Today (or yesterday, by the time most of you read this) is the feast day of Our Lady of Guadalupe. It marks the day in 1531 when the apparition of the Virgin Mary appeared before Saint Juan Diego on a mountain outside of what became Mexico City, and led to the conversation of much of the indigenous population to the Catholic faith.

This is a foundational event in Mexican cultural history, which is why I love this picture--dozens of young people (and a scrawny stray dog) carrying her image outside of the basilica. This parade--which is replicated throughout the country on this day--is a labor of love, honor, and devotion with just a touch of patriotism. If you’ve never been in Mexico on December 12th, check it out. It’s Christmas and Independence Day rolled into one. You’ll never forget it.

In honor of this great holiday, let’s take a look the upcoming rate-setting decision by Banxico on Thursday. Unlike the FOMC, which hasn’t surprised anyone with a rate change decision in going on a decade, this one is a toss up. The market is pricing a roughly 70% probability of a 25bp hike after higher than expected inflation prints in October and November and a coincident depreciation of the peso.

I think they are going to stay put at 7%. Here’s why.

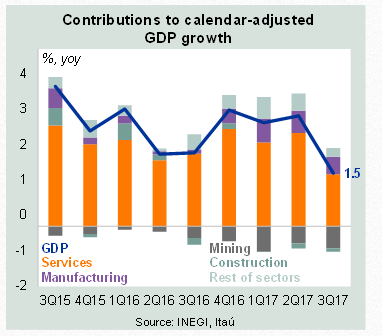

1) Growth is stagnant, at best. While there is some drag from the earthquakes in the Q3 numbers, the economy isn’t hitting it out of the park by any stretch of the imagination.

1) Growth is stagnant, at best. While there is some drag from the earthquakes in the Q3 numbers, the economy isn’t hitting it out of the park by any stretch of the imagination.

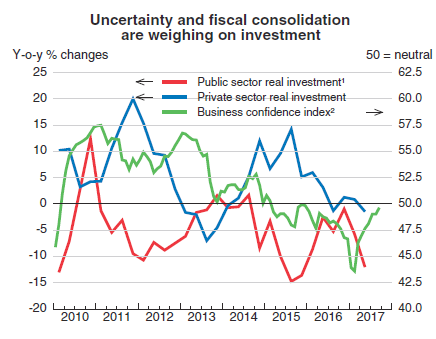

One of the main reasons for that is the ongoing tightening of fiscal policy by the government and poor business confidence, which has led to a decrease in private investment as well.

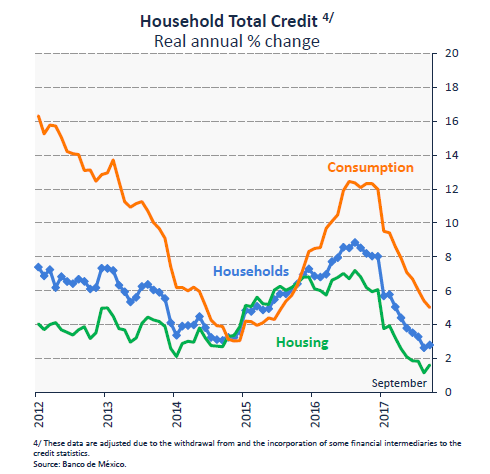

The combination of the above investment drawdown, Trump-phobia and Banxico’s 400bp hiking cycle has hit the consumer hard too--household and housing credit growth rates are falling significantly.

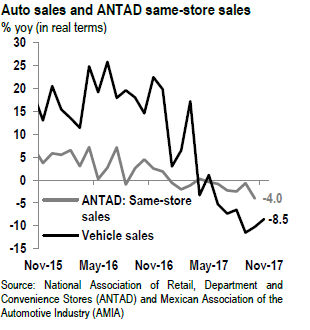

Which has also caused a slowdown in retail sales, and hit the bottom line for retailers.

That equity rally you’ve been hearing so much about? No habla español.

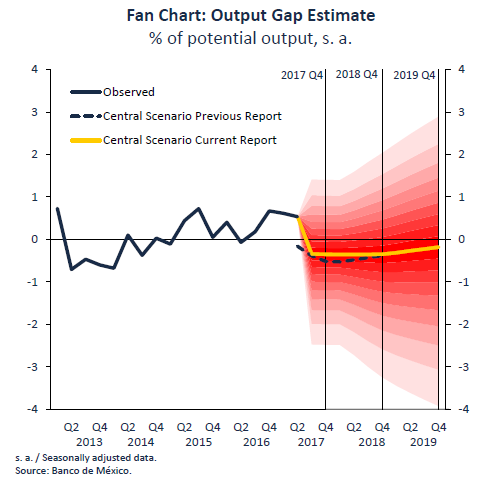

Taken together, this negative view on growth has led the central bank to forecast a slowdown leading to a persistent negative output gap well into the future.

2) Inflation: those calling for a hike rightly point out that inflation has been surprising on the upside--this camp claims Banxico must act to stabilize inflation expectations before they get out of hand. This argument ignores the underlying drivers of inflation that 1) have been impacted by one-off effects and price changes, and 2) with the exception of propane prices, have leveled off since the price shocks early this year.

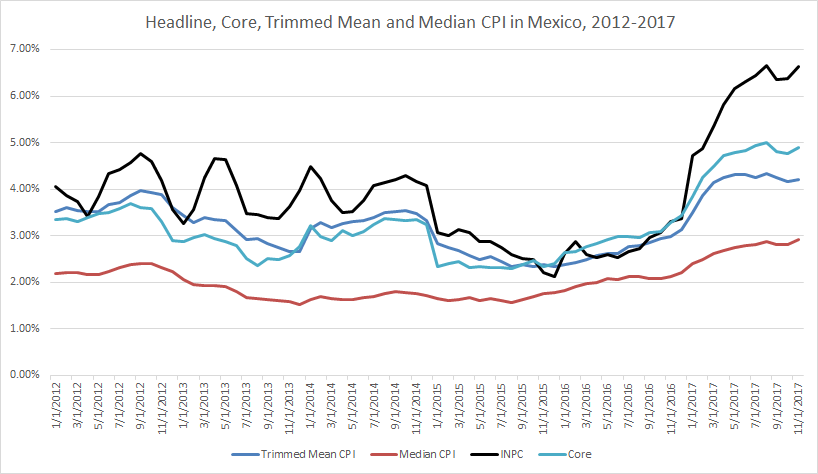

Headline inflation is indeed still over 6% and has yet to start falling significantly as the central bank predicted during the summer….but this is largely due to a huge increase in propane prices. Similarly, contrary to what many sell-side analysts reported, higher than expected inflation figures over the past couple of months were not due to pass-through effects from the depreciation of the peso, but instead from a modest seasonal increase in retail prices across the board, not one isolated to larger increases in the prices of imported goods.

More importantly, underlying inflation gauges have indeed stabilized--core, trimmed mean and median inflation levels have been stable for months, and will soon start to decrease as the base effects from the price shocks of early 2017 roll off.

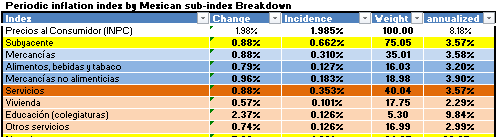

High frequency data also points to a stabilization of price increases--the right hand column of this chart shows the 3m/3m annualized inflation figures...core is 3.57%, as is services...a number that is skewed higher by a seasonal increase in education prices. These figures are well in line with historical norms.

3) Rates are already high. Given the deteriorating consumption, investment and growth figures, there is good evidence the current level of rates is already stifling economic activity.

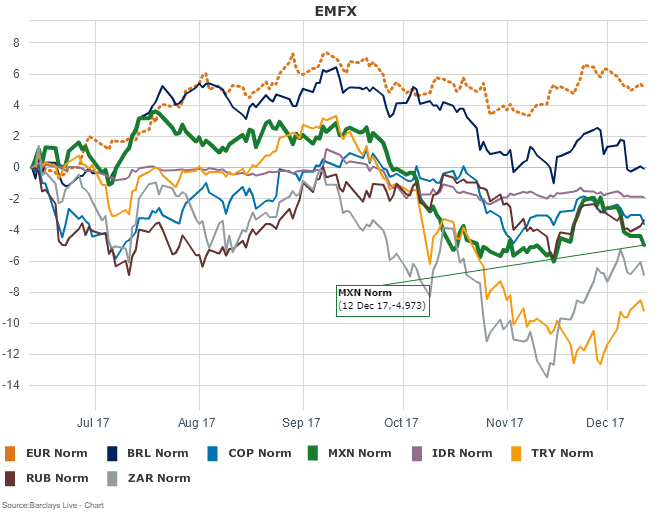

4) Which leaves us with the peso...has the selloff in MXN really been that big? It’s off 5% over the last six months...in the bottom tier for EMFX over that span but far from a game-changer for monetary policy...especially when you got back around 3% of that in carry.

I like to err on the hawkish side in orthodox EM monetary policy debates because so often the question comes back to financial stability and volatility. But in this case the central bank has already done the heavy lifting, and another 25bps is going to do more to hurt domestic investment than it is going to stabilize the currency, which is going to bounce around like a pinball in 2018 as NAFTA and the presidential election take the center stage--there's little Banxico can do to change that.

Does the selloff in front end US rates and the steepening eurodollar curve change any of that? It should...eventually--if the Fed persists or accelerates hikes next year and causes a big strengthening of USD vs. EMFX. That continues to look unlikely after today's low US core inflation print, so there's no pressing need for Banxico to react in kind to the Fed's hike. Regardless, I think Banxico has done enough already to buy itself some time in 2018 when the bank's forecasts of lower growth and inflation will come into focus.

What about the Alejandro Diaz de Leon, the new boss at Banxico? Some say he’ll want to come out swinging with a hike to prove he’s a tough guy. Banxico doesn’t operate that way. They’re smart, data-driven, and painstakingly independent. They’re no more likely to be pushed into a hike now than they are to be pushed into doing PRI a monetary favor before next year’s election.

A weakening economy, cratering credit growth, high ex-ante real rates, and stable (and soon to fall) inflation...Doesn’t add up to a hike!

Shawn

TeamMacroMan2@gmail.com

@EMInflationista

Shawn

TeamMacroMan2@gmail.com

@EMInflationista

10 comments

Click here for commentsNo strong view, but makes sense. Thank you. Tomorrow is a big, BIG day of central bank meetings.

ReplyI think it's safe to say that govts and institutions are amassing a pretty big offensive on cryptocurrencies. Only a matter of time. My bet is that gold gets a bid sooner than later and starts taking out stops galore above 1300. If it has not gotten demolished on the coordinated CB tightening view yet, it may just get a boost on coordinated cryptocurrency annihilation assignment to be carried out in 2018.

ReplyMea Culpa on nat gas. I was wrong, wrong, wrong... Pick up the pieces and move on.

not to go all zerohedge here, but how would CBs or governments go about annihilation of cryptos? and why? (I mean, i kinda get why, I just don't know why they would be motivated to do so) the coordination of CBs was touch and go at best in the midst of the financial crisis...how would they hold their dirty cartel together?

Reply@Johno, I wish I had something intellegent to say about TRY and the CB there....if you have any bright ideas, pass them on!

@Shawn, I don't think it would be hard for the govts and CBs to prick the over-inflated bubble. It is much easier to destroy than to build. Cryptocurrencies possess the feel of anarchy not usually welcomed by the "dirty cartel". There can only be one sheriff in town, and we both know it's the one with the bigger gun that wins.

ReplyOh yeaaaah, Norges Bank takes in first hike from summer 2019 to Autumn 2018. At this rate, we'll have a spring hike!

ReplyTurkey. Seriously. You couldn't hike the late liquidity window another 50bps and put this thing to bed? You couldn't give the market just a 25bps real return despite you over-shooting your target forever, inflation and inflation expectations going into the stratosphere, and 11% GDP growth (yoy) last quarter? What a joke.

ReplyAt least I dumped all my delta one exposure (profitably!) in the Tokyo morning ...

@Shawn: not so much about why (insert your favorite conspiracy theory here), but as for the how, I think this is rather straightforward. Make sure that crypto "currencies" cannot be converted into real currencies like USD, i.e. shut down the exchanges. For example you can force them to KYC their customers and impose fines if they fail (which would ruin the whole point about anonymity). If you have crypto coins but can trade them only OTC with all risks involved the attractiveness should vanish. No more price increases every day, thus fewer interested parties and there she goes (imo at least).

ReplyHope everyone shaved this morning. The attractive news anchors are coming to see us.

Replyhttps://www.marketwatch.com/story/80s-cheer-for-end-of-year-stocks-that-remind-bulls-of-the-reagan-volcker-era-2017-12-14

heh, that's awesome...welcome, Marketwatch readers! With any luck they will overlook the following piece about Banxico staying on hold. You miss every shot you don't take, I guess.

ReplyMy guess is getting long Nordic currencies through year-end, you'll be able to unwind much better in a month. Think this move is year-end dollar demand-driven (plus some other passing factors). We'll see .... Best thing on my radar right now.

ReplyFingers crossed for South Africa this weekend ...