a major effect on corporates; and (3) the commodities sector had likely peaked in Q1 and was now in slowdown mode as well. Our data undercut all of these.”

“CBB data show aluminum firms wildly outperforming the current market narrative, seeing broad Q2 gains in revenues, profits, volumes, output, and new orders, as well as cash flow, which jumped into the black for the first time in our survey’s history. The why is less clear than the what, but one obvious possibility is aluminum is the latest recipient of some of China’s excess liquidity. “

“In Q1, corporate reporting to CBB showed credit tightening was limited to interbank markets. In Q2, it hit firms: bond yields and rates at shadow banks touched the highest levels in the history of our survey, and bank rates their highest since 2014. So why did borrowing not collapse, denting the broader economy? One reason is what we call the “Party Congress Put.” While borrowing did see a mild drop for the third straight quarter, companies’ six-month revenue expectations remain robust in every sector save property. Companies assume deleveraging is transient, likely because they are skeptical the Party will allow economic pain in 2017. It will not be until 2018 when we find out whether deleveraging is genuine – because it won’t be until 2018 that it will actually hurt.”

Bottom line, these guys mention the deleveraging and tightening is hurting property firms and cash flow….but that isn’t hurting the broader economy….yet. When does the other shoe drop? Well, not until well after the party congress at the end of October. Will copper stop its crazy run higher before then?

EMFX and the commodity currency club is poised for continued strength-- with inflows continuing--and yesterday's Brainard comments signaled the Fed is not going to get in the way any time soon. If inflows persist and start to seep into FDI and the broader economies in commodity driven economies...welcome back to 2005-2006. Canada doesn't seem like a recipient of those flows so long as oil is still stuck in the 40s, but that theme should be intact for those driven by base metals in Australia, Chile, maybe even South Africa. Low natgas and oil prices will benefit those countries too...as well as soft commodity exporters like Argentina.

What else is going to throw sand in the gears? North Korea? the ECB? A trade kerfuffle or a NAFTA trainwreck? Not seeing any likely culprits here.

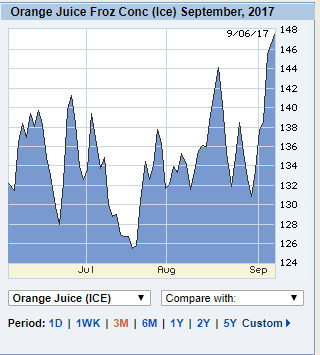

Back in the Atlantic, no macro opinion on the natural disaster front...just prayers to everyone in the path of Hurricane Irma.

Took me a sec to realize that was what was driving frozen concentrated orange juice futures.

At first I thought it was the Dukes. Which I say just to have an excuse to post this, which I think every trader should be required to watch as a part of his or her training.

Stay safe out there!!

12 comments

Click here for commentsBest Packers And Movers Chennai List for Get Free Best Quotes, Compare Charges, Save Money And Time, Household Shifting Services...

ReplyPackers And Movers Chennai

Taking half off KRE and XLF shorts here. Stops moved to b/e. TNX is crapping, they follow.

ReplyPutting the profits onto XLE, XOP, OIH, and UNG. Folks, there is going to be an epic rally in energy into the end of the year. Better catch it, I think it has begun.

Best. Movie. Scene. Ever.

ReplyIPA. What's the catalyst for the epic oil rally? Trump takes action against Venezuela and/or Iran? OPEC surprises with another cut/extension in November, led by Aramco-conscious Saudi? None of those scenarios seem far-fetched to me. Still, the 1Y forward is capped by shale production. Maybe a bet on the widow-maker CLZ7CLZ8 going into backwardation the way to express the view here?

Shawn. Feels like we'll dance to the edge of the China cliff in 2018. Assuming there is a cliff in 2018, that is. China bears by now have the credibility of the little boy who cried wolf.

+FEZ/-SPY. Look. Everything we told ourselves about Continental Europe versus the US is wrong. We told ourselves they had fractious lefty governments while we had a decisive two-party system. Look there in France -- an INVESTMENT BANKER got elected, with a parliamentary majority, and he's implementing labor reform. In France! Look there in Germany -- coalition government led by conservatives. Italy? Hey, when push came to shove, they had technocratic government reforming entitlements in ways "rugged" America won't even contemplate. In America, if the Millennials bother showing up to vote in 2020, we could have Bernie Sanders in charge. Where's the last bastion of capitalism? Where's your safe haven? Continental Europe. You should be selling every American asset not nailed to the ground, and putting your wealth in Europe.

How would you have liked to buy the US market in 2010? We are in year ONE of the European profit recovery. Operating leverage, baby. Plus, rates are low, corporate balance sheets comparatively un-levered, and with profits turning up, CEOs may have confidence to start levering up. Equities too punchy with all the uncertainties and rates too low for fixed income investment? Buy German real estate! It's listed. VNA GR. Easy. Click. Buy.

Opposing views most welcome. But seriously, dollar bulls from 103, put a fork in it. No shortage-induced dollar squeeze higher until the next global recession, whenever the hell that is. Think Stephen Jen's dollar smile -- we're at the bottom of the smile.

Stephen Jen? We're kickin it old school, I love it...

ReplyI like you're euro/US theme--Europe is indeed growing. As I alluded to back at the election, I'm not buying what Macron is selling....it is still France! Maybe he gets labor reform done, but I continue to believe it isn't the game changer he would have us believe. But your point is a valid one--the governments in Europe are much more business friendly relative to the US than we generally give them credit for, something that is probably not priced into valuations here.

I'm all ears on what would drive the oil rally--i was just thinking that yesterday--will oil catch up with the rally in industrial metals, or is the elasticity of supply just too great? my gut is with IPA on this one but looking for what the driver/catalyst will be.

I also write advertisements for e*trade ;)

Replyjohno and Shawn, on energy... I am just following previous chart patterns:

ReplyWTI Oil Feb 2009 - Sep 2010 (Feb 2016 - Today)

Nat Gas Apr 2012 - Sep 2013 (Mar 2016 - Today)

Simple... I think both are getting ready to rip.

Johno, I am with you on the dollar bear story but I think there's a story to be made on the bull side. First, there is very little priced in the rates space for US, look at EDZ7EDZ8. Sitting at 20bps I see the risk/reward as very skewed especially given how sentiment is now. Also, whereas 10y made new lows today , the ED spread didn't and had a demark 13 on the daily yesterday. If you look at front-dated ER-ED boxes they also look very extended historically. The issue is what will be the catalyst, I see one. Not a new concept but put GSCI 1y chg vs US CPI, it's pointing up. The same it was pointing down early on the year after the Trump craze and allowed me to make some good money on it, I expect it to go the same way now. I am skeptical of high inflation but I also don't buy the story that suddenly EZ is the growth king and US is dead. Underemployment is still huge in EZ so I have very little hope in wage growth ex-Germany but in the US it will show up sooner rather than later. Old story but I think this scenario is not being priced in correctly.

ReplyOn the EZ/US side I strongly agree with you. Previously, I saw NPLs as the biggest hurdle to companies levering up as they can't lever if banks don't loan them the money. Now , I see the tide turning. Not necessarily that NPLs will disappear at insane rates but I see some very interesting moves. For example, in Portugal I heard that BCP management is feeling very optimistic about current earnings as they are able to dispose of NPLs. There are also seems to be a govt & bank consensus on how to handle this issue quickly and I read some stuff today on new proposal being announced 1 week from now. It could be that the proposal is ill-prepared as we have seen a few in the past but from what I am hearing it seems this time might be different. If this changes it could really push banks up and the rest of the mkt along with it.

Thank you for the feedback, Shawn and MacroWatcher.

ReplyJust looked at GSCI 1y chg vs US CPI. Good point. Similar relationship exists with EZ inflation, so EURUSD implications somewhat ambiguous. Could certainly say that US economy is tighter, so more sensitive to inflation uptick. Guess I buy that. However, I would say that the EZ is still relative growth king for simple reason that US real growth trend will converge to productivity while Europe has lots more unemployed labor, so its growth should be productivity plus newly employed. As for wage growth, after a long struggle, I'm in the "seeing it is believing it" camp. Maybe I'm a good contrary indicator in that. Wouldn't be the first time!

By the way, just as I was writing off any USD-liquidity considerations until the next recession, Goldman was writing this: "The details of the debt limit increase are somewhat different than in the past. Under the legislation, the Treasury will still be able to use its “extraordinary measures” to extend borrowing capacity past the December 9 reinstatement of the debt limit deadline, contrary to early reports that this would be prohibited. However, the agreement allows the Treasury to issue debt sufficient to bring the cash balance to $150 billion on December 8. This will allow the Treasury to return the cash balance to a near-normal level in the interim, drawing it down to $150bn (rather than the $25bn level common around prior debt limit deadlines) by December 8, and then raising it again." So maybe we get a partial USD-liquidity suck in the not-too-distant "interim."

MacroWatcher, pull up 2009 DXY Weekly chart. Begin from March and compare to this year. May start rallying around the beginning of December. Go long on a close above 8ema. Or on consecutive close above it, if you are a conservative trader.

ReplyShort gold/short usd/jpy. Try and catch that 6% spread. 2.5% stop.

ReplyEnormous confluence of moving averages at $47.70 on WTI. Picking up some on this pullback @ 47.75 right now.

ReplyWinDrawWin.com: Casino, Hotel & Event Center Tickets - JamBase

ReplyBuy WinDrawWin.com: 대전광역 출장안마 Casino, Hotel & 보령 출장샵 Event Center tickets at Ticketmaster.com. Find WinDrawWin.com: Casino, Hotel & Event 포천 출장샵 Center venue 밀양 출장샵 concert and event Jan 14, 2022John FogertyJan 21, 2022ShinedownFeb 18, 2022Hold 거제 출장안마 'Em Up