Under-the-hood price action suggests that there are lot of flamingos being hunted at the moment. The decline of the dollar is the most obvious, not just in currency terms but also against a range of commodities. Dollar-led deflation has been a key theme of financial price action over the last year (even if it didn't make it into enough investment portfolios early enough); given the apparent climb-down from the Fed, it's now being unwound, if only temporarily.

Far from fulfilling Kuroda's hope of generating yen weakness and unbridled Nikkei joy, NIRP has thus far rampaged through Tokyo markets like Godzilla after a detour at the sake factory. Although not technically a head and shoulders, the USD/JPY formation below is nevertheless ominous, particularly in light of last week's BOJ whiff. A break below the neckline and it's goodnight, Irene from a technical perspective.

Of course, dollar weakness cuts both ways, as evidenced by the recent renaissance in gold, copper, iron ore, and that Alcoa chart posted yesterday. Miners have fared particularly well, no doubt because of a combination of rallies in the underlying metals and short covering. Despite a few hairy moments, Macro Man remains long the GDX he bought a few weeks ago. It looks to have broken out, though he wants to see the $17 level go before he considers adding any more.

The distribution of risks around today's payroll number presents an interesting question. On the one hand, almost all tightening has been priced out for the Fed this year, despite their stated desire to be able to hike several times. Moreover, the walloping that the dollar and yields have received recently would suggest a significant flush, thereby leaving ample room for both to go higher on signs of strength.

The distribution of risks around today's payroll number presents an interesting question. On the one hand, almost all tightening has been priced out for the Fed this year, despite their stated desire to be able to hike several times. Moreover, the walloping that the dollar and yields have received recently would suggest a significant flush, thereby leaving ample room for both to go higher on signs of strength.

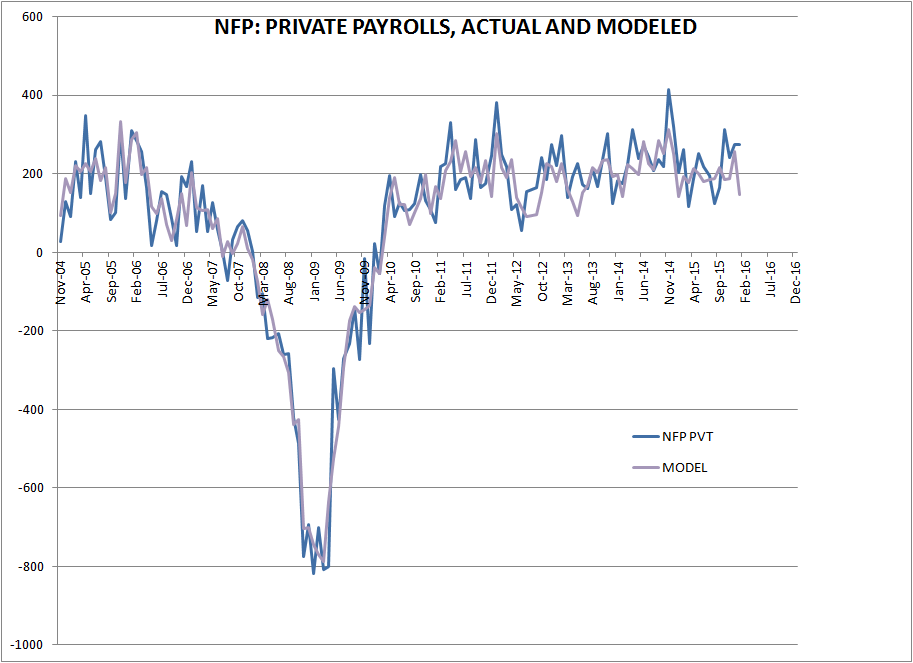

That being said, generally speaking the data has been very weak- substantially weaker than Macro Man was expecting, and clearly not just down to the mechanistic impact of a simple quarter point rate raise. A very weak number would amplify these concerns, and clearly do nothing to dissuade either fixed income perma-bulls or equity bears from pressing their bets. Moreover, given how close the dollar complex is to some key technical levels, further weakness could prompt a reassessment from more strategic players. All in, Macro Man comes down on the side of a weak figure prompting the more violent reaction, loathe as he is to simply extrapolate the last few days' price action into the future.

Perhaps he's also coloured by the output from his model, which has produced its weakest forecast since January of last year, expecting tepid payroll growth of just 145k. That would almost certainly put paid to March as a rate hike proposition, though the market had already come to that conclusion over the last few weeks. However, another few months of weak data could well start a drumbeat of recession talk, so any figure that might expedite that process needs to be taken seriously. While Macro Man doesn't like to bet on the outcome of a payroll number- too much noise, not enough signal- it's clearly prudent to anticipate where the market is most vulnerable. Prepare for the worst, and you'll rarely be disappointed....

Far from fulfilling Kuroda's hope of generating yen weakness and unbridled Nikkei joy, NIRP has thus far rampaged through Tokyo markets like Godzilla after a detour at the sake factory. Although not technically a head and shoulders, the USD/JPY formation below is nevertheless ominous, particularly in light of last week's BOJ whiff. A break below the neckline and it's goodnight, Irene from a technical perspective.

Of course, dollar weakness cuts both ways, as evidenced by the recent renaissance in gold, copper, iron ore, and that Alcoa chart posted yesterday. Miners have fared particularly well, no doubt because of a combination of rallies in the underlying metals and short covering. Despite a few hairy moments, Macro Man remains long the GDX he bought a few weeks ago. It looks to have broken out, though he wants to see the $17 level go before he considers adding any more.

That being said, generally speaking the data has been very weak- substantially weaker than Macro Man was expecting, and clearly not just down to the mechanistic impact of a simple quarter point rate raise. A very weak number would amplify these concerns, and clearly do nothing to dissuade either fixed income perma-bulls or equity bears from pressing their bets. Moreover, given how close the dollar complex is to some key technical levels, further weakness could prompt a reassessment from more strategic players. All in, Macro Man comes down on the side of a weak figure prompting the more violent reaction, loathe as he is to simply extrapolate the last few days' price action into the future.

Perhaps he's also coloured by the output from his model, which has produced its weakest forecast since January of last year, expecting tepid payroll growth of just 145k. That would almost certainly put paid to March as a rate hike proposition, though the market had already come to that conclusion over the last few weeks. However, another few months of weak data could well start a drumbeat of recession talk, so any figure that might expedite that process needs to be taken seriously. While Macro Man doesn't like to bet on the outcome of a payroll number- too much noise, not enough signal- it's clearly prudent to anticipate where the market is most vulnerable. Prepare for the worst, and you'll rarely be disappointed....

75 comments

Click here for commentsWondering if those masters of the universe were smart enough to short CNY against something other than USD? Probably had a side of short CL to boot.

ReplyA butterfly flaps its wings in Tokyo.

Now what I can't figure out is whether that was the low in commods or they are just having one final face ripper..they couldn't possibly rally if DM takes a dump could they?

Am I recalling correctly the last few yrs started out reasonably strong on the jobs front - think it had to do w seasonals. Guessing we get a lower number but still high enough to beat expectations which are v low.

Long term thou big believer in reverse wealth effect having detrimental impacts to consumer confidence when your economy is heavily service oriented. You see a manufacturer has to make his plans at least what, 6mos in adv? Consumers can change their purchase habits tomorrow if they wanted. So yeah the drums you hear in the distance are growing much louder. ECRI will want to make sure after last time. But unless vol subsides soon its probably only a matter of time.

given last months strong print of 300k, expect some giveback this month - historically 300k prints have been followed by a swing to the low end. that said, trend is good in us payrolls-lagging indicator or not.

Replygiven the hammering eu equities are receiving on the back of euro pop this sets up a interesting trade going into ecb march...

everybody eying dax lows for a flush lower but this index is notorious - i am looking for a flush down as a false break and then a rip higher...

basically expect a dump in risk followed by a quick pop.

interesting to see bnp doing ok on the divi increase...very beaten up name along with all the other banks but expect that on to outperform on any risk on.

lots of desiring under the surface as popular long shorts get taken behind the woodshed

LinkedIn shares -28% after hours

Replycongratulations NYSE you have created a casino

+gdx / -qqq (in odd lot size) - looks about as peachy as a pair trade can be

ReplyLooks like the dollar short/long/asscovering is almost over. It is certainly looking a bit over-done. But then I thought it was overdone the other way until a week ago.

ReplyI am thinking these are nice levels to short EUR.USD and AUD.USD from.

I think expectations for this NFP are low, low low. And we have gone from pricing in 2 rate hikes this year a few weeks ago to less than half of one now. So those are not bad odds to take the other side of.

In any case, employment is a lagging indicator anyway so I suspect once it is out of the way dollar sellers will emerge from the woodwork again. Because if this is the beginning of a recession in the U.S, then commodity currencies will be easing and Mr. Aghi may have to bring out the Bazooka next month. And this time he will be more motivated after the whipping he got after the last ECB meeting and the BOJ effort recently. Nothing will suffice except an increase in QE! and that should get the dollar index moving again.

"NIRP has thus far rampaged through Tokyo markets like Godzilla after a detour at the sake factory"

Replypriceless!

GDX really saved my neck from this weeks episode of USD carnage.

ReplyAgree with Draghi needing to bring the bazooka, but it needs to really be a big one bc

a) he kind of explicitly promised, or at least that probably was the general interpretation

b) the stakes in the CB Wars are getting higher and the competition is getting rougher

c) general diminished and long term time decaying effect of forward guidance and the market is becoming a tougher audience by requiring larger expectation exceeding margins than before. Shortly diminishing CB credibility

If US data (i.e core durable, retail sales) gets weaker, then it will really need to be a mega sized bazooka to counter previous points and brake flows out of US at the same time. In that case it's a reasonable chance that EMs, miners and oil actually continue to rip. I still hoped oil would go to the 20-25 value range. But big oil and shale industry have been recently swinging previous existing and future capacity capex with sledge hammers and offshore drillers are priced like they are going bust (some of them will and have already gone). Which makes me wonder as the news tide on the supply side continues getting negative by the day.

EZ M2 bounced from 2% in April 2014 and has since gone up and stayed above 5%. That continues to be a good sign for now and augmented by any potential commodity/EM bounce might actually result in data improving again so it might actually not be all doom and gloom.

Nico, they are hammering high growth expectations who fail to over deliver. ..tableau, also down 25% or so. Watch tsla and Amazon as they are good poster boys.

ReplyRotation, rotation.

But I still want to see industrials and banks make a sustained bounce.

A Draghi bazooka. To take out what though?

ReplyFurther neg rates? Kills already struggling banks. Banks have to deal with rates down, regulation up, NPL's in periphery, overheated property markets in certain locations, exposure to oil & HY and, general poor performance in volatile markets. Look at the European bank performance thus far.

Buy more bonds? They've already distorted the core periphery and long end of the curves. Hampering insurance companies and penison funds.

What does/can the ECB buy within Europe apart from equities and outright assets?

They have cornered the market and are trapped. I'm sure they will come up with something to distort things further but, it will all end in tears.

Could they directly support deficit spending on infrastructure projects?

I know Anon but in the short term (March) they have to deliver it regardless of bank erosion/NPLs/oversaturating the bnond market and other stuff or the toys get thrown out of the pram very quickly, again...

Replyisn't markets reaction to last CB antics (Abe) not clear enough?

Replythe CBs have ran out of both ammo and credibility

people the 2009-2015 period is over, get over it and go back to pre-2009 thinking. It will now require ANALYSIS i.e. an intellectual effort to make money trading - for anyone who did not make enough to retire buying dips throughout the period aforementioned.

nah forget analsys, look, I can't even spell it. Stick to the basics:

ReplyQE = very good juice

NIRP = not the real deal

ECB is due for a QE expansion and if they do, I would think it may well send eur.usd back to 1.05 and below. Anyway, short eur.usd at 1.12 today is better value than 1.08 last week. It looks rather enticing to me.

Nico - bit unfair to the Teppers of the world to say closing your eyes and buying didn't require analysis no? Certainly there are plenty of people on the other side who whipped themselves into a frenzy reading zero hedge and hussman, thoughtlessly sold rallies from 1400 to 1900, and then, parted from their capital, sullenly retired to the sidelines relegating to booing breakouts. Their time may now have come, but my point is that too smart for a certain market condition is too smart by far.

ReplyAs for the negative rates stuff and its impact on financials - look, everything depends on whether the end result is bull steepening or bull flattening - you would think given the reaction in banking stocks that 5/30 must have moved in 20 bps or something, when in reality its unchanged to slightly out - makes me wonder if the sellers of banking stocks are 1) assuming DB contagion, or 2) watching too many sanders-clinton debates.

In the end, the root meme that has set off this train is dollar strength - the commodity bear market is now approaching its 2nd anniversary - depending on your perspective it could be maturing and turning, or preparing for one final awesome hyper nova. In the end, if the Fed were determined that everything could be set 'right' by weakening the dollar, with the crowded positioning that exists, it can be achieved without rate policy being a factor. Like MM said, FX (unlike equities) is one area where CB's can and do intervene, and weakening one's currency is much, much easier than strengthening it.

I would watch for some coordinated dollar policy statement from the G 20 later this month - I don't think the market is prepared for it.

@ washed, given that just about every other member of the g20 wants a weaker currency (if not the weaker commods that go with that), I would say there are two hopes of G20 $ statement in the pipeline: Bob Hope and no hope.

Replyhttp://www.marketwatch.com/story/obama-proposing-10-a-barrel-oil-tax-to-pay-for-clean-transportation-2016-02-04

Reply.....Productivity of only .3% over the last year, you say, BinT? Well, there are lots of things that when analyzed go into decreasing productivity...

...Today's economic animal is such an amalgam of stimulus and increased costs...it must either look like a tiger or a leopard...

MM - they wanted weaker commodities because they believed that was good - they are now realizing that is bad because of the 'pernicious deflationary forces' it unleashes - they are slow and lazy but not stupid - eventually if a strong dollar starts taking a dump on everyone's lawn through financial repricing they will have to coordinate or at-least appear to - if you are saying they are not at that point yet, well, okay - we will see.

Replyhttp://www.cnbc.com/2016/02/04/world-food-prices-tumble-near-7-year-low.html

Reply"World food prices fell to almost a seven-year low at the start of the year on the back of sharp declines in commodities, particularly sugar, according to the latest data from the United Nations (UN).

The Food Price Index, published by the UN's Food and Agriculture Organization (FAO), averaged 150.4 points in January, down 16 percent from a year earlier and registering its lowest level since April 2009"

...Well, how do you gin up inflation with such deflationary trends? Ah, yes, not paying attention class...after seeing the ideas with petroleum, how about a 10 dollar a bushel tax on avocados? To this observer, I see plenty of pressure for tariffs in 2016...not just mass devaluation, either...

Washed...you and I see the world pretty much alike I think...However, it doesn't mean the world pays much attention to us...

Reply:)

anyone else remember when the market used to get excite about 1m ? perspective ?

ReplyThere's nothing pernicious about the disinflation we're experiencing now. It's benign and natural. Consumers are happy as purchasing power rises. Some of the deflationary forces are transitionary (oversupply of commodities and goods, dearth of investments) and some are not (demographic abyss).

ReplyWe're transitioning towards HEAVILY service based economies where manufacturing will have diminishing role. Investments in services will increase heavily once the markets run out of inexpensive labour AND services become more specialized requiring more skills (aka human capital). THEN we'll see inflation.

People aware of approaching death aren't interested in buying more stuff. They want experiences. No CB can change that. They shouldn't try to.

anon - ur 'transition' could be rather bumpy for the stock market is all - and you are right, thats fine as long as those people aware of approaching death weren't counting on their assets to y'know, pay for those fun experiences.

ReplyNice dollar bounce on bad news there. I notice though that USD.CNH has not participated much in this post NFP rally, so I might pick up some in anticipation of a post lunar new year hiccup.

ReplyAnonymous Anonymous said...

ReplyThere's nothing pernicious about the disinflation we're experiencing now

...Many would agree. BUT the problem is that the Fed doesn't. And the whole carnival ride is based on increasing credit. Is disinflation or deflation a road block to increasing credit levels...? Hmmmm......

Risk on...risk off...

Sunrise...sunset...quickly go the days...

And the winner is...

ReplyNFP 151k

Unemployment 4.9%

@ Booger, it wasn't bad news as such. Earnings and workweek higher than expected, unemployment lower than expected, HH survey added 615k jobs. The only bad bit was the headline!

ReplyMuch Ado About Nothing.

Reply"Friday's jobs report likely leaves Federal Reserve officials in a " watchful waiting" mode as they consider whether to lift short-term interest rates at their next policy meeting in March."

ReplyThat's what oncologists say is the most appropriate response for most men with prostate cancer...."watchful waiting".

Hey - MM had 145k and you had 190k - thats not nothing, thats a tush-whupping in the little quant-off you were trying to start yesterday.

ReplyI need an urn with many red and black balls...

Oh tell me about it. MM more bearish than LB... still, we didn't have any appendages under the guillotine today. Mr Market seems indecisive today and when he is in this kind of mood I don't like to give him any of my carefully squirreled cash.

ReplyGo on, Mr Market, it's your move. But if we had to make a guess, we'd say the USD would creep higher early next week to retrace at least some portion of that hard move down. Not a bad week for us, all things considered, as EMs recovered a bit. Likely we will raise a bit more cash later today and go into next week even lighter in the risk department. Oil and the rest of the commodity complex still trades heavy, and until that changes there is still substantial risk in EM equities. No time for heroes. Don't want to get an ice pick. Whatever happened to the heroes?

No More Heroes

Does anyone have a firm view long CL?

ReplyTrying to piece together the bull thesis

Jesus H Soros Macroman, well done!!!!! Crackling forecast!

ReplyIs there a way to tie your NFP into UE and maybe even Wages? Would be quite the insight to have the trio. I seem to remember seeing some research that suggested that the US needs only 70k jobs to keep up with the labor force, so maybe it's not a hard calculation.

I wonder if LNKD shareholders were prepared for the worst this morning? Down a cool 40%? Does that qualify as "gapping and crapping"? That is like biotech investing, where the FDA announces something on Ponzi Drugs R Us and it gets decapitated.

ReplyA lot of those silly retail sausages are wondering why their "trailing stops" didn't trigger at 10% down, but did at 35% after the market opened.. oh dear. The pain that Mr Market can deliver to the unwary...

"The pain that Mr Market can deliver to the unwary..."

ReplyAbsolutely LB ... a lot of pain being dished out here, despite the market "bobbing up and down". Pick your horses with caution!

Yeah. If we look at today's action we see Spoos down with Usdjpy slightly up. That's a departure from one of the most popular recent market correlations. On the other hand, we see EMs down with DX up, which is a more traditional macro trading pair, and AUDUSD is getting (inverse) hammered on a big reversal candle.

ReplyFor next week, we see renewed upside in USDJPY to the 119 or even 120 area. So we are not inclined to take much risk at all in commodities, energy, EMs, or FX. Still, this does not seem to be an especially wise time to short the Spoos, or to get longer for that matter. We will take more Hammock Time, please. It's possible that to be able to look back on a return of 0.0% for February will be quite pleasurable come March 1st. Have a great weekend, all.

anon 4:26 - Re: CL I see it going up a bit, then down, then up a bit, then down... does that help any?

ReplyWages follow inflation. While the headline unemployment was lower than estimates the 2.5% rise in wages (last month revised to 2.7%!) is a real honest sign that inflation (as it matters to the markets) is on the rise. Does this mean the Fed will raise again in 2016? It certainly increases the odds a bit. Either way I think investors really should consider inflation effects on portfolio decisions because it's heartier than most believe and only likely headed further up.

ReplyHey Lefty, you wanna go down to the cigar club after work and join in with the great minds of Wall street and discuss who fellow hedge fund traders we can tag with this growth story. Asshole of US exceptionalism, please meet Dumbo.

Replyhttps://www.youtube.com/watch?v=YgGvd1UPZ88

Is the oil market trading based on the $ rather than supply issues in the short term?

Replyi think markets have made a momentum low last month and while we get a price low restest there are enough divergences at play for me to nibble at some upside calls...yes premiums high but if we get a false break kind of play the move up is going to be fierce...looking at movement beneath the indices, xlf holding ok and breath not that bad given a 2% day...looks like liquidation of well loved FANGS( i played these short year end along with xly now out- though europe v us has been pants )good to see gdx up with usd but needs to clear 17- will add more on a break

Replyi think good reminder to punters that yes we can sell of a bit without a recession..still think 1700-1750 doable is spoos but economy not tanking yet doing what it has for the last 4 years 2 percent give or take

finally given BOJ clusterfuck what for a upside surprise to ECB from draghi and lookt o reload ( add in my case) to eu longs

interesting that post 2008 people think every sell off is end of world and every rally is to new highs!!there are other paths you know...

GMO's quarterly updates and Grantham's comments in particular are always worth a read:

Replyhttps://www.gmo.com/docs/default-source/public-commentary/gmo-quarterly-letter.pdf?sfvrsn=26

In March of 2000, MicroStrategy announced some earnings restatements. For some people, that event was the prick that popped the dotcom bubble.

Reply"Shares of electronic commerce software maker MicroStrategy Inc. plummeted Monday - losing more than half their value in a plunge of $140 - after the company said it will restate operating results for the past two years to comply with new federal accounting guidelines on reporting revenue.

The little-known Vienna, Va.-based company, which has seen its stock shoot up thousands of percent over the past year, said it will report a 1999 loss instead of a profit, and also will revise 1998 results downward after changing the way it reports software revenue from service contracts." <a href="http://money.cnn.com/2000/03/20/companies/microstrategy/>CNNMoney: Microstrategy Plummets</a>

LNKD's 43.6% fall today, although catastrophic, is the result of reduced guidance. However awkward their product mix and murky their forecast, the company is still looking at billions in 2016 revenue. I have no direct position in LNKD.

As before, I look to central banks in China/Japan/Euro/US to come back in with their calming drops of money.

LNKD will be at 0 before the next financial year. There is no value there.

Reply@marshall jung

ReplyI agree with your interpretation of how the Fed will interpret the rise in wages. I noted, and assumed everyone else already noted, that the kansas city and now the cleveland bank chiefs both sounded like tightening was in the cards.

This idea of global coordination seems to me like herding cats. The US is probably still doing better than 90% of the western world, but now that Russia, China, middle east wars and a European refugee crisis are stirred into the cake...well, I still think there's a good chance we are in a US recession in 2016, and I am still planning to re-short the market. However I am patient. Not like Leftback, who is still in a hammock and may get his junk frozen...I am comfortably laid back in my bear cave...

LOL, that's funny, B in T. Staying patient here, also.

ReplyNot much difference between a bear cave and a hammock that is rigged up inside in NYC.

Waiting to see where Mr Market lurches next before leaving the safe haven of cash = Hammock Time.

"Interesting that post 2008 people think every sell off is end of world and every rally is to new highs!!there are other paths you know..."

ReplyEveryone should post-it this next to their trading screens. This sentiment continues to hugely distort any market discussion. The good thing is that quiet and disciplined work by the stock/sector picker can still do very well.

MM, you are quite correct, superficially I played off just the headline employment number and didn't bother to look under the hood. In any case the revisions and error inherent in the point estimate make it a not very meaningful look in the rear view.

ReplyUSD.JPY: I am tempted to go long UJ from here. Yes the BOJ failed last time but they can still increase NIRP in increments from here to -1% and zap yen bulls a few more times. After that they face the question o whether to use the last 2 bullets in their gun, expand QE or really go nuclear QE.

EUR.USD: I can't believe how little interest there is in shorting this now with Mr. Aghi speaking in March. Where are the people who were keen on shorting it at 1.08. Probably stopped out one guesses, which leaves rooms for it to go down again. The scene is set for a very interesting meeting in March, despite disquiet from the letdown last meeting, I suspect FX traders will embrace his call again, particularly if it involves a serious increase in QE, because that is like a siren call to sell euro and make free money. Anyway, count me in on that one and I've booked a seat at a pre-NFP price and the rest of the position closer to the day.

AUD.USD: Finally some disappointing numbers after the freakish run of good data from November to January. This time in the form of weak retail sales, more follow through with weak unemployment numbers could send this baby back to the 60's. I really like the setup here for a short and took out most of my position pre-NFP.

http://www.zerohedge.com/news/2016-02-06/wounded-deutsche-bank-lashes-out-central-bankers-stop-easing-you-are-crushing-us

ReplyA good thrashing of biotech and Internet names would be a welcome reset for valuation based investors ( are there any left?). It's always like that at the top of the cycle, the best fundi sectors are the last to turn ( oil and commodities in 08 ) and the first to bounce usually was well. But that would only be after a huge sell off. Over the past few days we have seen value and commodities hold the line much better than tech, so it could easily be the start of a healthy rotation. Or the beginning of the fun to the downside. You will only know in hindsight.

ReplyMessage out of fx, aside from yen which is worrying but a little too much focus imo, is pretty positive. And oil is looking more positive as well. Now if only Europe would catch a bid.

abee - agree that this may be the year of the value stock, but its hard to see oil do the V-shaped thing it did in 2008-09 on the backs of the gargantuan china stimulus. I think majors will be OK in the long run and are maybe priced for 8-10% CAGR conservatively but thats a 12 year play, and I doubt the final lows are in.

ReplyI think US focused REITS and domestic, US consumer focused value stocks could handily outperform (and no, AMZN is not yet an example of the latter, not for another 60% selloff). Indian equities are also finally getting to nibbleville - we will see.

Headlines or Monday...brace yourself

Replyhttp://imgur.com/JRN5Yx1

not digging the new snazzy website look. i like the old keep in simple stupid look...

ReplyYeah well, time marches on, and the old one had problems displaying charts etc, particularly on mobile devices. There is always an adjustment process, particularly when it's a caveman like me doing all the work....

Replyhttp://etfdailynews.com/2016/02/05/four-days-after-predicting-oil-will-double-t-boone-pickens-sells-all-oil-holdings/

Reply"Pickens has sold all his oil holdings and is waiting for the best moment to get back in, he said Thursday in an interview on “Bloomberg Go.” With prices low, mid-size U.S. oil companies such as Pioneer Natural Resources Co., Anadarko Petroleum Corp. and Apache Corp. are acquisition targets for larger firms like Exxon Mobil Corp., he said."

...I think he had to raise some money to pay to get his hand bandaged.....

@MM, I like the new look, and appreciate your continuous efforts!

ReplyI thought for a moment I logged onto the wrong site when the header had a "Kinky" And "Car" Section...

Replylots of rotation at the single stock level over the past few days. Hard to say if its a good or bad thing, as defensive and high growth both sold off hard, however commodities and oversold industrial held in there, though i would hardly say the action for those groups is really positive yet...

ReplyLots of theories on what caused the rotation and implications for the market at large, but I will put 2 out there for agent mulder and scully to discuss.

1) The selloff in momentum names (high growth like FB (who killed) and AMZN (who missed) was caused by some large hands who finally decided to sell what has been working as they go outright short (Druckenmiller when last asked what he was long, said long some momo names )

2) The sell off of momentum, while value stock and commodities especially have held, is a positive divergence in the market and was mainly due to quants jumping over themselves.

I'm glad to see tech joining the rubble, I've been waiting to see some value there. LNKD trading for 2x Expected sales currently. looks like they have some internal problems but still growing > 30%. Using a reasonable software earnings margins in a few years, valuation is no longer demanding. No position, but curious to hear others.

MacroMan,

Replyare you using CSS for the layout? Honestly, I find the new one less homely and a bit sterile. Call me old fashioned.

So bearish on tech at the moment

ReplyGoogle is at a 5.3 EV / sales multiple. I get the growth thing, but 5x on 17% growth?

Amazon $2 billion operating profit on 225 billion EV. At least its sales ratio looks respectiable, though online retail has gotta be one of the lowest marign businesses around.

IPO market shut, newcomer tech investors like Fidelity already writing down their shoddy top of the market investments.. who would bid these up to new highs right now?

Eddie said...

ReplyMacroMan,

are you using CSS for the layout? Honestly, I find the new one less homely and a bit sterile. Call me old fashioned.

Eddie, you mean less homey, don't you? Homely is what the women say when they see Leftback.....

Adamatic, I don't have my bloomy in front of me but isn't googl expecting $40 EPS next year. 20x, for a 20% grower isn't so bad. Maybe a tad expensive when u are that big. But it's seen as blue chip now.

ReplyAmzn, was all about a pending increase in margins as aws, starts slowing down capex..but it's valuation always is demanding.

Fb at 7x sales but it's a juggernaut and already very profitable, at least ebitda...

But agree new tech ipo is done. Square is poster boy...under its last vc capital raise level .. Keep selling Mr market. I would much rather buy tech on the cheap than Banks.

China forex reserve was down by $99.5 billion for 01/2016.

Replyhttp://www.wsj.com/articles/chinas-forex-reserves-plunge-to-more-than-three-year-low-1454816583

If I remember correctly, GS predicted a $185 billion drop and someone mentioned a $200 billion drop. If the data is accurate, then it must mean that PBOC had a really successful battle in last month with those HFs. It sounds to me the most reasonable reason is that a large number of speculators shorting RMB were forced to cover their positions which really reduced the magnitude of decrease in forex reserve.

Does it imply a more stable Asia markets at least for a few weeks? I do not know.

That will be taken as quite a positive, given the numbers floating about. Of course, for Chinese markets it's sort of irrelevant, given they're closed for New year this week and by next week the market's attention will likely be diverted by something else....

ReplyNews wrap-up:

ReplyChina's running out of FX reserves, and we're all gonna die.

European banks are about to blow-up and we're all gonna die.

I'm long equities Monday.

@MM,

ReplyI am thinking about AUD NZD even CAD and all those EM assets/currencies/commodities. I expect a mid-term secondary effect.

MM - I actually think 99 B vs the armageddonish nos. thrown about is a huge surprise, and you are right, given sentiment it probably won't matter to spoos.

ReplyCapital controls in China are a way higher probability than an ongoing skirmish between PBoC and fx trading illuminati that resolves in a few quarters, so the blokes betting on a massive de-val may want to slow down on the drooling - they are also quite likely to work because y'know if you skirt the controls in China you don't simply have a conversation with the risk manager.

The right way to look at Chinese troubles, is to to imagine what would have have happened if the 2008 financial crisis happened in the absence of MtM accounting - I can guarantee Burry and Paulson would still be waiting for a payday while driving around in shabby volkswagens and asked to report to the local police station every day.

The ability of the western world, especially the investing community, to pretend that the rest of the world works exactly like theirs, never ceases to astound me.

Here is the ft article. http://ftalphaville.ft.com/2015/01/29/2104532/china-vs-the-so-called-art-industry/

ReplyWeird how did my first comment get deleted ? Anyway again

ReplyWashedup, a relative of mine does business in china so they have dealt with the capital controls. In a convo late last year they said that the going rate was 3% To get your money out and it wasnt hard at all. There are many ways to get money out (There was an ft alphaville article on this) Which are too many to plug, not to mention the monied class are all doing it too so its an open secret. While xi has centralised power much more now it still true that china is a huge country and beijing cant keep track of everything that happens in the provinces.

Bruce in Tennesse:

ReplyYou are right. Another sign that I'm getting old.

Thanks anon 3:59 - of course there is a black market the way it exists in every middle income country, but it amounts to a slow leakage and not a stampede of money - the majority of the reserve drawdown so far has been chinese corporates swapping dollar debt for yuan debt in anticipation of rate rises and plain valuation adjustments.

ReplyIn the end, I think where the world is heading is a slow motion lurch to the pre-bretton woods, pre globalization, domestic economy (as opposed to trade) driven growth - think of it as capital going home everywhere - implications? Productivity keeps hooking down, inflation comes from wages and not commodities, and growth is limited to pockets of tech and bio-tech. There is not a single high growth story in that new world except India, and they will surely find a way to f@3k it up, because they always do. The ceiling on inflation in that new world is higher than the consensus thinks right now, but we may be 8-10 years away from that particular chicken coming home to roost.

Done with the armchair theorizing - go Broncos - their quarterback is washed-up like me, so I have sympathies…..

The right way to look at Chinese troubles, is to to imagine what would have have happened if the 2008 financial crisis happened in the absence of MtM accounting

ReplyIn March 2009 Mark-to-Market valuation was substituted by Mark-to-Myth resp. Mark-to-Model valuation and a ton of assets that used to be FVtPL were reclassified into L&R. I guess this is reasonably close to no MtM.

Madoff whistleblower Harry Markopolos

Reply"I'm looking at about 3 funds right now that are also Ponzi Schemes. 1 is bigger than Madoff."

http://time.com/money/4209599/bernie-madoff-new-ponzi-schemes/

We are in for quite a ride...

ReplyBond fund leverage setting off alarms. Just now?

BlackRock’s Fixed Income Global Opportunities fund had an average leverage of 746 per cent over 2014.

Pimco’s Global Bond ex-US fund and Goldman Sachs’s Global Strategic Income Bond Portfolio had leverage of 468 per cent and 674 per cent respectively over the same period.

http://www.ft.com/intl/cms/s/0/f9555ac0-bea9-11e5-846f-79b0e3d20eaf.html#axzz3zVATMu2P

First WSJ and now Forbes on EURO banks...

ReplyWSJ

http://imgur.com/JRN5Yx1

Forbes

http://www.forbes.com/sites/petertchir/2016/02/06/what-is-happening-to-european-banks/#32cf3e1f5b2f

Charles Mackay's "Extraordinary Popular Delusions of Crowds" just as relevant to hypnotics of QE as it was to all other madness in his book.

Replyabee crombie just checked - GOOG next year consensus EPS is indeed 40 (seems high), but ttm were 23 and GS has them at 28 (seems low).

ReplyAmazon AWS is at a $10 billion revenue run rate with 30% margin. 1 billion of that is apparently from Apple.

It's very nature (high initial capex on databases) will force them eventually to compete on operating costs rather than total economic cost. Compare this with how much the AWS story shifted their market cap.

Having said that I have some tesla shares so am guilty of optimism myself