Below is a chart of the VIX daily vs. a rolling percentile

ranking +/- 3St Dev. This is a simple way to look at implied volatility

that I often use in FX land, but

in this case I am applying it to the VIX index. Based on this very simple

indicator, and as is known to just about anyone knows who pays attention to the

financial media, the VIX at the moment, is

cheap. Another key indicator you can grasp easily from the chart below is when

the distance between the Percentile highs and lows narrows it represents a compression of the vol of the

VIX, and as it expands the vol of the VIX is rising. As you can see below while the

gap currently is narrow there have been two other periods when

the gap has been tighter still. So, while the VIX may be close to an extreme

low, the vol of the VIX is not yet at an extreme.

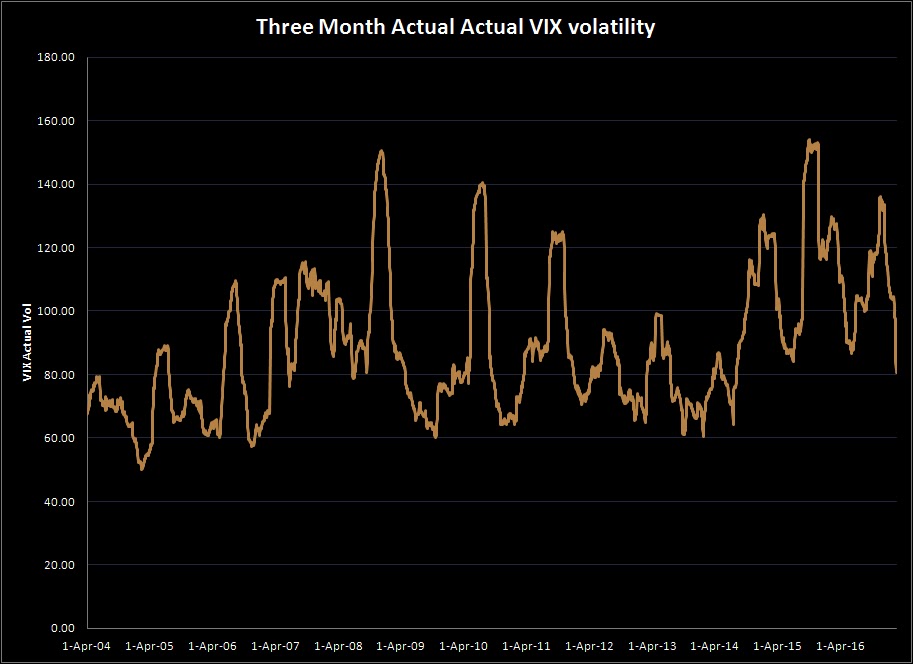

And below is the proof of what we surmised just by looking at the chart above. The chart below is the three month actual vol of the VIX; currently just over 80 but it generally bottoms around 60. What may well be more important is that it is clearly in a downtrend having taken out some support around the 90 level.

The next chart is the VIX plotted against the daily momentum of the VIX. Notice too, not surprisingly the momentum trend is down. However, as you can also see the most recent trend had been rising quite steadily from 2013 until it formed a nice double top in 2016 and broke the trend line and now is testing levels just aboe the previous cyclical low. Since we are not too far from the historic VIX lows, momentum is going to find it a bit of a hard slog to move much lower from here, and may in fact start to find a bottom.

The next chart might involve a bit more controversy, from any conclusions we may try to draw. It is the rolling 55D and 143D correlations of the VIX and the S&P 500. As you can see, and not without too much surprise, in general the S&P and the VIX are negatively correlated. The VIX tends to contract in periods of equity trend expansion and expand in those sharp short periods of equity market weakness. The interesting thing about this chart, is the current weak negative correlation between the VIX and the S&P. It is still negative, no doubt about it, but is is showing the least negative readings in years. Well, it may just be telling us nothing more than what the momentum chart above is suggesting, namely that the VIX can go lower on higher equity prices, but the room for contraction is limited. The other possible explanation is the market short covering gamma positions produced from the sharp rise in the S&P.

The other factor that may be holding up the VIX is the skew, which is also not at a compressed level as out of the money options get bid up for protection purposes.

Apologies for the busy chart below but this is the VIX plotted against the CBOE Skew index which attempts to measure the degree of skew in option prices. And as you can quickly see from the chart below, while the VIX is close to a low, the SKEW is elevated. In fact the skew, recently traded up the its limit at 150 indicating very robust demand for downside protection. The easy conclusion to draw from this is that the skew is not worth owning at these levels, and that option based hedge strategies should incorporate shorting some skew against ones longs. The most obvious trade is put spreads, but there are other variants as well.

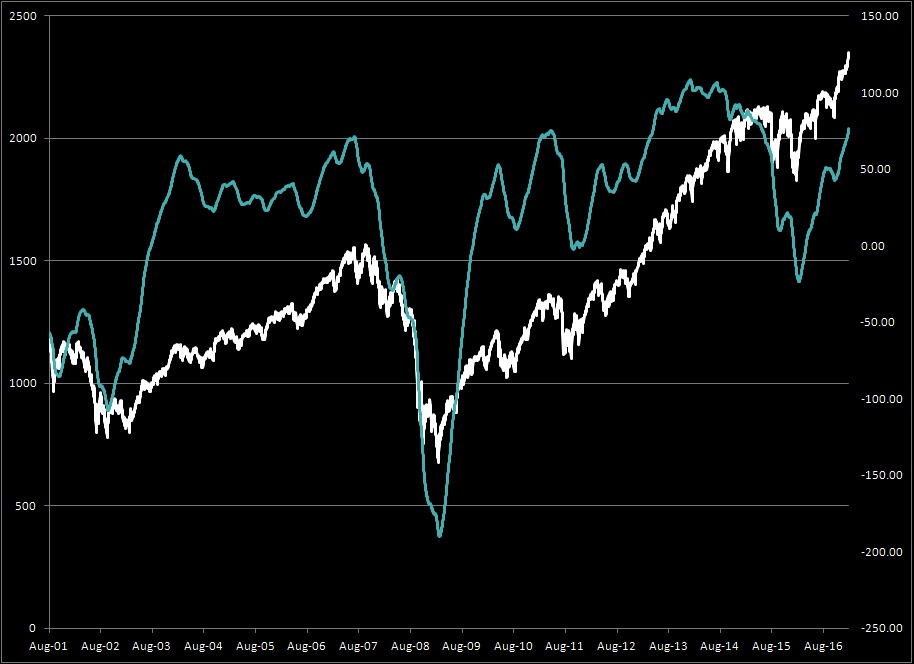

Finally, the next chart below is the S&P 500 daily plotted against the VIX as well as the actual vol of the S&P calculated using a variant of the Parkinson statistic(using the daily Hi and Low of the S&P as apposed the the close to close values). This chart demonstrates that the spread between the VIX and Actual Vol (AV) is almost universally positive and the only times they narrow substantially is following a VIX spike where the VIX declines faster than the AV. Apart from those instances the spread is positive. Another way to asses the cheapness of options is to do the same percentile ranking exercise on the IV-AV spread. At the moment it is running at around 0.66. This is with the VIX at 11.49, the AV at 5.24 and the spread at 6.25. Ideally, it would be better to see the spread below 0.25. In other words the criterion would be less than 3stdev below the rolling percentile rankings, and in the bottom quartile in terms of IV-AV spreads, and some clear signs of momentum exhaustion.

The final chart blow is the S&P vs.my daily momentum indicator. As this chart demonstrates, momentum is just breaking above the previous highs prior to the financial crisis in 2008 and above the levels recorded just prior to the August sell of in 2011 but below the more recent highs seen in 2014. Whether we see those levels again is still in doubt but momentum is clearly trying to trend higher still.

Taking all these

indicators together in sum, it is not unreasonable to expect some sort of

S&P correction.

This may not be a

secular top (unlikely) but more probably, a top that leads to some sort of 10%

or as much as a 15% correction. In a more ideal scenario, we would like to see

the skew get sold off as well, as it is in periods of total capitulation that

the market starts to sell any sort of premium it can find. However, we are not

there yet, and more likely, we may not get there. So, any downside hedge or

spec trade should try to short some skew in the process. That, as I mentioned

above suggests buying put spreads, or ratio put spreads. For example buy 3X ATM

puts and sell 2X 25 Delta puts. On a 10% correction roll out of the put spread

2 by 2 and leave yourself long one in-the-money put as a running hedge.

Secondly idea is similar. Buy 3X ATM puts sell 2X 25 delta puts, and buy 1X 10

delta put. If you get the 10% sell off sell all of the put spread, and leave

yourself long the 10 deltas as a hedge. And the expiry of these options should

be long dated in my view. Consider Sept or Dec 2017 expiration with lots of

time to work in your favor. And in terms of execution work out the mid mark prices and then leave bids still lower. Let the market come to you.

-James

43 comments

Click here for commentsAppreciate the post, James. Several interesting points, especially the chart of SPX-VIX correlation and the explanations you put forward for the recent move. Would be interesting if others with insight into this could comment on which explanation is the likelier.

ReplyOne VIX-related fact I saw today: "Six-month forward returns of ~5% when the VIX is 15 or lower are stronger than returns of 2.1% to 3.1% when it's in the range of 15 to 30." That's a summary of an Oppenheimer technical analyst's work arguing that low VIX should be seen positively.

While some here are pros at shorting markets (I'm not), a cautionary note for those who are not: "Since 1937, the median return six months prior to the bull market peak was 14%, according to a Bank of America study. The minimum gain was 9%, which occurred during the last bull market ending in October 2007. How about 12 months before the peak? The median return was 21%, while the minimum was 11%. The gains were more than enough to absorb the subsequent selloffs in the months following the end of the bull run." I will stop quoting from that source now.

In other news ... a couple articles discussing possible Fed appointees, but nothing new. David Nason a front-runner. Cohn and Mnuchin heading the process. Polls now showing Le Pen at 42/58 or 43/57 in 2nd round, which is starting to look scarier, especially if we have a big act of terrorism (and seeing that ISIS wants a conflict between Islam and the West and Le Pen is likely to oblige, maybe the odds of a terror event are material?). Still, Daily Shot had a chart from CSFB demonstrating the difference in margin between this race and the US Presidential and Brexit votes. EM/PM had a link on the last page worth reading, in a sentence: "China’s financial regulators are working together to draft sweeping new rules for the country’s rapidly-expanding asset-management products that aim to make it clear there’s no government guarantees on such investments." Given that China led the whole growth uplift, it's worth watching how this story evolves. Authorities are clearly trying to slow credit growth in the financial sector (judging by increasing inter-bank rates but steady benchmark rates). I still think the China cycle has some runway, but after the 19th National Congress, I'd bet on a slowdown with global ramifications.

For my part, I took down delta-one position sizes in some Asian FX Sunday night, allowing me to buyback hedge.

@james thanks for that very good study - not that it takes away from your study at all, but the fact that market making algos are stuffed long gamma (and have to scalp it) from short pension funds (who do not have to scalp it) has a lot to do with the price action - I generally agree we are close to a vix bottom in price, but perhaps not in time.

Reply@Johno the bull market argument is a bit self serving - the way I see it we are currently (today) at +20% running YoY returns, and we peaked +28% last week corresponding to the feb 11 2016 low. Not sure what that tells me about where we are in the cycle other than we have checked a couple of boxes, and could be near a top or not, which we could probably say without the study. As for gains being enough to offset subsequent selloffs, it does need to be taken into account that a) losses are way more painful than gains and 2) the number of people who would have invested 12 months prior at the lows and then be prescient enough to pull out at the top would be close to zero, so the amount of increased pain and risk aversion in the market isn't as simple to measure - also, we got well behaved long drawn out topping processes in the previous two cycles, but its not obvious to me why that should always be expected. Central banks? OK, maybe.

The more interesting argument regarding the cycle is that volatility tends to increase prior to the end, so a higher floor on the vix could be about as good an indicator as one gets.

What is happening to German bunds in the front end? Think inflation print tomorrow could catalyze a reversal?

ReplyDoesn't neglect the analysis but the VIX isn't tradeable... It's just (technically the square root of)

Reply30day spx variance, that's often interpolated between two sets of SPX options series... Only really tradeable at the front month Vix future expiration time...

The vix futures (forward start volatility) are tradeable eg. April future, represents April to May fwd starting variance swap (with convexity correction...)

Buy April vix future, it is slightly cheap to fair value and will carry better than front end vix future, will still reset higher in correction (if with lower beta than the front future) ... larger UK insurer is rumored to be buying May SPX variance swap, dislocating the April VIX future from fair value (a variance swap is just vix future + vix options vs a third, otc traded vol product, there's an arb relationship)... If you want to sell skew, can sell an April upside VIX call against the future

Also, for some protection, against this, since implied vol of volatility is cheap, buy otm nearer dated VXX puts to protect you from negative carry/potential one final vol-level reset lower.

DT there is a lot of activity on bunds/OATs spread pertaining to hedging an increasingly likely le Pen victory, affecting the front end

Reply"we got well behaved long drawn out topping processes in the previous two cycles, but its not obvious to me why that should always be expected"

well said washed, as always. The late comers on this rally will be disfigured by speed

Mike Tyson's best quote can well fit complacency seen at every late market cycle: "Everyone has a plan 'till they get punched in the mouth."

James, bravo!! I totally agree with your assessment of the market and your strategy on put spreads (both structure and duration). Once the party ends, it will be one hell of a hangover. I just want to be there to witness it, vomit notwithstanding.

ReplyThis market has more legs than a centipede. You have a fantasy running rampant through peoples' minds. Can you put a multiple on a fantasy? I have been hearing/reading all kinds of crazy valuation calls on the bump the SPX would be receiving from the tax cuts, repatriation, deregulation, and Trump's rejuvenated sex life (ok, scratch the last one). I don't want to start the long discussion on valuations here, as they are subjective and hold no weight in parabolic moves like we are having in some stocks. So I am to believe that everyone woke up on November 9th and received a scripted message about the tax cuts going through with absolutely no headwinds on the way, i.e. in a total vacuum. It's childish to think that this market is driven on fundamentals at the moment. SPX is now trading at 18 X 2017 projected earnings. You factor in that there was a one percent reduction in 2017 consensus EPS by the analysts since the election date and SPX went up 10.5% anticipating an earnings increase on the fantasy alone, and you start to get a dizzy feeling from the euphoria around you. I am systematically going through the house every night collecting towels and burning them so I don't throw one in at the top.

washed @ 6:57. Good points. I'm not advocating long US equities. They do seem the wrong price and putting money into a strategy like merger arbitrage at this point in the cycle seems much better risk/reward.

ReplyWas just reading a GS piece of Feb 16th pointing to the pickup in medium and long-term loans, which tends to lead metals-intensive FAI and manufacturing surveys. They make a surprising argument:

"Unlike the beginning of last year when high credit was pushed into the economy by the government, which needed to boost GDP, it is likely that this year the credit growth was due to “organic” high credit demand by the private sector. One reason why we believe that it was “organic” is that unlike early 2016, the government currently is not trying to loosen monetary and fiscal policy but rather, tighten it, which is reflected in higher interest rates and slower SOE FAI growth. Therefore, the strong credit data is likely due in part to high demand for credit by the private sector (private companies and households) that is willing to borrow and invest even despite higher interest rates. In fact, historically China only slowed down SOE investment and increased rates in periods when the underlying economic strength was high and base metal prices were rallying."

Really? The "slowdown" in SOE FAI looks to be just one data point. And the benchmark rates which I understand to be most relevant for lending to the real economy are unchanged. But maybe I'm all wrong. Would someone enlighten me? Is China seeing a huge burst of "organic" loan demand? I presumed we were just seeing credit being pushed into the economy to get past the 19th National Congress without a wobble, i.e. a kicking of the can into 2018.

Vix and More did a nice post this week about clustering of low volatiity periods and the lack of its ability to presage market falls (a la 'complacency') on a mean reversion basis, versus that of high vol spikes.

Replyhttp://vixandmore.blogspot.co.uk/2017/02/putting-low-stock-volatility-to-good.html

Put on some EURGBP today. On a chart, you're close to levels where the market invalidates you. Only HoL remains to trigger Art 50, though FT suggested they may send back to Commons with amendments. Once Art 50 triggered I'd expect more offshoring announcements. Also inflation should start squeezing consumer spending soon. On the EUR leg, Bayrou announcement a positive for Macron and Hamon-Melenchon tie-up seems a non-starter for Melenchon. So maybe we've seen the peak in Le Pen's odds. Meanwhile eurozone data continues to look good, ECB minutes point to constraints, and EUR is fundamentally under-valued. I do wonder what happens to Europe's cycle as the impulses from China's credit boom and immigration-related spending fade. There's also the PD fragmenting to think about, though I still don't see 5-star party getting to a working majority.

ReplyOn the topic of VIX, daily shot attributed to the breakdown in SPX-VIX correlation to put buying. I should probably check out changes in put open interest to see whether that's the likelier explanation ...

FOMC:

Reply- A Few Participants Said Increase in Equity Prices Might Reflect Unrealistic Policy Expectations

- Some Officials Concerned Low Market Volatility Appeared Inconsistent With Policy Uncertainty

'unrealistic' 'inconsistent' is kinda like 'exuberant' innit? where is our 1996 5% down reaction to that

the Trump vs. Fed fight i've been expecting since his election was quite a one-way flop so far, markets shot up in the face of Yellen's warning and rising rates

Replyi'll insist on the same theme and now expect Fed to raise in March, and raise 50bps if equities have not corrected by then. Just because Yellen will be super pissed off she can't sound as scary as Greenspan

March expiry is going to be one big firework

Lol, Nico G, fed funds futures seriously argue against your 50 bp rate hike notion. But I would definitely take it. I am the biggest cheerleader of your prediction. It's about time Janet put her foot down and show Trump who's the boss of Dow 20K.

ReplyAnother day in fantasy land. Indices are clueless. Money is rotating between the sectors. No reason for concern. VIX this, yen that... FOMC minutes out, fed is impotent. We have a fantasy to dream about. Back to sleep.

Meanwhile, in the real world, behind the curtains, not far away from the fantasy land of perpetual tax cut anticipation, important individual stocks are getting murdered. JBHT absolutely killed during its analyst day today. I mean they couldn't push the sell button fast enough and it was stuck in sell all day long on twice the avg volume. No idea why but would guess it's all about BAT. They deliver a lot of NAFTA goods. Transports took notice and crap hit the fan fast just as DJ industrials made a new high. No confirmation of new highs, no problem. Back to fantasy dream.

More stocks are getting killed. Certain retailers are being taken to the wood shed: apparels and discounters. Someone is not convinced that BAT is DOA. Why would White House change ex-im calculation? I don't think it's only to exaggerate the trade gap. More imports = more BAT collected. Read between the lines. They are going to try BAT. So now we find out there is no tax cut plan or even healthcare plan coming from the White House. Apparently, Trump is a big picture guy and will let the congress make the sausages as he plays golf. So naturally, Paul Ryan's plan comes as a priority. Ryan will try BAT first, just to see how far he can take it. Wait, no "phenomenal" and "massive" plan from Trump? Who cares? Yawn... He'll just read the prepared text on Feb 28 which will include "phenomenal" and "massive" words no matter what.

Even more stocks are taken to the cleaners. AAL closed today exactly at the closing price of the day of its meeting with Trump back on Feb 9. Yep, a round trip. Coincidence? Hardly, that tax cut reform ain't coming any time soon. Not this year, folks. It took Obama and dems a whole year to pass the ACA. You think it'll be repealed and replaced in a few months? Lunacy!

Care for more shootings in a broad daylight? Don't look now but XLE and OIH are down 3.2% and 4.2% respectively and about a percent to two away from making new 2017 lows. With the way crude has held up, it's perplexing at best and plain out worrisome at worst. I can take a guess why. Look at nat gas. We are sending shitload of it to Mexico. Ain't looking too hot right now with NAFTA about to be scrapped.

This has been a brief interruption of a fantasy dream.

it is starting

Replyhttp://www.zerohedge.com/news/2017-02-22/mexico-prepares-plan-ditch-us-grain-imports-nafta-showdown-looms?utm_source=feedburner&utm_medium=feed&utm_campaign=Feed%3A+zerohedge%2Ffeed+%28zero+hedge+-+on+a+long+enough+timeline%2C+the+survival+rate+for+everyone+drops+to+zero%29

Still think copper goes much lower. It has not traded below 50 dsma since 10/26/16 and is approaching it fast here. Laminate with lower bb on daily and recent low back from 2/3 is at 2.61

ReplyI expect it to break and head lower on waning demand from China and no clear timing on US infrastructure plan. Look out below!

@Nico When you post a URL, you can (almost always) omit the "?" and everything after it - those are parameters most often used for tracking.

ReplyYes, I am hoping for a March rate hike. June would be fine, too. :)

Still not convinced of a Le Pen win (and yes, I thought that Brexit would pass, and yes, I thought, and publicly said so as a comment on this blog, that Trump would win). I might change my mind as developments unfold, but I still think she loses in the second round. One problem is that the "elites" have been crying "wolf!" They told us that if Brexit passed, there would be economic armageddon, and there wasn't. Then they told us that if Trump were elected, there would be economic armageddon, and there wasn't. Well, if Le Pen is elected (and follows through on her plan to take France out of the Euro and repudiate French debt), there WILL be economic armageddon, but I don't know if anyone is still paying attention.

James, very good and insightful article. Thank you.

Reply@Johno - I agree with your view on EURGBP. However, a caution note. Look at the 200-day moving average, it is testing to break below and it has been quite relevant in the past. I would rather wait until becomes a bit more clear.

If the timetable for Trump to fire a change in fiscal policy via the tax channel is thought to be March then Yellen will use it as a tactical gift to raise rates and tighten monetary policy. I'd have thought 25bps rather 50bps more likely ,but a I think a raise in March is as close to a certainty as it gets. She can afford to wait and watch for the effect (or not) of any fiscal change thereafter. I am of course assuming Yellen as some idea of strategy. Passing the baton manoeuvre.

Reply@checkmate yellen is done raising - period. She is too terrified to - in fact at this point the fed may be worried less about inflation (even though there is enough of it) and more about their physical safety from a mob unleashed by Trump at one of his rallies, coz I sure as hell don't see him taking the blame if anything goes wrong.

ReplyAs for her having a 'strategy' - c'mon dude, be serious - this is the same oracle that was running the san francisco fed when foreclosures were spiking in the valley and she was completely oblivious and reporting back in DC that everything was A OK. Her prayer is that trump makes good on the promise of yanking the hot potato from her hands before it starts scalding, which won't change any outcomes but keeps her out of harms way - make sure you pre-order her forthcoming book with the working title 'the courage to do nothing'.

As for the Trumpflation trade I maintain that fits and starts aside, the idea peaked sometime in December 7th and has been running on fumes ever since - its really big tech thats driven spoos subsequently, which has little to do with trumponomics and much more to do with retail index inflows that for obvious reasons are disproportionately skewed towards the top components of NDX. Apparently dentists have subscriptions to Barrons - who knew.

MANU, thanks for your feedback on EURGBP. Yes, probably would have been better to see some more follow-through first, which we certainly didn't get today. I'm still in, but position is on thin ice.

ReplyMnuchin interviews and Trump's Reuters interview later were most important events today, IMO. Two key takeaways for me: 1) some form of border taxation is likelier than I'd thought yesterday and 2) they aren't going to appoint hard-money types to the Fed (but we kind of knew that anyway). That Trump has gone from "too complicated" to "I certainly support a form of tax on the border" seems like news to me, but FX markets yawned. Took off short USD/AXJ positions as I re-assess. If Trump does impose a border tax, anyone care to share their favorite currencies for that scenario?

Anyone still thinking we get no BAT? Sell retailers hard and systematically. Sell retail REITs like crazy too. End of story. You know its coming. They are out there in Mexico putting the fires out. Trump talked to Canadian pretty boy today. XRT is gonna make some noise in the next few weeks. Can it take the whole market down with it? Transports are scared as s#!t. XLY daily outside reversal.

ReplyOh, and no infrastructure plan this year. What a surprise :) Sell materials, XLB is gonna puke. Check out the daily engulfing on it and XLI. This should get pretty interesting fast.

Ipa did you see Nasdaq today. Nvda short term double top. Same with tesla. Expensive stocks have topped ? But financials still strong. Crazy. Meanwhile retail is crazy. L brands guiding down big time. Something not right.

ReplyFor materials Chinese related commodities still making new highs so I am cautious. Insane imo. But not jumping the gun.

To answer you, IPA, I still doubt we're getting BAT or "a form of tax on the border." But I edged up my probability after today. With BAT, I'd imagine there would be one heck of a margin squeeze and shakeout in retail, and in the end the survivors will be the ones who adopt "Amazon Go"-like technology. Trump will hasten the firing of millions and millions of retail jobs, and after the convulsion and possible recession (as middle class real incomes are squeezed by import inflation), the dollar will have adjusted to negate exporters' competitiveness gains. And for what? To pursue some manufacturing job fetish that a guys who never worked in the sector (Bannon and Trump ) have. And the re-shored manufacturing is going to be done by robots anyway. Because it's just moronic and "so stupid only an intellectual could believe them" (as Sen. Cotton said), I thought BAT would surely be stopped by Cohn/Mnuchin/Ross and we'd only see targeted tariffs, but p(wrong) is now higher. Of course, I could probably be wrong about the whole chain of events following BAT. After all, nothing that bad could possibly happen? (paraphrased from my favorite line in the Big Short when someone was asked whether there could be housing crash)

ReplyThere will probably be phase-ins and/or some mess of exemptions to "border taxes." Trump has enough intelligent people in that administration who will object to some tax plan that would send the economy into recession.

On the US stock market, a favorite topic here, I saw a great chart in a DB "Asset Allocation" piece from earlier this month. It's of (cumulative since Dec '09) US fund flows and net equity buybacks. Basically fund flows have been flat all these years while net equity buybacks are a straight line from lower left to upper right. To those who are short the market, Green Day (not especially a fan, but a catchy song) asks "Do You Know Your Enemy?" Buybacks. When do buybacks end? Spike in rates and/or recession. Just keeping the conversation balanced here.

looks like someone was preparing the assassination of Geert Wilders

Replyhttp://www.reuters.com/article/us-netherlands-election-wilders-idUSKBN1611LB

WSJ has a good piece on buybacks: https://www.wsj.com/articles/economy-up-stocks-down-dont-be-surprised-1487684070

ReplyKey points:

1. Factset data shows buybacks declining for several quarters

2. A company now has to spend about $1.34 of its earnings to repurchase as many shares as $1 did in February 2012

My sense is that we don't need to wait for a spike in rates and/or recession. There are enough factors in place already.

thud, I don't have a view on that, yet. Bank research I've read argues for a smaller adjustment in the USD than that theoretically required to keep import prices unchanged. As for speed, who knows. The Reuters article suggests Trump buys the argument that this creates jobs and that he's for border taxes in some form. Markets have dismissed that (Asia was more focused on Mnuchin's comments on China and talk-down of growth expectations/rates), perhaps reflecting the difficulty getting this passed in the Senate. However, let's say it's not part of the tax plan. Trump still has the authority to implement tariffs, although there are limitations on broad across-the-board tariffs as I recall. NY Fed, by the way, was out with research today showing that BAT will raise the prices of everything. But then, does Trump care, or like Michael Gove, has he "had enough of the experts."

ReplyJadot throws support behind Hamon. Melenchon saying he's open to talks with Hamon, but hardly seems genuine. Still seems very unlikely Hamon can make 2nd round. Someone asked recently why German rates are rallying so hard. Zerohedge summarized a Citi report, talking about the required buying by the ECB this year. The other explanation is the market pricing re-domination risk. Where does new DEM trade versus EUR? Let's say +50%. So, you buy scahtz today near -1% and you have a bet that pays 25-to-1 if eurozone breaks up in the next two years. Maybe not ridiculous. I will note however that odds of Le Pen winning *and* gaining a parliamentary majority are seen as extremely low.

Celeraiac1972, thanks for that article. How much the still heavy pace of buybacks can push the market is going to depend on fund flows too, which certainly have NOT been driving this market up. All this said, I'm not advocating getting long the market here. China will slowdown by 2018 and Trump may cause a recession the same year by pursuing Bannon's "economic nationalism."

@Thud - in theory the dollar should track capital flows (i.e. demand for US assets) in the short term and real rate differentials in the long term - the latter is what I would call the fundamental underpinning and the former the flow, or speculative underpinning.

ReplyGiven that background, if a BAT is imposed it could cause re-shoring leading to demand for USD from a capex perspective - but thats not even 25% of the total picture - what would be the impact on inflation? If we are at full employment and productivity stays low then its highly inflationary which keeps real rates down - if there is more automation then it defeats the entire purpose and trump gets treated like a rag doll eventually. Dodd frank unwinds could sharply reduce the demand for treasuries as collateral at banks globally - these repressive requirements have in my opinion been responsible for a full 100 bps underpricing of 10 yr yields relative to fair value. That would have valuation consequences, which would then impact the demand for US assets also.

Thats a very long way of saying no one has a f@#ng clue what the dollar would do, and the assumptions that ryan's crew is making are laughably simple minded - bear in mind there are only 2 places left in the world where capex can actually lead to both higher real growth and higher inflation, and those are India and africa - they both have hosts of other issues. For OECD the only hope for that kind of reflationary growth was skilled high income migration, and the prospects for that don't look that great politically do they?

The way I see it Trump's economic plan (if one can call a series of brain farts a plan) results in stagflation with higher bond yields and whatever else that may imply.

johno, when I am speaking of BAT coming I mean the nasty congressional debate and Ryan proposal of it and not the actual passage. As you can see today, the retail stocks are rebounding on some pushback this morning by Cohn. Do we know that Cohn is speaking on behalf of Trump or just for himself? This is so confusing already and we are not even sure what the whole thing is going to look like. I say longs have to be worried if BAT is DOA then the whole tax reform may be in trouble, especially if Ryan and Trump are at odds and a fight breaks out.

Replyabee, NVDA double top trade was a blessing. A big short publicly covered this morning and it gave the stock a brief relief. I say it goes lower still, last scaleout target is 87. This said, if Naz decides to really fall out of bed one day, there is a juicy gap below @ 68. Half of that gap fill coincides with 200 dsma @ 73.

IPA, I am short NVDA from much lower. Think its too much hype (deep learning etc is for real but most of NVDA's earnings are for gaming still) they have margins and PE that is unreal for a semi. Its more of an intellectual bet for me. Though I should have added at the double top..

Replyyou follow NTAP? along with CSCO they are IMO doomed but for some reason the market wants to pay up for them now

abee, agree about NTAP and CSCO. Datacenter space is very crowded and extremely competitive and they were behind on their product refresh. Supposedly, both are about caught up with what is going on and probably why their stocks are out of the gutter. Cloud storage is going to give NTAP a lot of trouble in the future. CSCO SaaS strategy keeps them going for now, but there are many players that are better and more advanced in the space. I see some future consolidation in that whole part of tech industry, and probably benefiting CSCO more out of the two we are discussing. I have no position in either one.

ReplyWhile buybacks are still the lynchpin to the bull market IMO, I did find the points made in this week's Flows and Liquidity piece by JPM interesting. In a nutshell, retail flows via ETFs have been driving the markets YTD (flows at annualized rate 6x larger than last year). In light of the end-of-day run-ups we've seen in the market, I also found this observation interesting: "Passive funds typically rebalance at the end of the day because transacting at the closing price better aligns the performance of passive funds to the performance of the index they track.... Indeed YTD 37% of the NYSE trading volume took place during the last 30 mins of trading."

ReplyW/r/t long rates, LB will find an excellent commentary that probably fits his view here: https://globalmacrotrading.wordpress.com/

IPA, thanks for the heads up on the Cohn breakfast comment. Wonder whether this just means the White House will have its own version of BAT, but a BAT nevertheless.

IPA, re Csco they just buy shit for saas. They are a dinosaur, imo. Just a matter of time before sdn makes all their expensive switches obsolete. But timing is tough bc it's still seen as a value stock and they are managing to beat. When they start missing it will get fun. I need to stay short otherwise I lose track with the million other things going on in the market. Like Japanese long rates going up and up along with small cap stocks there. Along with India I think those are 2 good equity markets this year, and for a few years still.

ReplyCommodities slowly looking like they are turning but tough to tell. Xle getting hit and big cap miners taking a breather at least. Maybe we need to wait till after China congress.

abee, agree with you, they are a roll-up waiting to blow up. Chambers has been buying shit for pretty much everything new they sold for years. Current CEO will do the same until they swallow something toxic. It does not look like a bad time to sell. The stock is peeking its head above 2007 highs and I think there are massive (I sound like Trump) stops above. When those clear and price suffocates above monthly upper bb and runs into the upper trend line of the channel going back to 2011, the gravity will pull it down to the bottom of the channel. It's gonna hurt ;)

ReplyEven more confusion over BAT.

http://www.investors.com/politics/white-house-opposes-house-gop-border-tax-plan-retailers-rally/

Does not look like Rex got a warm reception south of the border.

http://www.newsweek.com/donald-trump-mexico-border-wall-wall-border-tax-560696

Trump called stock market a "big, fat, ugly bubble" on several occasions in summer/fall of 2016. Now he talks/tweets about Dow records every day (including this morning) and hires an economist who said back in 1999 that it's going to 36K within a few years. What could possibly go wrong?

Replyhttp://www.vox.com/policy-and-politics/2017/2/25/14728622/kevin-hassett-cea-economic-advisers

Crickets...

ReplyWe've discussed this at length here, but things may be picking up in a bad way for lower end shopping malls. JCP announced it will close 140 stores. It's a huge tenant and this will demolish any hope of stabilization.

Also, it looks like the wheels are about to come off the multifamily construction wagon. The conventional bank lending is down big time over the last few months and the developers are now scrambling to find alternative funding for the new projects. Saturation is the main reason. Some guys are saying it's the worst they've seen since 2008. Let's not forget about how important the multifamily construction has been for plugging the hole a single-family downturn created.

Speaking of which, Friday new home sales report was a miss and three previous months were revised lower. Also, anecdotal evidence now strongly suggests that Chinese buyers have completely dried up in California.

AIA architectural billings index contracted in Jan (sub 50). Need a few more down months though in order for the trend to develop. CRE space may be starting to tell us something here. Where are the animal spirits and the anticipation of new infrastructure spending? Could be a combination of higher interest rates, fear over possible loss of tax credits (due to upcoming tax reform), and waning demand. It would be ironic if the sector which president specialized in takes a dive during his tenure.

Back to sleep, fantasy dream...

So, what we know is 1) House's BAT is a hard sell and the White House has its reservations, 2) Trump favors some form of border tax, 3) Mnuchin this morning told Fox News they're looking at a "reciprocity tax." OK, so how do we define reciprocity? There are tariffs and there are VAT tax regimes.

ReplyJPM's Feb 22 Eye of the Market had a great graph plotting tariff applied by the US and tariff applied to the US ("simple average of tariffs on traded goods). The line where the two are equal is the "reciprocity line." Viewed this way, countries like CAD, CLP, ILS, JPY, NOK, EUR, TUR, SGD are on the line or aren't too off-side. RUB, IDR, KRW, COP are modestly off-side. THB, CNY, INR, BRL, ARS are all way off-side. To the extent a country does lots of trade with the US and is more off-side, you'd expect more currency depreciation versus those countries' currencies, no??

If reciprocity taxes account for countries with VAT taxes (with rebates for exports), then Europe (20-ish, both in the eurozone and countries like GBP, NOK, SEK) is coming under the cosh. China too, at 17%. TWD, THB, KRW are moderately off-side with VATs are 5,7, 10%, respectively. JPY is at 8% (consumption tax). MXN has the IVA at 16%.

So, if countries with larger bi-lateral surpluses with the US (as % of the country's GDP) and higher tariffs/VAT taxes are going to have to adjust most, then you can do some ranking. Anyone seen a good analysis along these lines? Anyone think the above approach is too facile and have a better way to look at this?

On a related note, some have said, "It's obvious that Trump wants a weak dollar," and seem to think that settles the matter. There's only so much jawboning Trump can do, and if he realizes this, then his best option may be a "fiscal devaluation" through "reciprocal taxes" that ironically cause nominal appreciation of the dollar. Just a warning to the "Trump equals weak dollar" folks -- you could be right but get killed on dollar shorts.

As for me, I was thinking US trade objectives might be solved in part by nominal appreciation of managed currencies, but last week's comments had me close out that trade, luckily in-the-money. My only dollar short is -USDTRY.

great post johno

Replyand yeah if you want to short USD you might as well long one of the worst destroyed currencies around: TRY. USD might not come down but TRY has a lot to retrace up

Some weeks ago, I pushed back against the long bond thesis, pointing to obvious momentum in the ultra-long end in Japan and Germany. Can't really make that argument any longer. 30Y JGB looks to have broken its trend. Some attributing to the seasonal pickup in lifer's purchases into fiscal year-end. Also, BoJ upped its 10Y+ purchases a bit. I suppose French polls are the ready explanation for the bund breaking its trend.

ReplyAt the time, I also pointed to momentum in US inflation break-evens. While the short-end continues to price higher inflation, it's worth noting that the 5Y 5Y forward break-even rate has also lost momentum. Real rates meanwhile peaked out in December.

What might "reciprocal taxes" mean for rates? Higher break-evens, but lower real rates, IMO. Bannon's "economic nationalism" may work for a developing country (if done right, like Korea did it), but it's probably likelier to make a developed country more like Argentina.

How are your equity shorts looking guys?

ReplyEnjoying your margin calls??? lol

Highest VIX close since 1/19/17. First time VIX 8 dsma crossed over and closed above 50 dsma since 11/16/16.

ReplyHey guys,

ReplyI left a new post with MM and Abee yesterday by email, assume both are busy - can someone (Pol?) get it posted for me while I am in transit today? Like most chart pieces, it is a bit time-sensitive... TVM!

LB

Get it up ;)!

ReplyPosted

Reply.. PTO

Actually would kids of today know what PTO means? never have to do it with an email.

Reply