Last week I posted some thoughts on Brazil, which I concluded by mentioning that I am optimistic on the outlook there, without getting too deep into the weeds on what that meant, given the combination of a volatile political situation, a strong rally in asset prices, and fair to strong positive expectations already baked into the market. Frequent contributor Johno rightly posited a few questions--questions I should have dealt with in the initial post. Without further ado:

- I see Meirelles saying a pension bill would generate 75% of savings originally planned while a doubter like CSFB sees 30%. A big spread! Any view where in that range a bill passes?

I mentioned the pension reform as a potential game-changer. As Johno mentions, the problem is how watered down this thing gets. The initial proposal would have been a good fix, but Temer administration already offered to water it down in May, and that was before he was caught on tape signing off on bribes, and subsequently accused of outright corruption. Looking back in my notes, JP Morgan expected a reform to be passed with 70% of the initial savings...in April. So go ahead and fade that number to anywhere between the bearish 30% CSFB figure and, let's say 50%. That said, to the extent the current congress can break this taboo would still be a positive--especially after the election.

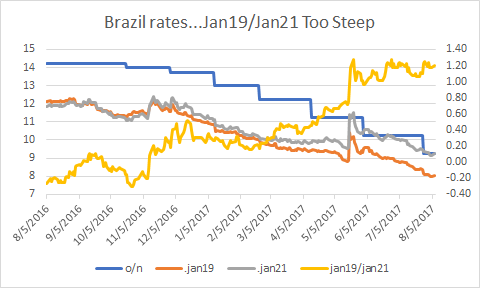

- The DI curve sees about 125-130bps of cuts in the next year and then >100bps of hikes the following two years. You alluded to value in (fading) that steepness. Curious how you think about that. A call on prolonged slow growth, or structurally lower inflation and maybe lower real rates?

The terminal rate is currently around 7.5%, with some steepness going into the election, and a return to double digit rates as we move into 2019.

The forward curve shows a couple of interesting points--first is the steepness implying hikes throughout 2018. That aggressive in an election year without a bounce in inflation--while this is possible, I don’t think it is a certainty so long as taxes are going up, fiscal policy is tightening and BRL is strengthening. Certainly the latter could easily change by 2018, but who knows.

The second point is the continued steepness to what appears to be a “neutral” level near 11%. If one were to assume a long-term inflation rate of 5%, which is 1% over the center of the central bank’s target mandate, that is a real rate that is still nearly 6%.

I hear you thinking, “hold on there hombre, wasn’t it just last week you were talking about the central bank’s low credibility and lousy inflation targeting credentials?”

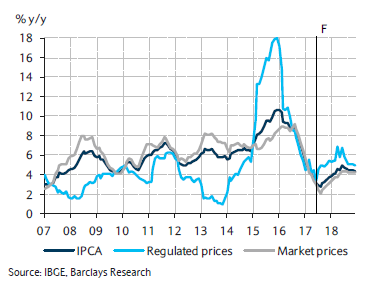

Yes, that’s true, and certainly warrants a term premium. But you can see in the inflation history that CPI bounced around 6% in an era of unprecedented commodity prices, fiscal profligacy and monetary irresponsibility during the reign of the Lula/Dilma/Tombini axis (read this brilliant article by former MS Latam economist Gray Newman to learn more about this era in Brazilian economic history). With a center-right president, chastened congress, a more orthodox central bank board and governor, tighter fiscal policy, and lower commodity prices, medium term rates of 6% real on 5% breakeven is way too high if you buy into the reform story, which would clear the logjam of red tape and bureaucracy that has held down Brazilian productivity for generations.

If structural reforms pass, long-term breakevens and real rates will fall. Simple as that. And the Jan19/Jan21 flattener is a great risk reward if the central bank doesn’t cut quite as aggressively as the market thinks right now, but then leaves rates in the basement during 2018 which we can’t rule out quite yet.

- How worried should we be about Lula?

This is really the fulcrum around which the rest of the long Brazil thesis rests. I think Lula has been strong in polling thus far because of a) name recognition, which goes a long way anywhere, but especially in Brazil, and b) he’s still the leftist flagbearer, despite his recent conviction and subsequent prison sentence due to corruption charges.

But I don’t think he is going to win, in fact, he may not even get to the starting blocks. He will have to win an appeal to even run, which may or may not happen before the election. But as Johno mentioned, while he is polling in the high 20s-low 30s, this is a block of people that have supported him for the past thirty years and would continue to support him even if he showed up on TV wearing a sportsuit made of gold and holding a suitcase full of cash. The rejection rate is the key thing for Lula--there is probably a bare majority of the electorate that wouldn’t vote for him under any circumstances.

In the end, it is indeed not unlike Le Pen in France--even if he is eligible to run, he will suck the oxygen out of the leftist movement, despite being unelectable. As such, his candidacy is if anything a positive--and would likely turn up a few buying opportunities along the way, just as we saw in France earlier this year.

What does that mean for the rest of the field of presidential candidates? One “name” is Marina Silva, another leftist but more of the “green” variety. She doesn’t have the political machine or the money to make significant waves nationally. Same goes for other candidates from the left like Ciro Gomes, who will still struggle to get away from the legacy of the PT.

On the right, there is Jair Bolsonaro. He has been rising in polls lately but is probably unelectable due to some views that are, erm...let’s just say “old school”.

Bolsonaro's rise in popularity illustrates the strengthening hand of Brazil’s conservative movement. This will play into the hands of two center-right candidates from the PSDB, João Doria and Geraldo Alckmin. Unlike Aecio Neves, they have managed to steer clear of the Car Wash scandal, are center-right known quantities and will be cheered by investors, yet don’t have the baggage of a guy like Bolsonaro. Despite the filth of the political system at large, the PSDB money and machine will be of great importance--there just isn’t much breathing room for an insurgent candidate.

If one of those candidates wins in 2018, he will have the mandate to push through stronger reforms and tighter fiscal policy. So while there are certainly landmines in the next 12 months, I don’t see a candidate that is likely to reverse or sandbag the reforms that are necessary to put the country back on a sustainable growth path--in fact it is quite the opposite--there is likely to be a supportive government, a more reform-minded congress, and an orthodox central bank. That is a combination that Brazil hasn’t seen since, well….forever. The market is still trying to wrap its hands around that.

To sum it up--we could also spend some time drilling into the relative value between Brazil and similar credits, equity valuations, or recent performance of BRL relative to high beta EMFX. At the end of the day Brazilian assets have performed well over the past year, but not dramatically better than the rest of the asset class given the massive tailwind for EM. There is plenty more to go if the politicians can deliver.

Shawn

TeamMacroMan2@gmail.com

@EMInflationista

Shawn

TeamMacroMan2@gmail.com

@EMInflationista

17 comments

Click here for commentsHey, TMM. I see the Jonah strikes again. No one will listen to me. The Jonah has ways crashing the foreign exchange market to its knees that you couldn't imagined even if you were teleported back to Woodstock.. Keep him over there.

Replyps..Jonah, I couldn't care less if I lost the pot that I piss in. Jonah's still exist and I managed to stay alive to prove it! I will be rewarded in the next life.

ReplyNice work Shawn!

ReplySome thoughts from a Brazilian hf I like

To conclude, a few words about Brazil, one of the main examples of complacency that we see among emerging markets. The country’s fiscal situation together with increased political uncertainty makes us more pessimistic, despite the improvement in the monetary side and in the balance of payments. Debt dynamics are clearly unsustainable taking into account the prospect for potential growth. On top of that, idiosyncratic factors such as the bankruptcy of several states will require even further fiscal effort from the federal government. The medium-term outcome of this mess will be a large increase in the already high tax burden, given the rigidity of the public budget and the political difficulties for deeper reforms

Im more of an equity/credit guy vs rates/fx so I dont have much to add to your thoughts, though I think most of the re-rating in Brazil happened already. Investors seem to like the 2Q earnings from the banks, though not Cielo which is still in the dog house.

yeah those are all valid points...that's what makes the market. It really is all about the politicians...if they were more reliable the country would have been fixed already. But i think the points these guys make are precisely why they will finally have to get their act together--and after the election the right people will be in place to make it happen.

ReplyAnother great post, Shawn. Thank you. Yes, even if only some parts are passed, markets may take it positively. Really an election bet, in the end, and there I found your analysis of Lula fascinating. The idea that he "sucks the oxygen out of the left," increasing chances of a non-left/reform-friendly candidate winning, is really interesting!

ReplyCan't we all just get along? Doubled up on SVXY puts. It has a look of a major plunge coming. No hunch, but when you have series of bearish engulfing in last 10 trading sessions culminated by a juicy daily reversal you gotta believe we are near one. Will sit tight and let the big-mouthed leaders figure this whole nuclear authority out. I hope Dennis Rodman can save the world. Was he ever on Apprentice?

ReplyA little closer to home... Those who rode the XRT wave off of $39.70 double bottom should take some caution here. While it is looking like it's about to break out of the W formation, the last three of those were all fakeouts: 2/22/17 - 5/10/17, 4/20/16 - 8/23/16, 11/3/15 - 3/30/16. Big retailers are reporting this week. I am taking profits and moving stops up.

Finally... I am going to add more Gold here. Pretty much the same thinking as above on SVXY. The world is a scary place. You can play golf all you want. You ain't gonna solve the problem by talking tough between the holes. Just plain silly!

There are going to be a lot of noobs out there this month and next who are focused on "the catalyst", i.e. in this case the "news about North Korea", and they will be trading for a while based on "nothing is actually going to happen". What these punters, in their naïveté, don't know is that the nature of the catalyst doesn't matter. At some point, it isn't going to matter to them what the North Korea news is, all that matters will be the margin call they are suddenly looking at, in some cases for the first time in their life.

ReplyOnce a catalyst has appeared - and the market has turned - the narrative in the media can quickly change to a negative tone, and once that happens, the catalyst itself ceases to be important as the correction takes on a life of its own, driven by margin, leverage, high volume and that ages-old mixture of fear and greed. Like IPA, we have been especially interested in SVXY as a vehicle for the unwary and inexperienced, and wondering how far and fast that thing might fall. It has risen 400% since Feb 2016.... vol has been so low for so long that low vol has become its own bubble, and all bubbles burst.

"Do ya feel lucky, punk?" "Go ahead, buy more SVXY. Make my day."

We look forward to an educational experience this summer or fall for a large cohort of millennial "passive investors" and pension fund vol sellers. Every generation has a day to remember in markets - the day when things that can't happen, do.

You are a wise man LB,

ReplyBut there is a fractal argument within yours that I ll play first .. there are a lot of noobs seeing the risk of nuclear war and trading on it as though something might happen. They haven't had Nuclear war scenario to model but no doubt a lot of 12yr old quants will be looking for nikkei data 1945 to model and there will be cries of 'we are all at risk because trading rooms have fired all the old managers who have had experience of nuclear war.. blah blah' but I will fade the first 'there will be nuclear war noob panic trade' and wait for yet another run higher in risk before we have your [insert catalyst here] dump, which I am in full agreement over but far too confused to put on now.

RU and CN must be loving this. NK is their savage oit bull hey are doing nothing to rein in and enjoying the grief it is giving US.

China MIGHT help out if the US concede to something really useful, South China Sea like, but while US is sabre rattling in the region in general they will play innocent. As for RU, laughing all the way waiting to come in as global peacemaker..

You aren't a really major superpower until you have a rogue state to goad your adversaries with.

In fact I'm very much out of everything. I'm pretty clueless as what to do in the markets at all at the moment. Trading Trump vs Kim is like trading gamma around a very large binary expiry. Trading the Fed is like waiting for Godot. Trading EU equities is like chasing after a bus to Hell in the rain - you hop on late hoping to keep dry for a bit and get off before the terminal but you don't know if that's round the next bend. Trading yield is like pennies before steamrollers and trading FX is like trading a random walk. So everyone is busying themselves in analysing the micro thinking it will drive the macro but most of it averages out into white noise.

- Pol

"after the election the right people will be in place to make it happen"

ReplyI hope you are right Shawn. I work with an office full of Brazilians and I am not sure everyone is as optimistic as you are. But they do want change that is for sure. For now its brazilian samba.

Thanks for the AQ link though, Great overview.

Pol - I agree with all of that, NK is irrelevant. The true catalyst is the usual one - higher rates and firmer US data leading to Fedhead Hawkspeak. Very weak auction of US10s, and given the risk off background today, that is very bearish bonds.

ReplySitting here we are out of everything but have IWM and SVXY puts for a punt. If you are charting IWM, which has done a delightful roll over, we are seeing lower highs and lower lows and I will take that sort of signal over any other in thin August markets. Then of course there is the VIX, which seems to be returning from the dead. Let's see if that holds above 12 into the close and remember to watch for signs of discomfort as those vol ETFs do their rebalancing late in the day.

When spooz are rising we often saw a drop in the VIX in the last half hour and a "ramp" in the spooz that was often attributed to the "PPT" but might actually have been due to ETFs. Now that spooz are lower, it will be interesting to see if we see a late spike in the VIX along with that most reliable signature of significant corrections, the late dump into a new low.

going back to my favorite topic, spoo's I've been taking a look at some cash flow metrics (Bloomberg estimates) and still kinda scratching my head.

ReplyBoeing, a stock I dont really cover, did a massive gap up on earnings. Looks over extended for sure. But trading ~14x free cash flow. MSFT trading at 29x PE I never understood, but look at cash flow. 15x 2019 estimates. FB at 20x 2019 CF, always beating estimates, growing at >30%, trading at the same multiple as old fart Honeywell. Even Adobe, which I do think is expensive is trading only at 23x 2018 CF, vs 36x forward PE. Until these juggernauts start missing numbers I think this market is gonna grind higher. That said I am looking at Chinese data to slowdown sometime soon, but so far I dont see anything.

XRT, I like the trade IPA. Do you know of any other consumer ETFs? Id love to get a restaurant one but cant find any

Overheard at a large state pension fund:

ReplyCHAD: Hey, uh, Thad, VIX is spiking. Risk is in my ear, asking me what's the leverage we are running on our SVXY? 20?

THAD: Actually it is like 50. Last week was so quiet that I increased it - it was the morning after the pool party at Brad's.

BRAD: Bro, it's up to 100 now. I doubled down this morning when it dipped at the open. Vol always goes down, right?

RISK: You "doubled down"???

RUT at one month lows today, threatening to close below the June 1 close of 1396.06. Two months gains vaporized, 55 points erased over the last 15 days. Small craps leading the way..... let's see how this closes.

ReplyShawn, one thing I wrestle with is the Jan'19 paid leg. For sure, quite a lot of cuts are priced now, but I wonder whether they couldn't end up cutting even more. The market's pricing of the bottom of this rate cycle has just dropped and dropped. Interestingly, over the past six months, the 3Y and longer part of the curve has been comparatively stable (down -100bps-ish versus -400bps-ish move in the overnight), so I wonder whether I need be so worried about the 3Y point backing up much on fewer-than-expected cuts. Besides the momentum of that 1Y point of the curve which is scary to fade, the fundamentals could also arguably justify a lower bottom to this cycle. Inflation down at 2.7% and the economy in a 3-year recession, after all. India has the same 4% inflation target (with slightly wide band), the depo rate is at 6%, and yet their economy is doing well. Maybe not a valid comparison (beyond them both having the same target and trying to regain credibility and anchor expectations) since real rates in India have been historically lower than in Brazil (a function of higher savings rates?). It is interesting to see that the past month or so, the curve just hasn't steepened despite the falling 1Y point, but I'm not sure what's magical about this level a steepness. Is it just a level that just happens to hold until it gives way to steeper levels if the 1Y point keeps falling?

ReplyUBS pitching a 6-month 1.27 put on GBPUSD with EKO at 1.2050. Thought that was interesting. 1/3 the cost of vanilla and looking at a chart, I figure GBPUSD it's going to take full-on hard Brexit worries to go to a sub-1.20 regime, and that's likelier beyond a 6-month horizon. Until then, the squeeze on consumers and rolling-over real estate market will have the BoE on-hold and sterling drifting lower, IMO. The whole rate hike talk was just an attempt to support the GBP and consumer real incomes, but they probably realize they'll be pulling a Trichet by hiking now.

@abee, the only pure restaurant etf I see is MENU (link below). I would not touch it with a ten foot pole. AUM just $1.6M, total shares only 100K, very thin volume, and no options. The other one, BITE, closed down, never gained any interest. Restaurants are in big trouble, imho.

Replyhttp://www.uscfinvestments.com/menu

@Pol and @LB, agree, we don't really need a nuclear war to have a big selloff. We just need a strong hint of one to scare the $hit out of everyone and create the mother of all margin calls in a very illiquid time. SVXY is a vehicle too hard to control on the downside. Will completely unravel, imho. Looking for a trip down to $50. It really does not matter what gets it going, but once it does, look out below.

Now here's the thing.

ReplySmall spike up in spx clise.. like 9pts.. and VIX collapses back.

But I m thinking that market is still not ying yang long of stocks yet with cash still to chase it. What folks do have in it they cant afford to hedge as it reduces further their performance vs cash benchmark. So fewer natural buyers of puts. Tgey can rationalise not buying cover as wanting a dip to buy more on. On top of that those who need a monthly return sell options for premium to lock in some cashflow.

So.. this could go further up in the cash. You could even see vol go up on a massive up move in underlying.. you what? Yes.. peeps may even buy upside strikes. Don t think that just because VIX has always correlated to downdraughts that it always has to. Now THAT would be an hilarious correlation crap out event. Vol screams higher on mahooosuve underlying rally stuffing the vol shorts too.

I am of course huuuuugely sceptical of said noobs we have mentioned thinking VIX ETFs are nice vanilla products you just buy or sell cos it s a single price innit.. open the lid and see that your nice simple vol trade is a mess of cost and risk worms.

Looks like I made a newbie's mistake re DI futures. Somehow thought they were forward, not spot rates. So take back my critique of the '19/'21 DI trade. Looks good to me.

Reply