Just when you thought the reflation trade might be getting a head of steam, equities ran into a tumbling crude market, which itself ran into Saudi oil minister Ali al-Naimi, who suggested that the taps are going to keep running. While prompt WTI and Brent shed roughly a buck and a half, in fairness it probably could have been worse; yesterday's candles don't stand out in any way at all when looking at a chart of the last few months. Still, it's an all-too-familiar story, as an equity rally gets f(oil)ed again.

In any event, the prospect of another W shaped bounce in the SPX has been deferred but not destroyed; if you look closely, during the previous W stocks retreated for a couple of days when first testing the neckline. Per yesterday's post, Macro Man is fairly agnostic on equity beta at current levels, insofar as the SPX is more or less smack dab in the middle of the range. Frankly, he wouldn't be surprised by a 3-5% move in either direction.

One source of legitimate concern is that the nascent recovery in Europe could already be fizzling. Yesterday's ifo survey was little short of execrable, and worryingly confirmed the recent weakness in the PMI. Of the various components, Macro Man has always found the expectations measure to be the most useful in gauging the cycle; suffice to say that the sharp tumble from 102.3 to 98.8 doesn't exactly engender much confidence in the resilience of the German, and by extension European, economy. Gee, it's almost as if conducting a monetary policy that eviscerates the profitability of your banking sector could be detrimental to growth! Who'da thunk it?

The pressure is now squarely on the shoulders of the ECB to rectify what is now widely considered to be a mistake committed at the December meeting. Certainly the weakness of the euro appears to be anticipating such an outcome, but it's unclear what realistic options the ECB has. More QE, perhaps, but with large swathes of high quality Eurozone debt already in negative yield territory, it remains far from certain that a further decline in yields is beneficent. The same holds for the increase in reserves generated by purchasing bonds, given that the ECB immediately starts clawing some of that dough back via the negative depo rate. A program to buy bank debt could certainly soothe financial markets, though it's unclear how much they could buy and how politically palatable it would be to certain segments of the governing council. Macro Man will be on the lookout for any "sources" stories in the run up to the meeting, given that they've been very accurate recently.

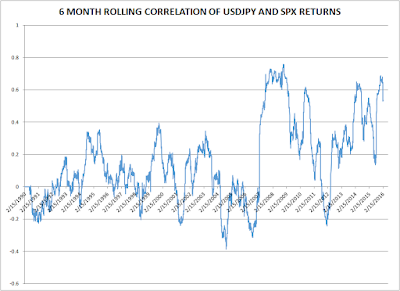

Switching gears, Macro Man thought he would address an issue that's occasionally raised in the comments, vis-a-vis the relationship between equities and the JPY. There has been some suggestion that the ongoing strength of the yen should instigate further weakness in the SPX and other equities, given the apparent strength of the relationship. Macro Man has generally been sceptical of this viewpoint, as it sounds a lot like the tail wagging the dog; while currencies often react to developments in other markets, it's generally more rare (particularly outside of EM) for FX to cause them.

Anyhow, Macro Man figured he might as well run some correlations over a large sample to verify the relationship- or lack thereof. He looked at the 6 month rolling correlation of daily changes in USD/JPY and the SPX, which is a long enough window to iron out noise and give generally meaningful readings. he has to confess at being somewhat surprised by the results, which you can see below:

Holy regime change, Batman! As you can see, from 1990 until the end of 2006 there was only a scant relationship between the yen and the SPX over meaningful periods of time. Sometimes the correlation was positive, sometimes it was negative, but it was never particularly large. That changed at the beginning of 2007, when the relationship became very strong indeed. Some of this may represent the "Quantmageddon" of a number of prominent multi-asset models in the summer of 2007, which resulted in the selling of both equities and yen crosses. Thereafter, of course, we had the crisis, which prompted extreme risk aversion across a broad swathe of asset classes.

How to explain the strength of the correlation since then? To some extent, this surely exemplifies the wretched "risk on/risk off" mindset that dominated many asset markets until a couple of years ago. With most central banks sidelined, there were very few independent thematic opportunities, thus encouraging all markets to trade off of each other. To some extent, the proliferation of algorithmic strategies may have played an important role in this regard; if they are programmed to expect the yen and SPX to move in lockstep they will trade accordingly, at least partially rendering the relationship a self-fulfilling prophecy.

Just when it looked as if the wheels were falling off the relationship in 2012, meanwhile, Abenomics came along and it was "party at Shinzo's house!" for a number of assets. Recently, however, the cops have arrived, busted the party, and confiscated the Asahi kegs and jars of sake. While risk aversion and algo issues persist, it seems reasonable, indeed likely, to Macro Man that the SPX/yen relationship should weaken further as Japanese macro policy becomes less of a hegemonic driver of global sentiment and asset prices.

One final observation is that the strong yen/SPX correlation has emerged at a time when FX carry as a strategy has slunk into the shadows. The reason for this is obvious: with low rates everywhere but the basketest of basket cases, there really isn't any carry to harvest, particularly relative to the level of vol. The Abenomics trade, of course, resembled an FX carry strategy, insofar as the yen has been a cornerstone funder of FX carry for a quarter-century. However, as markets get washed out of that trade, the resemblance should wane.

As an aside, the chart above represents a pretty decent approximation for the performance of your median global macro strategy. While some carry strategies were smarter than others, the fact remains that the returns generated from FX carry trades paid the bills for a lot of other bets, some of which were successful and some of which weren't. In the post-crisis period, not only have there been fewer independent bets to make as noted above, but macro hasn't enjoyed the tailwind of the FX carry return stream.

As an aside, the chart above represents a pretty decent approximation for the performance of your median global macro strategy. While some carry strategies were smarter than others, the fact remains that the returns generated from FX carry trades paid the bills for a lot of other bets, some of which were successful and some of which weren't. In the post-crisis period, not only have there been fewer independent bets to make as noted above, but macro hasn't enjoyed the tailwind of the FX carry return stream.

While it doesn't look like the pomp of FX carry is going to return any time soon, fortunately the last 12-18 months have seen the emergence of a number of more independent opportunities as economic and policy cycles begin to diverge. Who knows: selling that correlation between the SPX and JPY just might be one of them.

In any event, the prospect of another W shaped bounce in the SPX has been deferred but not destroyed; if you look closely, during the previous W stocks retreated for a couple of days when first testing the neckline. Per yesterday's post, Macro Man is fairly agnostic on equity beta at current levels, insofar as the SPX is more or less smack dab in the middle of the range. Frankly, he wouldn't be surprised by a 3-5% move in either direction.

One source of legitimate concern is that the nascent recovery in Europe could already be fizzling. Yesterday's ifo survey was little short of execrable, and worryingly confirmed the recent weakness in the PMI. Of the various components, Macro Man has always found the expectations measure to be the most useful in gauging the cycle; suffice to say that the sharp tumble from 102.3 to 98.8 doesn't exactly engender much confidence in the resilience of the German, and by extension European, economy. Gee, it's almost as if conducting a monetary policy that eviscerates the profitability of your banking sector could be detrimental to growth! Who'da thunk it?

The pressure is now squarely on the shoulders of the ECB to rectify what is now widely considered to be a mistake committed at the December meeting. Certainly the weakness of the euro appears to be anticipating such an outcome, but it's unclear what realistic options the ECB has. More QE, perhaps, but with large swathes of high quality Eurozone debt already in negative yield territory, it remains far from certain that a further decline in yields is beneficent. The same holds for the increase in reserves generated by purchasing bonds, given that the ECB immediately starts clawing some of that dough back via the negative depo rate. A program to buy bank debt could certainly soothe financial markets, though it's unclear how much they could buy and how politically palatable it would be to certain segments of the governing council. Macro Man will be on the lookout for any "sources" stories in the run up to the meeting, given that they've been very accurate recently.

Switching gears, Macro Man thought he would address an issue that's occasionally raised in the comments, vis-a-vis the relationship between equities and the JPY. There has been some suggestion that the ongoing strength of the yen should instigate further weakness in the SPX and other equities, given the apparent strength of the relationship. Macro Man has generally been sceptical of this viewpoint, as it sounds a lot like the tail wagging the dog; while currencies often react to developments in other markets, it's generally more rare (particularly outside of EM) for FX to cause them.

Anyhow, Macro Man figured he might as well run some correlations over a large sample to verify the relationship- or lack thereof. He looked at the 6 month rolling correlation of daily changes in USD/JPY and the SPX, which is a long enough window to iron out noise and give generally meaningful readings. he has to confess at being somewhat surprised by the results, which you can see below:

Holy regime change, Batman! As you can see, from 1990 until the end of 2006 there was only a scant relationship between the yen and the SPX over meaningful periods of time. Sometimes the correlation was positive, sometimes it was negative, but it was never particularly large. That changed at the beginning of 2007, when the relationship became very strong indeed. Some of this may represent the "Quantmageddon" of a number of prominent multi-asset models in the summer of 2007, which resulted in the selling of both equities and yen crosses. Thereafter, of course, we had the crisis, which prompted extreme risk aversion across a broad swathe of asset classes.

How to explain the strength of the correlation since then? To some extent, this surely exemplifies the wretched "risk on/risk off" mindset that dominated many asset markets until a couple of years ago. With most central banks sidelined, there were very few independent thematic opportunities, thus encouraging all markets to trade off of each other. To some extent, the proliferation of algorithmic strategies may have played an important role in this regard; if they are programmed to expect the yen and SPX to move in lockstep they will trade accordingly, at least partially rendering the relationship a self-fulfilling prophecy.

Just when it looked as if the wheels were falling off the relationship in 2012, meanwhile, Abenomics came along and it was "party at Shinzo's house!" for a number of assets. Recently, however, the cops have arrived, busted the party, and confiscated the Asahi kegs and jars of sake. While risk aversion and algo issues persist, it seems reasonable, indeed likely, to Macro Man that the SPX/yen relationship should weaken further as Japanese macro policy becomes less of a hegemonic driver of global sentiment and asset prices.

One final observation is that the strong yen/SPX correlation has emerged at a time when FX carry as a strategy has slunk into the shadows. The reason for this is obvious: with low rates everywhere but the basketest of basket cases, there really isn't any carry to harvest, particularly relative to the level of vol. The Abenomics trade, of course, resembled an FX carry strategy, insofar as the yen has been a cornerstone funder of FX carry for a quarter-century. However, as markets get washed out of that trade, the resemblance should wane.

While it doesn't look like the pomp of FX carry is going to return any time soon, fortunately the last 12-18 months have seen the emergence of a number of more independent opportunities as economic and policy cycles begin to diverge. Who knows: selling that correlation between the SPX and JPY just might be one of them.

59 comments

Click here for commentsexcellent article again. I'm with you in terms of directional outlook. There's just too much information / factors to work through for markets. I think we will lack direction until we get more clarity where we're heading.

ReplyJust out of curiosity. How do I short correlation? Sure I can go long the one, short the other but are there more clever ways to construct it (besides correlation swaps).

I know politics is not to be discussed in general, but wondering of anyone has thoughts on whether a Trump presidency will lead to trade barriers that lead into reciprical action by other countries ... especially since global cbs are trying to chase demand through devals. Dont know USA politics so wonder how much latitude he has in the face of opposition from both sides of the aisle.

ReplyHenner,

ReplyMore vanillas guy, so not my style, but you could enter conditional binary options, ie get xxx payout if both Future SPX < Current Spot AND Future USDJPY > Current Spot, given current correlation is highly positive this negative/no correlation structure should come at a decent discount to the standalone options. I'm sure, however, that someone more clever than I will find a better way!

Anon

"Buy Bank Debt".

ReplyThe Bundesbank would be apoplectic.

3 more QE nails isn't going to help anyone except short term market traders. Economically the zero rate appears to be signalling that it is time for fiscal policy to finish the job of creating trickle up growth for the global economy. Not that I expect ay central banker to have the moral strength to come out and say that nevermind act upon it. Afterall 'turkeys don't vote for xmas'.

Good and interesting article. But can you tell me how I'm going to get rich quickly. ;-)

ReplyIt rather supports a prominent poster's (scepticus) theory of "heat death" for returns on money. That what we've seen up to this point is merely the precursor of what will be the end point for money - no interest (NIRP even) and no zipping around in search for yield. It is not "the end" in any doom laden or deleterious way I should add, just the end point of this particular story. Of course it brings its own challenges but I guess this is the much lauded Keynesian "death of the rentier" (he was referring to interest on money rather than rents). Is this what the Central Banks have indeed been deliberately pursuing? A money supply that is effectively free to bear?

Macro Man, you've inspired me along with Polemic and Lefty,especially Lefty and his reminiscent diatribes of his Oxford days. So here it is , its in another place reading your blog from its new home of,the University of eCONomics. Their going to teach me high order thinking..how's that! that'll be sure to put the fear of god in opposing traders. And how about semester 3 , yep , dummy trading room all Bloomberg'ed up and trading derivatives, their going to train me how to blow things up!..how's that. But don't you worry about that..I haven't spotted a bankster in my new home town since arrival..

ReplyTHAT IS BEAUTIFUL.

What we are seeing in financial markets is a race to the bottom in all currencies vs the USD. The USD is going to go parabolic from here as the ECB, BOJ, PBOC, BOE etc conspire to devalue at the expense of the US. US corporations will see a massive destruction of profits, exacerbated by further commodity carnage (courtesy of USD strength). Expect to see trade wars follow and the collapse of globalization after that. I can't wait.

ReplyMost of what Trump says he will do would be impossible for him to actually do.

ReplyGreat article. Thank you.

ReplyThe strengthening Yen is another sign that risk trends may have topped out and that W might turn out to be a triple top. Although the carry was not much, it may well have been a source of ramping the Nikkei (and Spoos) to a lesser extent. Japanese QE, QQE, GIPF gaffe has been a tailwind for asset markets everywhere, but if they can't increase QE further...we may have seen the best there.

ReplySo it is really up to the Europeans to do a massive QE expansion to give risk markets a chance of reaching new highs. The euro is the new Yen.

Trump: if the main candidates become more polarized as a result, it might be a negative for risk at the margin as it creates more uncertainty. Bloomberg could also run and financial markets might love that.

A parabolic USD: this could happen if the Chinese lose control of their exchange rate peg. After letting the peg fall last August, they had too much capital outflow, so now they have gone back to a stronger USD peg, but new loan data indicates corporates may be trying to flatten out their USD exposure. But it all doesn't matter because it is all owned by the state! It will may end with a peg break at some stage and the PBOC head being fired, like the securities guy being let off recently, for hashing up the stockmarket.

I suspect the Chinese are structurally short USD and they are going to be stuck if the USD appreciates further. A parabolic USD would end with some type of coordinated measure to weaken the USD.

Something that does not make sense to me is if the Chinese SME's are reducing their USD exposure and taking out RMB loans to repay them, the PBOC is keeping the peg/yuan strong, then the fall in FX reserves should be more. In Jan, 800T loans say, 400T in USD loans being repaid, FX reserves should be down more than what it was. The strategic thing to do would be to refinance the majority of USD loans to RMB then let the peg go, but surely the market would cotton onto that before they could pull it off one would think.

Why China Does Not Have a Trade Surplus

ReplySee www. baldngsworld.com

Quite an eye-opener in every respect . Very detailed analysis of China trade and service accounts basically saying that capital is flowing out massively and likely to continue.

It is an interesting article, but does nothing to prove that China does not have a trade surplus. It is quite clear that in the boom times, exports were over-invoiced, thus exaggerating the surplus. These days, if anything, imports are over-invoiced, thus dampening the true level. Indeed, if we look at the 2015 we see that the US reports a larger deficit with China than China reports surplus with the US.

ReplyThe real title of the article should be "capital outflows in China are larger than the trade surplus"...but then we knew that already.

Adrem - thx for the article - agree with MM's conclusion - also, a vast proportion of the kind of fraudulent capital outflow you are talking about tends to get into real estate (swiss banks will only take so much) and not easily traceable US treasuries - if there really is a high probability of trillions that come pouring in this way, the china bears should simultaneously prepare for a massive bubble in real estate and home builders across DM. Capital doesn't just disappear.

ReplyBalding is not the only one calling for actual Chinese GDP to be 0-2% last year, although still in the minority.

ReplyWashed: the Chinese capital outflow has been going into real estate (Canada, Australia, NZ, high end London/ NY/ other major capitals). It is probably most obvious in Vancouver and Sydney which appear inflated still despite the commodity bust. Why else would real estate still be topping out in Toronto when the oil price is down 75%, and real estate in Sydney with iron ore down 70%? The average house price in Auckland (NZ) was $800,000 recently (about $530k USD). Then when you look at Chinese house prices themselves then it becomes even more strange and illogical.

Great piece MM! We now hold our breath in the Eurozone and wait for more QE and the rebound in the survey data, or not!

ReplyAs for China; the trade surplus with the Eurozone is RISING in my view. At least this is what is implied by the bilateral trade data from Eurostat and Germany. Don't know about U.S. trade data.

But the Chinese surplus is indeed key. A capital acc deficit is perfectly normal with a surplus, and you would expect this to open up quickly if they liberalise the flows. But if the trade surplus fades, well ... then the decline in FX reserves suddenly take on a more sinister meaning.

Booger - the subject of your conclusion seems to be that it can't last because its somehow irrational - well, if the trend of well heeled chinese lining up to exchange cash with guys promising them a piece of paradise in wauwatosa WI is accelerating, then why is real estate 'topping out' anytime soon? This so called marginal chinese buyer doesn't seem particularly discriminating to me if the desperate picture painted by many is true.

ReplyJust making the point that we can't have it both ways, and capital rotation/migration is not the same thing as sticking it under the mattress.

Washed: it can't last because it is running out of steam. The Chinese economy is slowing, and just as there are fewer Russian oligarchs buying high end London real estate now with oil where it is now, one suspects there will be fewer well to do Chinese buying in the other places mentioned, with the Chinese economy stalling. Particularly if capital controls intensify.

ReplyMy statement that Chinese house prices themselves are strange and illogical was reference to the cost of housing there (relative to income), the fact that the majority of the housing stock is unproductive and unused/unrented and deteriorating. It is pretty weird when you think about it, that Chinese wealth is accumulated largely by buying unused property that no one lives in and which deteriorates over time. That this has gone up so much in the last 20 years that the after effects of this bubble inflate and affect other cities is pretty amazing too.

But without the Chinese buyer effect, property would be lower in the commodity countries, interest rates would be lower, and their currencies would be lower.

10,000 Yen notes now 92 percent of all yen notes

Replyhttp://imgur.com/FmfxOyI

A poorly received investor day at JPM is leading financials lower...

ReplyMarkit SERVICES PMI just came in sub 50..

I thought I was going to have some time to short... maybe not. Looking for Notes to close over 132 or SPX below the 20 day .. which we are at right now... bah

Booger:

Reply1)The Chinese economy slowing is exogenous to capital flight - the very idea behind the latter is that it should be exacerbated, not reduced, by a slowing economy.

2) If capital controls are forced (or rather, re-inforced), it will arguably slow the economy further even if accompanied by much lower RRs, but then yuan devaluation is out the window.

I've been saying the china prognosticators seem to want everything at once - ignore the destination of the capital, argue that the economy is completely off the rails, and want devaluation all the same time.

China will lock up capital and the people who send it out before any of the so called 'market' outcomes happen - its that simple. Ultimately the US and China will drift apart and the last outcome from that on everyone's mind should be structural deflation.

Same as yesterday: $DB, oil $USDJPY all red.

ReplyCan't look at $GS, $JPM, $DB without thinking something larger is going on.

Steen: Why March could get nasty for risk on

ReplyA stronger USD would translate to risk off in every single asset class

USD strength will kill commodity stability, lower investment and reduce US earnings

Uncertainty is the market's worst enemy and there's a bucket load coming our way

The ECB and EU mirror Japan's failed policies and are not tackling the real problem

https://www.tradingfloor.com/posts/why-march-could-get-nasty-for-risk-on-7164348

@hotairmail: Not sure how prominent here but increasingly believe he's right about the secular story - should have kept his blog. Absent the CB intent though; rentier influence won't subside gracefully, but it will nonetheless.

Reply-Just the type of market to catch you wrong-footed..

ReplyThe Saudis, as I understand it, make money on oil at 6 dollars a barrel...why wouldn't they BK the shalers?

This JBTFD stuff is harder than advertised.....

ReplyCentral banks buy oil on DOE to save esx from the gap. You're all jerks.

ReplyAt least that's what i'd say if i was jbtfd! /joke

Weidmann comments were interesting today. Is he turning? Is something big coming? I fear for the price action on ECB if it's viewed negatively again.

I prefer cointegration to correlation myself.

As a perennial TWINEr, LB is fading the latest spike lower in US 10y rates, which was surely driven more by machines than by rational trading humans. Should the world not in fact end in the morning (and this would not be the first time the world has failed to end, we would observe), a few nervous punters and machines might sell some govies and buy some spoos, and we suspect a lot more of that is in the offing, with crude oil apparently hanging on to the $30 level for the time being.

ReplyA lot of discussion on China.

ReplyRegarding real estate buying:

1) Not every Canada city has a real estate boom due to Chinese buying, i.e. Ottawa now is in a housing downturn. For the few cities that seems to have housing price rising forever, we should consider restrains on housing supply because of local zoning regulations. When you have limited supply and a large demand (even when the demand growth may be slowing), the impact to push up price could be huge and lasting.

2) Housing markets in China is unbalanced, in the first tier cities, you actually see housing price rising, just like London's real estates being used to park capital, Shanghai and Beijing's properties are likely to be in demand for a long time. But smaller cities are already in housing busts, no doubt about it.

3) Many people are ignoring China's capital outflow shown in the M&A. So many deals have been announced recently and billions of USD are used to purchase shares of foreign companies. Notice this, most of these M&As must have been blessed by the government otherwise they cannot move forward in the first place. These capital outflow far outpaced any wealthy Chinese buying an apartment in Vancouver. These actions showed me two things: a) RMB will devaluate further and these SMEs are taking advantage of the short time windows to spend money and it is cheaper for them; b) the government so far is not panic because they still allow those USD to be used for shopping around.

4) The affordability of Chinese housing regarding the housing price to income ratio. Well, regular Chinese can own houses because they own the initial dwelling apartments at the time the housing market is set free. So they bought their own houses 20 years ago for $100k, and now worth $1 million. When they buy new houses, they simply sell the old one to get down payment and thus their mortgage is manageable. Those young people who just move to Beijing or Shanghai then are ones without any hope to buy an apartment and become long time renters, not that different from NYC.

Insults = ejection

ReplyKindly piss off.

ReplyAnyone notice WTI future slope is getting extremely more steeper? one would think that implies oil is so stretched that a short-term rebound is nearby. but apparently saudi's petro minister has insisted fighting the war to eliminate US producers...Wonder how much damage will spread from the oil industry to banks and others

ReplyFrom the Federal Reserve: Wed, February, 24, 2016

ReplyDue to technical difficulties, the Wed, February, 24, 2016 (11:15 – 11:45am) agency MBS outright operation was cancelled. The operation will be rescheduled for a later time.

- Stocks and Oil immediately ramp.

LB,

ReplySo there is no scenario where I wake up a week from now (TWINE) and bond yields are lower? If TWINE, then rates must be higher? Why?

anon 4:34 indeed the M&A side of the China story has been conveniently glossed over by many - why? Because it doesn't quite fit neatly into the apocalyptic scenarios predicted by many - plus there is a more mundane reason - this stuff has been making fewer splashes because the moolah has been collected by local investment banks as opposed to the wall street boys.

Replyhttp://www.pressreader.com/belgium/the-wall-street-journal-europe/20160222/282222304824317/TextView

anyway - I maintain (sigh) china will be a long drawn out whimper and not a bang.

AB - look forward to LB's response to your question, but I'm curious, why do you feel bullish bonds at these levels?

Any views on Brexit? I think EU will worse off than the UK despite most papers focusing on deterioration of UK trade position and mkt access to EU and RoW.

ReplyCable seems is oversold and it's still a long way from the June referendum. Can anyone envision cable at 1.0000?

Views on Brexit? UK will not Brexit, so Brexit price moves can be faded. Timing, as ever, is the key.

ReplyAB - on rates, I hear you. Here is my take, its all Global. Bunds are slowly back near lows at 0.15, JGB's now negative again. There is obviously going to be pressure on US rates as well.

ReplyNotes bid up on the services PMI then faked out with Spoos on oil inventories before reversing (a classic algo type of trade). But not sure if anyone will want to be long when ISM services comes out next week Thursday.

Algos are RAMPING US equities... reversing an entire day's downtrend in 2 hrs.

ReplyCENTRAL BANKS WILL NOT ALLOW EQUITIES TO FALL. PERIOD. US data today was abysmal, oil data shows too much supply, and yet we have a huge ramp in oil and equities. Or you can choose not to believe this is happening and sit there losing money or making substandard returns while those buying the dips make double digit gains.

Jbtfd .. agree nice rally but us peanut throwing morons want to know when you sell to leave yourself room to buy these dips in your crammed full portfolio. You views on when to sell between your when to buy comments would be most welcome.

ReplyGuy who lives cross the street from me is a coder works for AQR they have 280 billion AUM all algos 500 coders work there

ReplyPolemic as you say, I'm obviously not listing entries and exits in any posts (I haven't seen anyone here who does). I'm merely stating over-and-over that EVERY dip in US equity indexes will result in higher prices within a few weeks. We are seeing 1-2% daily moves in equities, and 3-6% in crude. I know people don't like it that JBTFD always wins, but it does.

ReplyIf it always wins, why is oil, the SPX etc closer to the lows of the last year than the highs?

ReplyWell to be honest Nico, your antithesis, does a pretty good job of showing both sides even if he does have a bearish tendency.

Replynow onto other things..

ReplyGBP- the shock with which everyone was shocked at the not at all shocking news that BREXIT would be a close run thing appears to have caused a kitchen inking of all possible reasons to sell GBP being chucked at the current Brexit inspired move lower. Seeing DB and their ilk now citing debt overload and diminishing current account balances due to FDI seizure smacks of 'chase the dragon' muck chucking or ( now I ll put on my jbtfd conspiracy tin foil beeny here) a deliberate besmirching of the mighty pound for Euro political reasons. Smash it hard and show the british what even the threat of leaving EU will do to their markets.. right I'll take the beeny off now.

But this kitchen sinking and sudden OMG from distant shore traders does have me thinking that maybe phase one of Pound crushing' may be over soon and LB's Mr Shorty may get a partial insertion of an 'Edward the Second'ing.

Bak in the old days before altos took over your decent honest and ahem truthful cable trader only knew two positions to hold. Short and VERY short. So I can assume there ar some old lags out there finally going toldja so. But when that happens you normally want to buy it.

Other odd thing is how the press are suddenly riffing everything to cable not EUR/GBP when the later is the one that we should really be watching. Of course it isn't really that odd. Cable is performing not since the [insert last time] with new levels whereas EURGBP is only really where it was not that long ago so effectively not a headline story.

It is amusing how not that long ago everyone was decrying the EU and ECB for being complete muppets when it came to handling crises and how EU was doomed, yet now, have one of the more stable entities threaten to leave and whooo . EU is the strong battleship and sanctuary that you would be mad to desert. Not that I m declaring a hand either way , but the narrative doesn't half swing with perspective.

Pol

Macroman I am not buying the dip in oil. (Currencies & commodities do not trade freely in these days of central bank interference, so I do not trade them). And my bias is to US equity indexes (I think EZ is a mess). We will always see corrections of 5-10%, as I previously stated these are buying opportunities. Spoos will reverse the Jan 2016 fall just as it did after Aug 2015. In every correction since 2009 people have said that the end of the world was nigh, instead equities just recovered and pushed to new highs. The same will happen here.

ReplyAll about positioning, pol, all about positioning. The one to watch is GBPCAD - if crude even half rallies here that one could be quite the toilet flush given the way people have been leaning.

ReplyTrading views on the cable aside, it would be nice to visit london from the US in the future and not feel completely destitute!

Washed .. I d always buy you a drink anyway if you did.

ReplyAnon 7.40 . I m sort of hoping that 500 coders just got shafted in that reversal.

Polemic - I entirely agree with everything you said above re sterling and government manipulation. I would also add that the UK govt and BoE will be delighted that sterling is falling so heavily...

ReplyAs an aside, all US indexes are now magically green on the day. The bad news and horrendous price action of the past 2 days is vanished within a couple of hours. Imagine what will happen when we actually get good news and data...

@jbtfd: if your thesis would be right, why does it work for spoos and FED, only CB that's not printing anymore...what's different for ECB and BOJ? NIRP vs PIRP (positive interest rate policy) :)?

ReplyThanks Pol for your insight on GBP.

ReplyI would like to bet on GBPAUD for now as AUD was the strongest currency in the past few days and the reward/risk of a reversal is tempting.

JBTFD told :Macroman I am not buying the dip in oil. (Currencies & commodities do not trade freely in these days of central bank interference, so I do not trade them).

ReplyHonestly i would call a 120 to 30 price downside something more than a dip :)

Currencies and commodities trade freely, much more than bonds...!

But according to you it's not so due to CBs interference (what's their frequency?), but you trade spoos due to the same interference???

i notice some confusion...

TheBondStrategist, allow me to explain/clarify:

Reply- I mean I do not buy dips in oil on a day-to-day basis. But yes I agree the collapse from 120 to 30 is more than a "dip".

- I agree the bond market is also a mess as a result of QE/ZIRP.

- My issue with 'interference' is the type of manipulation: the Fed would like to see the USD trade lower, the ECB would like to see the Euro trade lower, the BOJ would like the Yen lower yet they can't all succeed; that is not easy to trade. Now, the Fed, ECB and BOJ would all like equity indexes higher. This can succeed and is easier to trade. Is that more clear?

ok, it makes some sense... like "stocks in the long period always grow" and "in the long run we are all dead"

Replyhttp://www.economist.com/blogs/buttonwood/2016/01/investing

but with some caveat

PMI services flash...indicating trouble ahead?

Replyhttps://twitter.com/CiovaccoCapital/status/702544850412032001/photo/1

Tom McLellan

Reply"The robust rally in mid-February 2016 has pushed the TICK’s 10MA up to its highest reading since late 2014. The message is that traders were a bit too eager in chasing that countertrend rally, and so the stage is set for the next leg down."

http://www.financialsense.com/contributors/tom-mcclelan/tick-indicator-suggests-downturn

i'm not one for conspiracy theories but when you see the price action in today's equity indexes it makes you wonder...

ReplyCounter trend rallies in the initial stages of a market regime change ( bull to bear ) are very hard to distinguish from genuine turns that last longer. You can only know after a period of time. Welcome to the current world. Place your bets carefully.

ReplyBeaten down value in some parts of the market is outperforming in other areas it's not. By now all the brokers have put out their research saying financials are cheap. So it's an easy sector to watch for confirmation. I'm also keying in on transports here, which have been an early outperformer over the past month. Eu and Japan should also be watched but for now they seem to only follow on the upside and lead to the downside. Wait for them to make new lows, imo, otherwise stay away.

Equities feel bid so far.