"You better move! You better dance!" - Ke$ha

Oh boy.

And here I thought the Donald was going to take down Mexico.

Trump goes after Canada on the lumber trade. CAD moved on the news. Fast forward a couple of days, Trump comes out Wednesday night and says we are staying in NAFTA, CAD moves back on the news.

In the midst of these flashy headlines, I wanted to take this opportunity and actually dissect the noise and actually pinpoint what I think is truly important for USDCAD.

Let's start with the noise.

These were the main Canadian exports in 2014 - (sorry for the lagged data) Assume they haven't changed much.

As you can see, lumber is not a big driver here. From a correlation perspective, you get a lot of noise for both lumber and gold. Looks like nothing substantial there. I understand the Donald's posturing has ramifications beyond the Canadian lumber industry and that could have been the cause for the move. But I digress, there are more important factors for CAD - all shall be revealed as you keep scrolling down.

My eyes hurt from looking at this chart.

Alright, moving on to car exports, we start to see something more interesting.

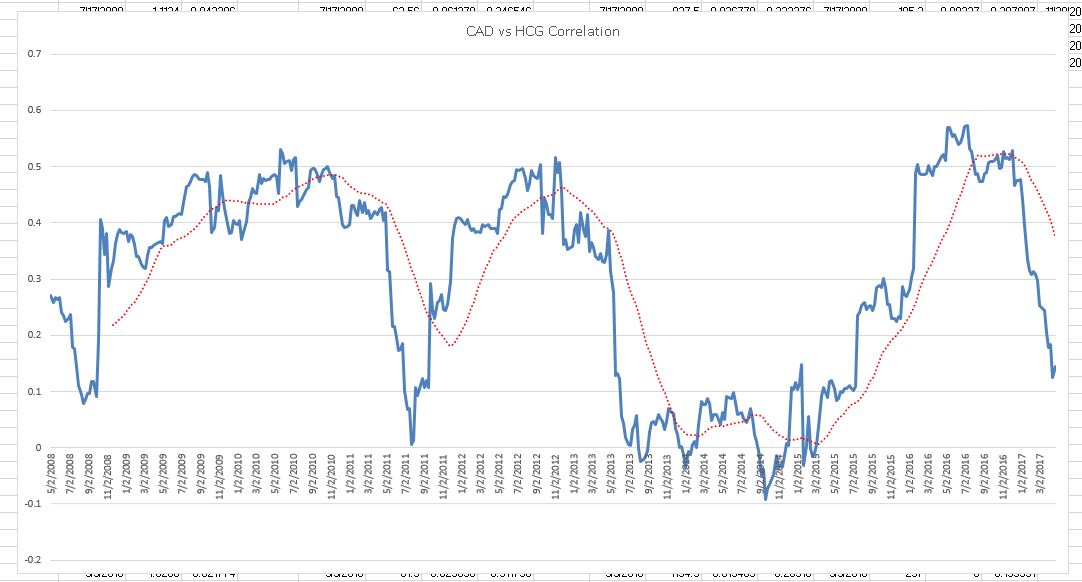

Finally, looking at oil price, we really get something juicy.

But even here, we have seen the correlation between CAD and oil slipping since the height of the oil crash. In fact, weekly correlations (what I have plotted above) have been hovering around 0.2 to 0.3 in the last 12 weeks or so.

Now comes the signal.

This brings me to something that's even more interesting. The Canada housing bubble. I think this will be the main driver for USDCAD moving forward the rest of the year.

But in this situation, the housing bubble has gotten me thinking that things can actually continue to worsen.

If it does worsen, what will Poloz do? I think negative rates and QE are not out of the question in Canada. In the meanwhile, we could see steady rate hikes in the US (yes, we can argue about this, but let's do that on another day).

Thanks guys, good luck.

52 comments

Click here for commentsThis is why I read this blog. Thanks. You might also want to checkout the GBPCAD chart. One might wonder why a currency for a country locked into an uncertain economic path managed to recover 10% of it's purchasing power against a country that historically as had much better finances.

ReplyYeah GBPCAD is very interesting. Macro Clown made some good points about it from a high level a month back.

Replyhttps://macro-man.blogspot.com/2017/03/carney-cable-guy.html?m=1

ReplyRate markets aren't sniffing doom yet in Canada I don't think (haven't looked in options space though). Meanwhile, oil is probably near the low of its range and USDCAD is trading modestly rich to its drivers. You now just had Trump say US staying in NAFTA. I suspect specs have been drawn in by that break above 1.36, the NAFTA rumors, the softwood lumber tariff (which itself is pretty insignificant). My guess is you'd need to see USDCAD driving higher soon, otherwise the air comes out. A housing debacle is going to be a slower moving process, I think, and maybe isn't ripe yet for near-term action in the currency. It has been (slower moving) in Vancouver since the 15% tax on foreigners was implemented.

ReplyI think you may both end up being right on this in the sense I think it might take time to come to fruition. I'm always wary of buying 'news' near breakout points.

ReplyGood points Johno. I guess it boils down to how tactical you wanna get. Personally, knowing my own limitations, I don't want to get too cute trying to catch what I believe would be a small drop in USDCAD and in turn miss what I believe will be a huge move. Markets are very hard to time and bubbles are near impossible to time. With that caveat in mind, I do believe this housing crisis is near the tipping point as Canada's first subprime lender is prob on the verge of going bust.

ReplyThat's why I put the time table at 8 months - I think the rest of the year, housing will continue to become a bigger driver for CAD.

I really like the USDCAD chart too.

We shall see!

Detroit Red, nice post! I've been yapping about my Canadian banks shorts here for months ad nauseam. For the sake of the argument on when to take this trade, while one could draw the comparison to US housing bubble for the timeline of the euphoria resolution and how quickly it may evolve, it should be noted that there are no happy endings in bubbles. So I agree, the trade is on and there will be opportunities to add to it (like today on NAFTA announcement). Keep in mind that last night's NAFTA decision rests on the assumption that our neighbors would bend over. But I think all Mexico and Canada are doing is buying themselves time while looking for new trading partners. They are not blind and can see what's ahead. All it would take is for POTUS to have an extended restroom break to reverse his decision to stay in NAFTA. Sorry, exhilarated Trump voters (if any reside on this blog), you can't defend the egocentric lunatic on the issue of flip-flopping. Going back to my Canadian banks shorts. My intention originally was to short the mtg lenders like HCG. But like in US housing bubble (where I opted out of shorting AHM & CFC and went with the big banks) I think that large players will also take the hit due to their exposure to all problems you so skillfully depicted above. So, short TD, RY, BMO, and my favorite - CM. Check out the double top on monthly charts, sweet.

ReplyGood analysis DR.

ReplyHome Capital looks to me like Canada's version of Countywide or Northern Rock. Now what we need is for Poloz to say that "the problems in the subprime market seems likely to be contained.” and we will know that the worst is at hand.

A thought experiment. Canada exports oil. Many Canadian investors (read: large banks) will from time to time be long oil, with leverage. Oil prices are weakening, continuing a structural change in the market that began in 2014. As oil weakens, many Canadian (and Texan) investors will lose money. If oil weakens significantly, Canadian (and Texan) employment is going to be affected. Some Canadians will fall behind or default on their mortgages just as the housing bubble pops. The losses associated with falling MBS values will be felt by Canadian investors (large banks) who will lose money. As this cycle proceeds, Canadian investors will reduced leveraged long oil positions, and global investors will be forced to follow suit, allowing the price of oil to fall closer to its natural (supply-demand) level, perhaps as low as $20/bbl or lower. The tumbling oil price will exacerbate the drop in Canadian house prices. Eventually a banking crisis will ensue.

ReplyDetroit Red is on the money with this one. We like CADJPY as the best FX play for this trade, as it by-passes the undulations of King Dollar and policy wobbles of The Donald and the Muncher, while incorporating a likely source for many leveraged carry trades that will have to be unwound.

It is an awesome thing when you have watched a bubble like this one grow, literally for 10-20 years, and then the first canary in the coal mine appears to indicate that the goose is cooked. All bubbles burst, without exception.

"All bubbles burst, without exception" Who would argue with that truism. The problem is ironic really. Getting an acceptable definition of what constitutes a bubble in such a way that it could be recognised and circumvented. The ironic part is of course economic experts can't actually recognise one apparently before the fact and of course if everyone could then we would never actually have one. Let's just accept that some of us care more about fundamentals than others and over the long haul it helps us manage our portfolios.

ReplyIn domestic news, Atlanta Fed lowered GDP 1Q forecast to 0.2%, JPM lowered to 0.3%. Not that we are predicting a yuuuuge recession or anything, but surely the New Normal slow growth meme is back? The domestic consumer clearly isn't in great shape, which is somewhat unnerving given the present rate of unemployment. Traditional retail is melting down, and the restaurant recession is in full swing. All of these seem somewhat predictable consequences of stalling wage growth in the U.S.

ReplyThis week's Treasury auctions have been mixed. 2y was strong Tuesday, yesterday's 5y was weak, perhaps b/c of the timing right on top of the tax reform policy announcement. 7y auction up next. Be careful, Mr (Bond) Shorty...

How is 20 usd oil the natural level? Inventories have corrected about 20pct so far globally and the pace should pickup with demand growth. Offshore is a third of global supply and needs higher than spot to sustain on average. Shale still a bubble with true breakeven north of 60, so where's all the 20usd oil going to come from sustainably?

ReplyIPA - How are you deciding between the currency versus the bank shares? Are you shorting the actual shares of the Canadian banks or are you doing it via options, and where are your targets? Put spreads going out to year end look to have decent pay offs and vols look cheap for equities.

ReplyGuys, you are in an echo chamber where all your analogies to the US housing market crash seem obvious. There is a world of difference between the two situations. For one the laws. Here in Canada we take a mortgage seriously, perhaps because some of us speak French. Mort = death and gage means to be 'engaged' or tied to something.

ReplyThus a a mortgage means you are tied to the death for this borrowed money. Very different from US laws, where you can walk away by mailing back the keys. Here the bank sells the house and any part of the mortgage not paid off is still your responsibility.

House prices have only risen dramatically in 2 cities - the rest of Canada has had hardly any appreciation for at least 3 or 4 years. There are fundamental drivers in Toronto, where I live, such as 42 people, on average, moving into Toronto every day, 100K a year, a million a decade. For almost 40 years, the greater Toronto area has been the second fastest growing urban area - after Miami -and the momentum is only increasing. There is tremendous fundamental demand for housing in Toronto, that will only stop with a major depression or some other black swan event like an avian flu epidemic or war.

The oil crash in Alberta, actually caused a lot of Albertans to move to Toronto adding to housing demand here.

Very high real estate costs are the problems of incredibly successful cities like London, New York and Paris and our rising real estate prices reflect that change in Toronto and Vancouver's status. Talented and moneyed folks all over the world are moving to these livable and interesting cities because their brand, as well as the Canada brand, are rising.

That speculation is a problem with both local and international players is true and is now being addressed with 15% tax on foreign buyers and a city vacancy tax. But the underlying fundamental drivers of housing demand will not go away soon. The CDA may fall versus the USD but a housing collapse, which has been predicted for 10 years now, will not be a driver of that fall.

Thanks for posting an alternative view, cogitoergosumm.

ReplyEURNOK looking ripe to fall over. Been weak all day despite oil falling and now oil coming back. Impressive bounce back in USDCAD after the Trump/NAFTA selloff overnight. Still just watching that one. Mentioned at the end of the last thread that the CBT is using yesterday's hike in the late liquidity rate to push up rates -- looking good for USDTRY. Any views out there on policy changes affecting foreign investors' ability to hedge MYR debt holdings starting May 2 and what they're going to mean for MYR? Look at EURCZK -- what a joke. Can you imagine what happens to that crowded POS when we actually get a risk-off episode?

@Unknown said: "How is 20 usd oil the natural level? Inventories have corrected about 20pct so far globally and the pace should pickup with demand growth. Offshore is a third of global supply and needs higher than spot to sustain on average. Shale still a bubble with true breakeven north of 60, so where's all the 20usd oil going to come from sustainably?"

ReplyThe rebalancing story is hogwash, OPEC members will cheat as always. The inventory data are suspect and in many cases are politically manipulated. Demand growth for crude is a concept that some energy CEOs and central bankers would love to see, but it isn't really happening and that's reflected in prices since 2014. The energy markets have already undergone structural changes toward renewables that are probably irreversible, and the era of breakneck growth and energy use in China is behind us. 20 usd oil is quite possibly the natural level of price for a commodity for which there is now declining demand, especially if we are in the mid-stages of a stronger dollar FX regime. It could even go lower. Whether this is "sustainable" or not is a good question, as it depends on economic activity in a demographically challenged developed world (Japan, EU, US, UK, Canada) plus now we can add China - but if demand stays low, there is still a lot of easily reached oil out there that will be sold at low prices. Shale is a bubble, for sure, and it is one of many many bubbles out there in asset prices.

Cogito seems to think that "it's different this time" and "it can't happen here"…..

ReplyI also live in Toronto and I can tell you EVERYONE in this city is oblivious to the fact that it can happen here. Every time I go to starbucks (which is usually every day) I see a Chinese Real Estate agent sitting with a client signing documents on a house purchase. I've overhead so many conversations and everyone seems to think its a no brainer.

ReplyThe truth is this market is a bubble and the fundamental arguments people make is nothing but rubbish hogwash. There are 28 year olds sitting with 10 housing properties as investments all over the GTA. I hear it at the coffee shops as this is where a lot of them come to do business.

Once the unravelling begins the no sayers will see how much froth has been built into the market over decades.

Cogito, I too live in the epicentre of the Toronto real estate bubble and have heard your arguments over and over again. With all due respect, I completely disagree.

ReplyToronto is not New York, London or Tokyo and never will be. We don't have the climate, geopolitical location or tax system that are prerequisites. This us a bubble of historic proportions. You are right that this isn't directly comparable to the US... in fact, it is much worse. Canada is a tiny economy with no manufacturing base and entirely dependent on imports for all manufactured goods. This puts limits on what the BoC can do to stimulate through monetary policy. Unlike the US we do not control the global reserve currency and could never get away with the type of balance sheet expansion that the ECB or Fed have. It would be hyperinflationary.

cogitoergosumm: There are fundamental drivers in Toronto, where I live, such as 42 people, on average, moving into Toronto every day, 100K a year, a million a decade.

ReplyET: Unlike the claim that 20 USD is the natural level for a barrel of oil (which can't really be proven one way or another, either you are using a different numbering system than the rest of us, or you are just plain incorrect. My trusty calculator tells me that 42 * 365 = 15,330, which is close to an order of magnitude away from 100,000 per year.

cogitoergosumm: Very high real estate costs are the problems of incredibly successful cities like London, New York and Paris and our rising real estate prices reflect that change in Toronto and Vancouver's status.

ET: Very high real estate costs are mostly the result of corrupt and/or stupid politicians who persue policies that artificially restrict the supply of housing and/or drive up the cost of residential construction.

We heard similar reasons explaining why prices could never fall in certain U.S. cities (and several U.S. states do give lenders recourse to other assets if a borrower fails on his mortgage). I still say that debt levels make the current situation unsustainable.

I am usually not an "events" person (one look at my results would tell you why), but adding risk before the first round of the French election (which I worte about here seemed obvious, and worked out spectacularly well. Therefore, I am going to press my luck and try again. I have reversed most of those trades, in particular buying back Treasuries at much lower prices, and actually adding to the my positions in anticipation of the GDP release tomorrow. If the GDP gnomes spit out a bad number (it could even have a minus sign in front of it, though that is not especially likely), we could see the move to lower rates accelerate rather dramatically (and that might just turn out to be the Godot that Nico is waiting for, though that seems rather unlikely, as well).

No Lefty, I am the guy who bought my first house in Toronto in 1982, when everyone was screaming that mortgage rates were 22% and housing was going to zero and sold it for 300% appreciation in 1989 when everyone was saying that housing could only appreciate because the Hong Kong Chinese were all coming. By the way no one at the time was talking house crash, yet prices fell over 40% in Toronto over the next few years.

ReplyI bought a better house in 1992 in a better neigbourhood and am up about 500% on paper, but I am not selling because I love living in my house and over time it will do well. Even a 1% annual rise means I am up 15K. However,there is a pretty good chance that we now get a pullback of 10 to 25% or a sideways move or minor appreciation for a number of years, while we digest the huge gains we have made.Some speculators will get hurt but the vast majority of Canadians have considerable equity in their houses and are not speculating or flipping homes and have their mortgages with our banks, which do not allow us to use our houses as ATM's. The debt numbers may look scary, but not if put against assets owned.

So a crash will only happen, if we get some black swan event or interest rates jump by 4 or 5% rapidly, which I do not see. In fact, decent chance that Poloz moves rates down in the near future, which would make Canadian dollar weaker still.In fact he probably would already have done so, except for what it would do to prices in Toronto and Vancouver. But he has no reason to raise them, as the rest of the country would not accept being punished for what is a localised problem.

But this weak dollar is great for many industries up here, like the TV and film industry I am in, which keeps having huge record years. In fact, high oil prices which tend to make our currency much stronger are quite tough on everywhere except ALberta and Sasketchewan, where there is oil.

I am only trying to get you guys to see that there is a reality outside your own echo chamber. NO point losing money over groupthink, the group will not help with the losses.

cogitoergosumm, thanks for the feedback. I've heard this over and over again.

ReplyPrice appreciation occurs at the margin. When some chinese dude comes into a neighborhood and pays some ridiculous price over asking (which mind you is staged by the RE agent) then all homes in the neighborhood get re-priced to that standard.

What has been happening is a game of re-pricing as investors keep over paying. So the on the surface it looks like there is a healthy reason why prices are appreciating. Reality is its all activity at the margin.

Once that activity at the margin changes, it will be timberrrrrr because the boat is bloated and people so levered they can't sleep at night. I know guys that are literally having panic attacks because of the number of properties they hold and mortgages on them.

There was just an article out there somewhere on jingle mail in US and potential parallels for Canada. Basically only 7 states in US had non-recourse mortgages and Florida for example was not one of them (but California was). Two provinces in Canada have limited non-recourse as well. The fact that majority of states had recourse provisions in US did not stop the housing crisis from developing.So I would still bet on fundamental affordability here or the lack thereof and confidence crisis as the trigger - the Home Capital trigger may or may not be it, but definitely striking parallels.

ReplyLefback: The energy markets have already undergone structural changes toward renewables that are probably irreversible, and the era of breakneck growth and energy use in China is behind us.

ReplyET: Yes, see this story about flatlining electricity demand. This is even more remarkable considering the growth in U.S. popluation and the massive increase in electricity usage by data centers. Oil could very well go the way of coal (lagged by a few years).

On your oil post LB I'd say I wish you are partly right for the disruption it would cause and the many things that might happen as a result. However the numbers for oil have basically been so stable for years, and probably will be for a little while longer. That leaves a trend of inventory normalisation which if it continues will leave the oil price looking too low in six months time.

ReplyA dip to $20 would be great but my base case is we grind into 60s as global inventories continue their trend and lack of capex. It's a furtive space with lots of way to skin cats so I'd love to see vol

i&t, I am long puts on the banks I mentioned above with a target of middle bollinger band on monthly, and also long USD/CAD with a target of 1.40

ReplyMeanwhile on the otherside of the Atlantic perhaps EU negotiators should take alook at sterling and ask themselves where's the money flowing.

Reply"In a vote of confidence in Brexit Britain, UK FDI inflows soared to $253.7bn (£197bn) in 2016, up from £33bn the previous year, according to the Organisation for Economic Co-operation and Development (OECD).

This represents the highest level of inflows since 2005.

The figures also showed the UK drove the bulk of the 17pc increase in FDI inflows to the European Union."

Just one comment on Canadian property @ cogito. First, let me say I appreciate the otherside of the argument and in fairness your take on it is not bullish so much as simply not systemic crash which still leaves a lot of room inbetween. Anyway , my comment is this. Price rises as mentioned do actually function at extremes at the margins. By this I mean when volume drops and prices are still rising it is because there is still the odd greater fool wandering in. This does not just apply to housing ,but housing is also relatively illiquid compared to many asset groups and as such when the marginal buyers do eventually disappear the effect of the turnaround as we have seen in the past can be dramatic. I would cite you the best example I can think of here and it is not the USA crash. It's actually the Spanish property market. You see the Spanish market leveraged up just like The US and UK ,but there was one major difference and that might be very much the case for Canada as it is for OZ. It was a market where the marginal buyers were not domestic. The demand in other words was external. I don't know enough about Canada to know if this is the case there , but if it is then how the market will respond may depend upon whether there is any substantial hangover in the new build developments. The latter were critical in Spain as you saw massive uplift in supply facing almost instantaneous drops in demand and inbetween huge cashflow issues. We know what came next of course. I was heavily involved n every property market cycle from the early 70's onwards so I think I have seen every shade of what this market can offer and in the UK I don't have any problem recognising where we are in the cycle. Unfortunately, I don't know the Canadian market in the same way, but I can suggest what signs to look for and hope the above might give thought on those.

Reply@checkmate Isn't the marginal buyer (esp London) in the UK foreign as well? Could you share your thoughts on the UK property cycle please. I'm AU based and I think foreign interest has peaked for now (2017Q1), so the cycle may turn soon. Although exactly when is anyone's guess, of course.

ReplyWell, this article was excellent! Nico keep the good stuff coming and ignore this nasty Harry chap.

ReplyParallels with Aus are striking - both have scary house price appreciation relative to income and anything else you choose, but also population growth and supply shortages in major cities. Australia doesn't really have a subprime game though.

As an Aussie I'm going to watch this closely, may provide a playbook

On oil, I've had a bit of luck on the short side twice this year, that seems to be the way the market is cracking when it moves. It's striking that oil is stuck around $50 with all these attempts to jawbone the market. Bodes weakness from these levels, but I may take profits here after catching an 8% move.

Short oil and long a low-cost cash-generating producer (I chose Beach Energy) seems a decent two-way bet.

Thoughts on biotech and Elliott vs BHP if anyone's interested:

http://www.fraziscapitalpartners.com/pdf/FrazisMarch17.pdf

Hey, Macro Man. you member that guy back in the day that got pinched in his mothers garage for causing the flash crash. Well , I feel like that little trader in the garage with every move on my computer screen being watched. Have you ever seen a guy spew so much bullshit within 100 days! Sorry Wall street, get f##ked. I'm not jumping in on the next rally. Get f##ked. You've got over there traders at the desk that you can't stop from fiddling around with the bid , but you want me to invest everything in wall street while the transactions costs just eat away at my account.Get f##ked.

ReplyLook at how many listings are there right now. And people are talking about no inventory?

Replyhttps://www.realtor.ca/Residential/Map.aspx#CultureId=1&ApplicationId=1&RecordsPerPage=9&MaximumResults=9&PropertySearchTypeId=1&TransactionTypeId=2&StoreyRange=0-0&BedRange=3-0&BathRange=0-0&LongitudeMin=-79.56822632696769&LongitudeMax=-79.24309967901847&LatitudeMin=43.83775174407336&LatitudeMax=43.93672555240795&SortOrder=A&SortBy=1&viewState=m&Longitude=-79.43121909048698&Latitude=43.9089830861792&ZoomLevel=11&CurrentPage=1&PropertyTypeGroupID=1

The Toronto Area property market is 60%-70% over valued. My parents bought their home in Richmond Hill for 280K in 1998. That same house is going for 1.7-1.8m today.

Did we discover oil, gold or diamonds on our property? I don't see anything like that and nor do I see a job boom in Toronto.

I have never cared for analysis based up this was worth X in 1998 and now it's Y so there must be a problem. There may well be a problem ,but usually it isn't the absolute values that are the issue. It's whats happened in the general economic environment over the same period and how far out of line for the fundamentals been stretched in terms of servicing the underlying debt.

ReplyAs far as Canada goes I would be looking at the new start numbers for the last 2 to 3 years and particularly those in the cities that have may have been the target for external buyers. If supply of new builds as ramped up significantly then it's much more likely to be a sizeable cashflow problem if demand then diminishes. If there is no build up of supply in new builds then to be honest it may just be one outfit who are out on a limb misjudging the recent policy changes to dissuade foreign buying.

What did strike me was the comment about Chinese brokers meeting up with buyers posted above somewhere. It might just be parochial and of no real significance ,but it resonated with me when I was thinking about the Irish leprechauns who were swarming allover the Spanish Med Coast back in that day. In effect both groups were people who were playing in strange hunting grounds in the sense that neither had any real fundamental understanding of the market they were playing in. All they knew was where the momentum/noise was. As I say it may be parochial and there may actually be substantial differences between markets in question regarding supply.

@Tester. The UK market is not actually a market. There's London SE (+ hotspots like Bath) then there is everythingesle. They perform quite differently most of the time.

London over the years as had three major factors in play. Finance and all things finance that underpin it as the area to be. I suppose I could have caught the second factor in with the first in that it's been a great target for money looking to diversify away from political instability elsewhere. The third factor as been currency. Weak pound inflows. None of those factors count anywhere else in the UK really apart from maybe Bath with dribbles finding it's way to B/Ham ,Manchester . The latter not really enough to disturb the local factors that determine market fundamentals. If you think the cycle turns up again for London soon then all I can say is look again at the factors I have just mentioned and think about it. The rest of the UK outside of hotspots I would describe as stagnant. Low volumes ,but prices held modestly flat because of supply issues. This is mainly a policy issue. Current transactional costs are such that it's made staying put/upgrading more attractive than moving. Hence, the drop off in volume. To pat myself on the back here I said this would happen well over a year ago. It really was obvious. People ascribing it to politics/ Brexit have no idea what they are talking about.

Some more charts on Cdn housing market

Replyhttp://www.chpc.biz/housing-price-momentum.html

Very interesting and informative discussion on the real estate throughout the world and especially Canada - the latest child of human fascination with speculation. While all real estate is local one has to remember that greed and fear are not bound by borders and don't speak a language. Those are universal feelings that reside in all bubbles and could be brought in from abroad. Hot real estate markets attract speculation from the outside and eventually get to a wildly overpriced level from which the fall is usually sharp. All the market would do is discover the price level at which the equilibrium is attained and fundamental price stability is restored. Unfortunately, the pendulum always swings far on both sides and overshoots occur when speculators either enter or exit en masse. With this in mind, a trader like me wants to capture the chunk of the move down on their exit but it's not my objective to remain in the trade until the whites of the eyes are seen. Furthermore, I could not care less if this move is anything like the one in US or not, and I want to capture the fear of a possible resemblance, even if it's just a perception. As you can see, the move down is well under way and fear does not care about fundamentals many posters here are defending, just like the greed did not. We are in a full-fledged panic phase here, where players shoot first and ask questions later. So time to cover half and move stops to b/e. At least this trader just did.

ReplyJust to be clear IPA, there is absolutely no panic in Toronto (or anywhere else in Canada) right now, amongst the general public. Folks are completely mesmerized by the housing market. Houses are selling for hundreds of thousands of dollars over the asking price. The vast majority of people have never heard of Home Capital, and those who do have no idea what are the implications of disruptions in the mortgage funding market.

ReplyEveryone, and I mean everyone, here is talking about housing. People are questioning why they are working at a job when there are such tremendous opportunities in real estate speculation. I had dinner with a good friend last night who is a highly successful entrepreneur, and the first thing that he wanted to discuss was the houses that he is looking at for "two year investments", on which he expects to make a 30 - 50% return, based on a linear extrapolation. This guy has an MBA and built a $30 million business from scratch. He doesn't see a scenario where real estate prices could go down. "The worst that could happen is that I get to collects rents until the market picks up again."

I paid a lot of attention to the US RE market in 2007, as I structured ABS and MBS at the time. This is exactly the same psychology.

P.P. Mazzini, I hear you. Your anecdote is yet another confirmation of the delirious state of euphoria mentality. Thanks for sharing the scoop from ground zero. I was talking about panic in bank stocks and CAD vs panic in real estate which I think is still yet to come. Stocks and currency anticipate what's ahead in the underlying asset of the bubble. The general public panic is still yet to come, imo. The little guy always gets hurt and ends up holding the bag. I just trade bank stocks and CAD on this development, that's all.

ReplyIPA

Reply'All real estate is local' is one of those pieces of nonsense someone must have thought up because it sounded good. Actually if the property happens to be a target for external demand then it is anything but local.

To summarise, the Canadian, Australian, New Zealand, UK(London) and Irish housing markets are smoking hot(all mentioned here in the last month). Give me the fertility rate of Nigeria in any of the mentioned and I will happily buy any dip.

Reply@P.P Mazzini...

ReplyI have many relatives in greater TO/Calgary/Vancouver area..Yes they too believe,"why work" when speculation makes you millionaires..And Real estates has made some of them more money then their Ph.Ds..

What are your thoughts on Toronto market? I know the Cdn market(especially Vancouver) was talked about a lot after the U.S. crash(never happened until the local govt imposed a penalty)

@Skr "Give me the fertility rate of Nigeria in any of the mentioned and I will happily buy any dip"

ReplyFor Canada, Australia just look at immigration numbers. Canada is yuuge!!! Crazy.

I was born in India..everyone I know and their aunt is now living in Canada

But I don't know the direction of the r/e mkt..

Checkmate, it does not mean it's only bought or sold by locals, it means the local fundamental specifics are the drivers of the asset prices. But I think we both underline the emphasis on the exact phenomenon which is the culprit of bubbles (in any asset), once it's hot it attracts speculation in a form of "demand" from outside which changes the dynamics of the balance between the buyers and sellers and adds volatile variables otherwise not present in balanced markets. I think the phenomenon is well documented in US housing bubble. We have a template to follow, wether it's securitization of foreign cash buyers, pick your poison.

Reply@River- check-out the Philippines if you want to see a bubble. Chinese, Japanese and Korean(South) monies heavily invested that will run for the hills if/when it goes tits up.

ReplyThe key factor here in Toronto and Vancouver is the level of commitment of foreign buyers to the market. Foreign buyers are a substantial part of the market. Estimates range of 5-20%, but they operate at the top end of the market, and as discussed above, are in many instances the marginal price setters.

ReplyIf the market turns due organic domestic factors, such as rising unemployment or interest rates, will the foreign owners hold or sell? Accepted wisdom locally is that foreign buyers have no where else to put their money, and have no choice but to hold. However, I question that. They can always go to cash. For them this is about security of their capital. If they are facing a combined decline in the CAD and housing prices, they could see a meaningful portion of their capital disappear. If they don't live in the house, isn't it then more of a trading asset, and wouldn't at least some of them pull the trigger on selling? If so, then the fall in prices could (I said "could", because I am not sure) be unlike anything seen before in magnitude and velocity, as they all rush for the exit concurrently. That is the nightmare scenario.

Foreigner could also sell for reasons unrelated to the domestic Canadian situation. Changes in capital controls, better investment opportunities elsewhere, a need for liquidity in the home country. I don't know, but it seems like a long list.

Thanks all for your input into this topic.

Reply@P.P Mazzini re foreigners especially Asians(Chinese,Indians) some of this money could be corruption money(hiding assets)...and hiding their families here

"18000 Chinese officials.. U$ 123 billion fled to the U.S, Canada Australia.."

http://www.huffingtonpost.ca/diane-francis/chinese-money-laundering_b_5664319.html

http://www.huffingtonpost.ca/ike-awgu/canadian-real-estate-foreign-buyers_b_10329000.html

Not to mention there are so many shady practices going on in the Chinese community here.

ReplyResident Chinese serving as proxies for foreign Chinese investors etc, loads of shady fraud money, etc. I live in Richmond Hill, which is one of the epicenters of all this laundering and not only do I see it every day I go for a walk in my neighborhood i.e. houses sitting empty, but I hear it at coffee shops and when I go to my qigong and tai chi meet ups every friday and sunday as most members are from the Chinese community. I hear it first hand from them.

The Canadian government is complacent in all of this. In this day and age, you can trace financial transactions and records but the government has chosen to look the other way so far for political purposes as economy has been a one trick pony the past 10 years.

The big issue isn't the bubble. It's timing the crash, correction, pullback, whatever you want to call it.

ReplyI will be so bold as to say 2019.

Here's the thing, interest rates need to go up at least 200 basis points to make a dent. And that's based on Toronto having a massive chunk of mortgages at 450% or more loan-to-income.

https://betterdwelling.com/city/toronto/more-people-are-buying-toronto-real-estate-that-shouldnt-and-half-are-at-risk-of-defaulting/

So they need to get pinched before they start to default. Next, every mortgage in Canada is effectively an ARM. Nobody signed a 20 year rate guarantee here because the rates are utterly ridiculous. You Americans are so lucky like that. So everybody has 5 year mortgages. This means, you won't any sort of real decline in housing until people holding these jumbo mortgages start renewing at +200 basis points or more. At that point, you'll also many who pre-qualify for less, reducing top line bids for most housing.

You'll see a frenzy this summer, then some pull back. Crash? Won't happen yet.

The money is to be bad on the margins. I made some on HCG's pain this past week. And when I say margins, I don't get why people are shorting the big banks. They're geographically diversified (with huge operations in the US and the Caribbean) and they have most of their mortgages nicely securitized by CMHC. And there's no way to short CMHC.

As for the dollar going down. The housing crash doing that is rather risky. Only because I see oil moving up over the next few years, once the Saudis are satisfied that they've hurt the frackers and Iranians enough. And with that, so will the CAD. That to me, will balance other troubles like housing.

What Canadians think about this subject: Comments

Replyhttp://www.cbc.ca/news/business/home-capital-faq-1.4090098?__vfz=profile_comment%3D7318500008131#vf-1071100008226

As someone above said when it comes to 'bubbles' it's all about timing ,but the problem is you can be 'wrong' for an awful long time before you are right. At various times in the past I have been selling out two complete tax years before the underlying market went pear shaped. For all of that time you have to be prepared for the fact that nearly everybody you meet won't share your view. Indeed some think you are a lunatic. You have to watch other people apparently still making money from the market while you are not. If you actively short there will be plenty of opportunities for you to get your weighting wrong and come under pressure to liquidate. It's a tough gig is I think the best expression and none more so than property because afterall everybody thinks they are an expert on this asset group.

ReplykEiThZ, I shorted big banks vs HCG because of liquidity issues. It trades on pink sheets with no options available at all. I am in US. Like to buy puts. Also, with low or non-existent daily volume the chart is gappy and iffy at best. Big banks went down too and gave me plenty liquidity and options volume to get in and out with no problems. And I was stalking a double top on those monthly charts, it worked out very well.

ReplyThe big Canada banks don't need to take a dollar of losses to be over-valued. The impact will be to the income statement, not the balance sheet. This housing bubble has artificially swollen revenue, and when that goes into reverse they are facing years of contracting top line revenue.

ReplyOn the expense side they are saddled with an incomprehensible amount of ancient legacy systems (30+ year old tech) and assets (too many physical branches). The can on infrastructure investment in the Canadian banks has been kicked down the road for decades, and we are reaching the point where the costs of new systems will be billions or tens of billions (per bank!). The revenue base within Canadian banks is too small to make these investments economic on any reasonable time frame. Management hasn't a clue what to do.

Booming housing has allowed the banks to paper over all of these challenges. If equity analysts did anything other than comparable analysis based on very recent history, they would have noticed this, but they live in an echo chamber.

Bloggers are amazed I guess. I have seen ZH etc talk about it since U.S. bubble burst..

ReplyThe Vancouver Housing Bubble Is Back, And It's (Almost) Bigger Than Ever

http://www.zerohedge.com/news/2017-05-02/vancouver-housing-bubble-back-and-its-almost-bigger-ever